Lviv, Ukraine. November 27, 2013. Ukrainian students singing national anthem during demonstration for integration into the European Union.

Major Asset Classes

February 2022

Performance Comparison

Introduction

February returns were dominated by events in Ukraine. Equity markets were down with only a few exceptions in emerging markets. Value again led growth, consumer defensive stocks beat consumer cyclical stocks, and small-cap beat large cap stocks. A consistent theme in February was the ‘risk-off’ market regime and portfolio liquidations. Even fixed income assets suffered. though infrastructure project bonds again outperformed equities. Finally, commodities continued to inflate as the commodity super-cycle hit new highs.

The following analysis provides a visual record of returns across and within the major asset classes. The report is intended to help investors with portfolio comparisons and performance benchmarking.

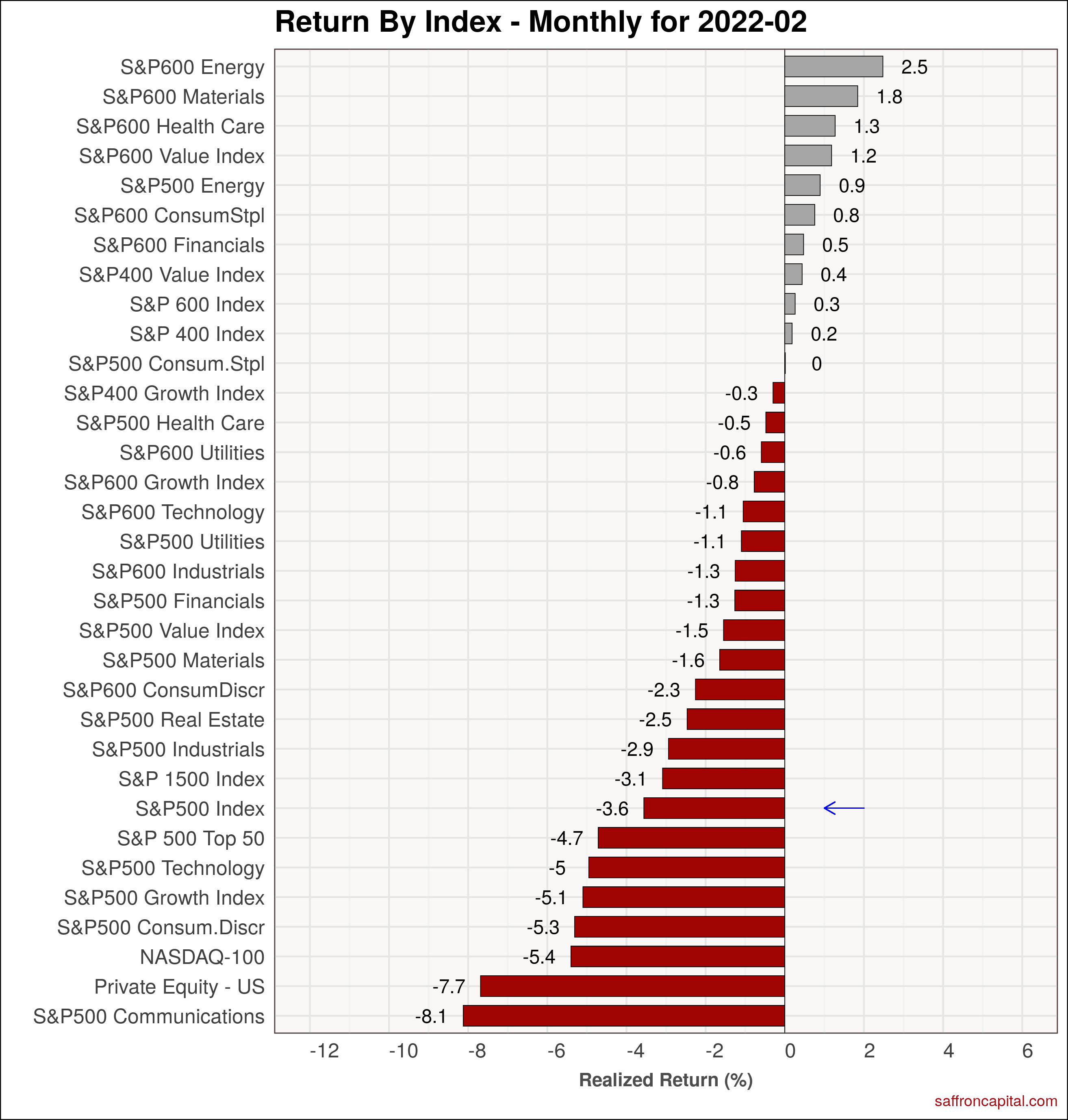

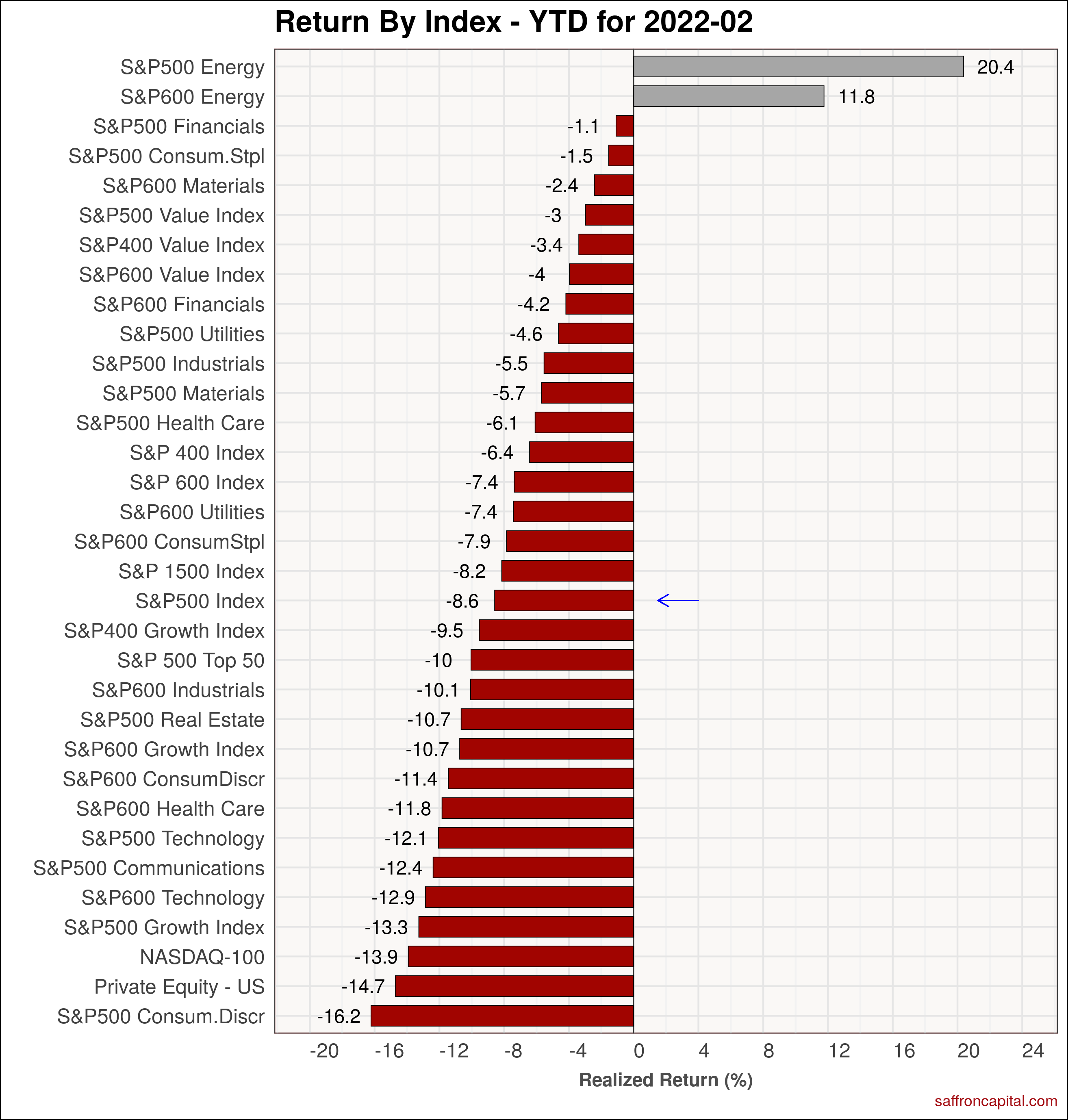

US Equities

The S&P 500 index was down -3.6% in January after accounting for dividends. In contrast, strength was seen in small cap energy (+2.5%), materials (+1.8%), and healthcare (+1.3%). On a year-to-date (YTD) basis, only large-cap energy (+20.4%) and small cap energy (+11.8%) have positive returns. Technology (-12.9%) and consumer discretionary (-16.2%) stocks have the worse returns since the year started.

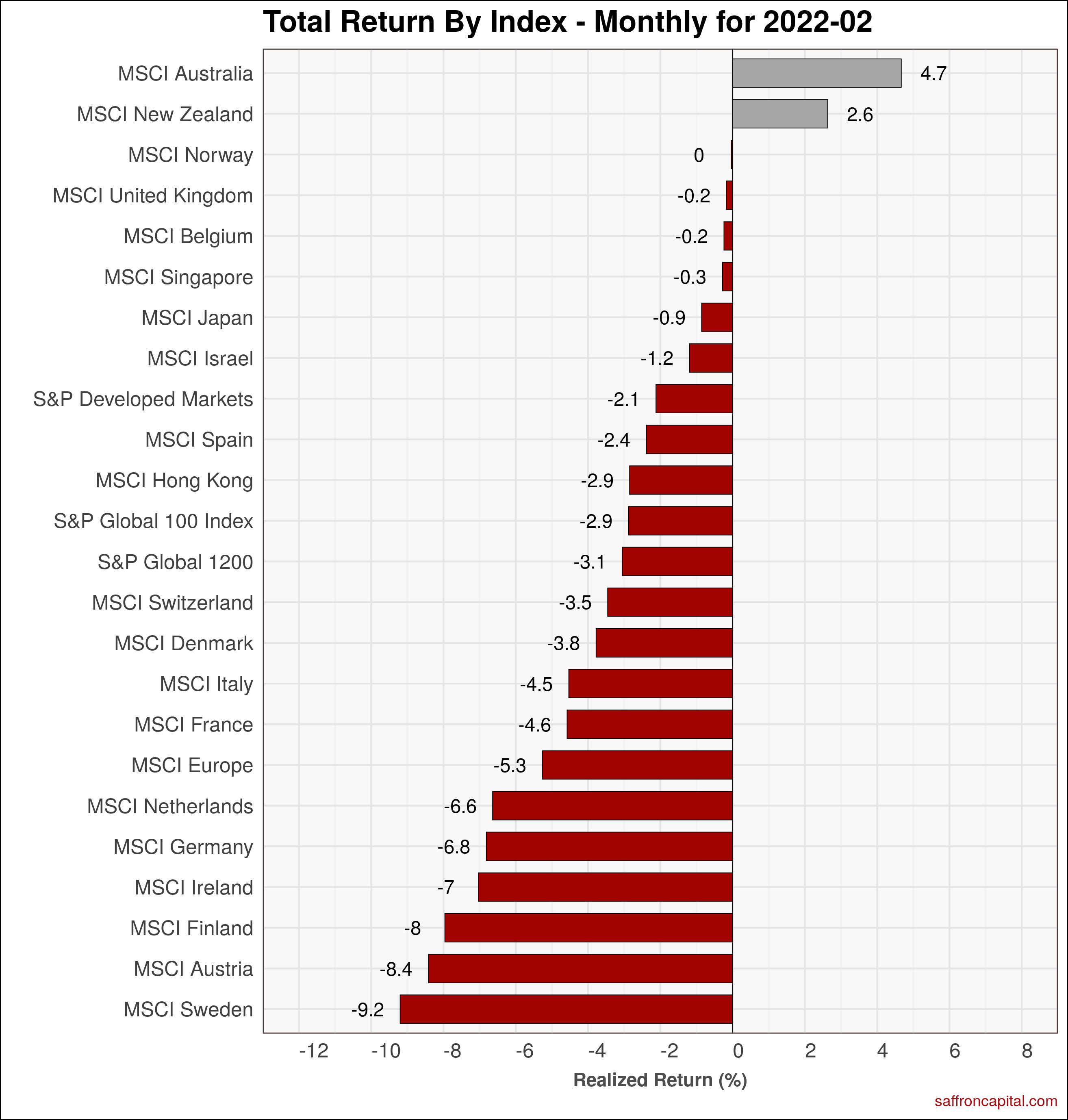

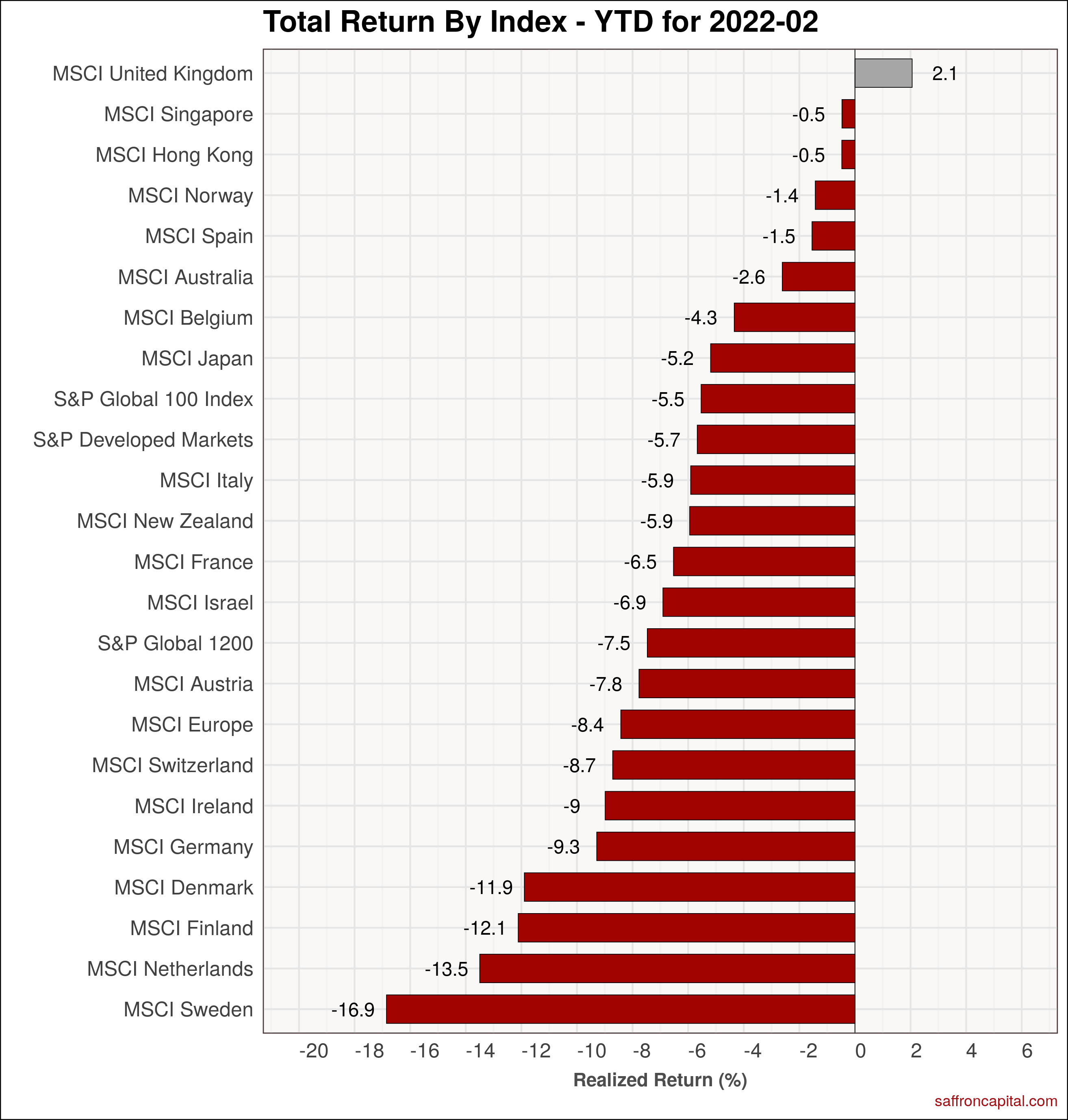

Developed Market Equities

Elsewhere, red ink is apparent across all the developed market indices with the exception of Australia (+4.7%) and New Zealand (+2.6%). In general, return momentum has swung back to favor ownership of US stocks stocks. Loss leaders – Sweden, Austria, and Finland are most vulnerable to events in Ukraine. All all had return losses in excess of 8%.

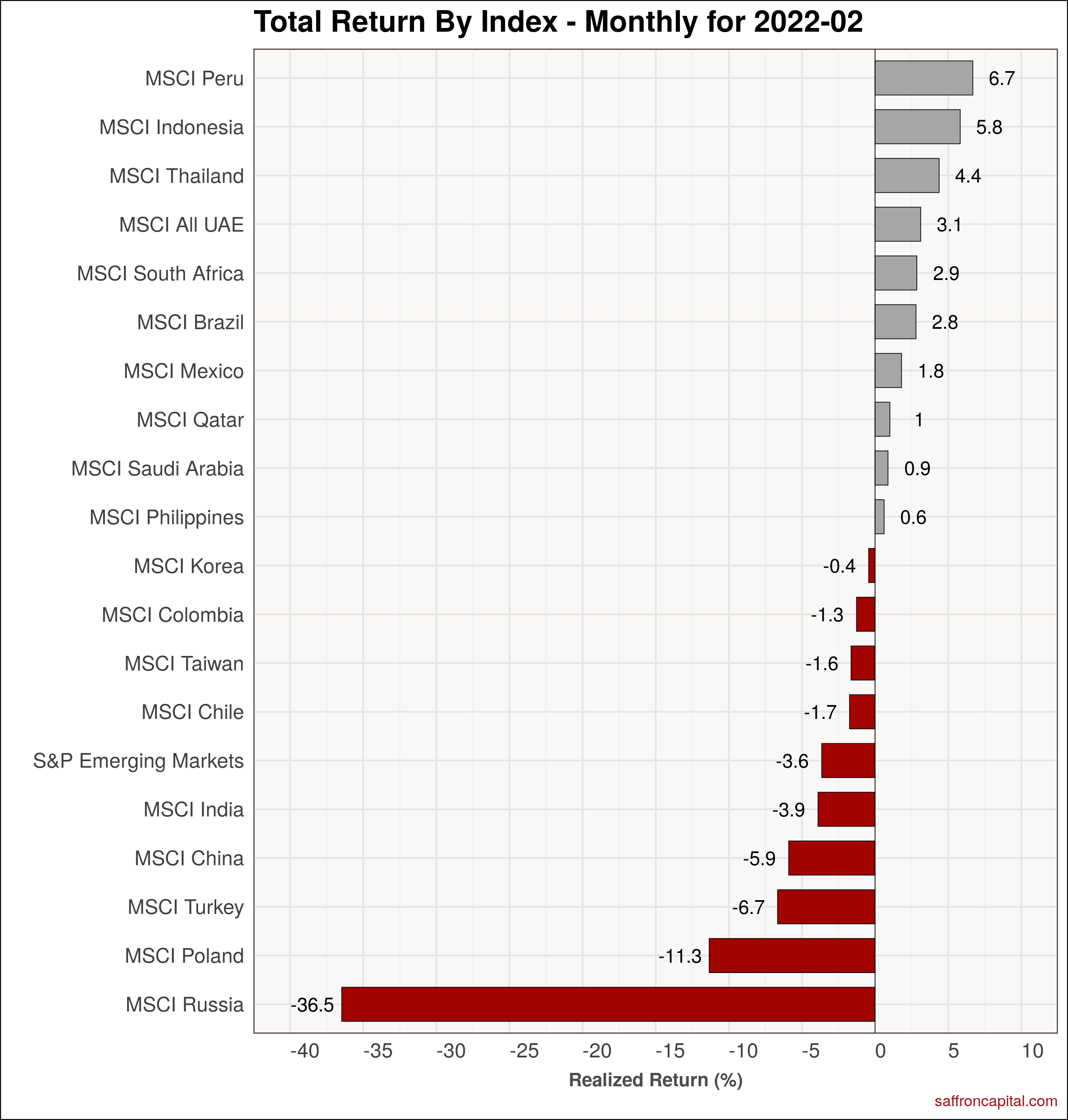

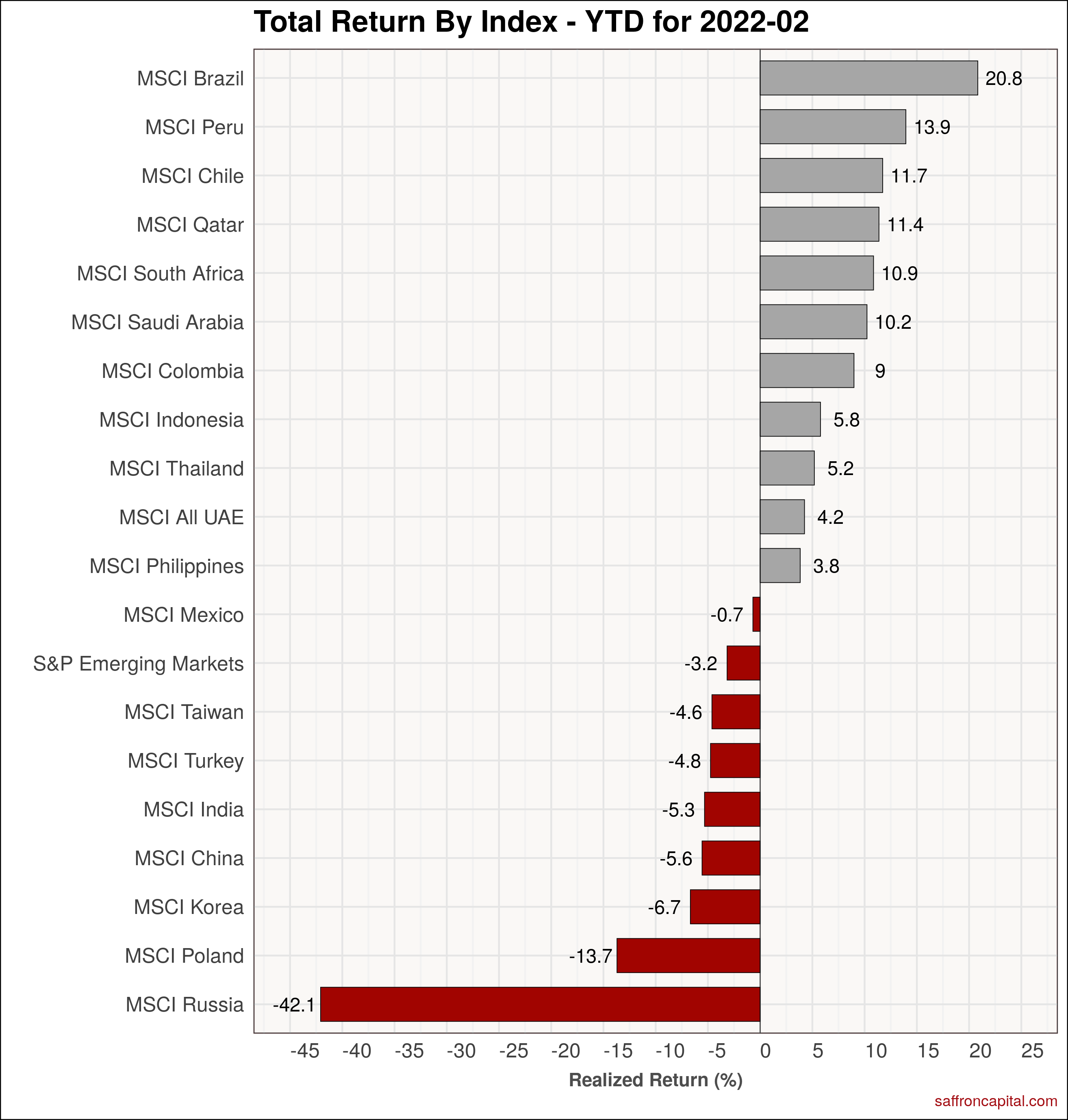

Emerging Market Equities

Next, we see that select emerging market equities offered solid returns and diversification for the second month straight. The S&P Emerging Market Index (-3.6%) lagged US equities, thanks to heavy losses in Russia (-36.5%) and Poland (-11.3%). However, persistent return growth is evident in commodity-based economies. For example, year-date gains for Brazil (+20.8%), Qatar (+11.4%), and Saudi Arabia (+10.2%) are all solid. Commodity consuming economies in Asia, notably Taiwan (-4.6%), China (-5.6%), and Korea (-6.7%) lagged their peers in returns.

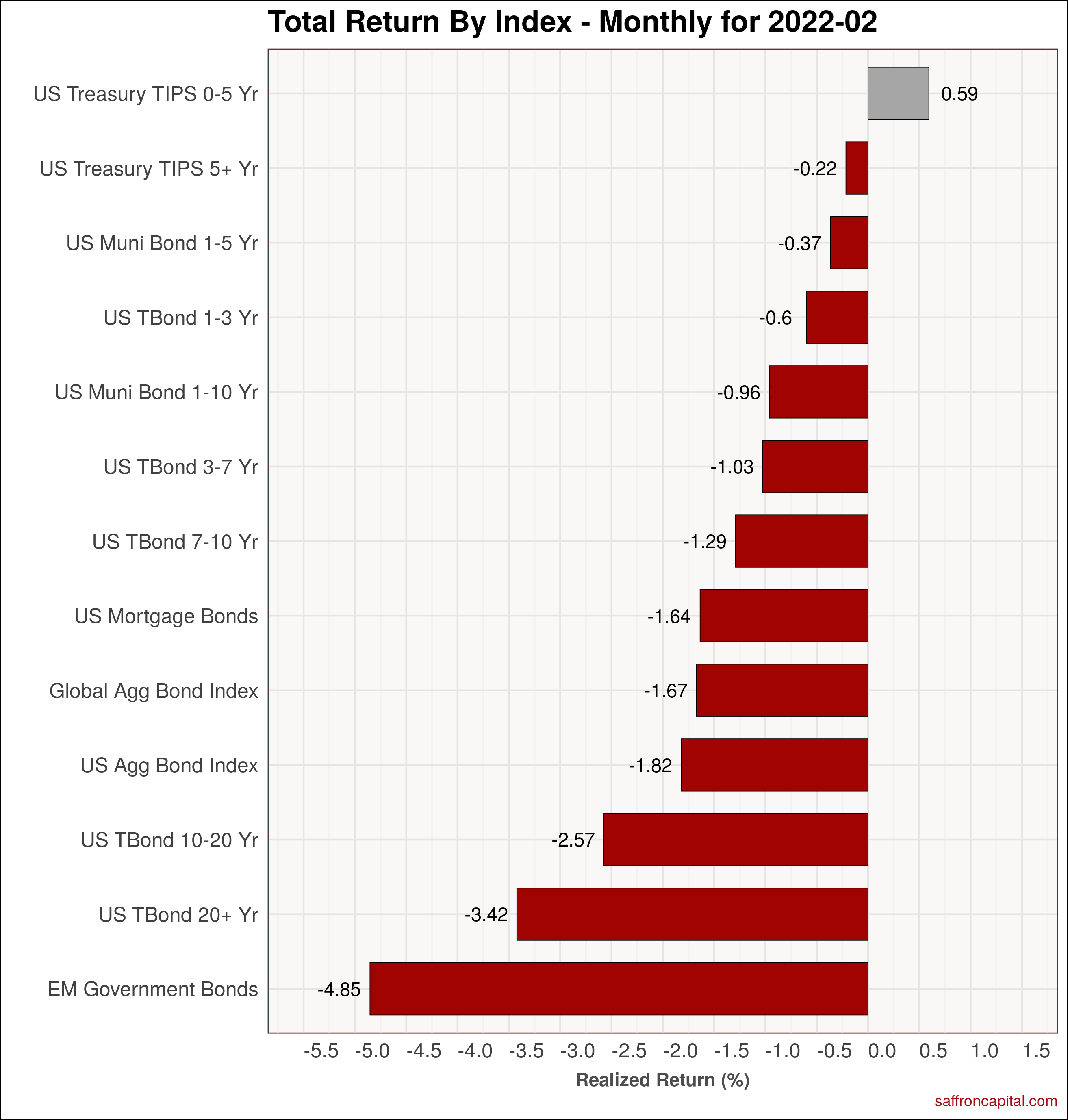

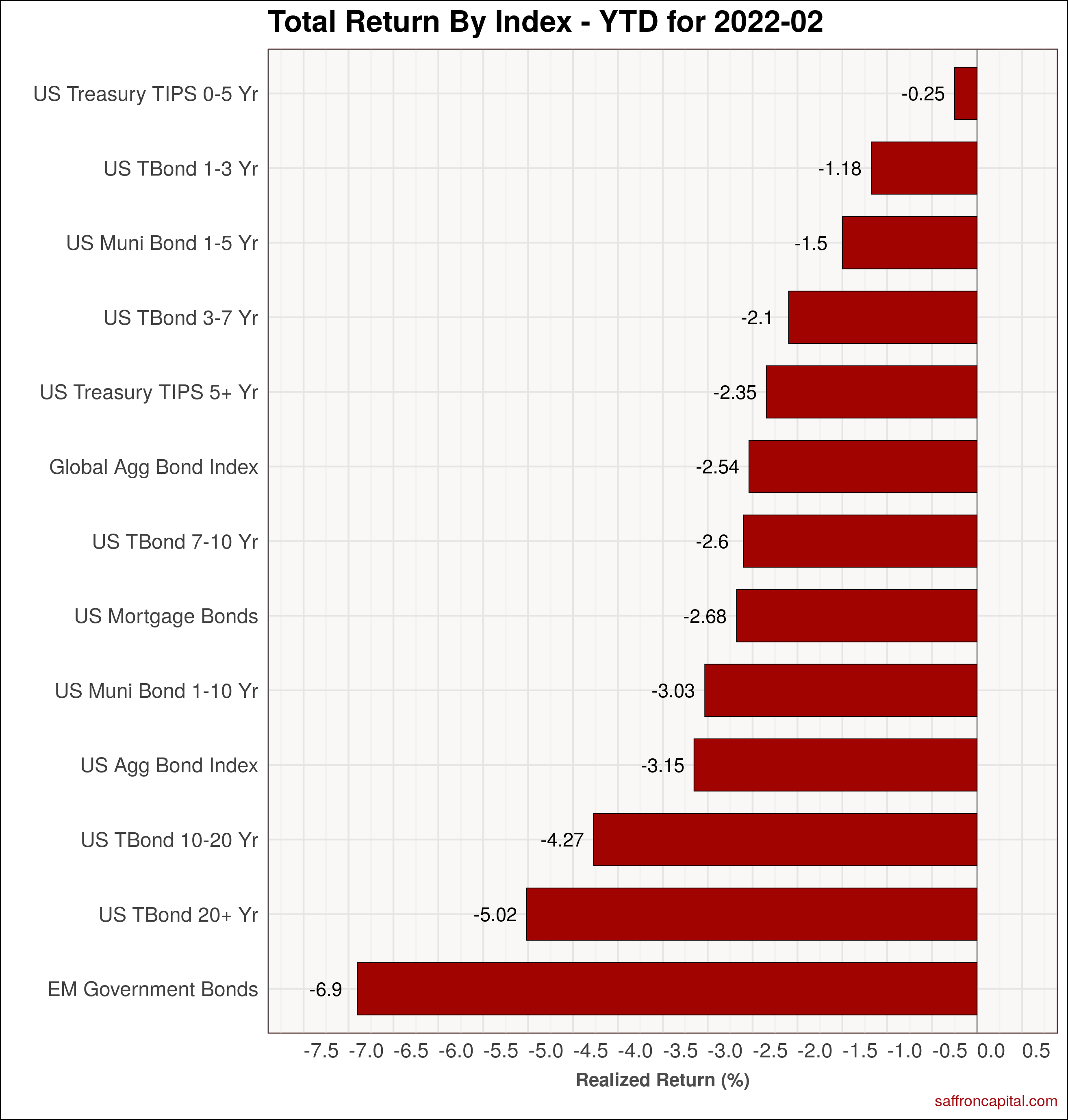

Government Bonds

Returns across all bond durations suffered price declines in February. Relative return momentum favored Treasury Inflation Protected Securities (TIPS), which geberated a gain of 59 basis points (bps). The US aggregate Bond index was down 167 bps and long bonds were down 342 bps. Emerging market bonds (-485 bps) were hit the hardest because of events in Ukraine.

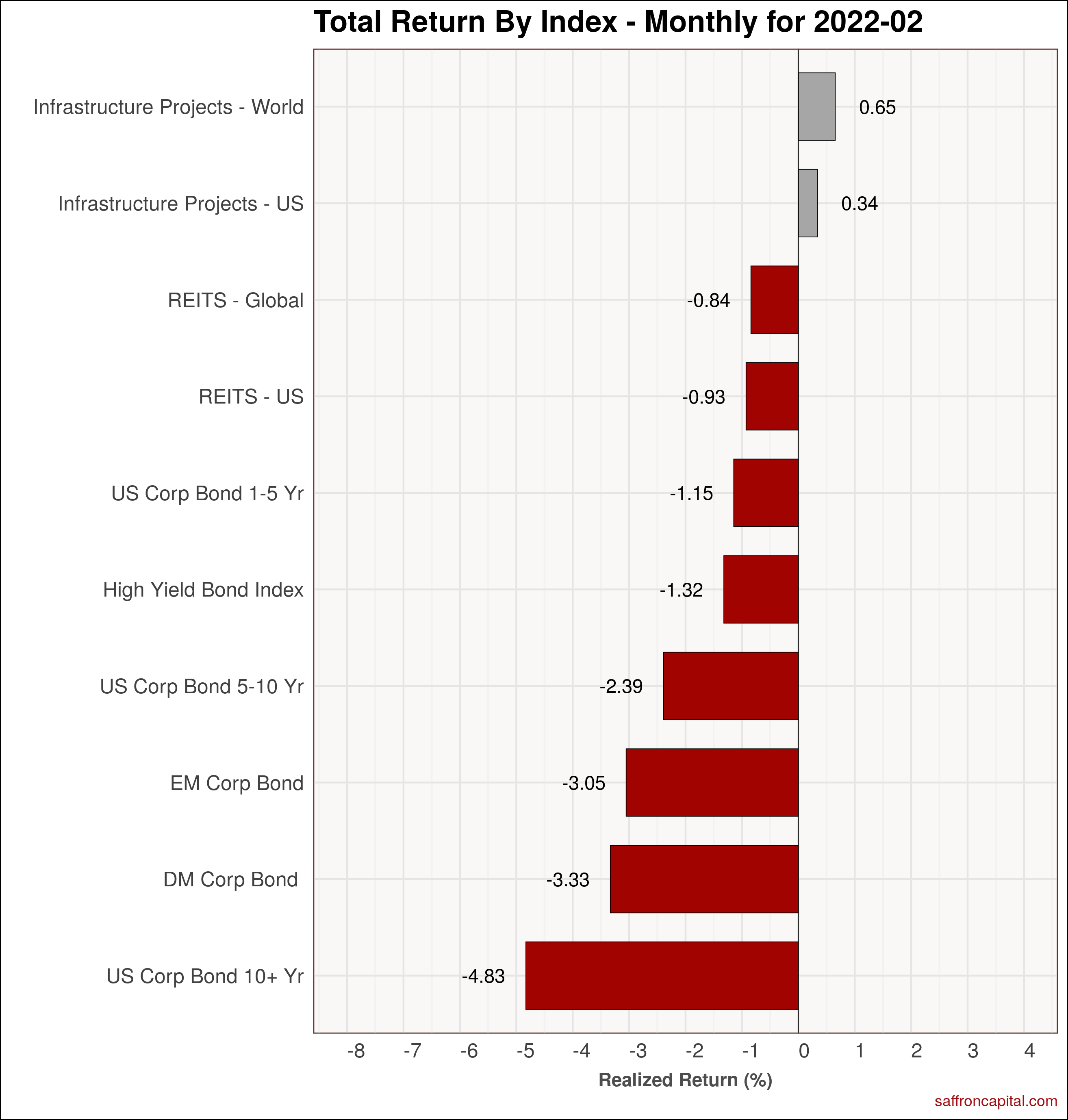

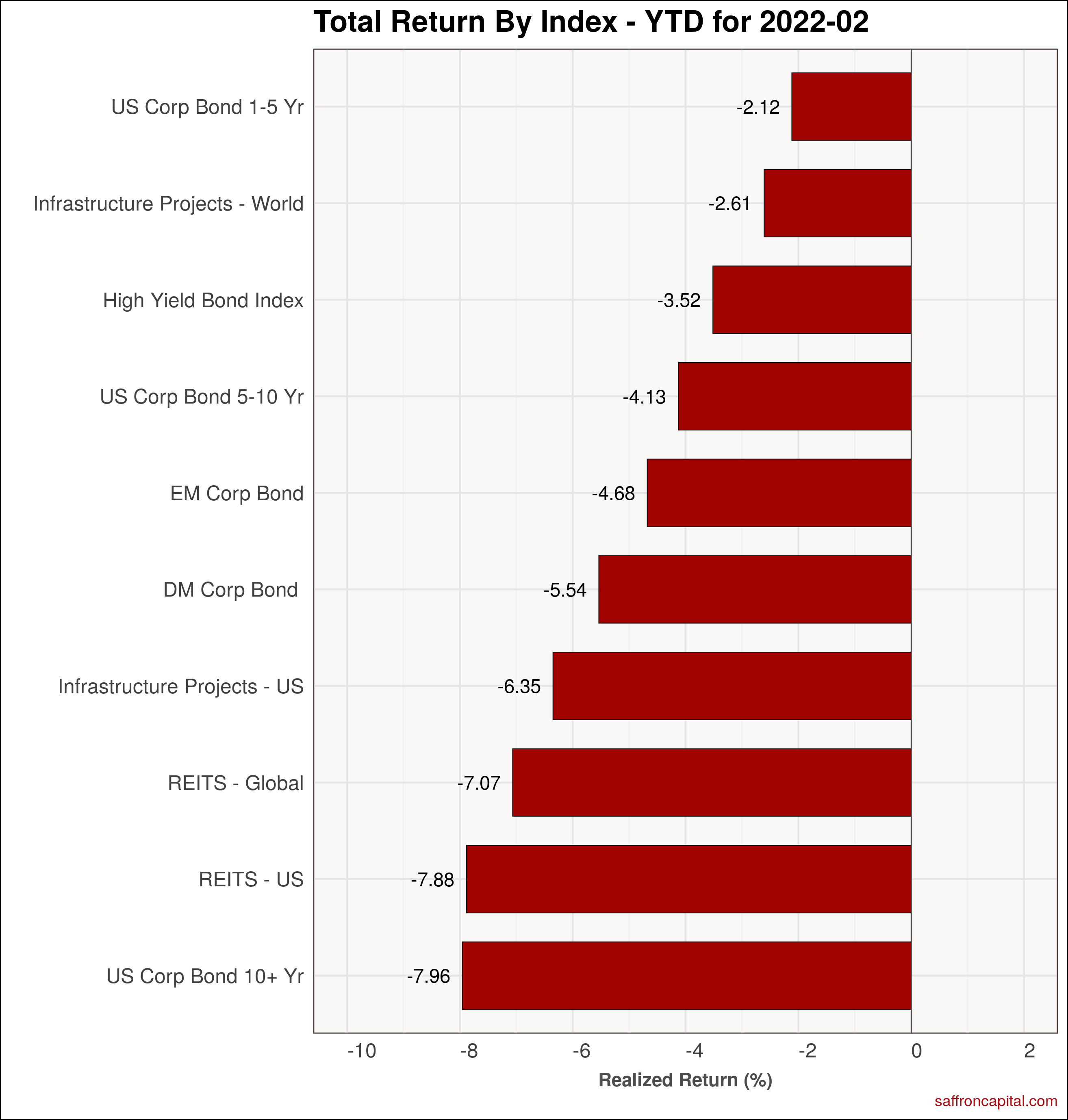

Corporate & Infrastructure Bonds

In February, US and global infrastructure project bonds turned in positive returns of 65 and 34 bps, respectively. Long-term corporate bonds (-483 bps) suffered from both yield curve and earnings outlook declines. Meanwhile, the High-Yield Bond index (-132 bps) had muted losses in line with short duration corporate bonds (-115 bps).

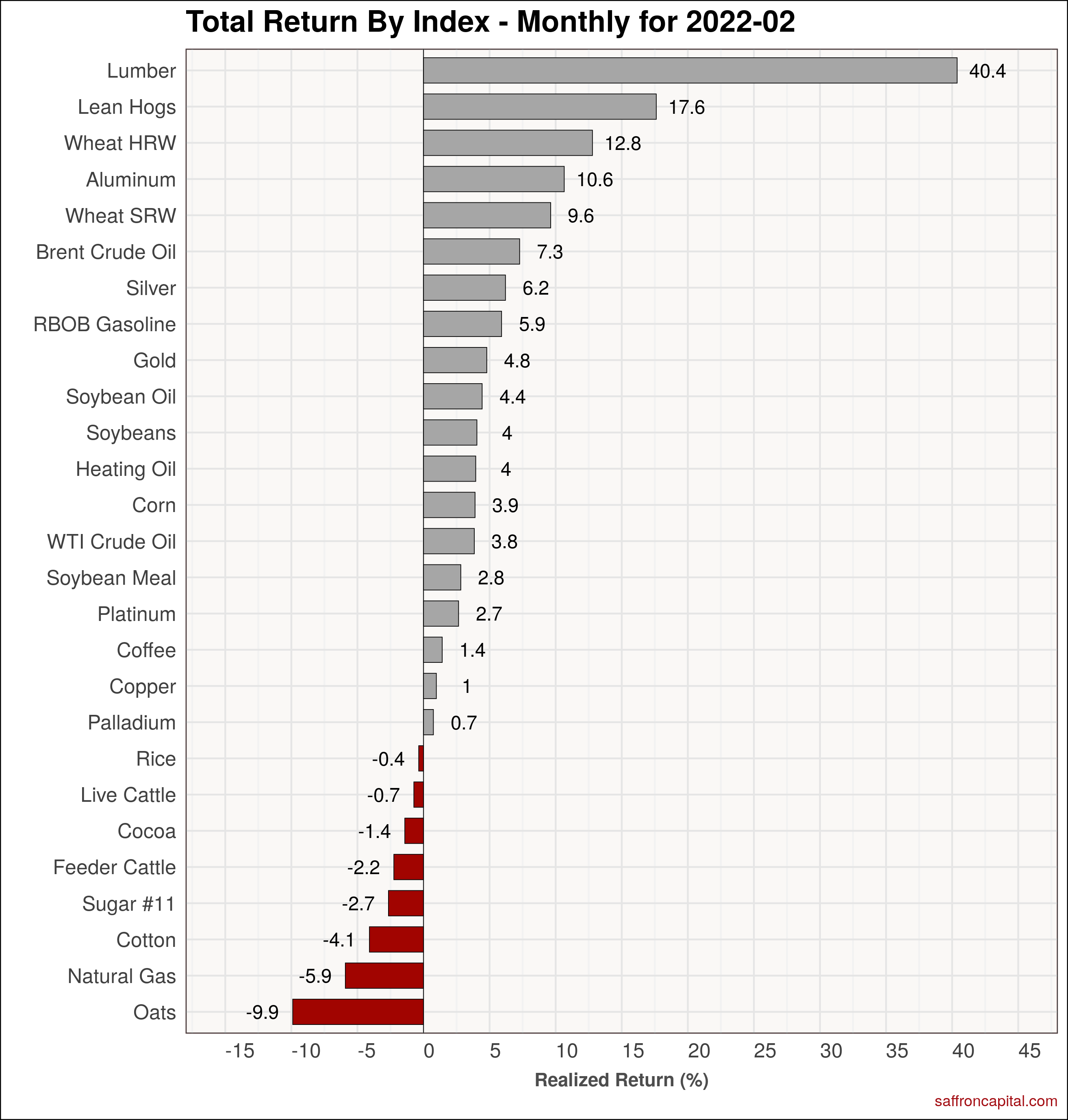

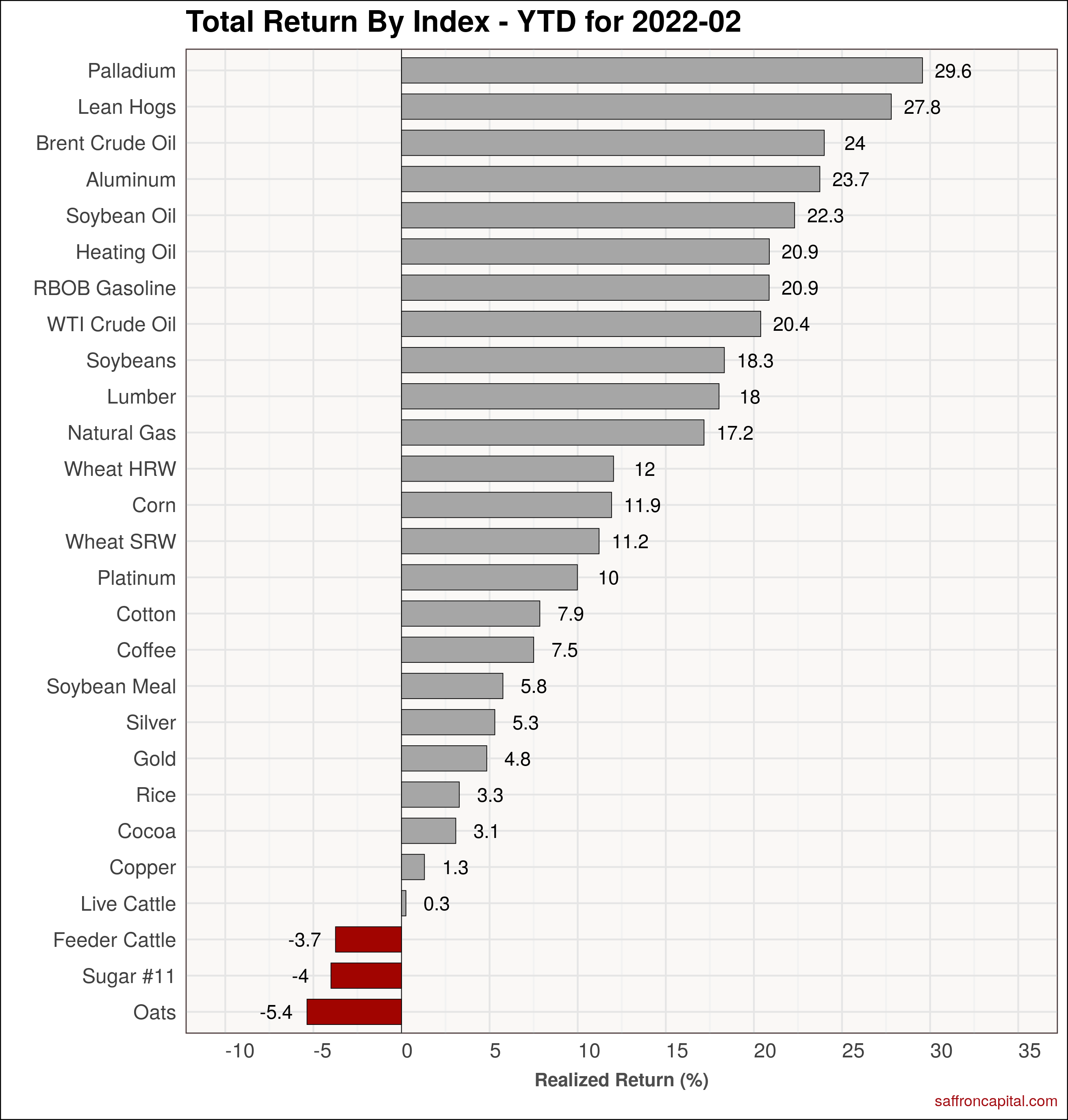

Commodities

Next, the fingerprint of the Ukraine crisis was again on display, influencing a number of commodities higher, notably Brent (+7.3%), aluminium (+10.6%), wheat (+12.8%) and lean hogs (+17.6%). In contrast, natural gas at Henry Hub (-5.9%) was not impacted even though LNG exports have been robust. Lumber (+40.4%) again topped the monthly list on high increases in housing permits and forward purchases for spring construction.

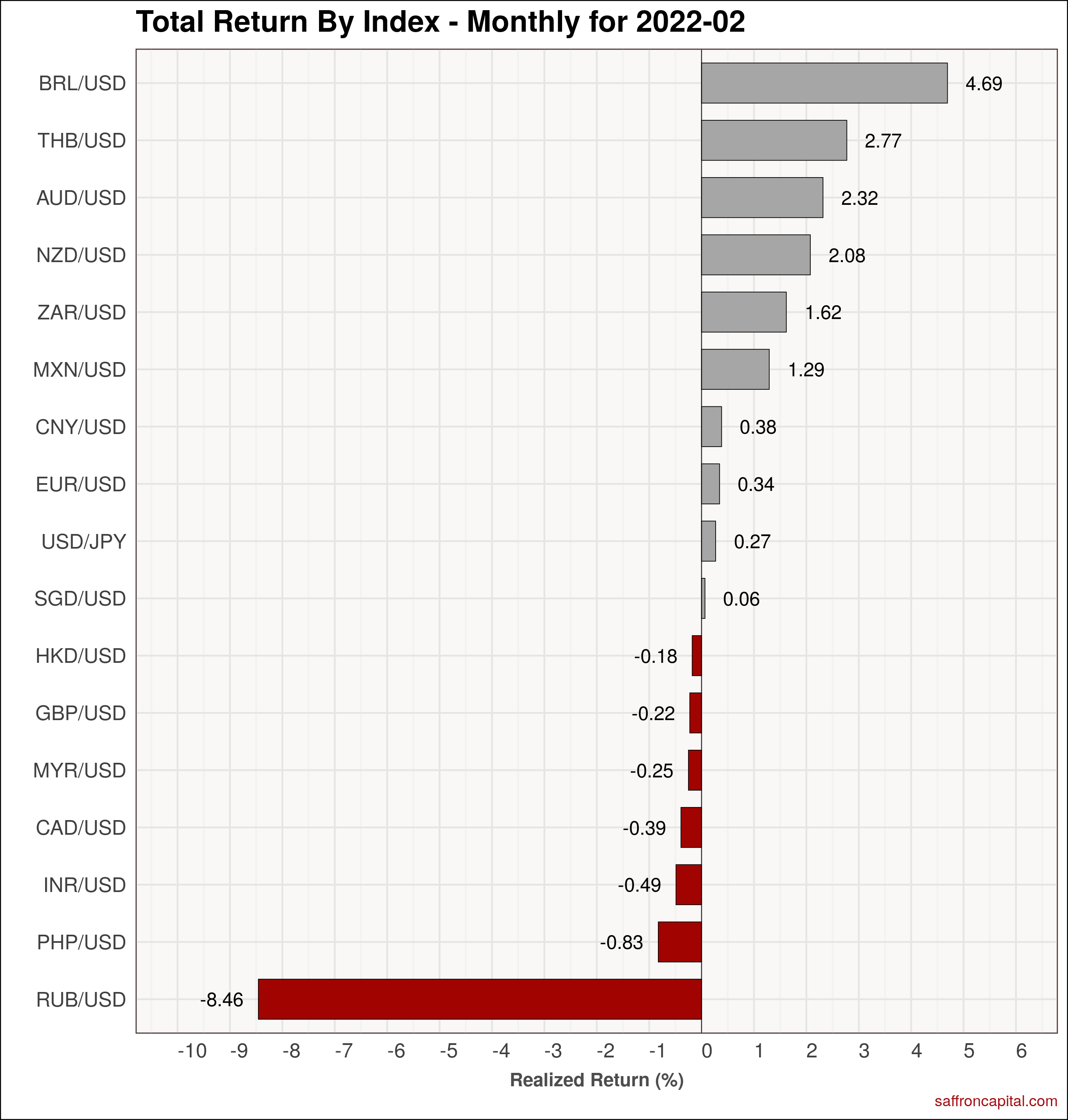

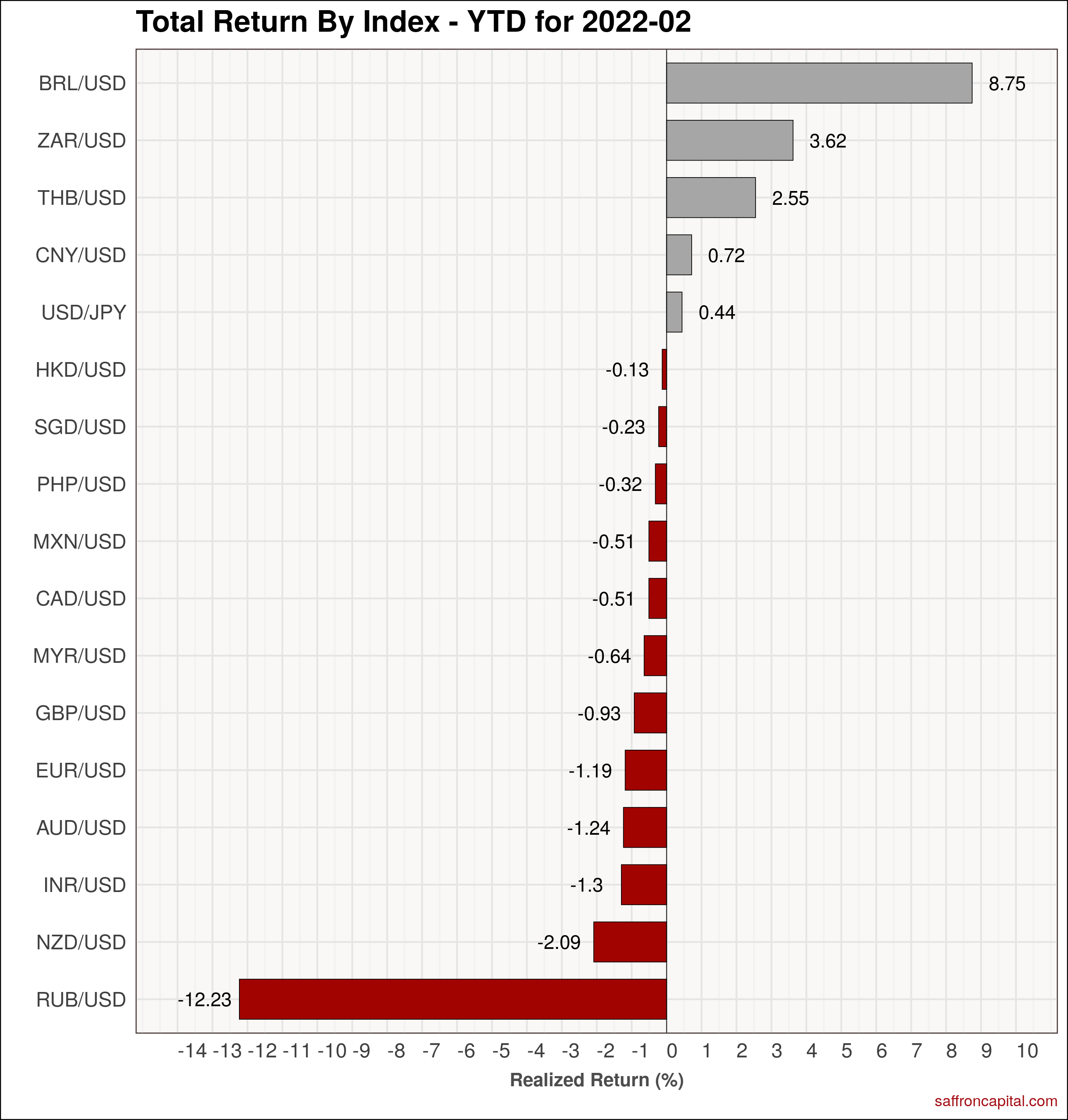

Currencies

The Russian ruble was down 8.5% in February, bringing the year-to-date decline to 12.2%. For the second month, the Brazilian real (+4.67%) led monthly gains and yeat-to-date gains (+8.75%).

{kind=link}

{kind=link}

{kind=link}