June returns for the S&P 500 index had one of the largest drawdowns in the last 10 years. Red ink is evident across all major asset classes. US equity indexes have now fallen 4 out of the first 6 months of the year, while US treasuries and corporate bonds fell in all 6 months. Equity indices for Developed and Emerging Markets fared no better with only a small number of countries showing gains. The US Dollar continued to rise in response to rising interest rates, while a broad-based commodity index dropped for the first time in seven months. The month favored investment strategies structured to benefit from falling prices and active risk management.

The following analysis provides a visual record of June returns.

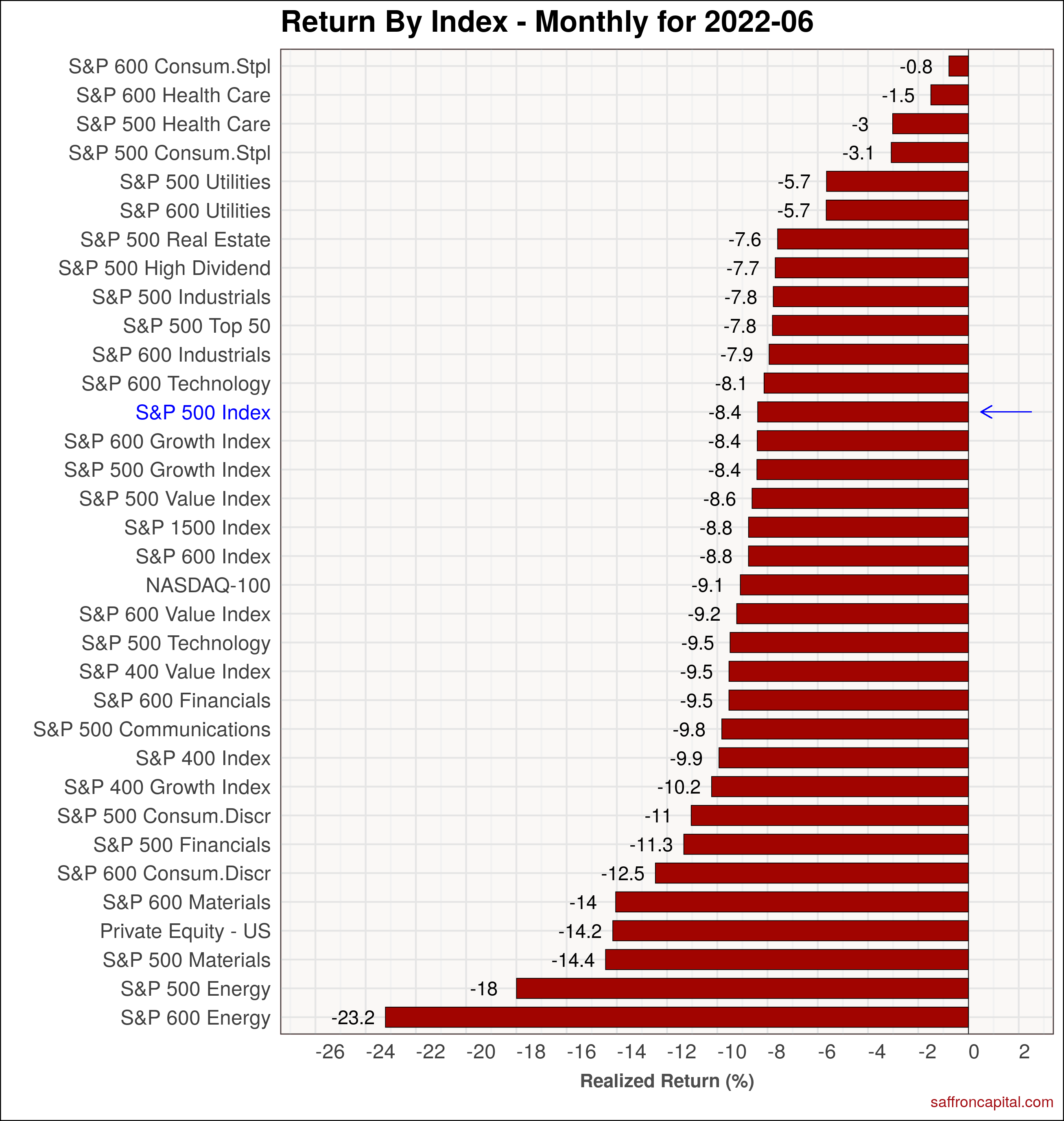

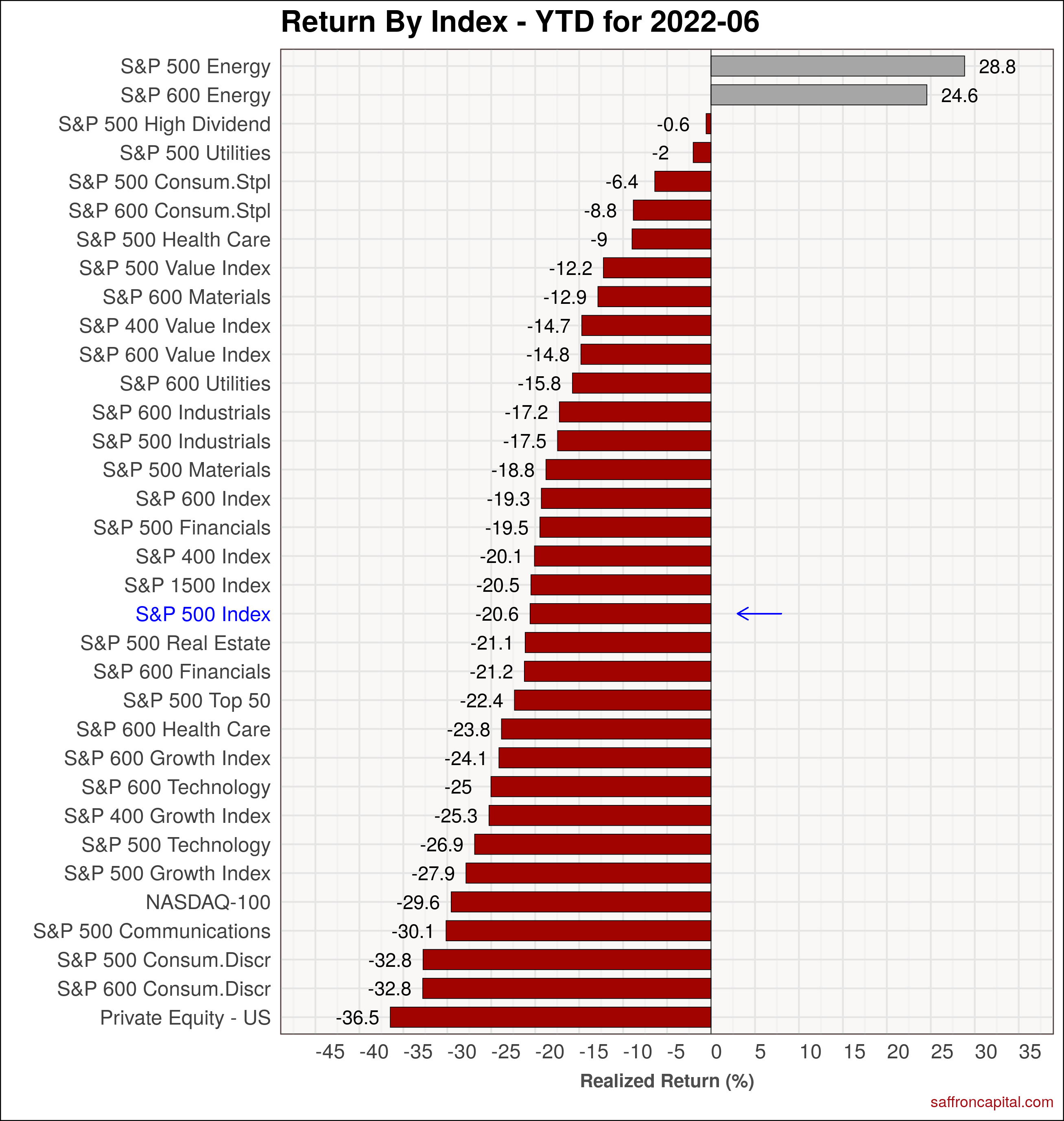

US Equities

June returns for the US S&P 500 index (-8.4%) were pulled down by the Energy (-18%), Materials (-14.4%) and Financial (-11.3%) sectors. Growth (-8.4%) modestly outperformed Value (-8.6%) last month. Safe havens included small cap Consumer Staples (-0.8%) and small cap Healthcare (-1.5%). On a year-to-date (YTD) basis, the S&P 500 index (-20.6%) continues to outperform strategic sectors, including Technology (-26.9%), Communications (-30.1%), and Consumer Discretionary (-32.8%) shares. Private equity investing (-36.5%) has been wrecked. The top performers since January are large cap Energy (+28.8%), small cap Energy (+24.6%), and high dividend stocks (-0.6%).

Click to enlarge

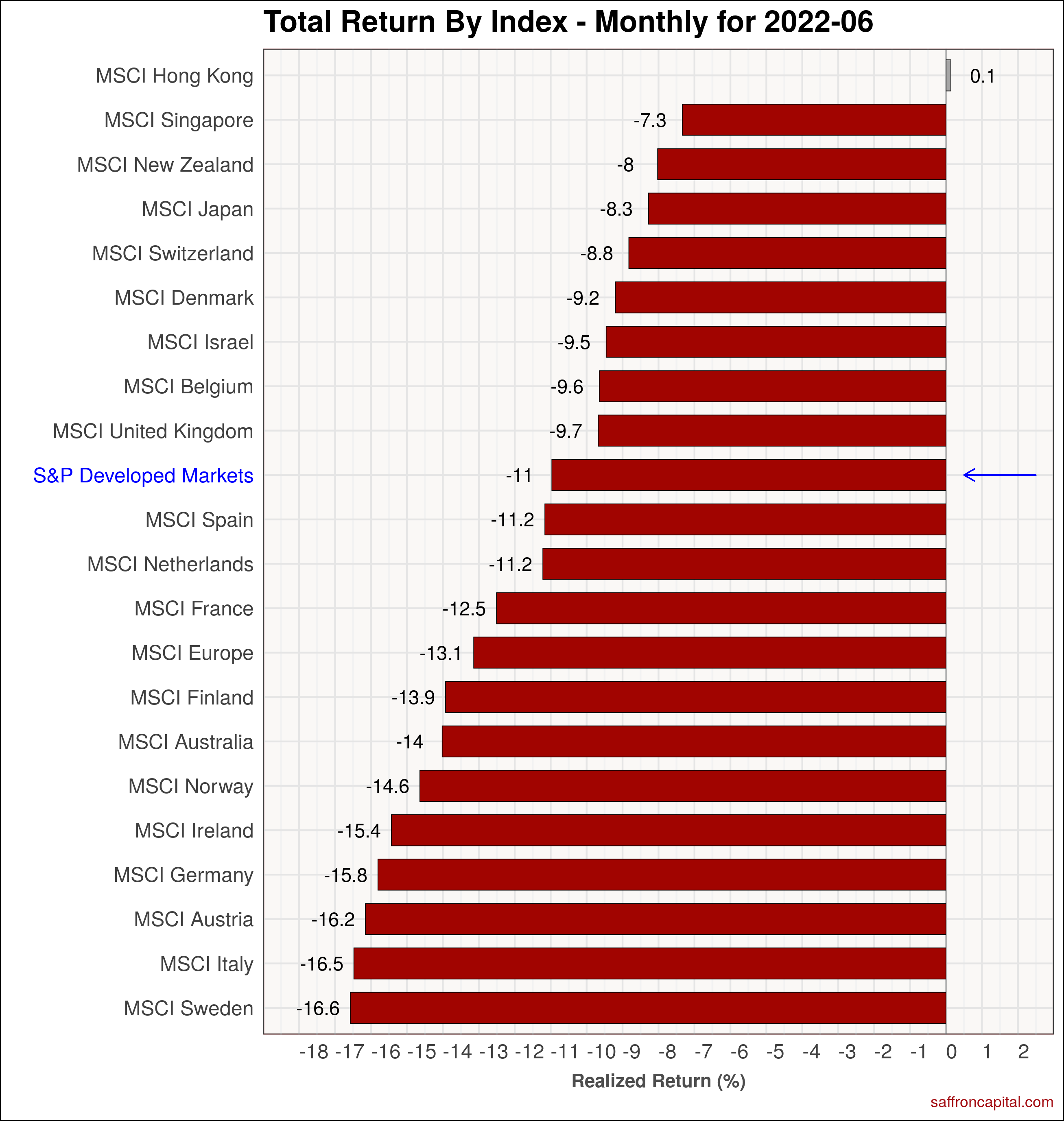

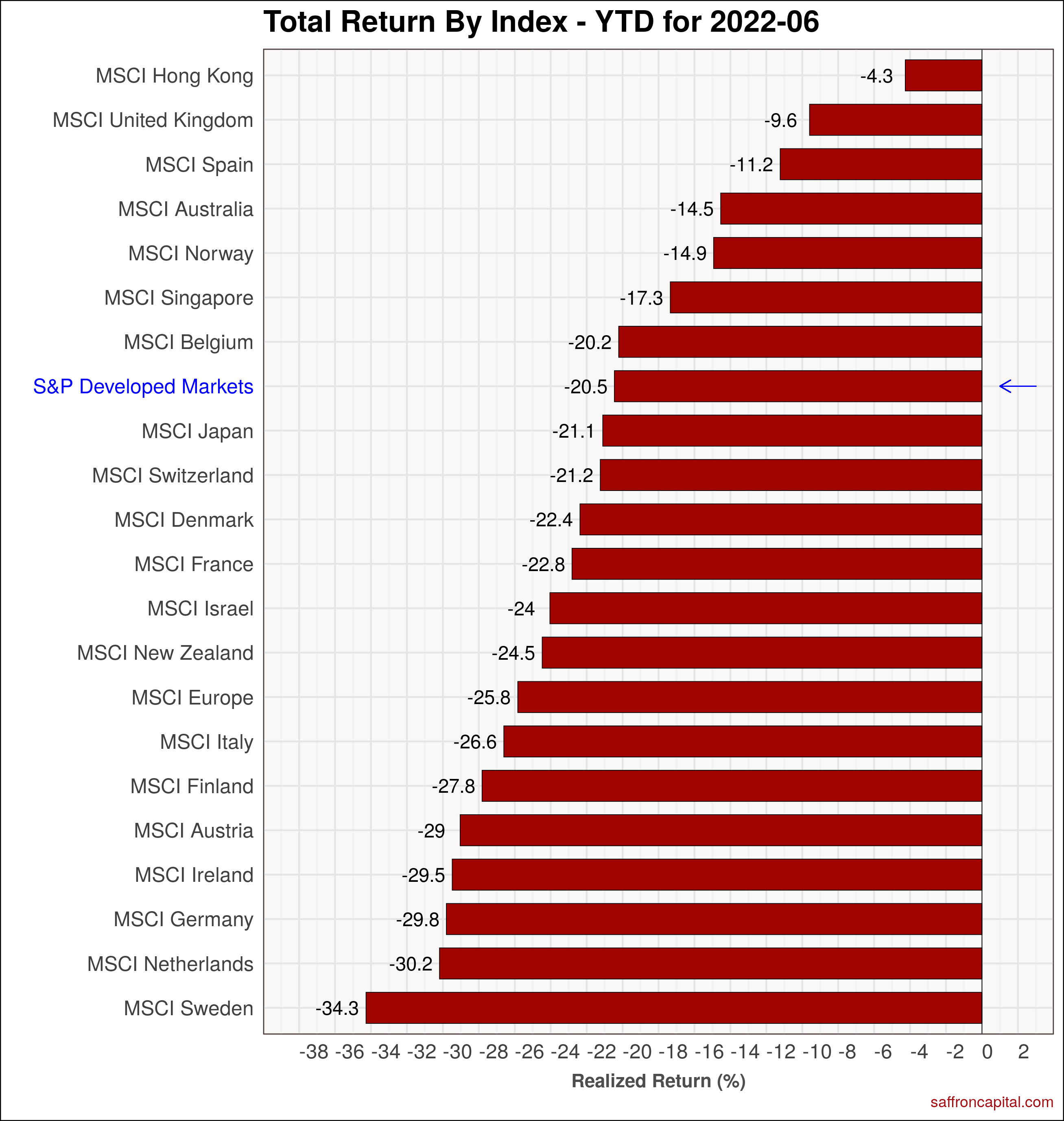

Developed Market Equities

Elsewhere, equity markets were negative across the developed economies. The S&P Developed Markets index (-11.0%) under-performed the S&P 500 index by 240 basis points (bps). Hong Kong (+0.1%) and Singapore (-7.3%) topped the chart, with Italy (-16.5%) and Sweden (-16.6%) showing steepest losses. Meanwhile, on a YTD basis, the Developed Market index (–20.5%) matches the performance of the S&P 500 Index. The best performers are Hong Kong (-4.3%), and the United Kingdom (-9.6%).

Click to enlarge

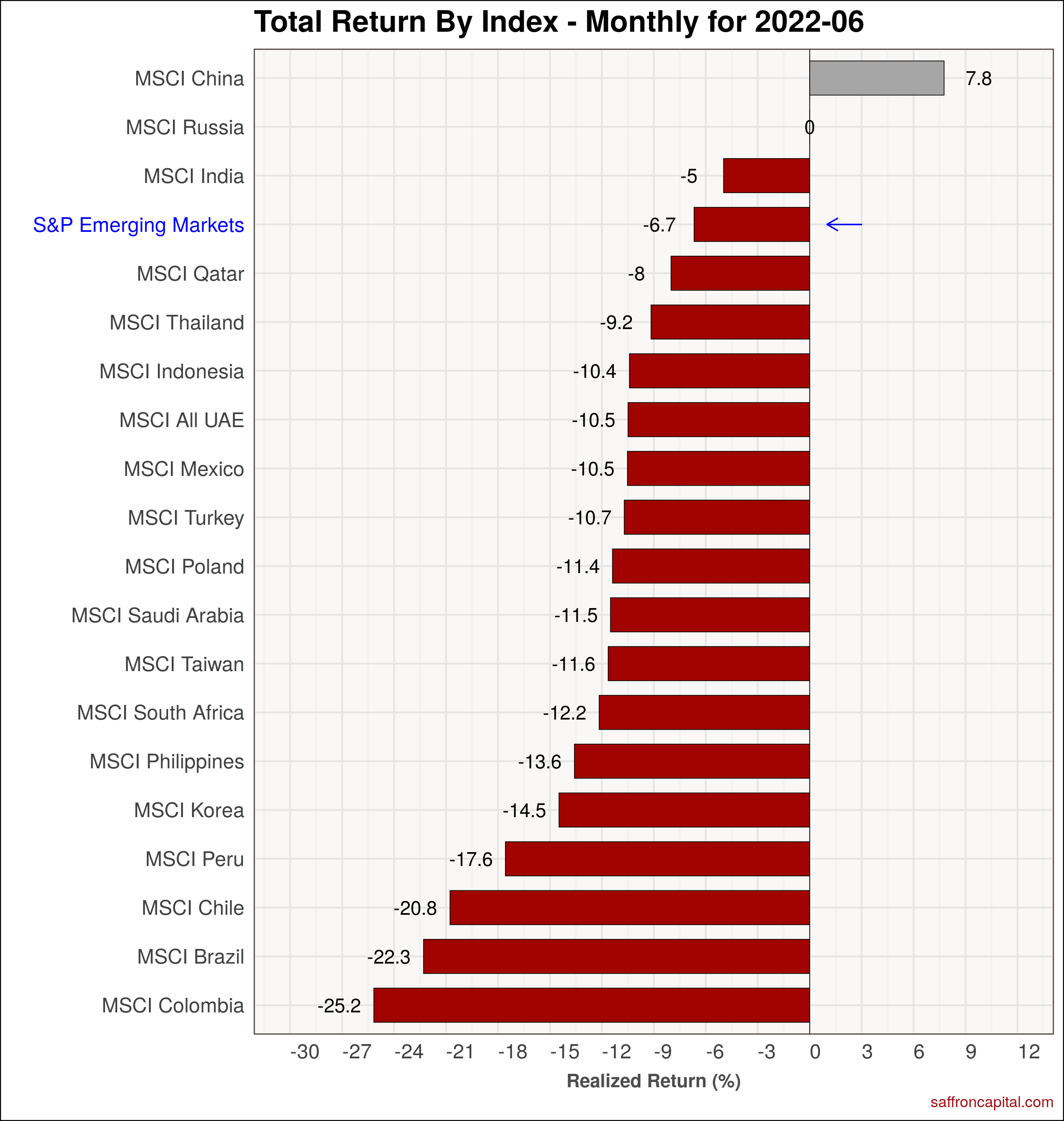

Emerging Market Equities

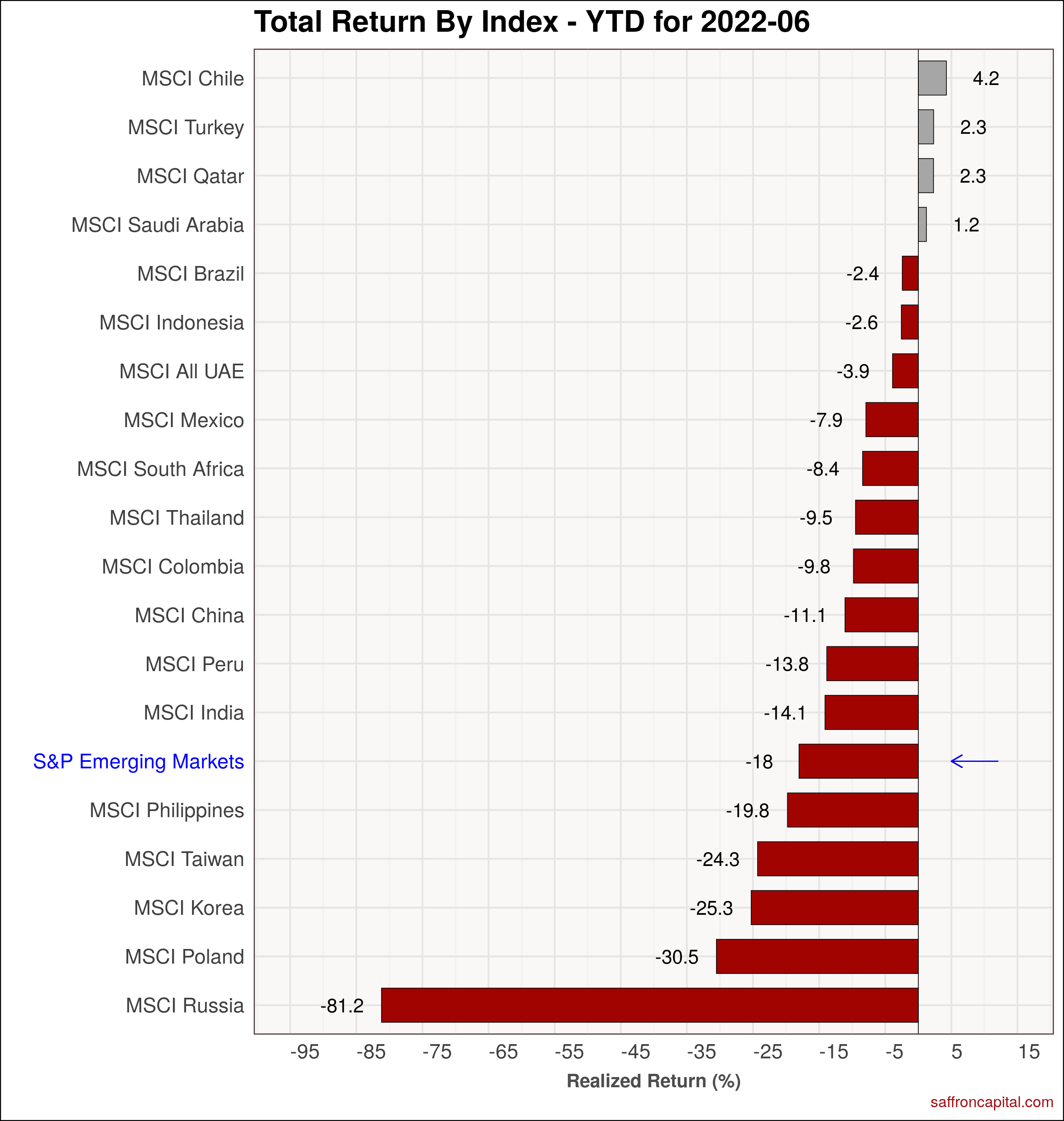

The S&P Emerging Markets Index (-6.7%) outperformed the S&P 500 index by 170 bps in June. The indices for China (+7.8%) and India (-5.0%) were the only ones to be beat the group benchmark. The chart confirms that many markets suffered in June, notably, natural resource exporters, Asian, and South American markets. On a year to date basis, several markets still have positive returns, including Chile (+4.2%), Turkey (+2.3%), Qatar (+2.3%), and Saudi Arabia (+1.2%). The Emerging Market Index has outperformed U.S large cap stocks by 206 bps since January. The Indian stock markets (-14.1%), while down significantly, outpaced most Developed Markets, including the U.S. since the start of the year. NOTE: values for the Russian stock market have not been updated since March 2022.

–

Click to enlarge

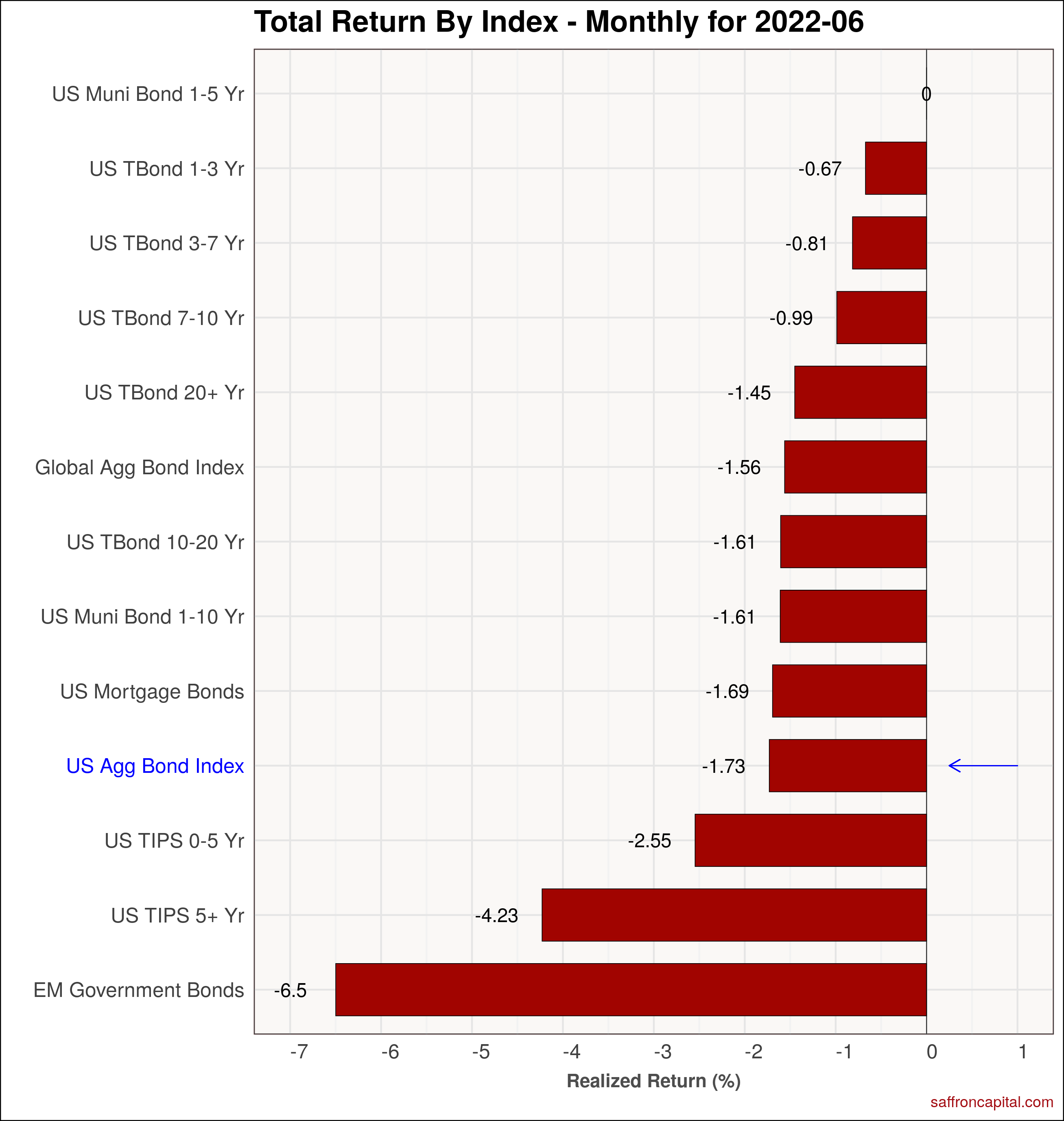

Government Bonds

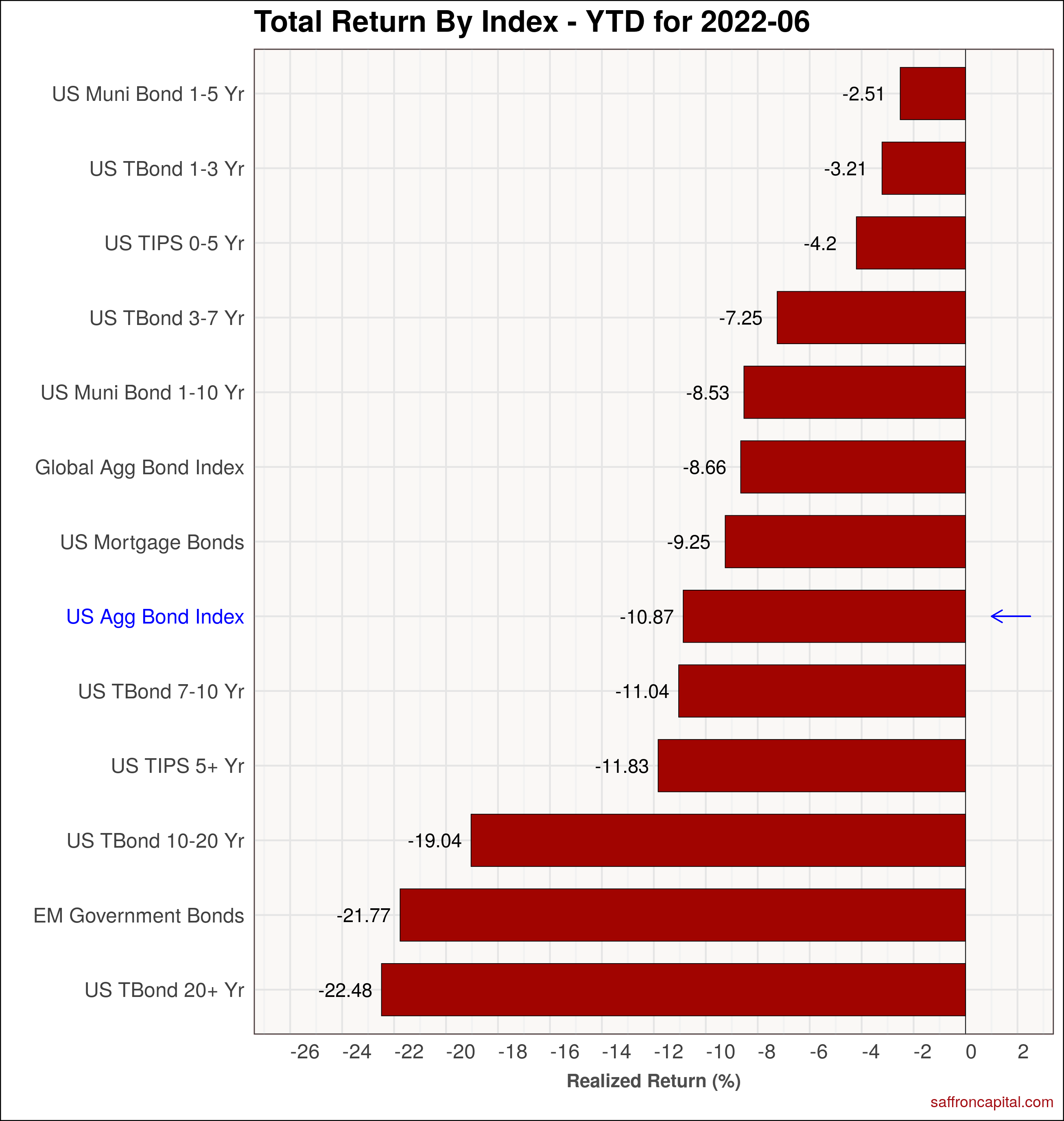

Government bonds were hard hit in the first part of June as market focus on inflation and the Fed pivot peaked, and then bonds rallied dramatically in response to increased recessionary fears. The US Aggregate Bond Index (-1.73%) trailed the Global Aggregate Bond Index (-1.56%), and both indices avoided the large losses in US equities. On a year-to-date basis, US Treasury bonds (-22.48%) and Emerging Market bonds (-21.77%) proved riskier than U.S. equities.

Click to enlarge

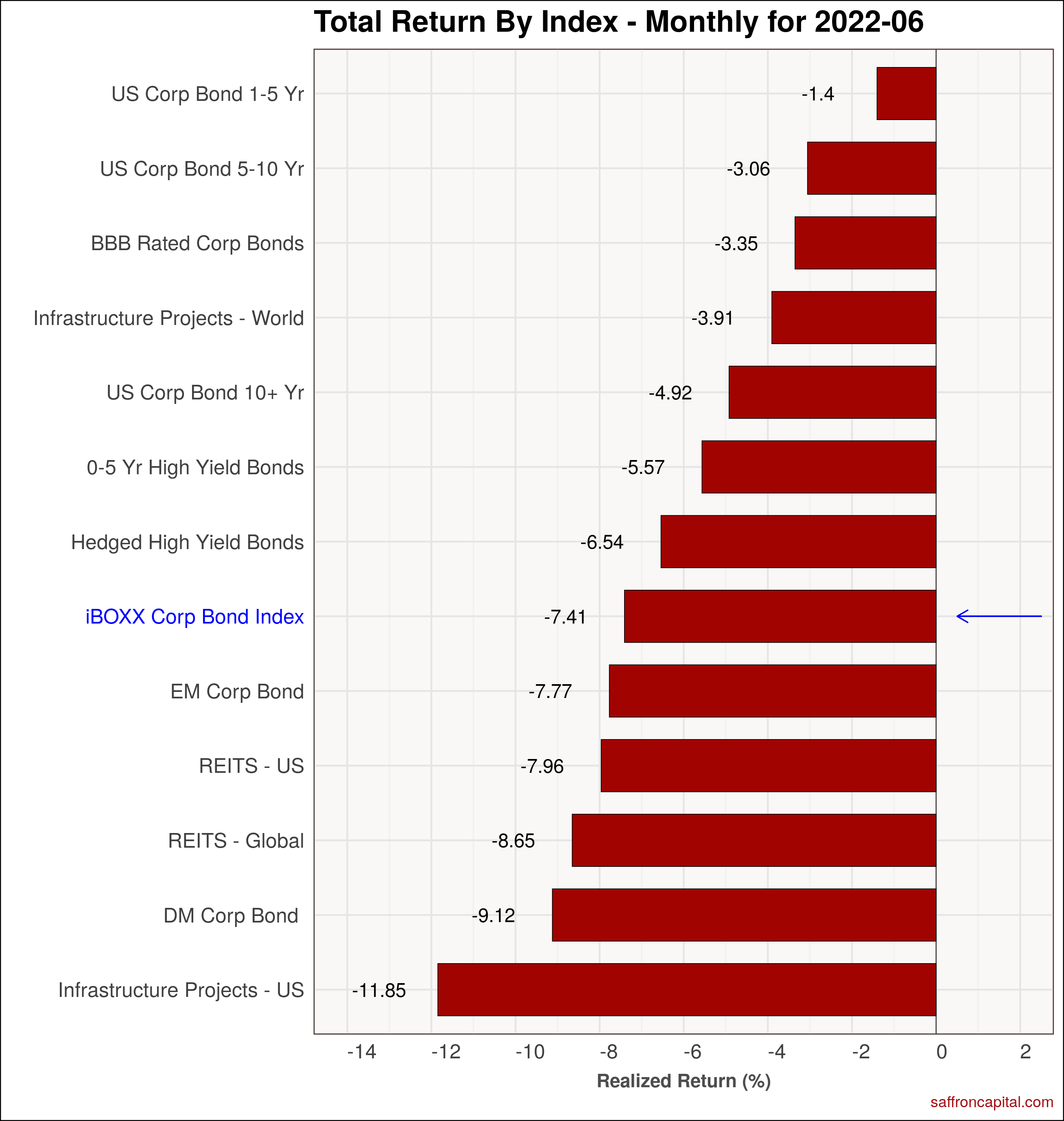

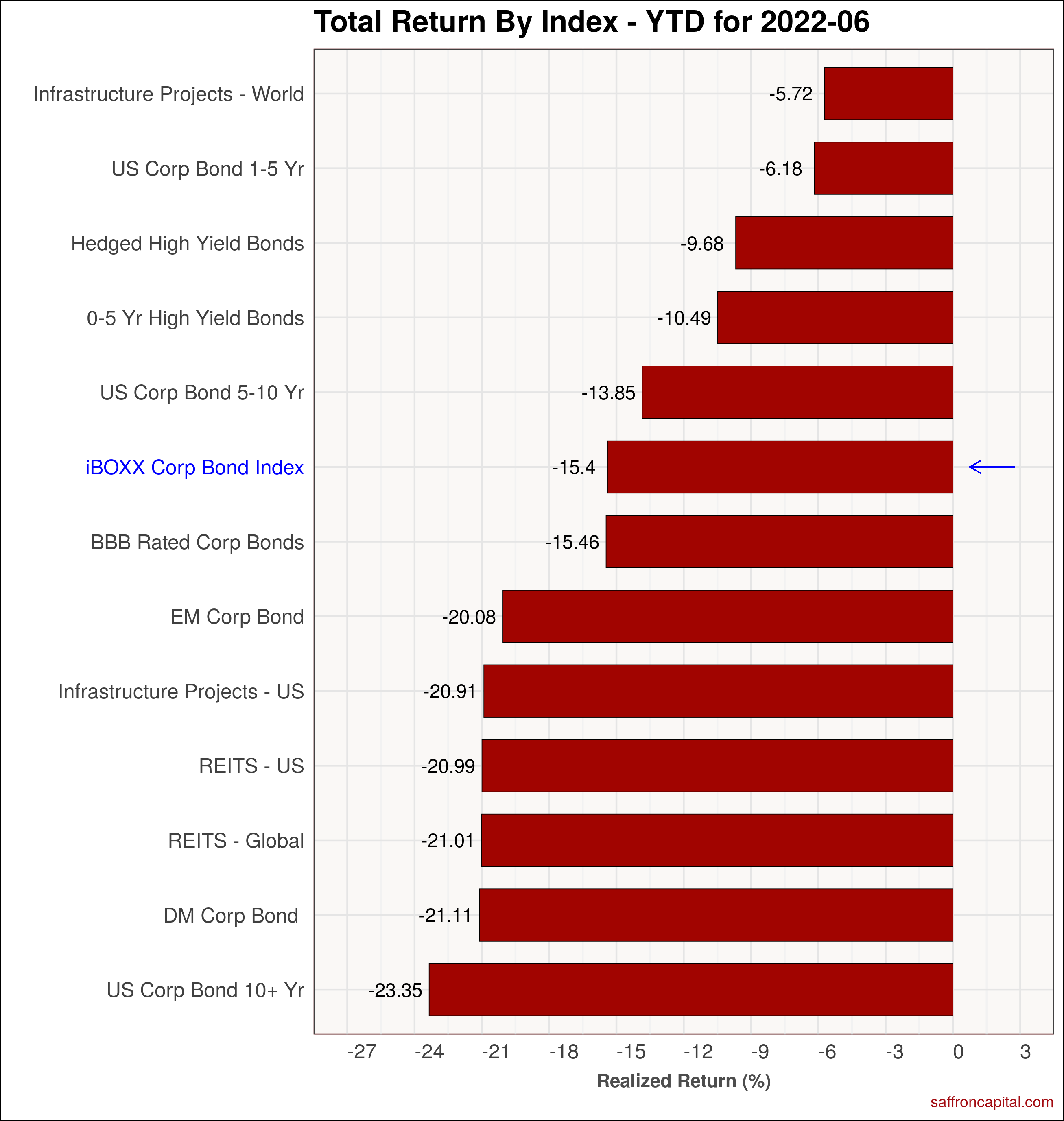

Corporate & Infrastructure Bonds

June returns were negative for both high-quality and high-yield corporate bonds. The iBOXX Corporate Bond Index (-7.41%) outperformed U.S. equities by 100 bps. Real Estate Investment Trusts (-7.96%) in the U.S. lagged index, as did Infrastructure Project Bonds (-11.85%). The best performers on a YTD basis are international Infrastructure Project Bonds (-5.72%) and short term U.S. Corporate Bonds (-6.16%).

Click to enlarge

Commodities

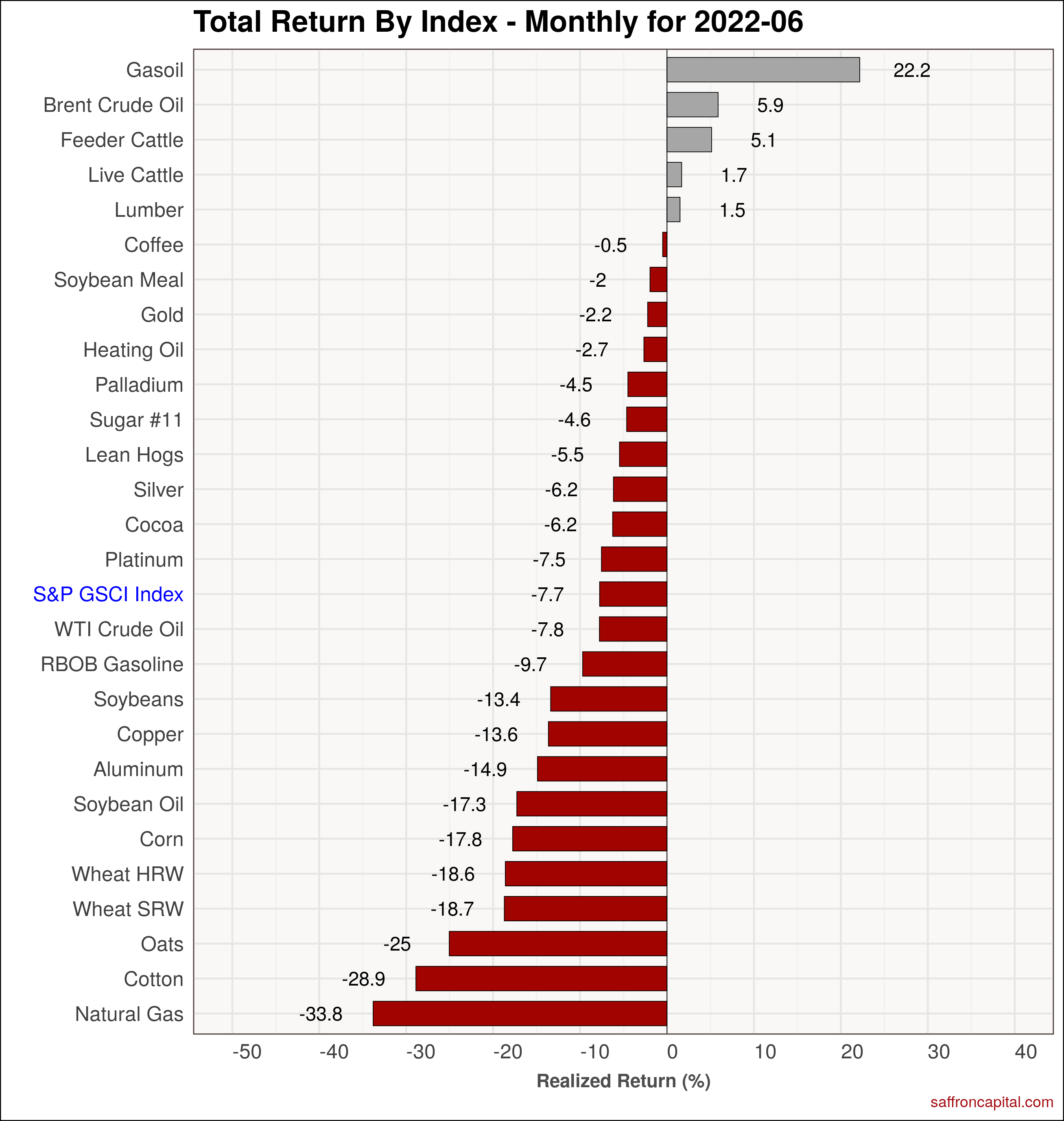

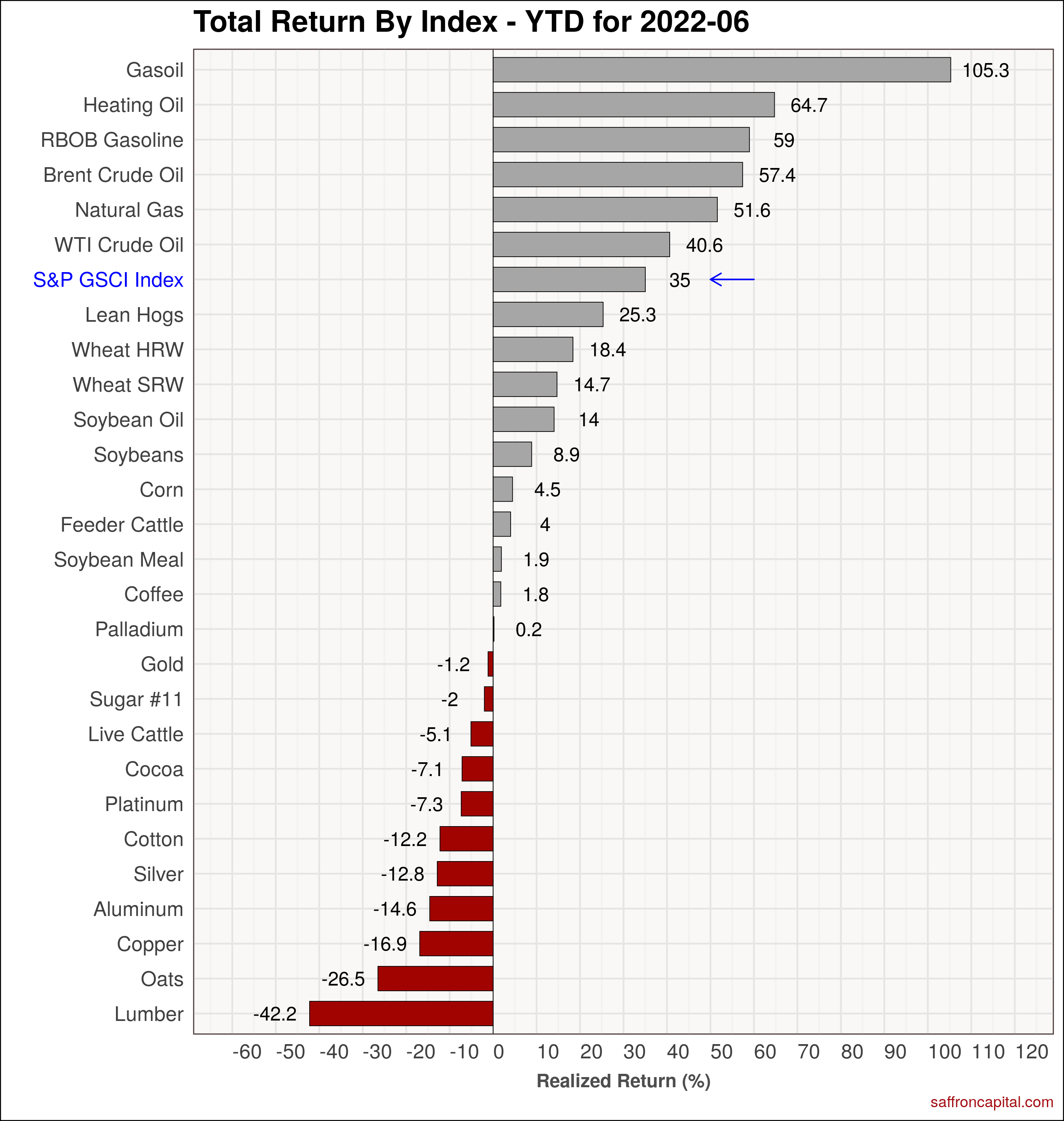

June returns for commodities were again dominated by energy, notably European Gasoil (+22.2%) and Brent Crude Oil (+5.9%). Meat (+1.6%) and Lumber (+1.5%) also saw positive returns. Overall, the S&P GSCI Index (-7.8%) declined for the first time in seven months. Price declines were most evident in wholesale Natural Gas (-33.8%), Cotton (-28.9%), and Oats (-25%). The S&P GSCI Index is still up (+35.0%) on a YTD basis, with energy markets outperforming all others.

Click to enlarge

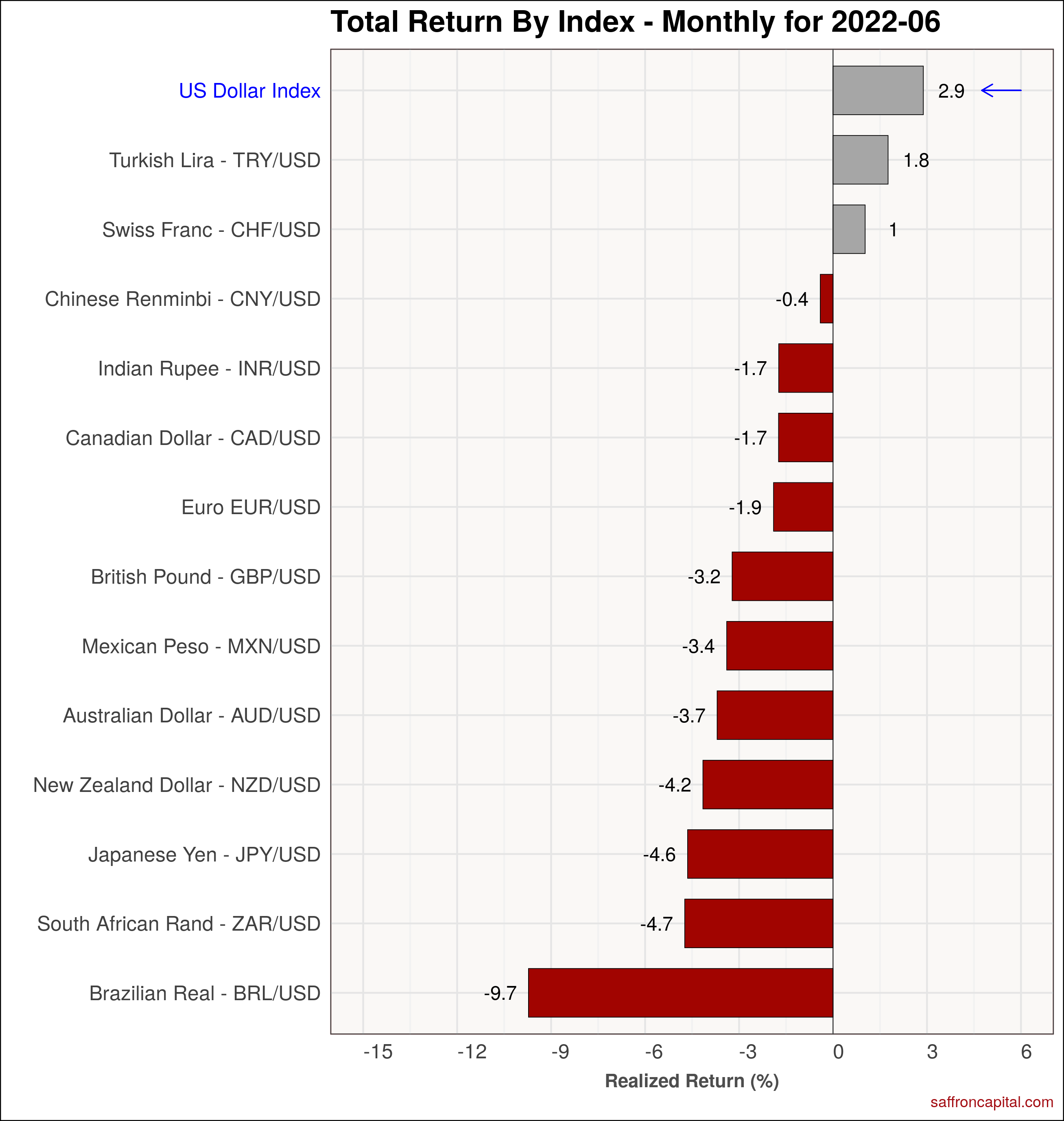

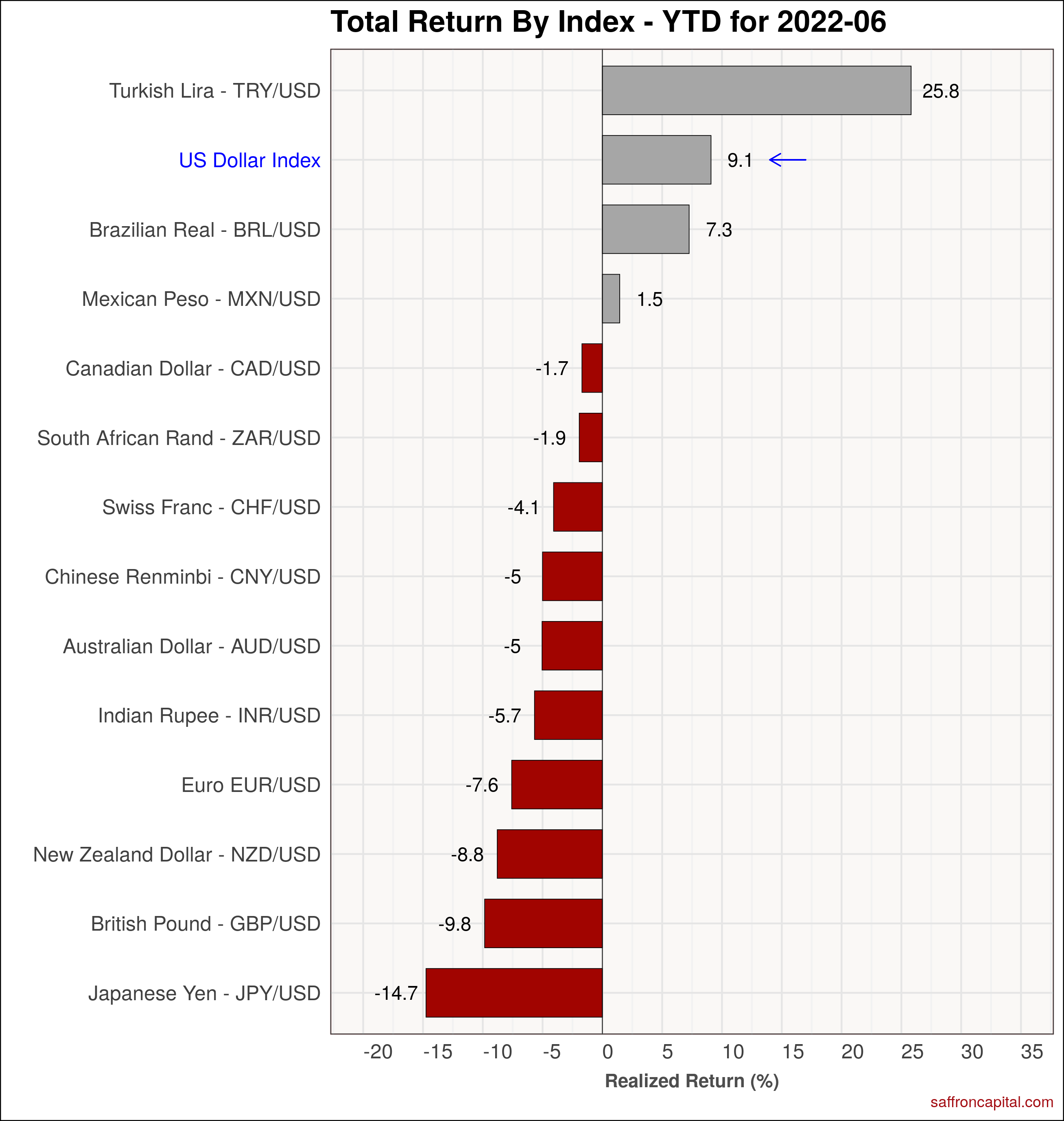

Currencies

The US Dollar (+2.9%) rose in June, negatively impacting most currencies, with the exception of the Turkish Lira (+1.8%) and the Swiss Franc (+1.0%). Since January, the Yen (-14.7%) has fallen the most, followed by Pound Sterling (-9.8%). Declines since January are also evident in the Chinese Yuan (-5.0%) and the Indian Rupee (-5.7%).

Click to enlarge

Have questions about the performance and investment plan for your portfolio? Schedule a call or meeting with us here.

{kind=link}

{kind=link}

{kind=link}