Storm waves over the Lighthouse, Portugal - enhanced sky

Major Asset Classes

August 2022

Performance Comparison

Introduction

August returns have been finalized and confirm the end of the summer rally. Losses were evident across all major asset classes. For example, US equity indexes were down and fared better than developing market indices, but trailed the performance of emerging market indices. Meanwhile, US government and high yield corporate bonds had losses that exceeded those in US equities. In comparison, emerging market debt proved more durable. Finally, the US Dollar continued to rise in response to rising interest rates, but failed to mitigate gains across commodities.

The following analysis provides a visual record of August returns and is intended to help investor’s to benchmark their portfolio performance.

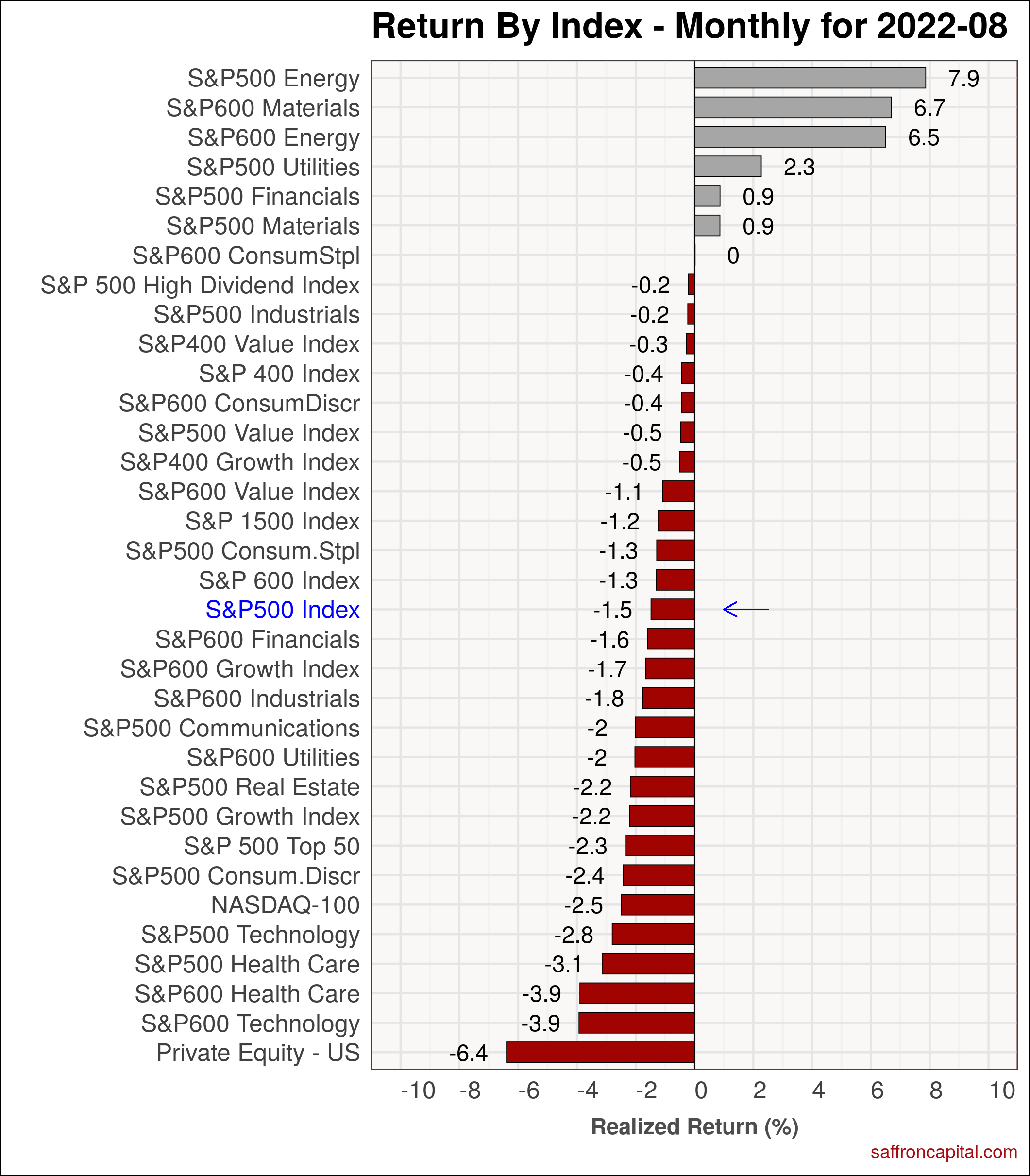

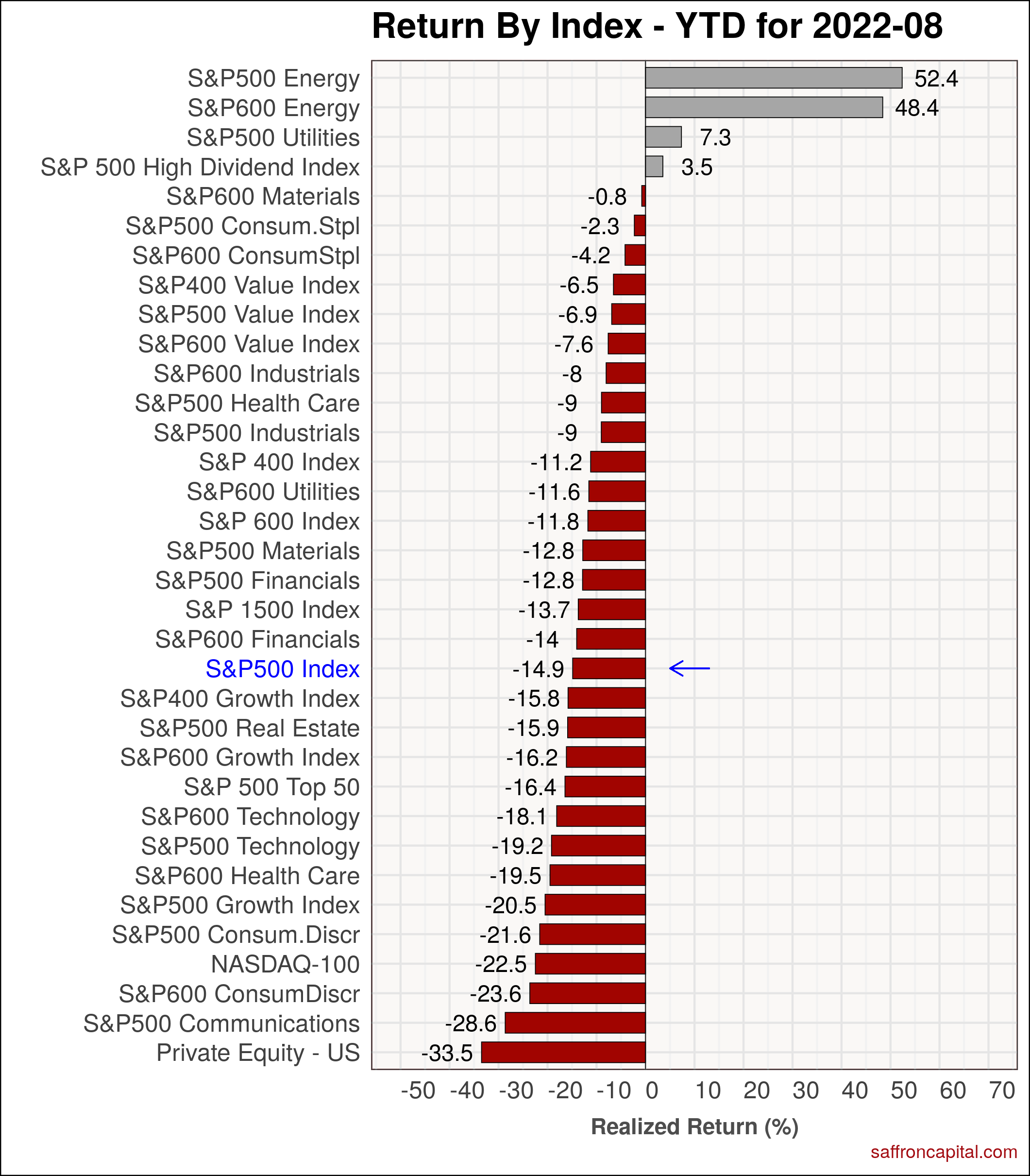

US Equities

August losses for the large cap S&P 500 index (-1.5%) were pulled down by Healthcare (-3.1%), Technology (-2.8%) and Consumer Discretionary (-2.4%) shares. By extension, Growth (-2.2%) trailed Value *-0.5%) stocks. Top performers were large cap energy (+7.9%), small cap Materials (+6.7%) and small cap Energy (+6.5%). Utilities (+2.3%) also did well. On a year-to-date (YTD) basis, the S&P 500 index (-14.9%) continues to outperform strategic sectors, including Communications (-28.6%), Technology (-19.2%), and Real Estate (-15.9%) sectors. The top performers since January are large cap energy (+52..4%), small cap Energy (+48.4%), large cap Utilities (+7.3%), and high dividend stocks (+3.5%).

Click to enlarge

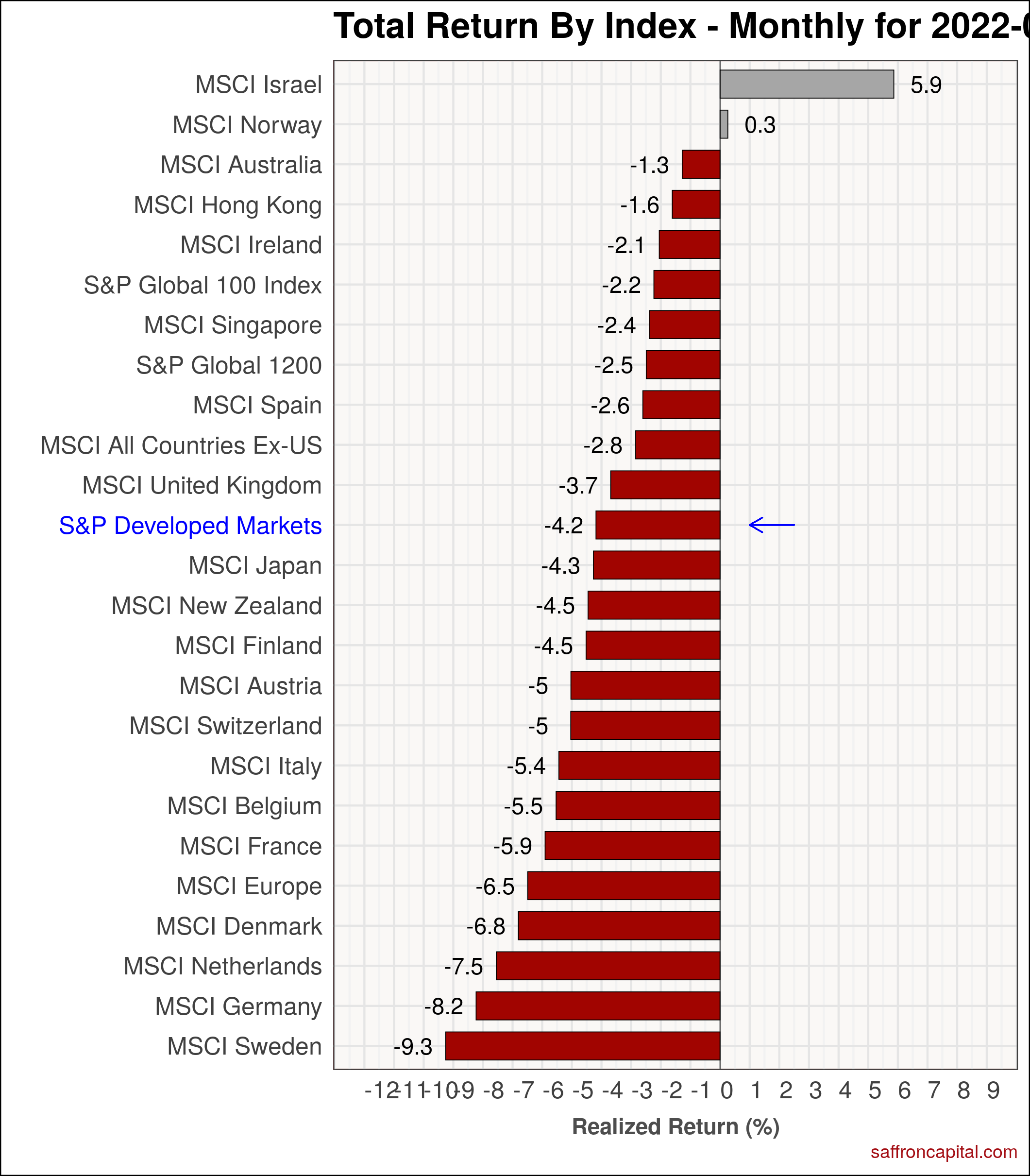

Developed Market Equities

Elsewhere, developed market equities were hard hit. Specifically, the S&P Developed Markets index (-4.2%) lagged the S&P 500 index by 270 bps in August. Markets in Israel (+5.9%) and Norway (+0.3%) both topped the leaders list for the second month straight. In contrast. Sweden (-9.3%), Germany (-8.2%), and the Netherlands (-7.5%) had the most negative. returns. On a year to date basis, the S&P Developed Markets index (-18.1%) trails US equities and every developed market had negative returns.

Click to enlarge

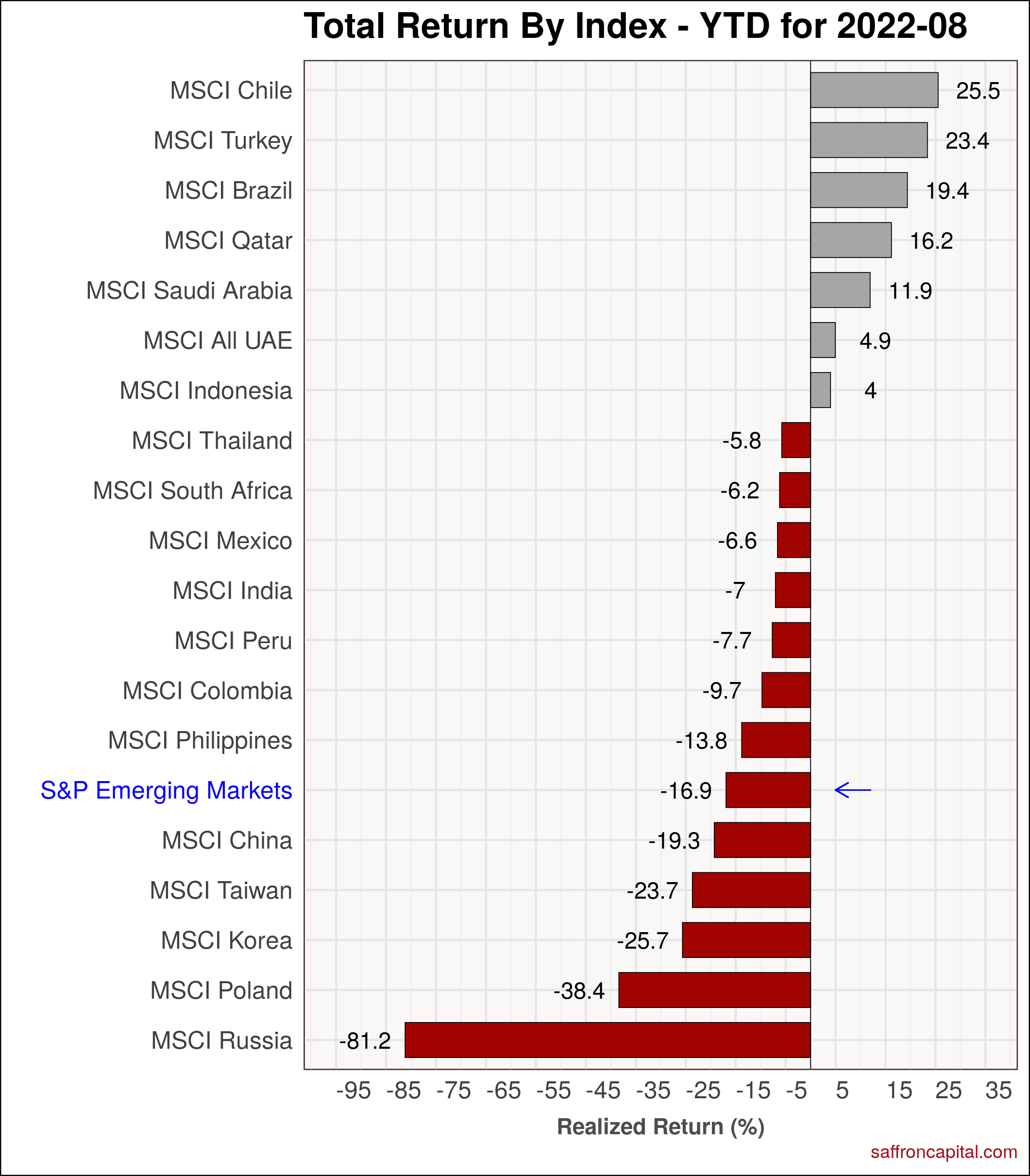

Emerging Market Equities

The S&P Emerging Markets Index (+1.0%) was just one of the bright spots in August. The strongest stock markets were in Turkey (+13.5%), Brazil (+11.6%) and Chile (+5.5%). Poland (-11.6%). the monthly outlier. Meanwhile, shares in China (+2.6%) beat returns on shares in India (-0.9%). On a year to date basis, the S&P Emerging Market index (-16.9%) remains down, and is led by resource rich economies. .

Click to enlarge

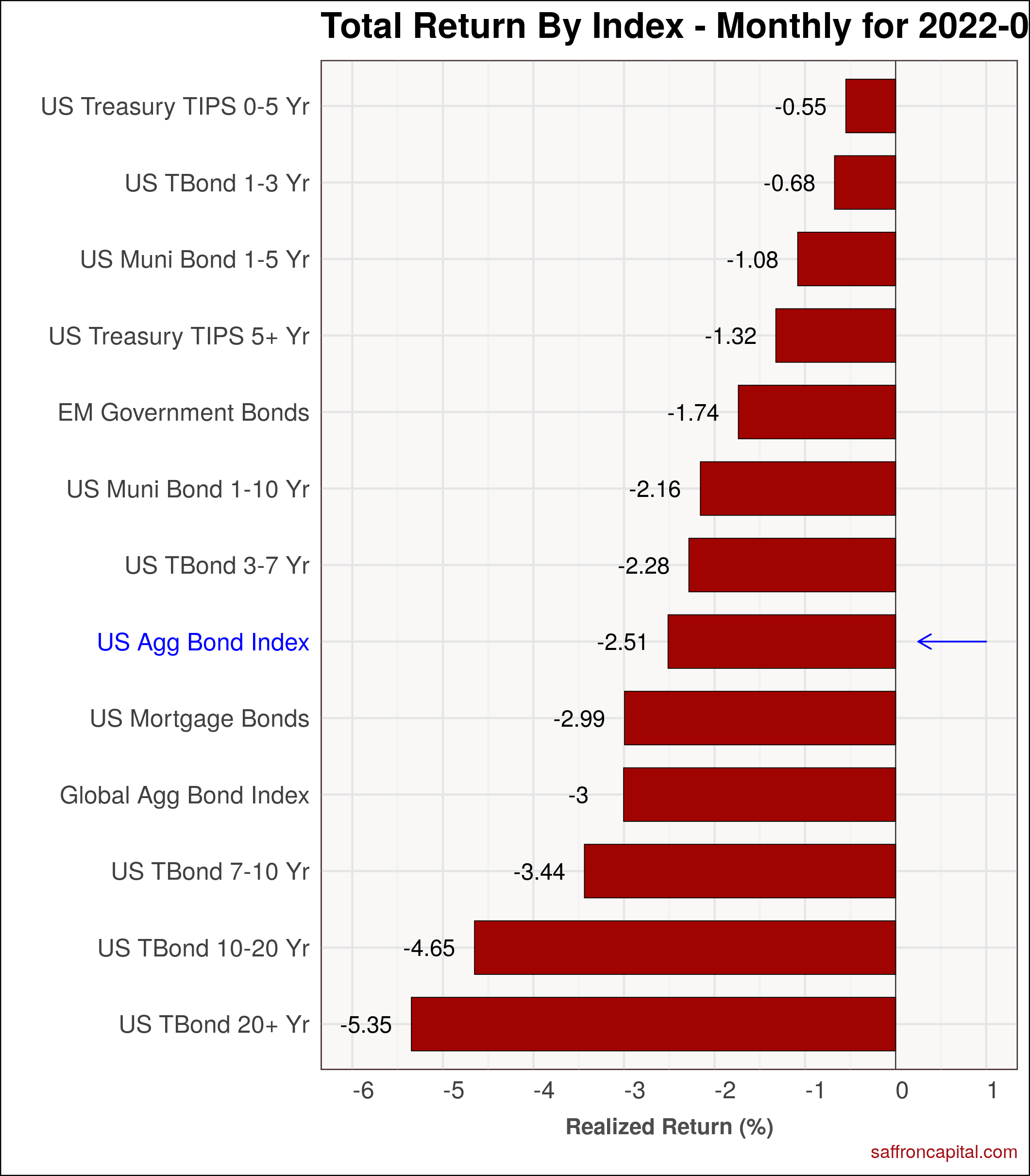

Government Bonds

July returns across the government bond markets were negative as Fed policy reasserted itself. Meanwhile, open interest data now confirms that hedge funds have their largest short yield curve position in over 40 years. The US Aggregate Bond Index (-2.51%) fell more than US equities in August, but outperformed the Global Aggregate Bond index (-3.0%). Sovereign bonds for emerging market countries (-1.74%) performed better. And as inflation continued to rise, inflation protected bonds (-0.5% to -1.32%) also fell. On a year-to-date basis, the US aggregate Bond index (-9.88%) is having one of its worse years ever and is being pulled down by long duration US treasuries (-22.44%) and Emerging market (-18.65%) government bonds.

Click to enlarge

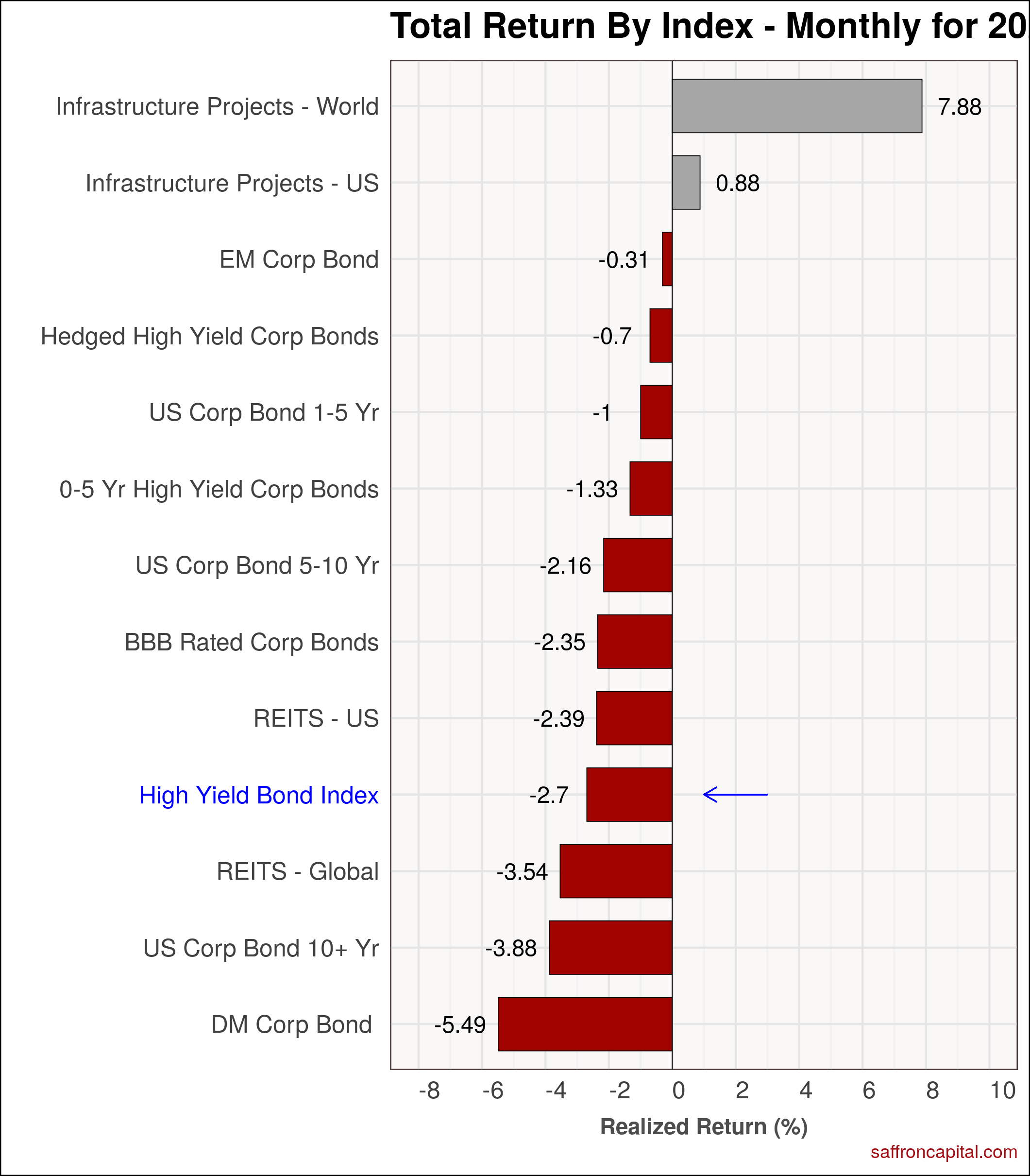

Corporate & Infrastructure Bonds

The High Yield Bond Index (-2.7%) was subject to heavy selling at the end of August. The best performers were infrastructure project bonds, both international (+7.88%) and domestic (+0.88%). Emerging market corporate debt (-0.31%) was also strong. Since January, the High Yield index (-10.44%) has outperformed equities. International infrastructure project bonds (+8.04%) remain the one bright spot in the asset class. However, red ink remains noticeable with Developed market corporate bonds (-21.7%) showing the largest losses.

Click to enlarge

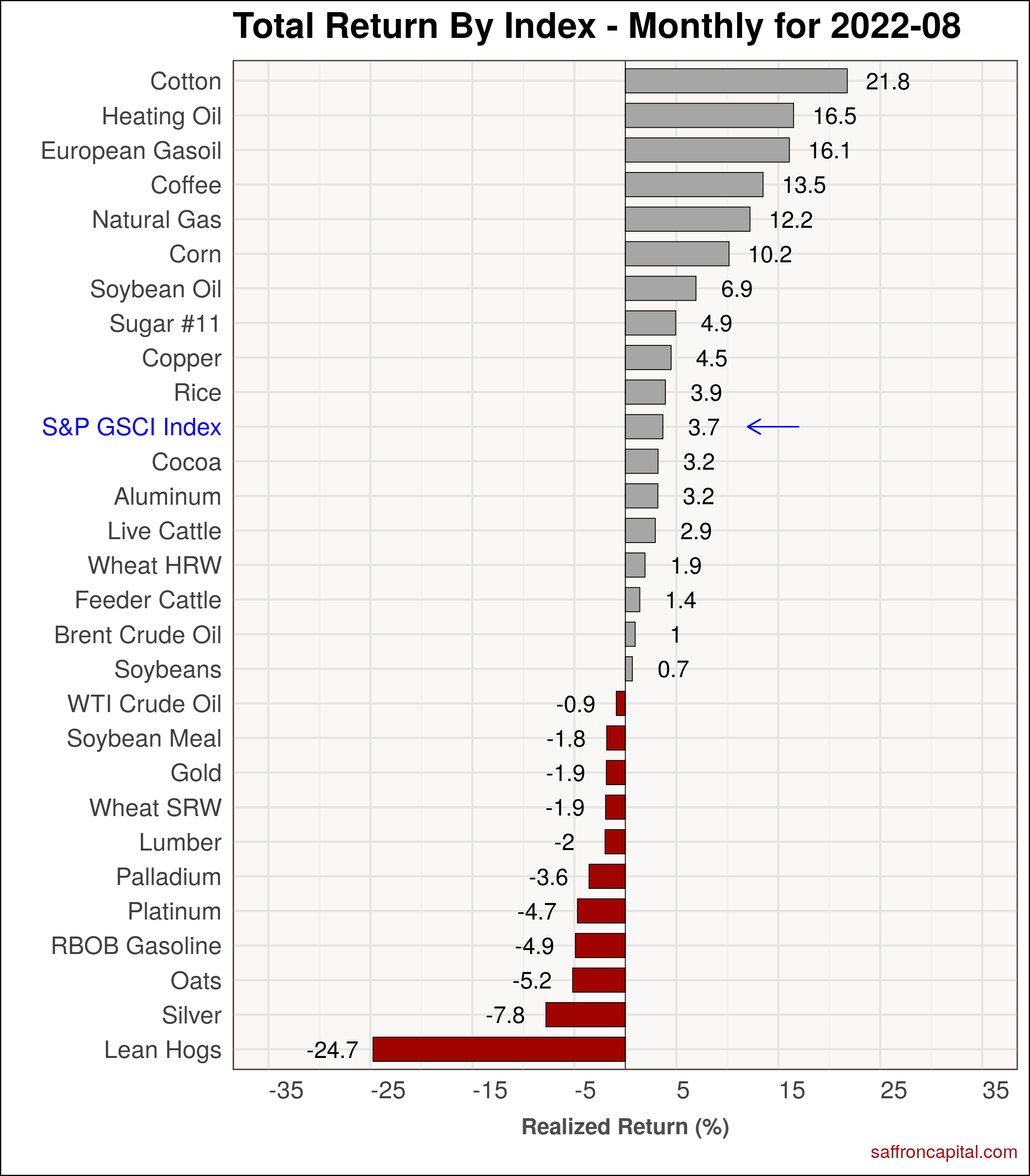

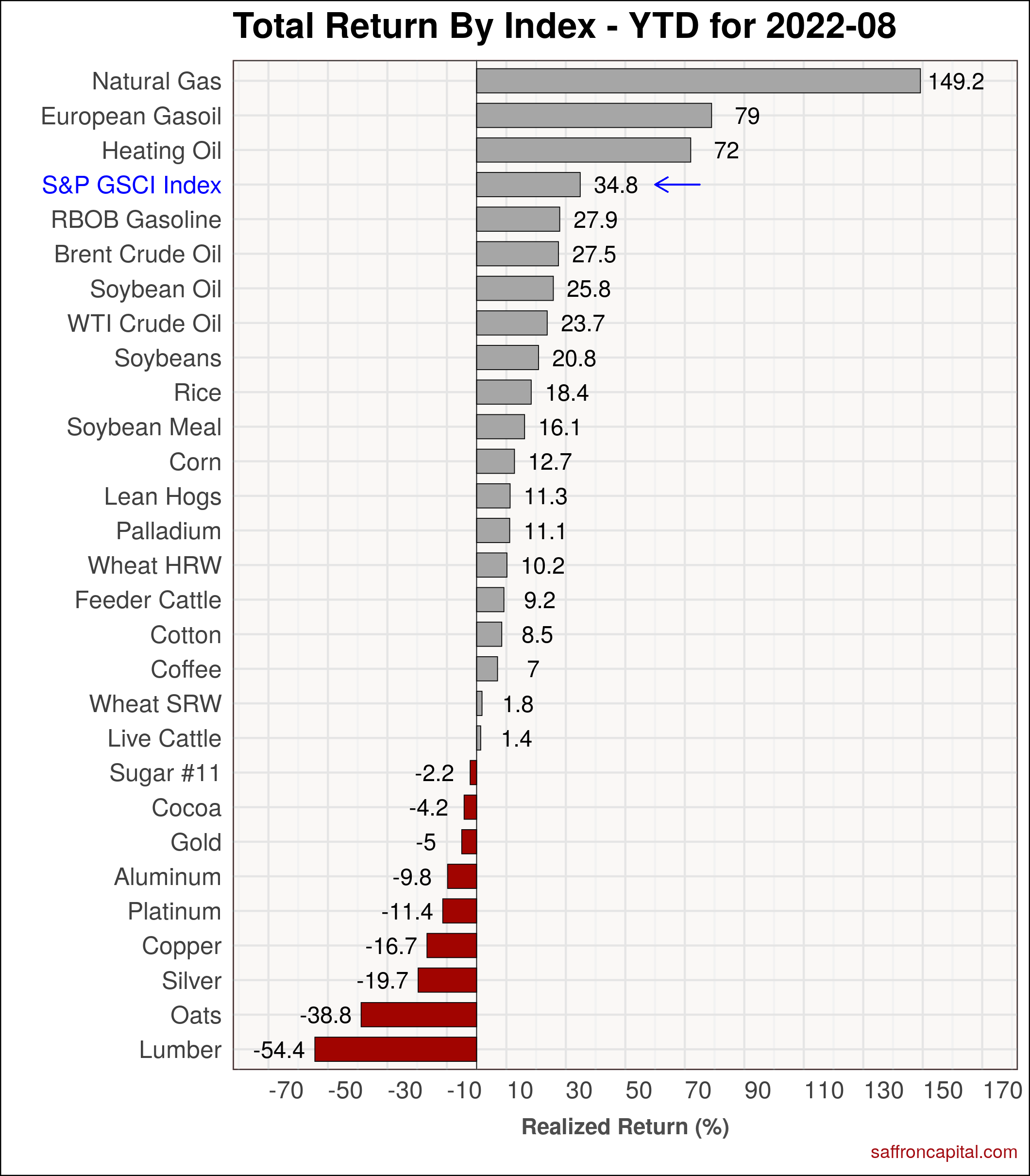

Commodities

August returns for commodities, as measured by the S&P GSCI index (+3.7%), remained strong. Climate sensitive crops and energy again top the list. For example, the US cotton crop (+21.8%) is struggling with dry soil in West Texas and prices were locked limit up for two days at months end. Meanwhile, US and European distillate prices (+16.5% and 16.1%, respectively) have ramped up given strong jet demand and reduced water flows on the Rhine river. Year to date, the S&P GSCI Index (+34.8%) is leading all asset classes. natural gas (+149.2%), European Gasoil (+79.0%) and Heating oil (+72%) have outperformed all other commodities.

Click to enlarge

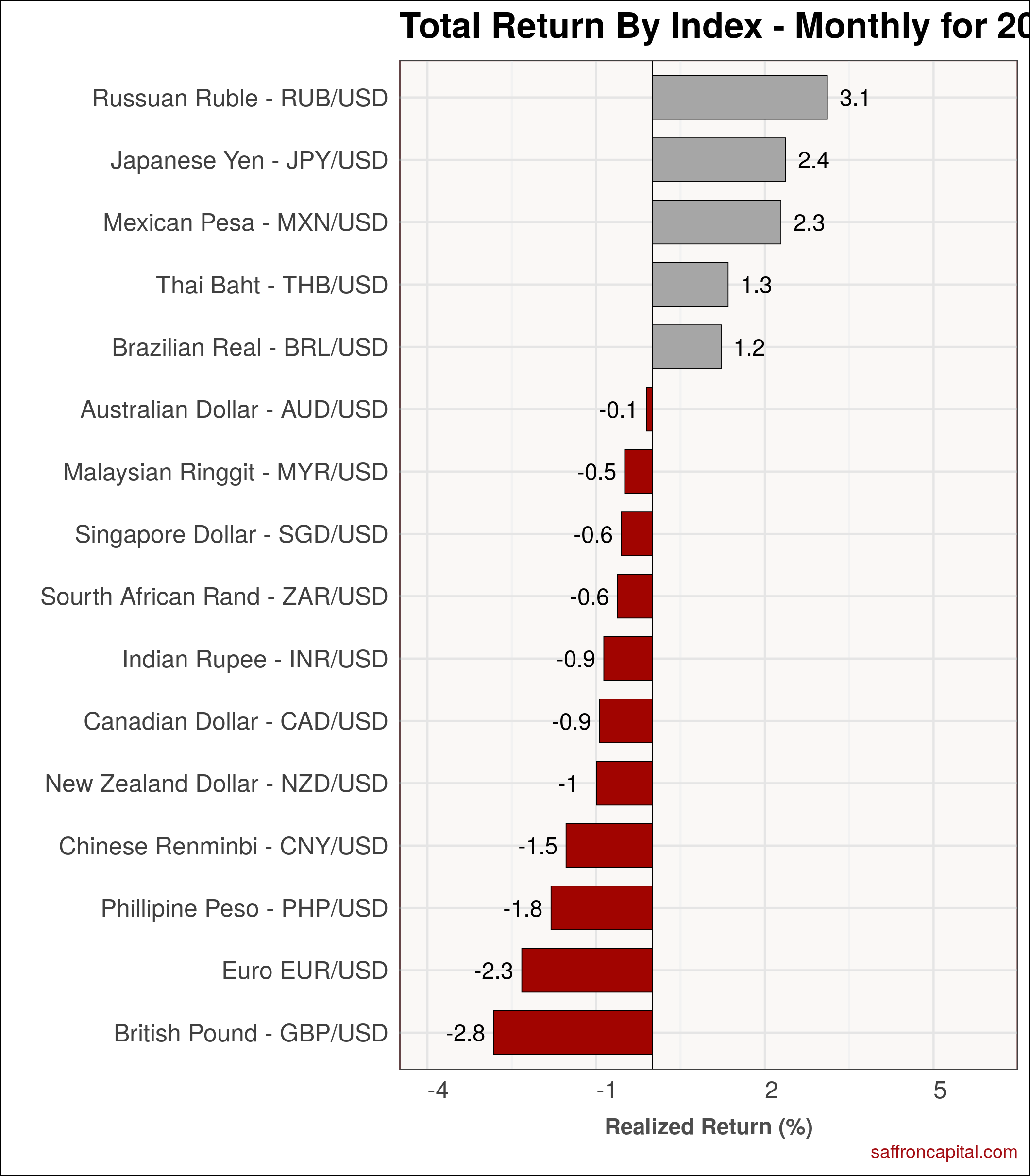

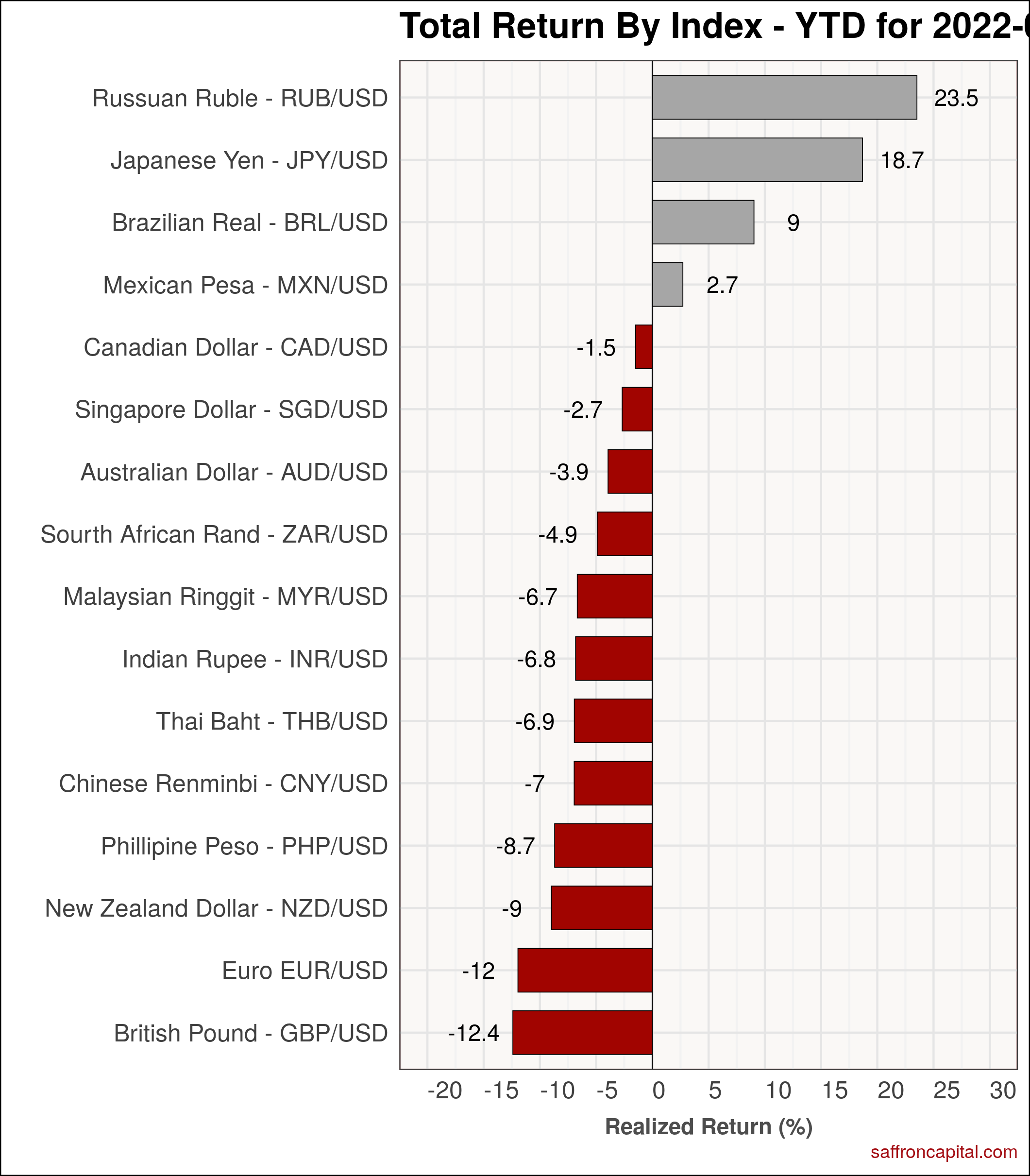

Currencies

The US Dollar (+3.3%) rose in August and remained the strongest of all the primary currencies, trailed only by the Russia ruble (+3.1%). The Japanese Yen (+2.4%) was also strong, while the Chinese Renminbi (-1.5%) continued to weaken. The weakest currency pairs in August were the British pound (-2.8%) and the Euro (-2.3%). Since January, the US Dollar (13.0%) has been strong, but is now out performed by the Ruble (+23.5%) and the Yen (+18.7%).

Click to enlarge

Have questions about the performance and investment plan for your portfolio? Schedule a call or meeting with us here.

{kind=link}

{kind=link}

{kind=link}