August Returns – The Best and Worse Performing Assets

Introduction

August returns proved to be exciting in both financial and commodity markets. Corporate equities and high-yield debt both proved to be solid performers . This was evident in the US, developed markets (DM) and emerging markets (EM). The month also saw wide swings in commodities, with oil loosing ground for the first month since March. Otherwise ,it was pretty subdued for government bonds and major currency pairs saw little movement.

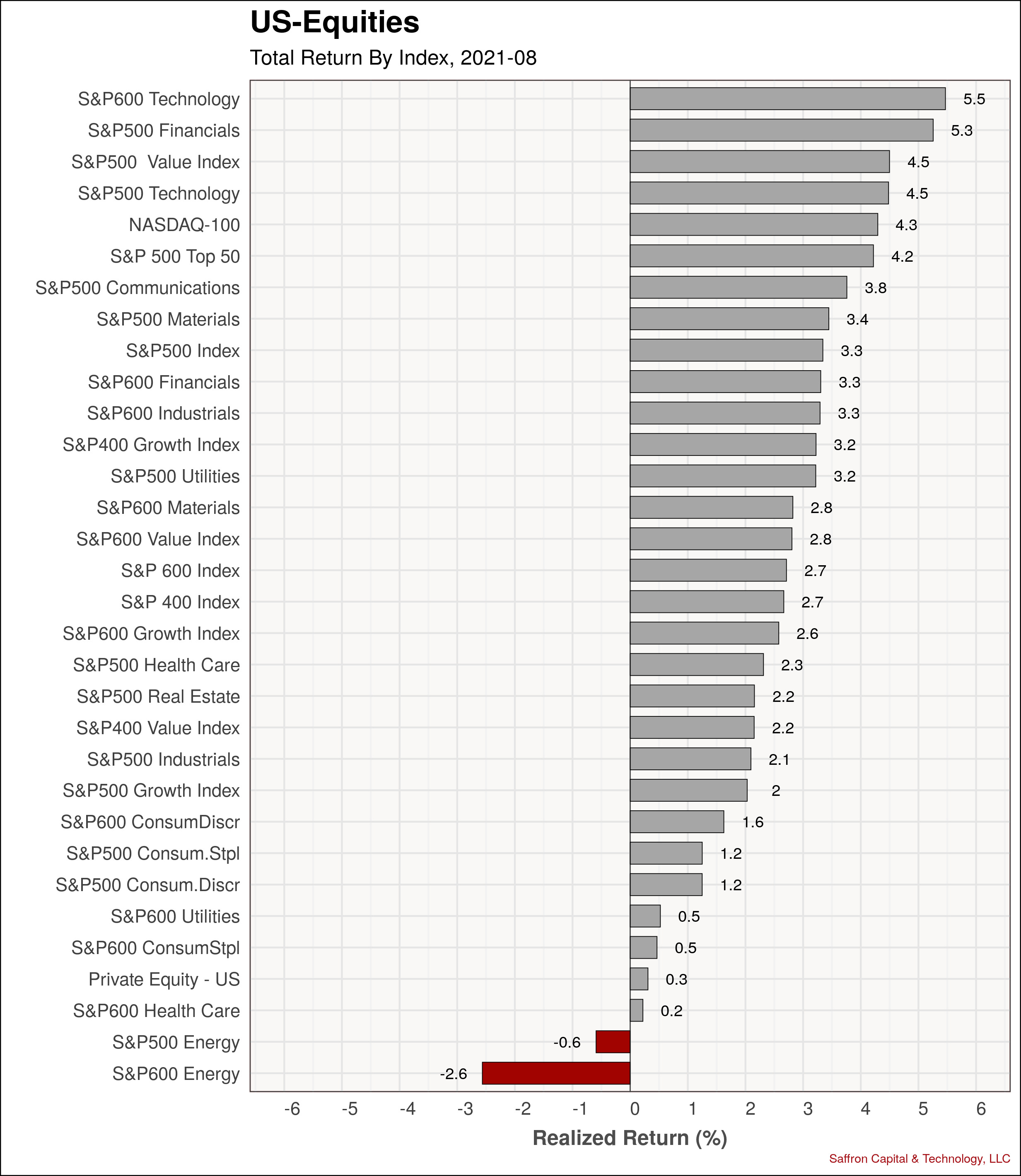

US-Equities

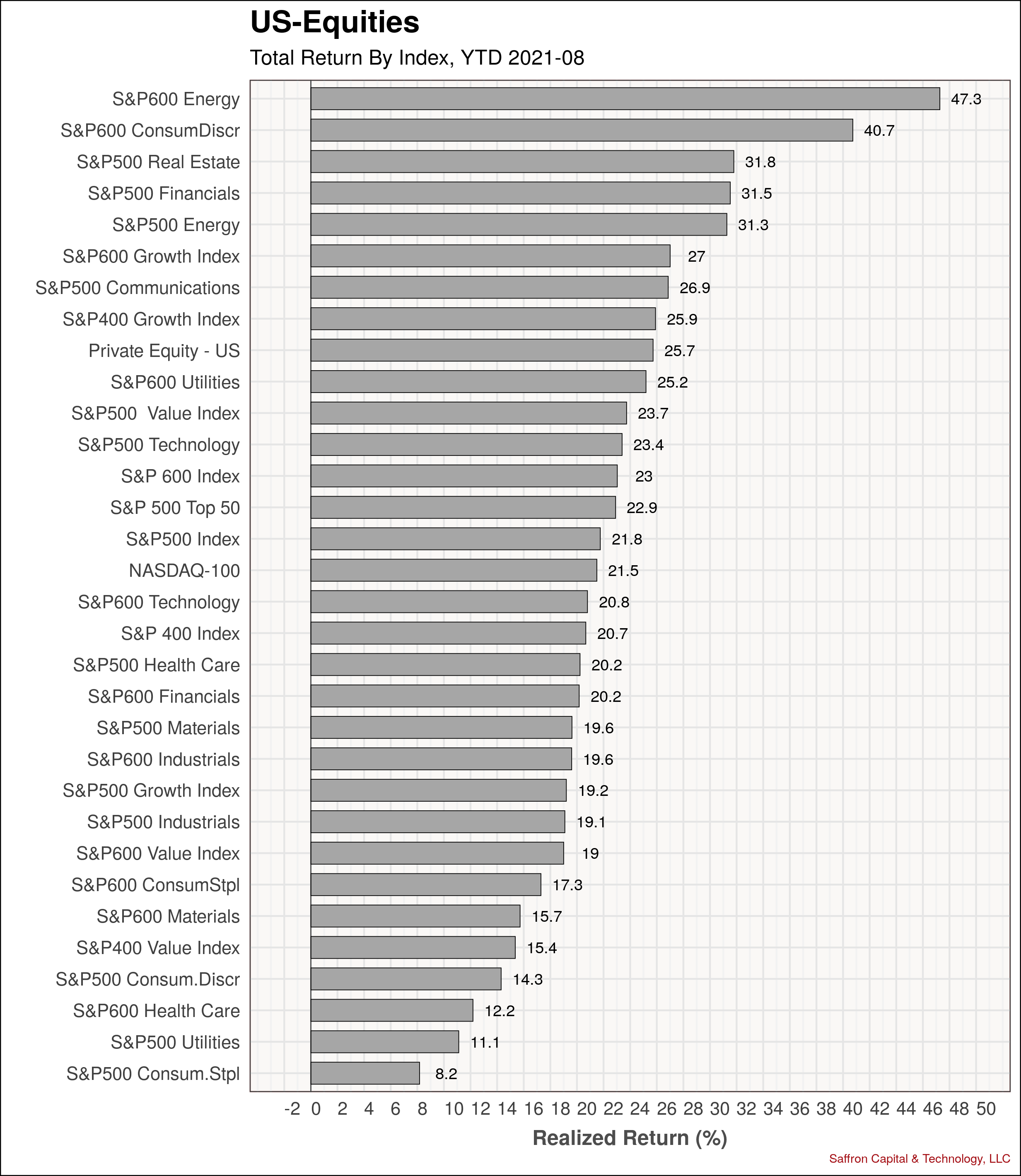

The S&P 500 Index was up 3.3% in August and is now up 21.6% year-to-date (YTD). Small cap technology, large cap financials and value over growth stocks dominated performance in the prior month. Large cap energy, small cap consumer discretionary, and real-estate continue to dominate performance over the first 8 months. Looking closer at the August returns, its no surprise the S&P500 value index was a strong performer. Large cap financial companies dominate the value index, which also topped the chart for August returns.

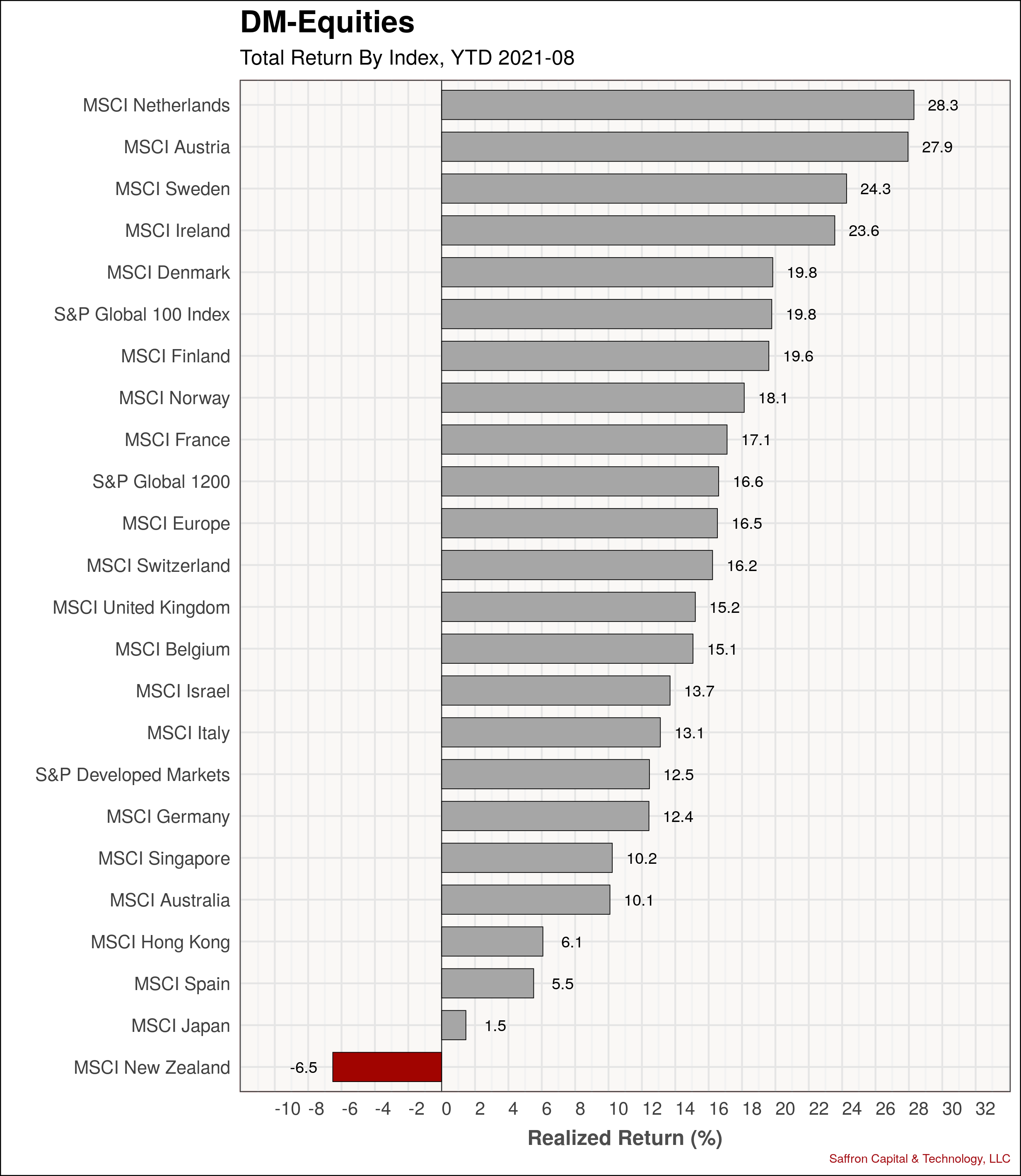

DM-Equities

Global equities and developed markets in particular advanced for the 7th consecutive month. As a result, many national stock indexes have cumulative returns greater than 20+% YTD.

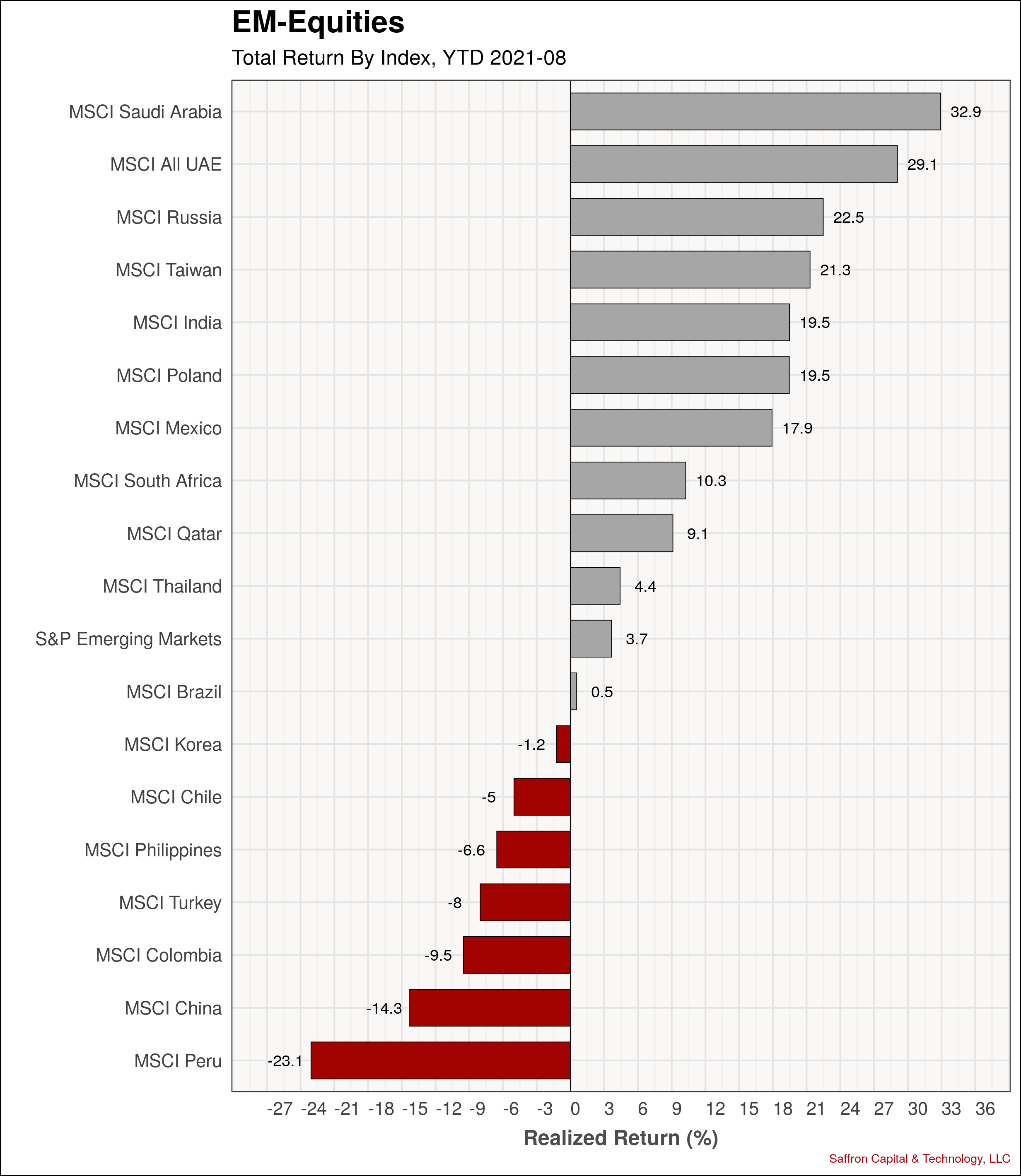

EM-Equities

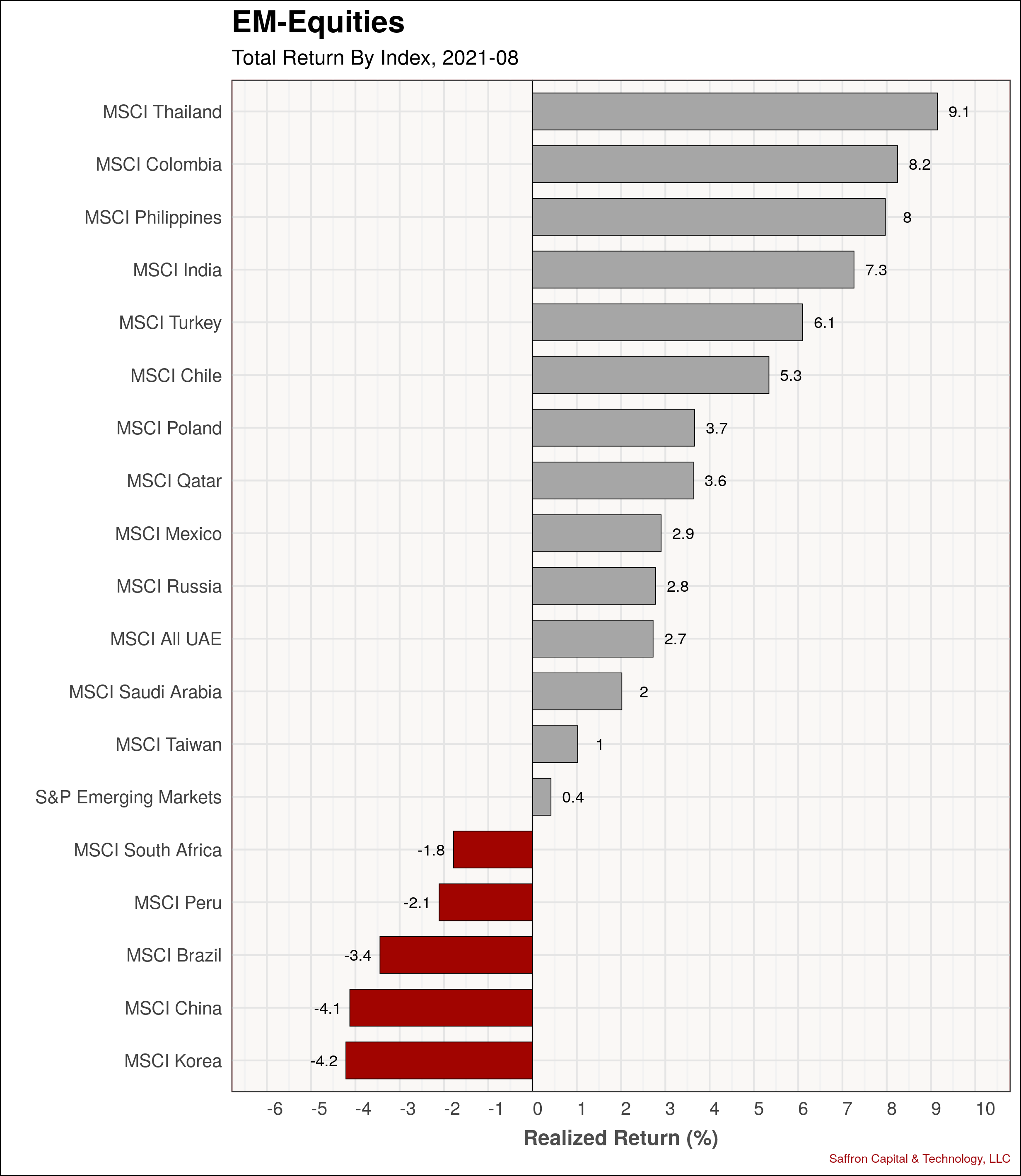

Emerging market equities had a mixed performance in August with loss leaders including South Korea, China, and Brazil. YTD performance continues to favor top oil exporters, Taiwan and India.

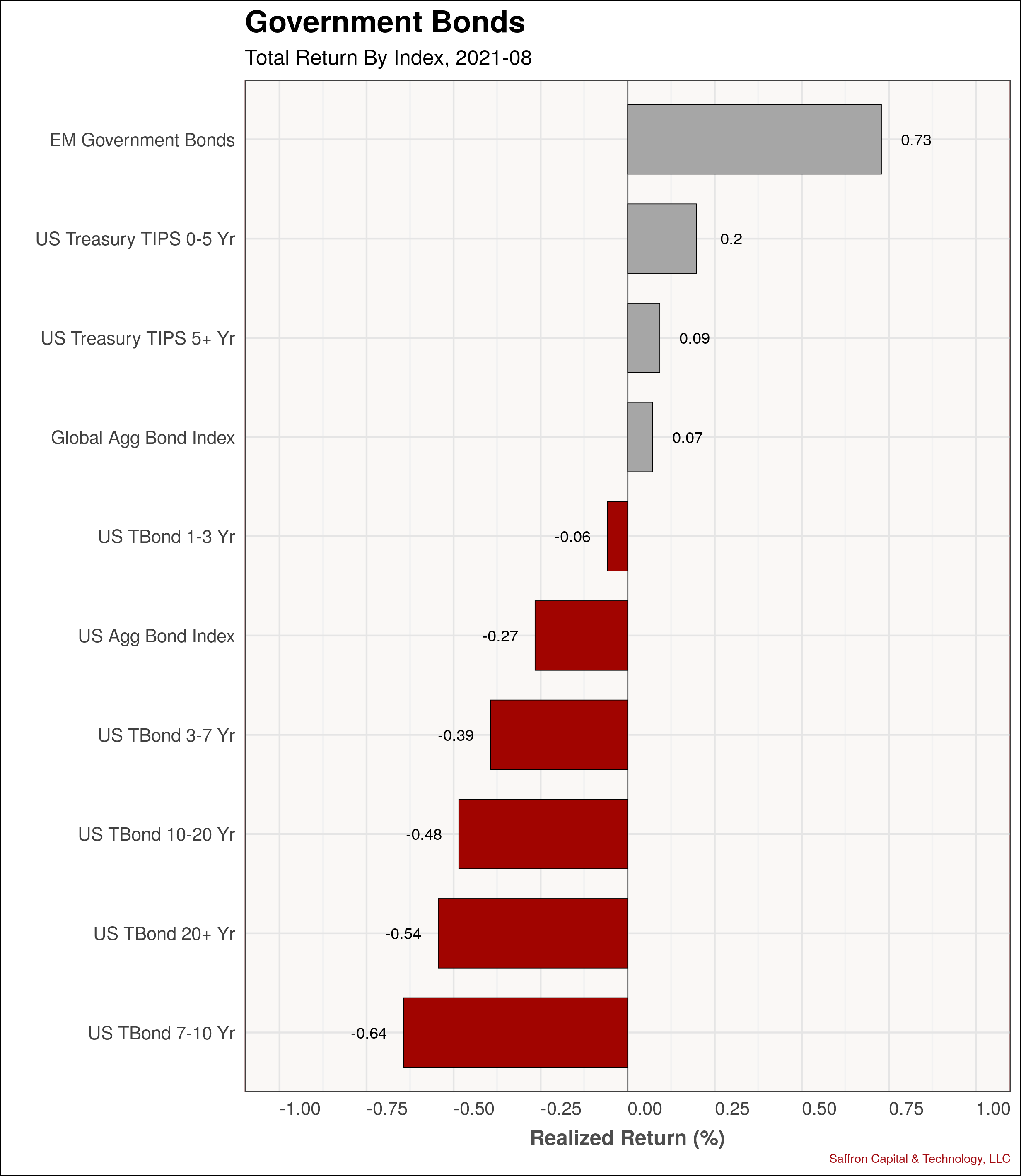

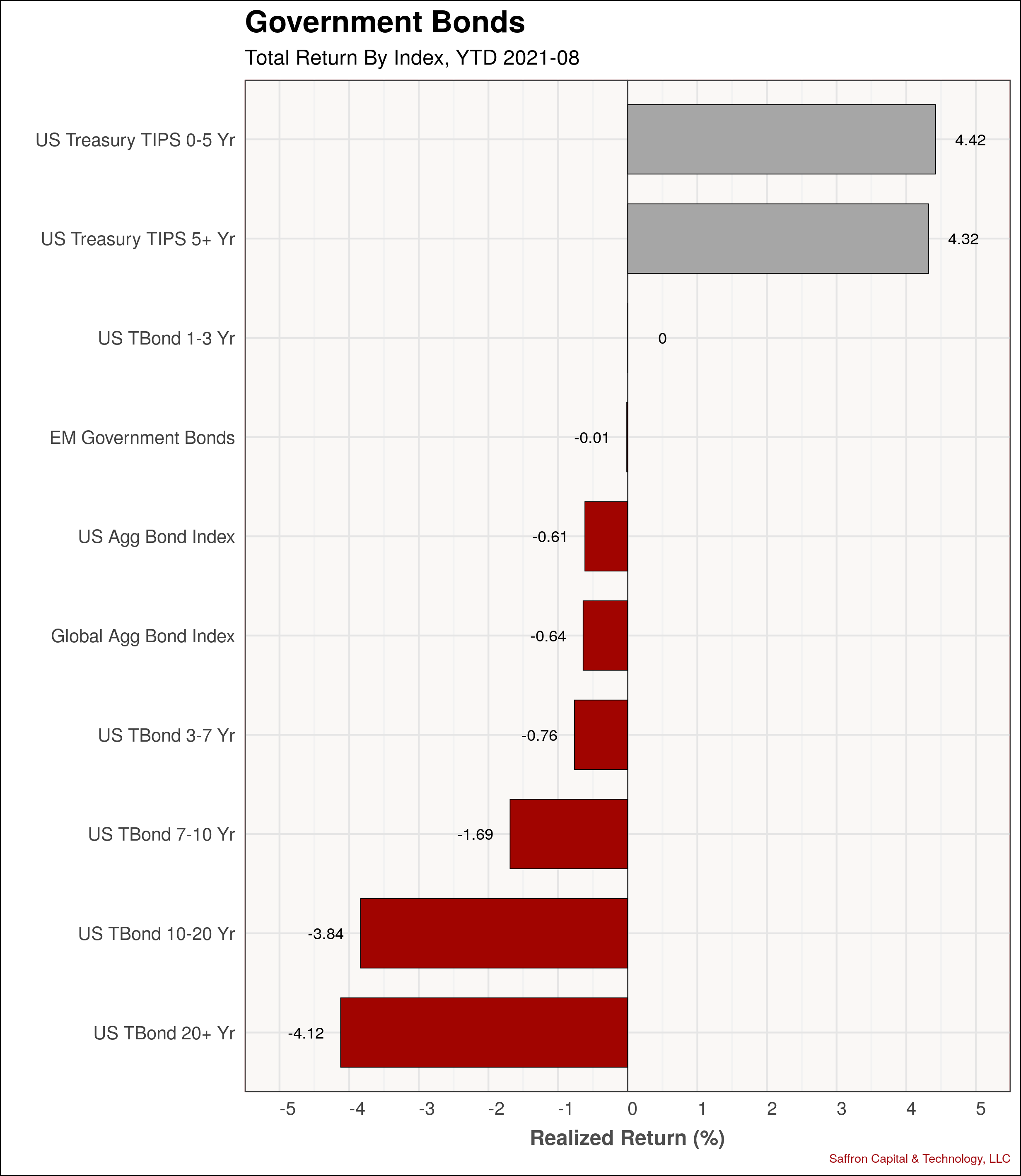

Government Bonds

Emerging market government bonds had a 73 basis point return in August and lead Developed and US markets by a large margin. US treasuries remained range bound, trading sideways in August. European yields have been rising relative to US yields since April, but gave ground in August, continuing to trade 170 basis points below the US yield curve. Long duration bonds lost 54 points, largely due to inflation as inflation protected bonds were unchanged. Inflation protected bonds have yielded 4.4% YTD.

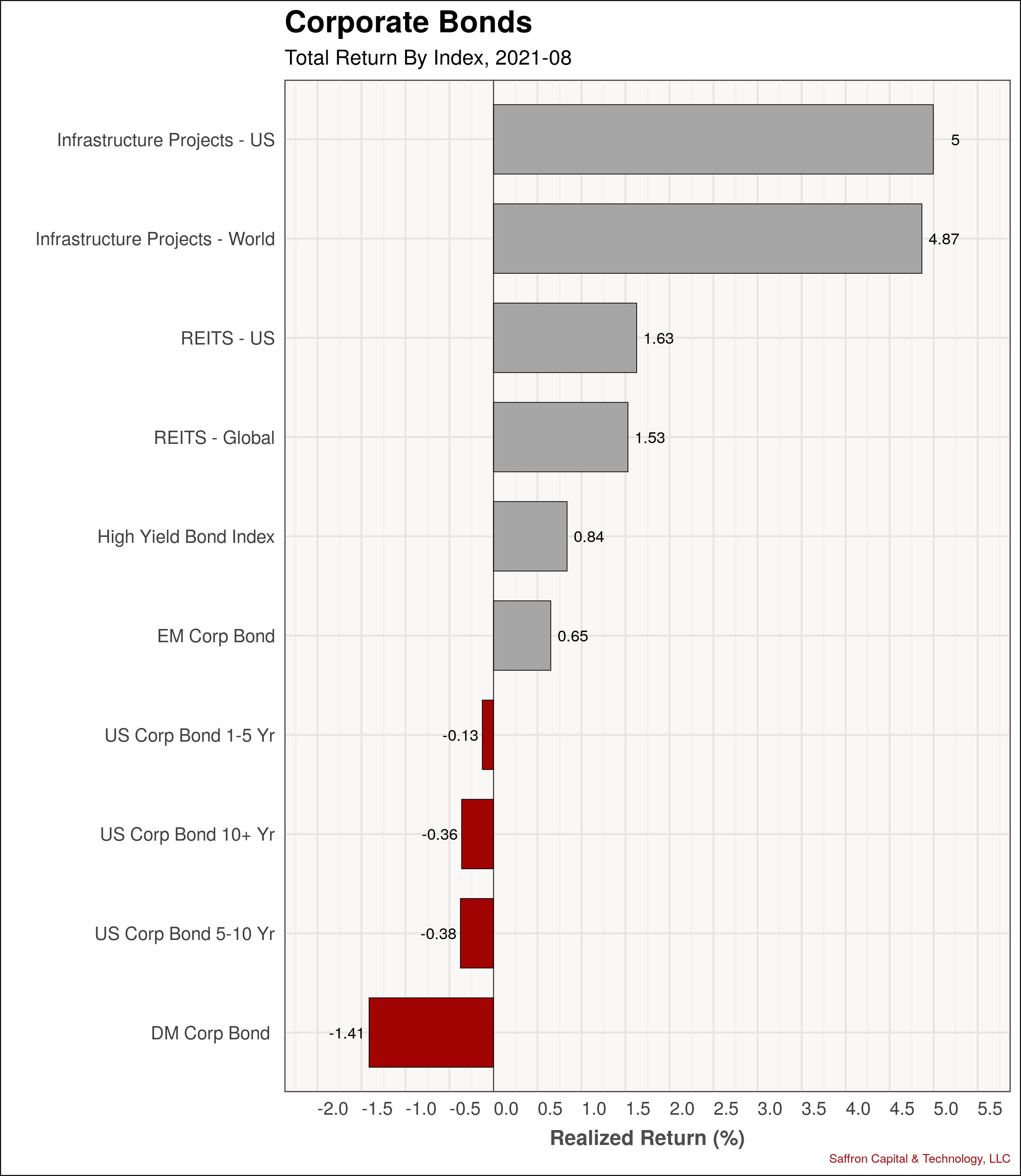

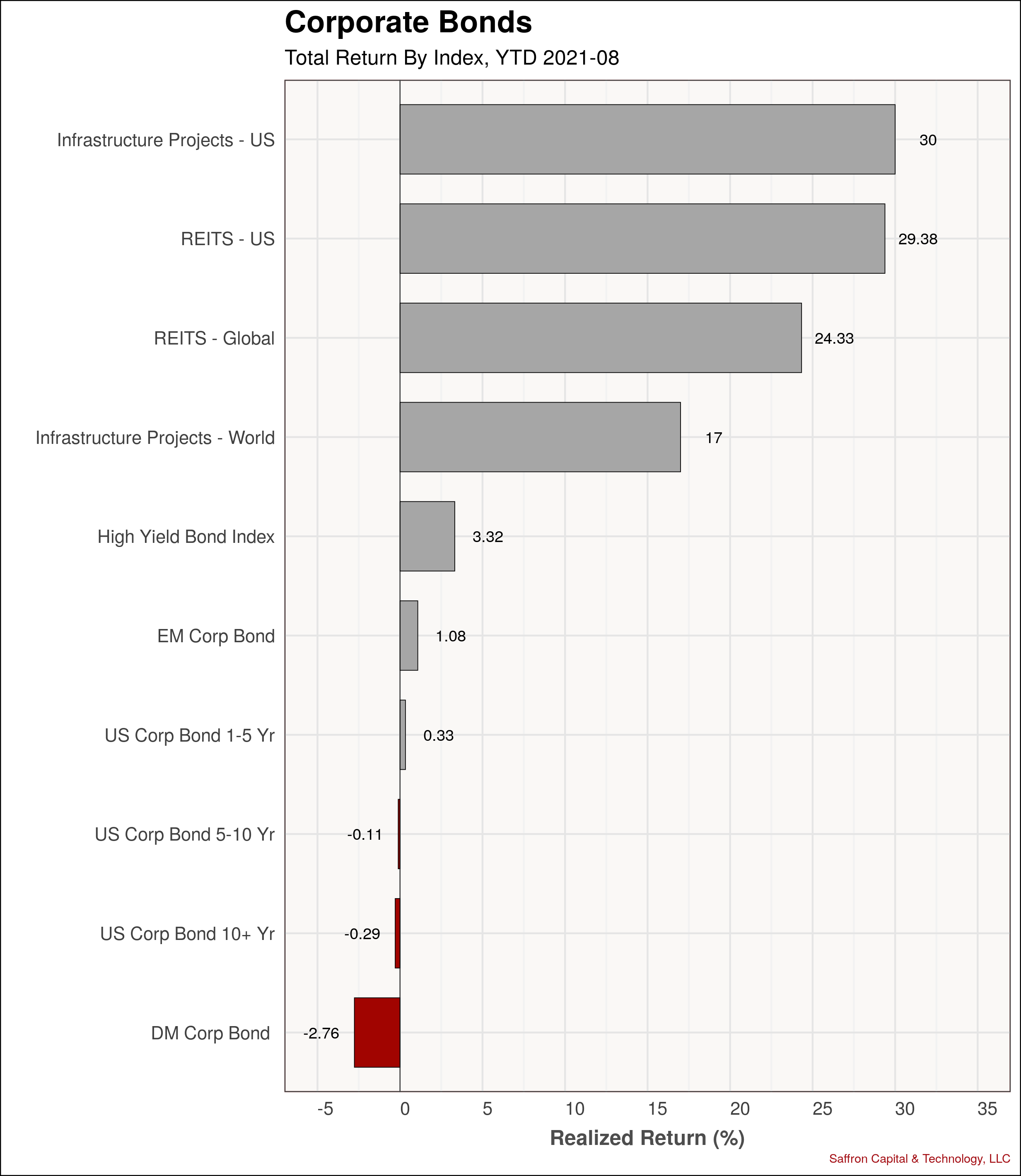

Corporate & Infrastructure Bonds

Infrastructure bonds, REITS and high-yield corporate bonds all turned in a positive month. Bonds tied to real assets again outperformed the S&P500 both MTD and YTD. US and international REITS also continue to outperform the S&P 500 on a YTD basis.

Commodities

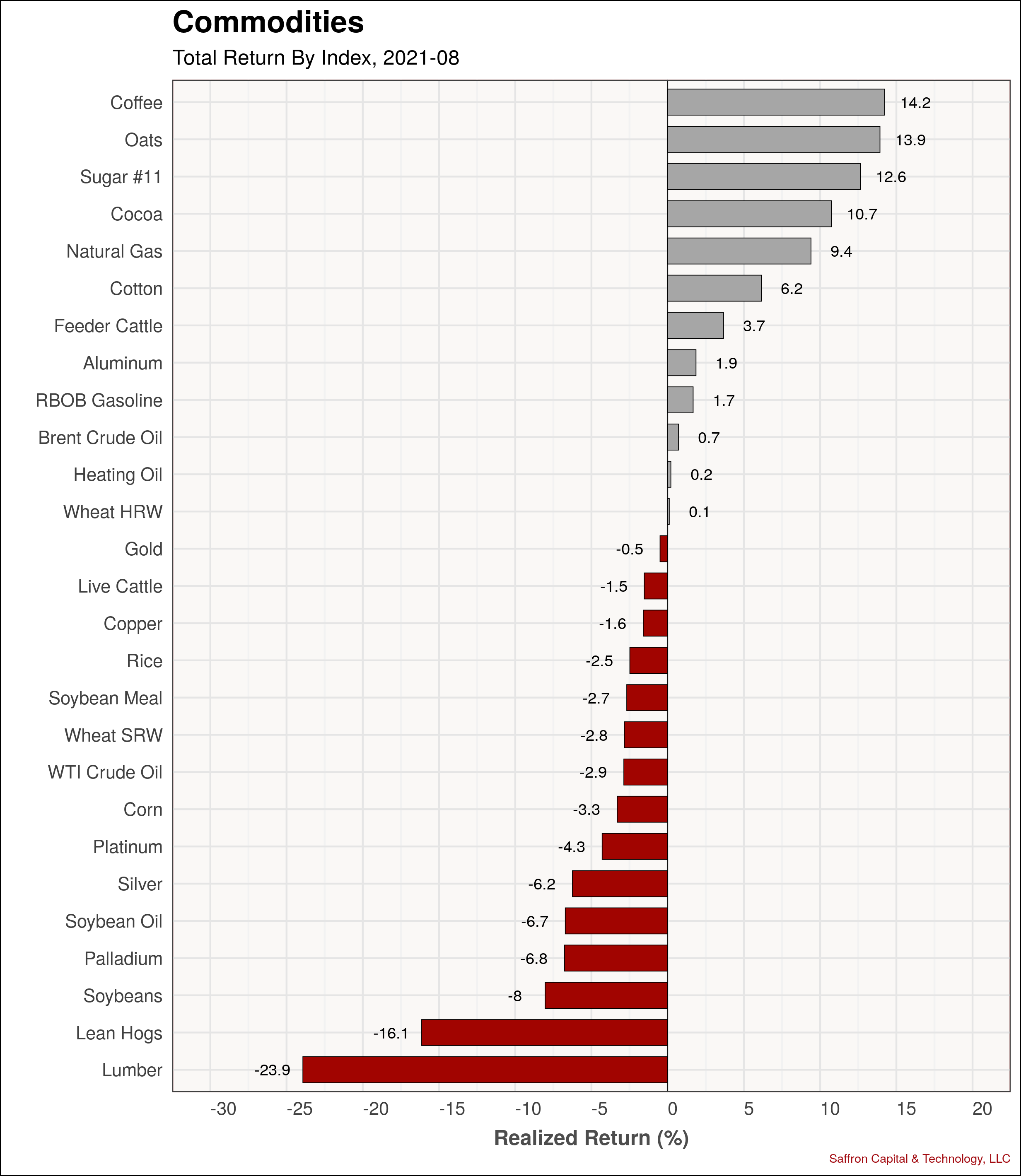

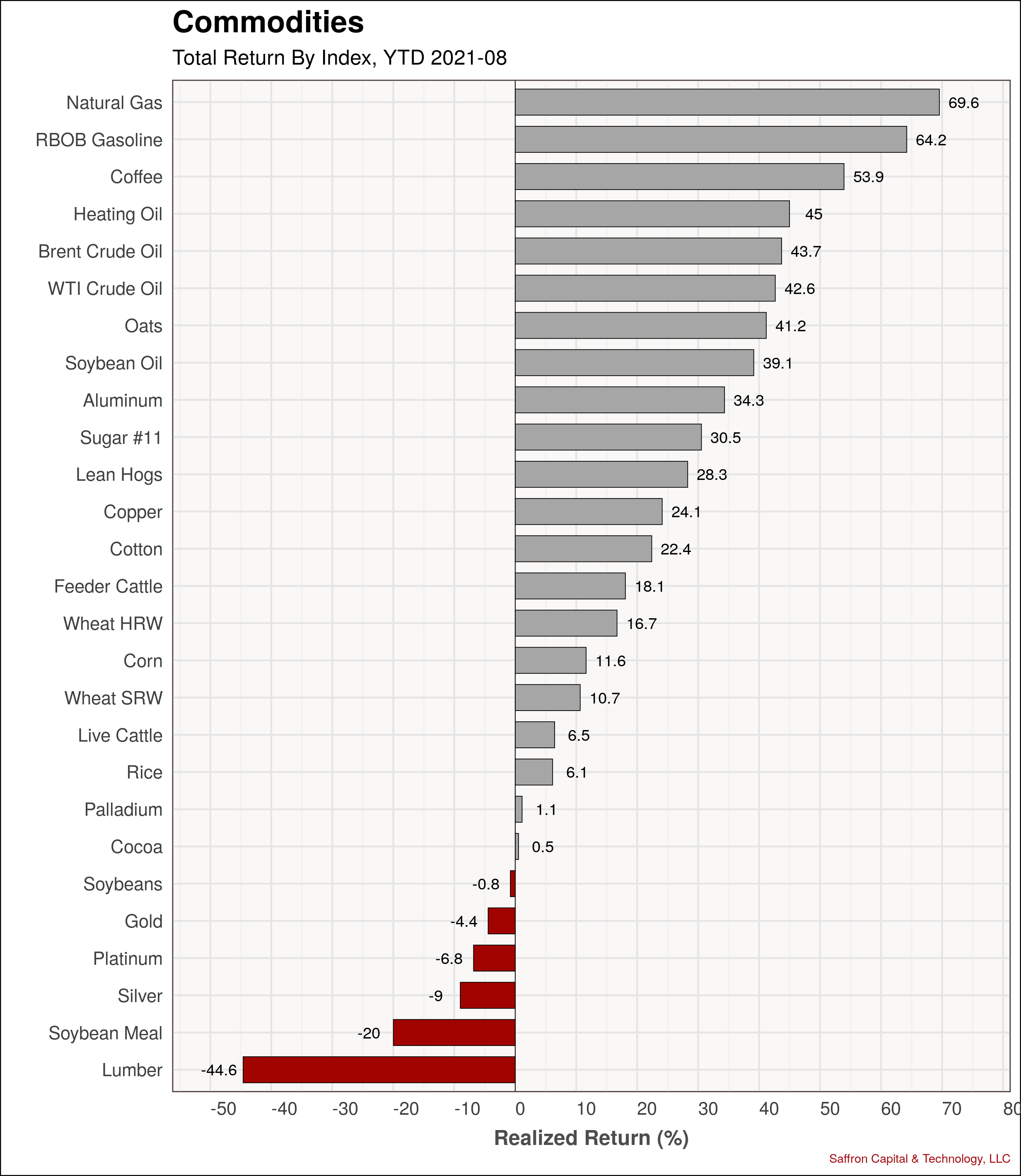

Turning to commodities, coffee turned in the strongest month (+14.2%) on long-standing crop damage in Brazil, plus supply chain bottlenecks in Vietnam. Oats (13.9%) and Sugar (+12.6%) also had strong gains. Lumber fell the furthest (-23.9%) in the prior month. Other commodities struggled as well, with soybeans (-8%) falling on improved weather and yield potential, silver (-6.2%) falling for a third consecutive month, and copper also down (-1.6%). On a YTD basis, natural gas is up the most (a massive +69.6%), followed closely by gasoline (+64.2%) and coffee (+53.9%). Both WTI and Brent crude oil, which fell in August, are both up over 40% since January.

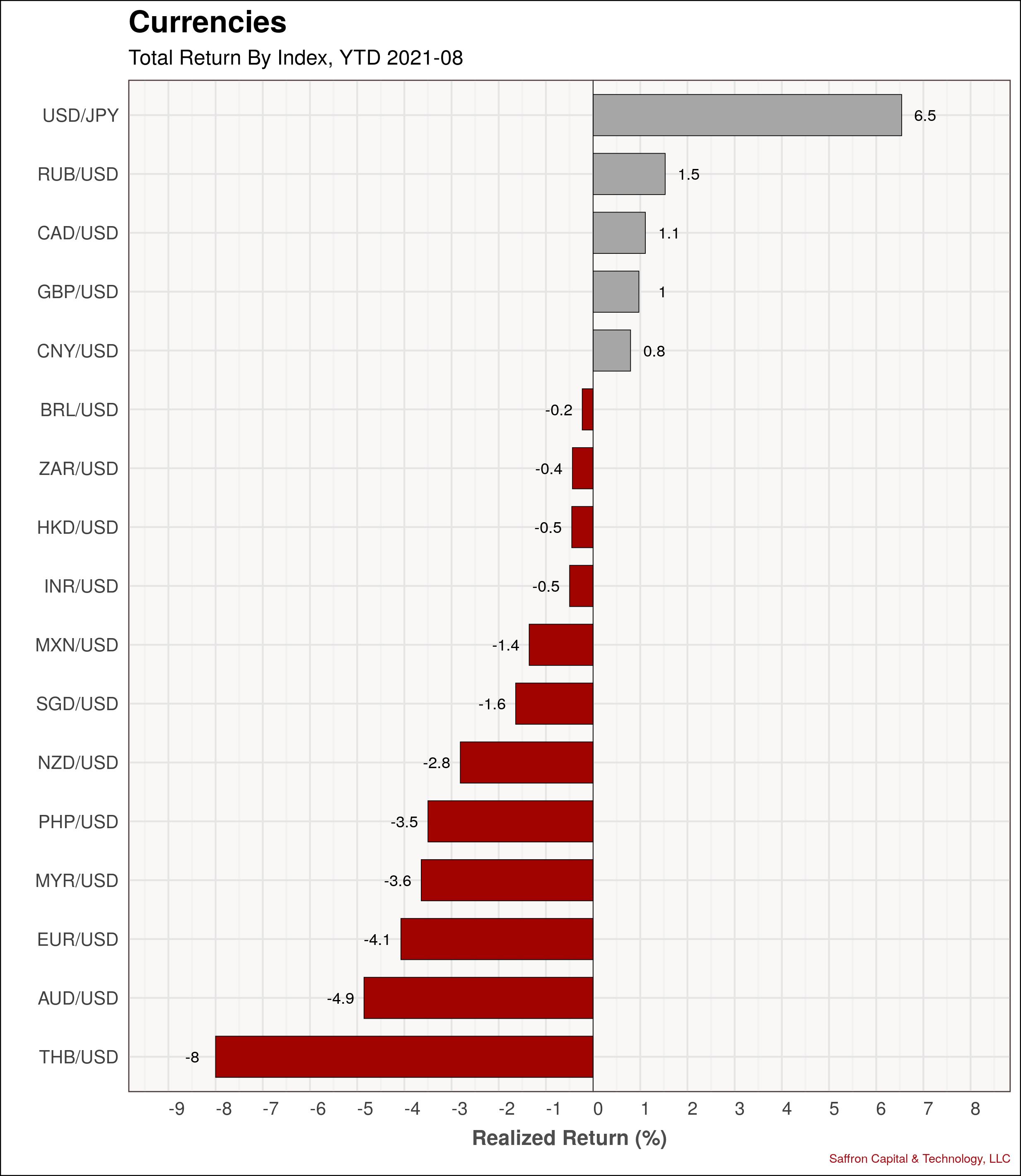

Currencies

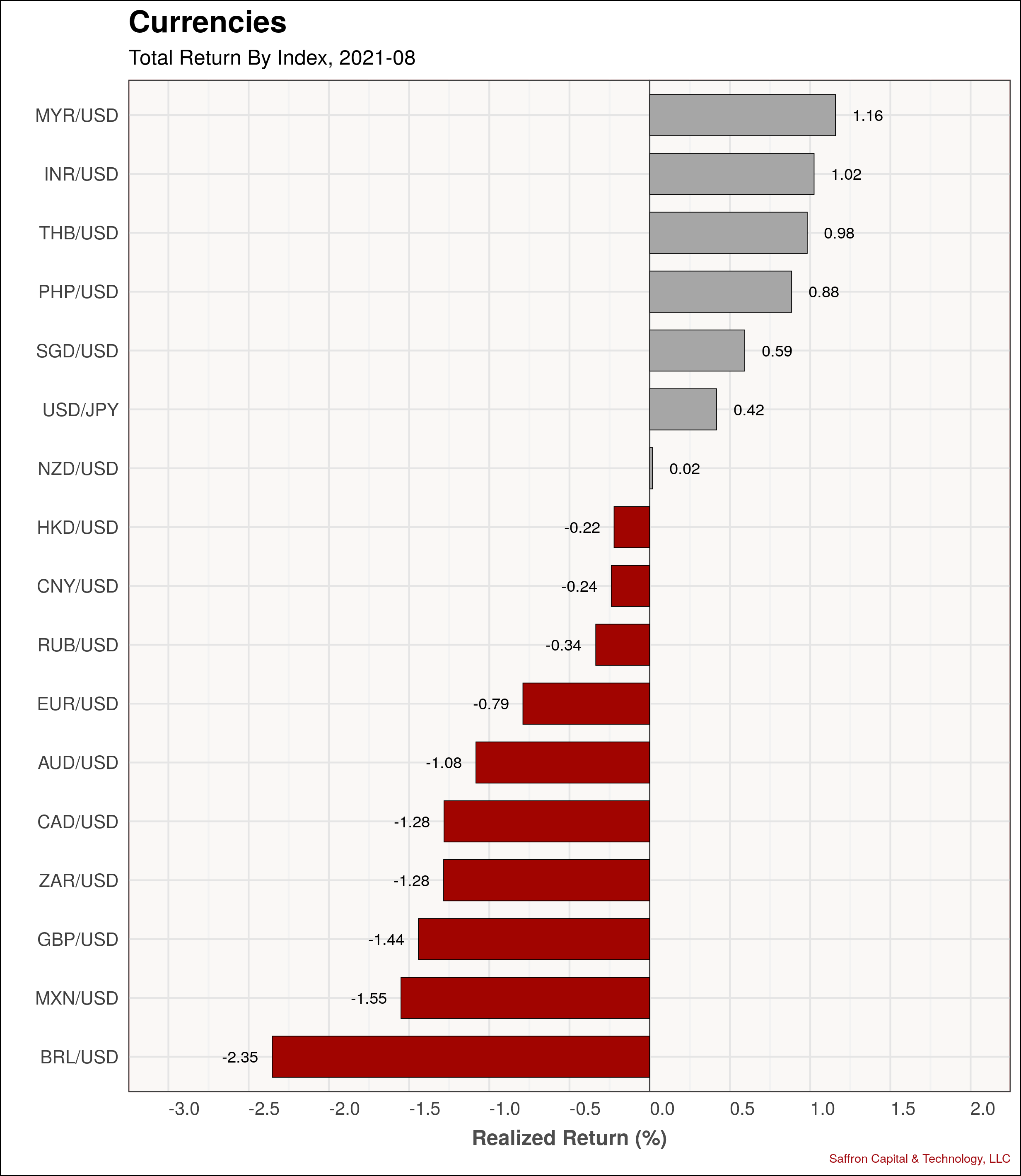

Turning to FX, there was no major moves in any of the major pairs.

{kind=link}

{kind=link}