July returns for the S&P 500 index were positive for the second month this year. In fact, we saw the best returns seen since April 2020. Gains were evident across all major asset classes, though results varied by index. For example, US equity indexes outperformed the gains in developing and emerging markets. Meanwhile, US government bonds lagged the gains seen international soverign bonds, emerging market bonds and high yield binds. Finally, The US Dollar continued to rise in response to rising interest rates, while a broad-based commodity index dropped for the second month in a row.

The following analysis provides a visual record of July returns and is intended to assist invetsor’s with performance benchmarking.

US Equities

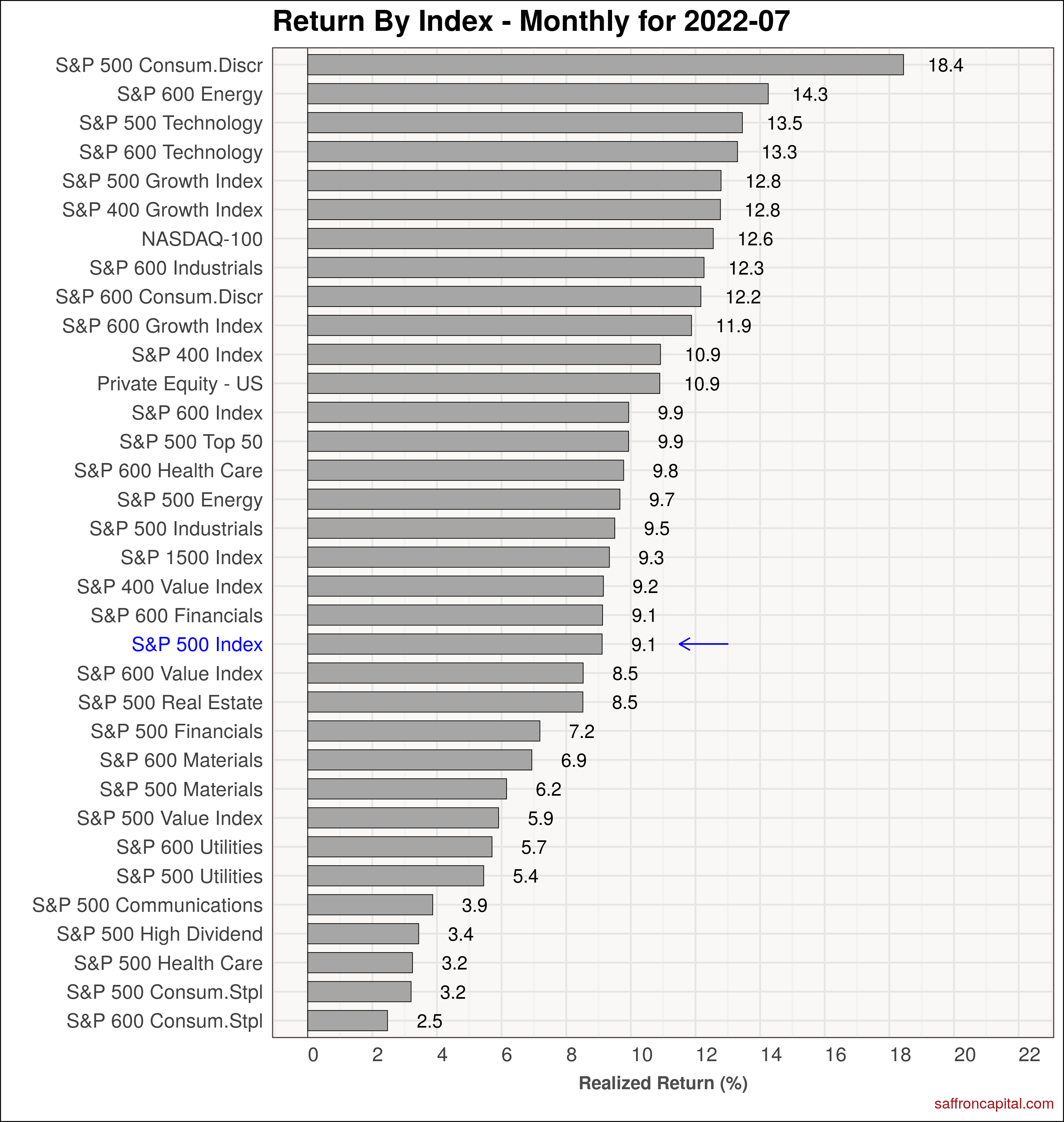

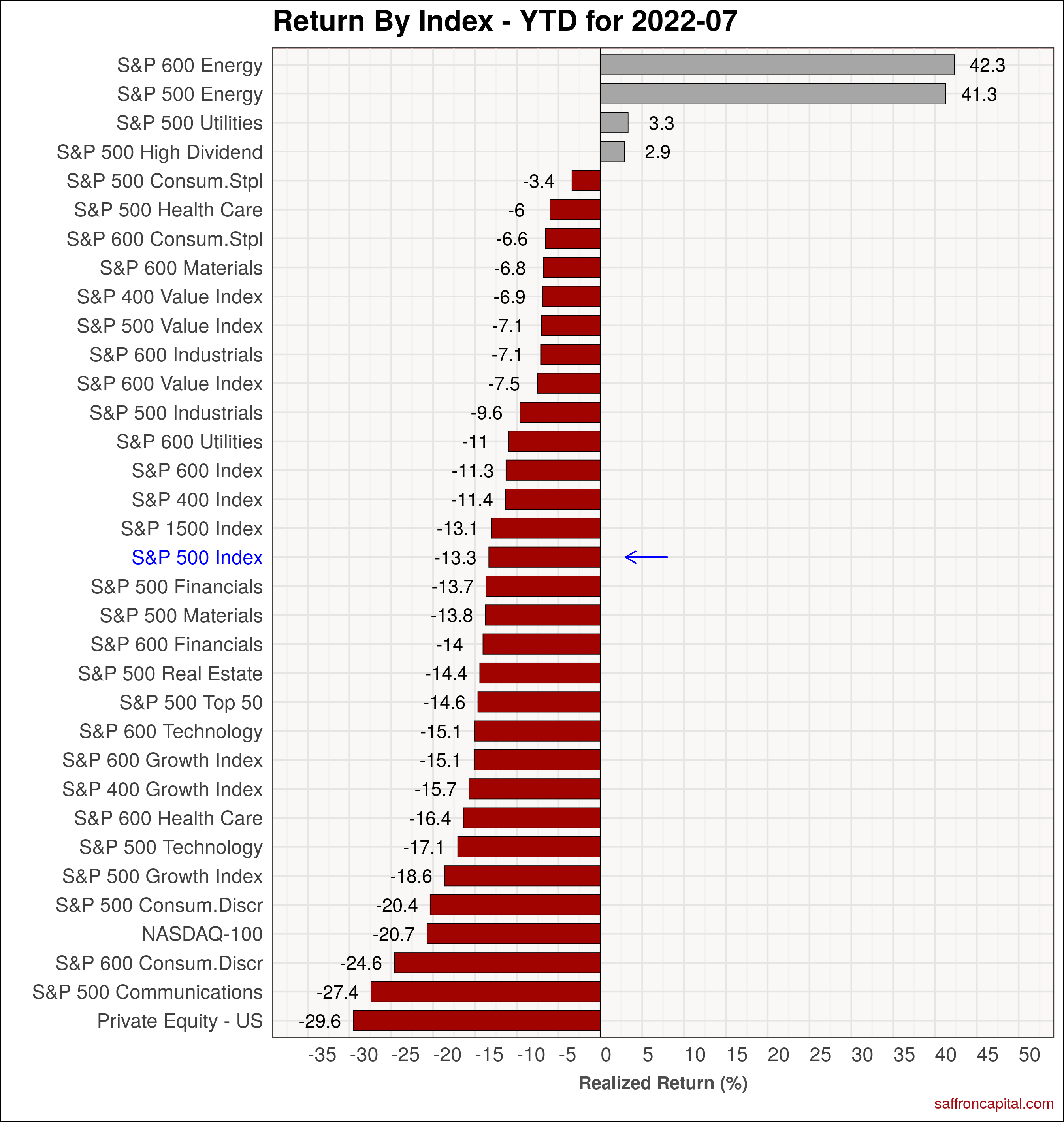

June returns for the large cap S&P 500 index (+9.1%) were led by strong gains in Consumer Discretionary (+18.4%), Technology (+13.5%) and Industrial (+12.3%) shares. By extension, Growth (+12.8%) stocks significantly outperformed Value (5.9%). On a year-to-date (YTD) basis, the S&P 500 index (-13.3%) continues to outperform strategic sectors, including Technology (-15.1%), Consumer Discretionary (-20.4%) and Communications (-27.4%), and shares. The top performers since January are small cap energy (+42.3%), large cap Energy (+41.3%), and large cap Utilities (+3.3%), and high dividend stocks (+2.9%).

Click to enlarge

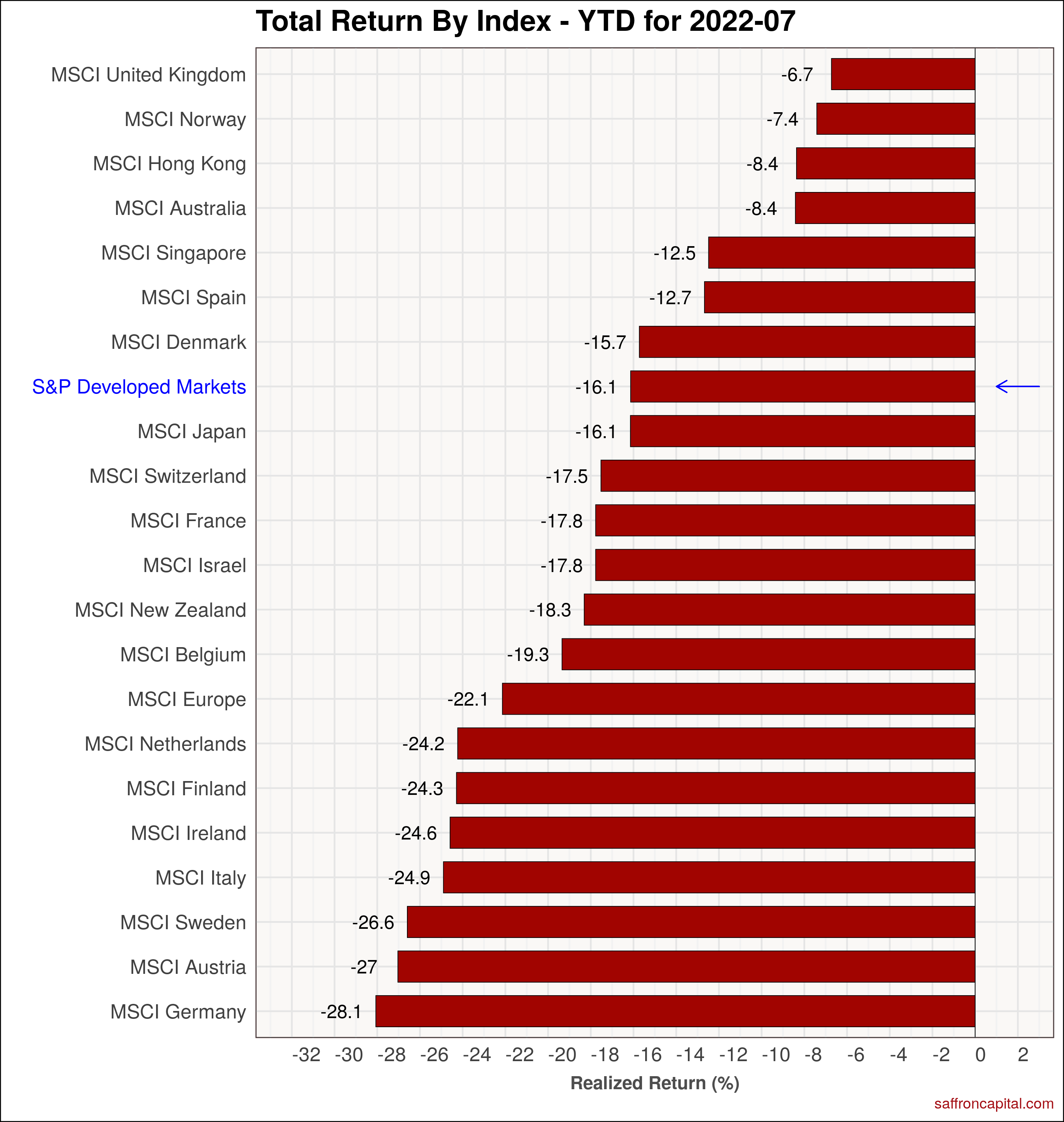

Developed Market Equities

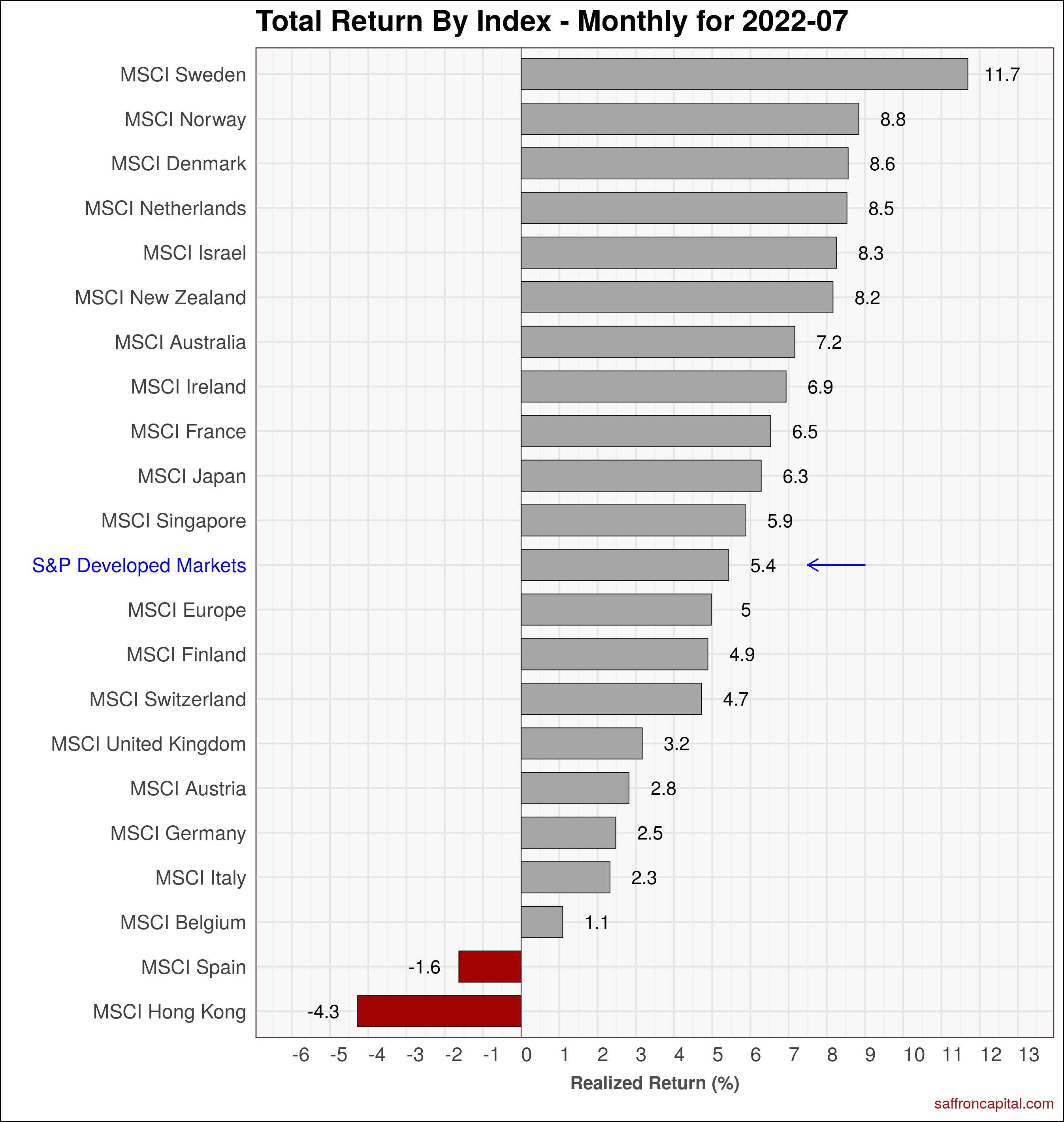

Elsewhere, equity markets were broadly positive . Specifically, the S&P Developed Markets index (+5.4%) had solid gains, but lagged the S&P 500 index by 370 bps in July. Markets in Sweden (+11.7%), Norway (+8.8%) and Denmark (+8.6%) led the pack. In contrast. the only negative markets were Hong Kong (-4.3%) and Spain (-1.6%). On a year to date basis, the red ink continues across the board. The Developed Markets index (-16.1%) is lead by gains in the United Kingdom (-6.7%), Norway (-7.4%) and Hong Kong (-8.4%). The markets with the worse performance since January include Sweden (-26.6%), Austria (-27.0%) and Germany (-28.1%).

Click to enlarge

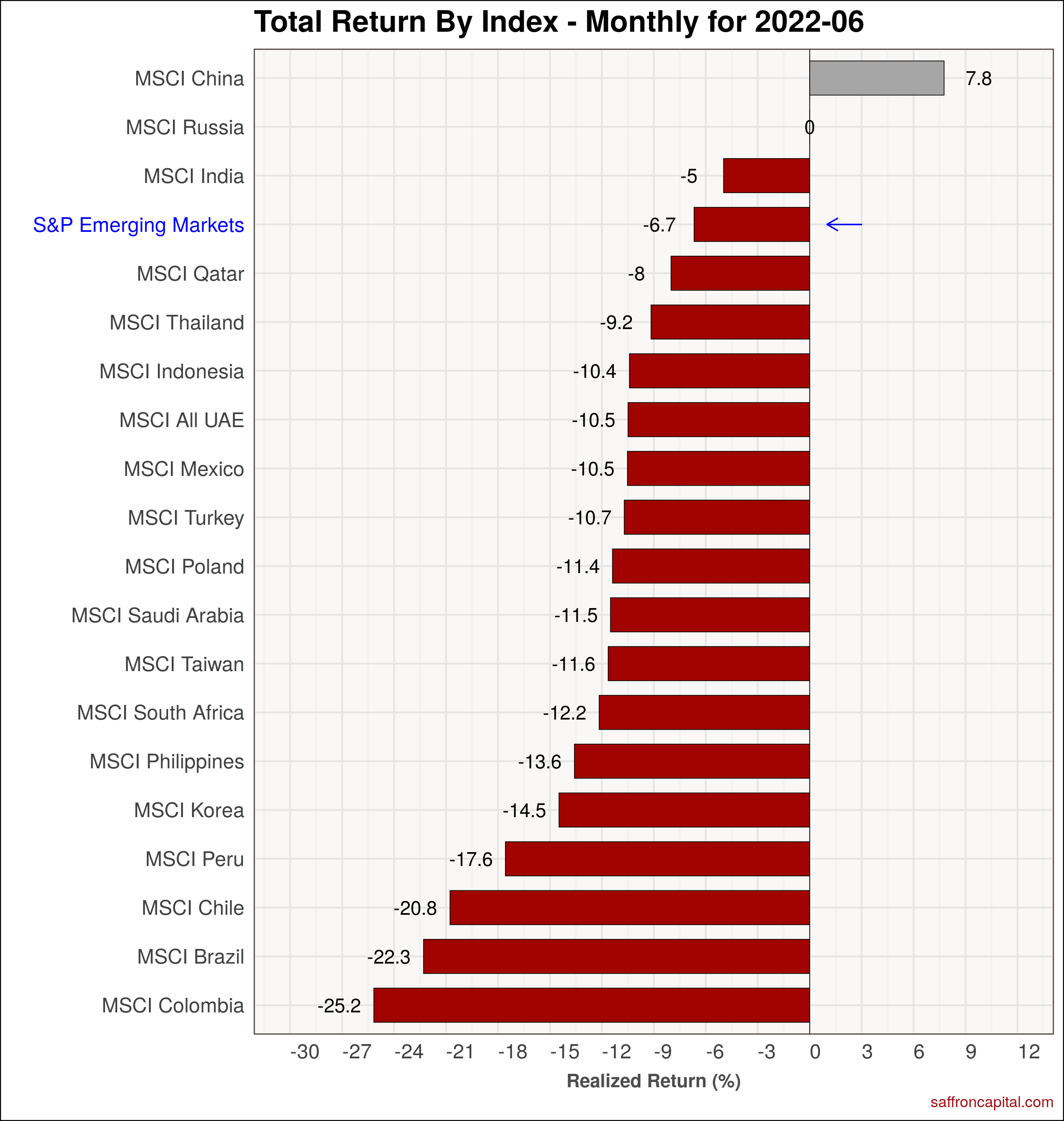

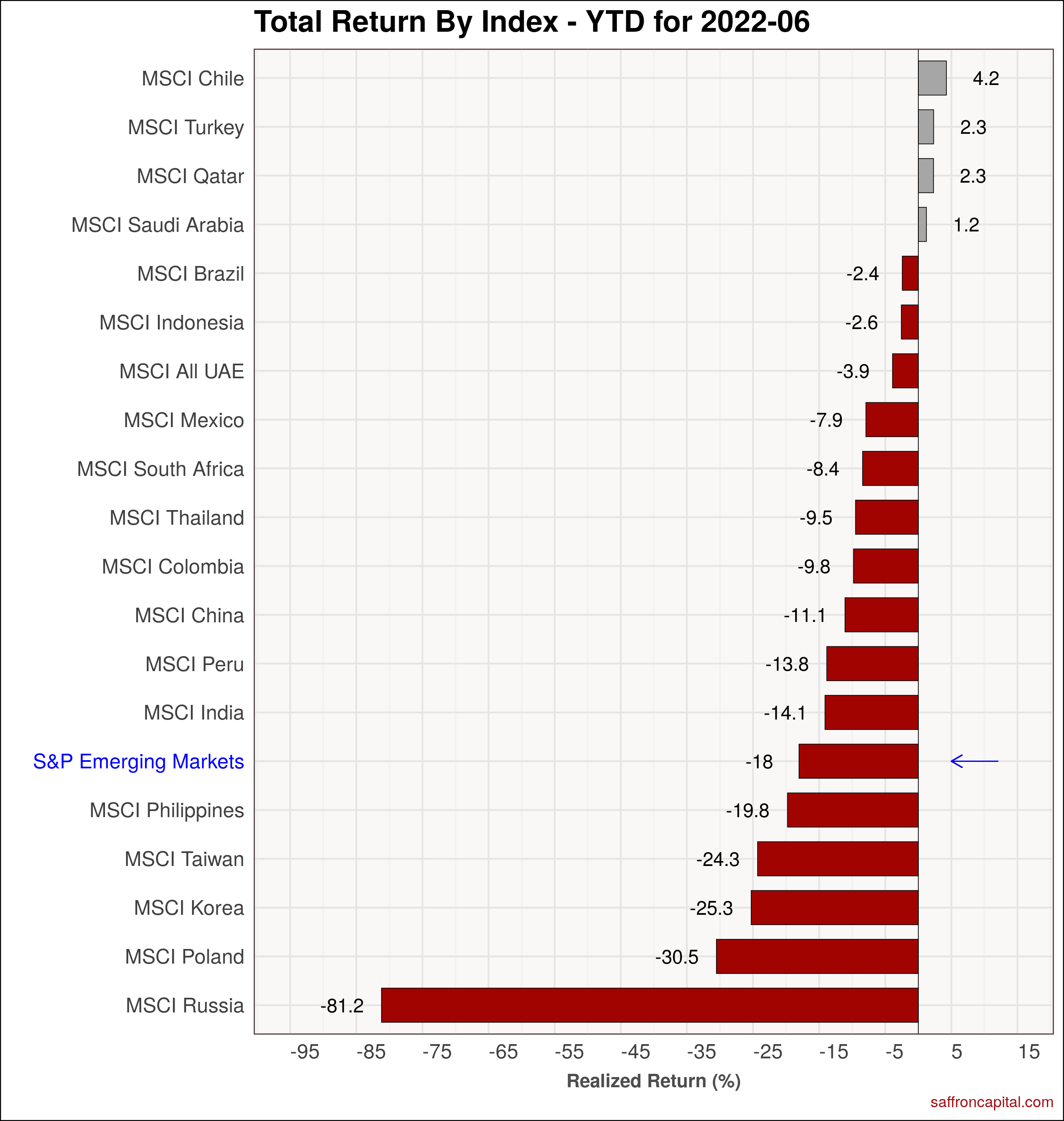

Emerging Market Equities

The S&P Emerging Markets Index (+0.0%) was unchanged in July. The strongest markets were Chile (+9.8%), India (+8.4%) and Saudi Arabia (+6.5%). China (-11.0%) was the outlier in July, lagging all other emerging markets. On a year to date basis, the emerging market index (-18.0%) remains down, led by resource rich economies. Next, we see that the Indian stock market (-6.9%) recovered more than 50% of its year-to-date losses in July. Finally, the worse performers are Russia (-81.2%), Poland (-31.6%) and Taiwan (-23.0%).

Click to enlarge

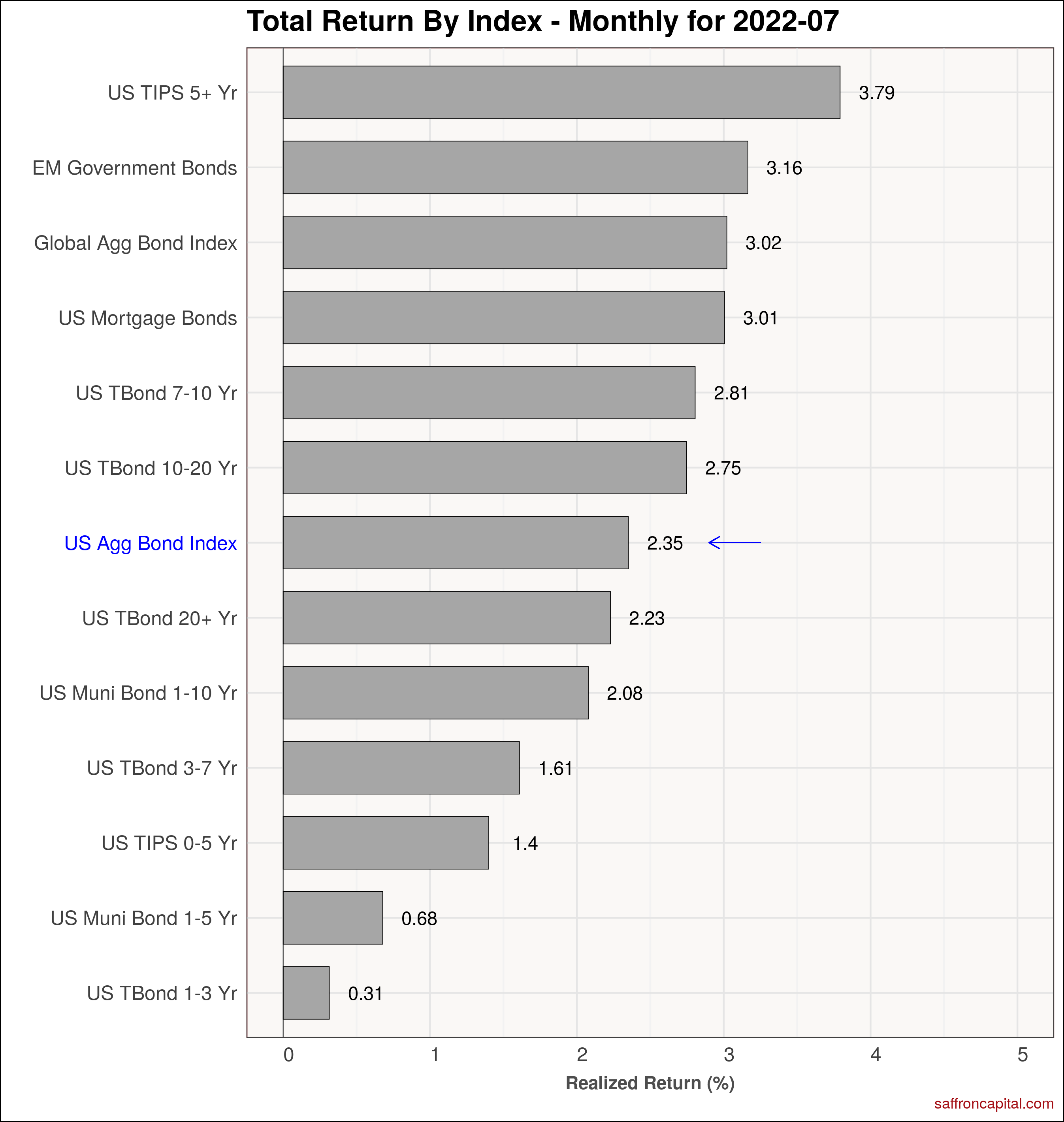

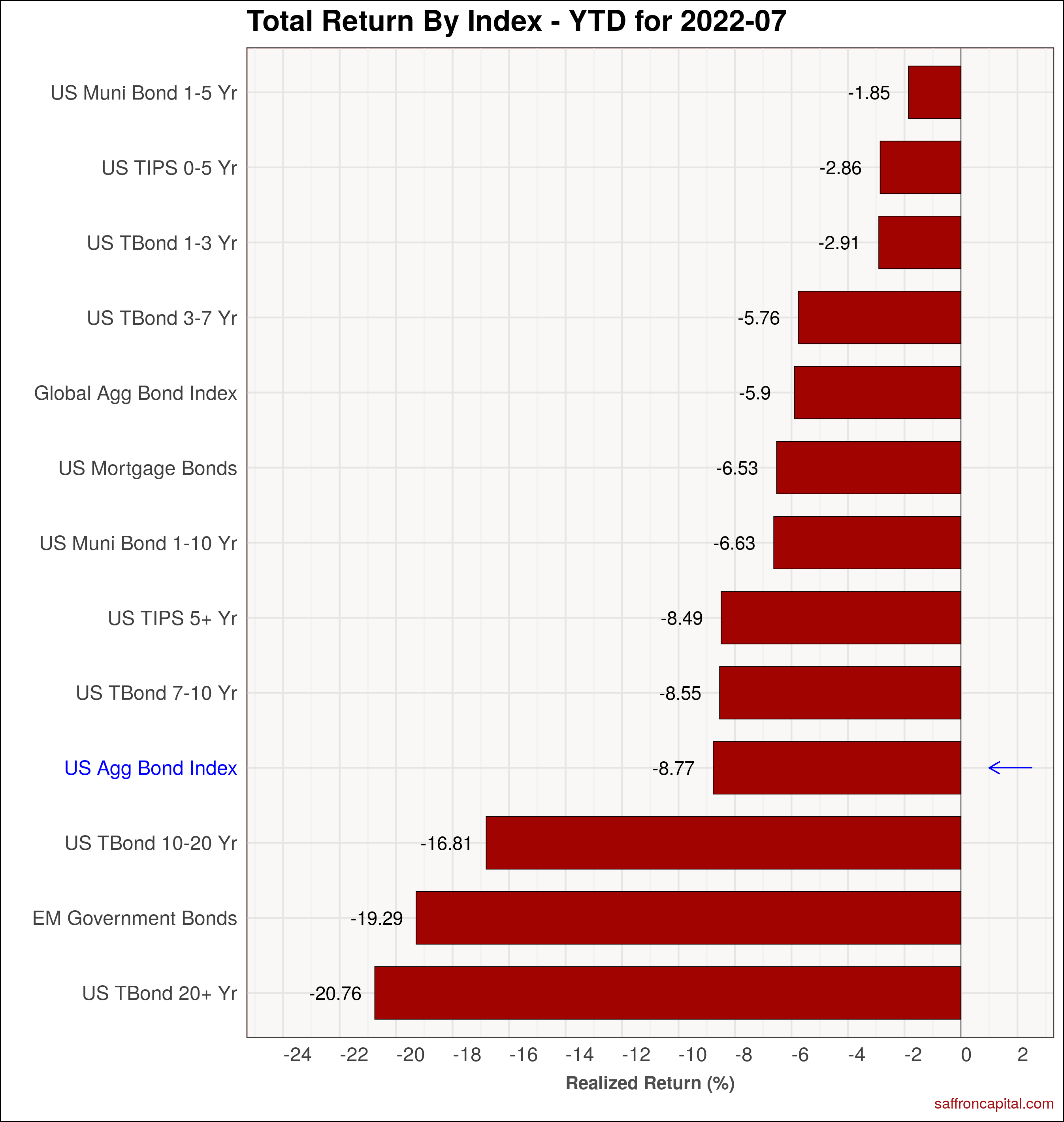

Government Bonds

July returns across the government bond markets were strong as inflation subsided modestly and the market increasingly thinks the Fed pivot will moderate given increased recessionary risks. The US Aggregate Bond Index (+2.35%) trailed the Global Aggregate Bond index (+3.02%) and Emerging Market index (+3.16%). Treasury inflation protected securities (+3.79%) lead the group. On a year-to-date basis, the US aggregate Bond index (-8.77%) is having one of its worse years ever and is being pulled down by long duration US treasuries (-20.76%) and Emerging market (-19.29%) government bonds.

Click to enlarge

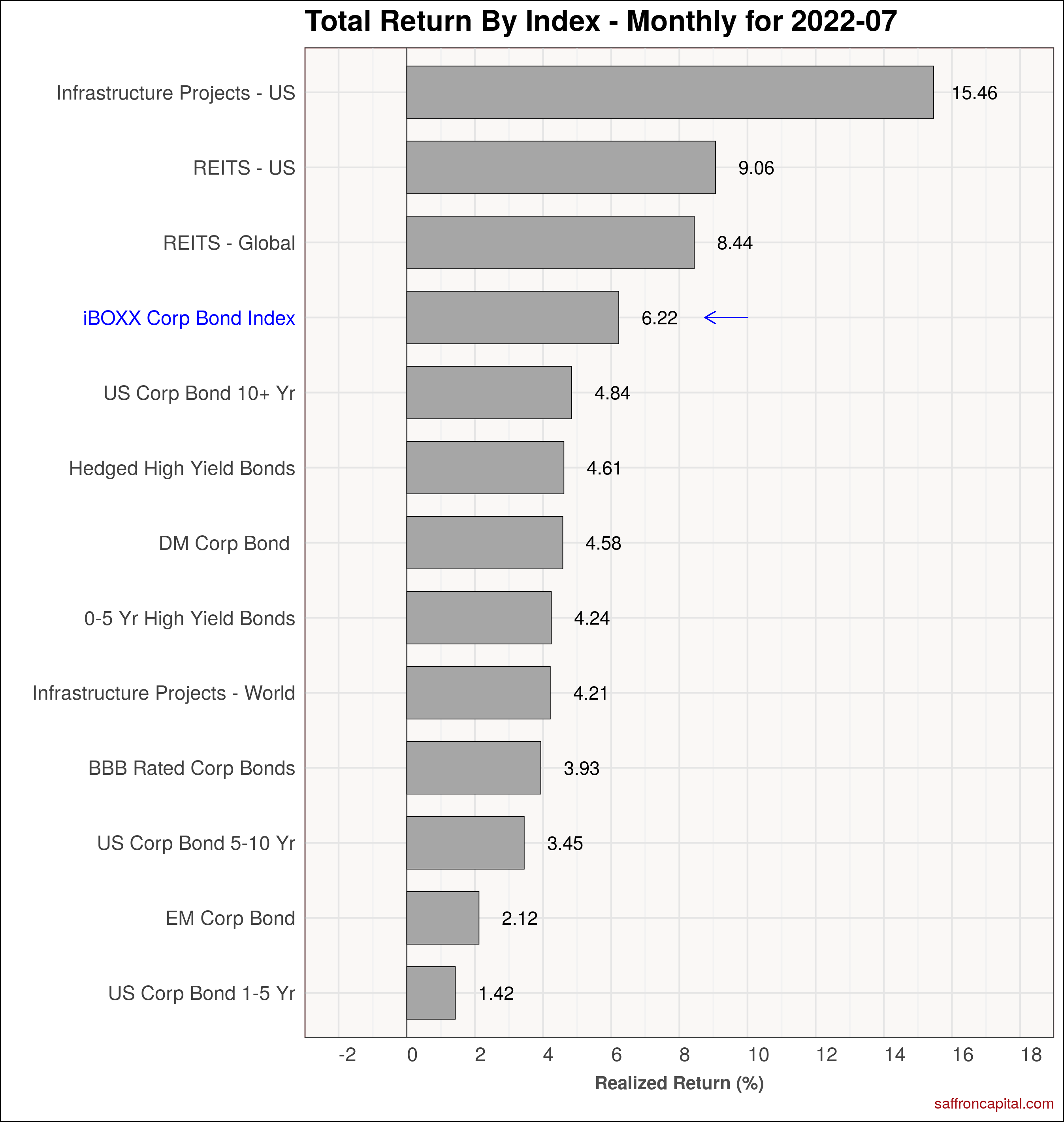

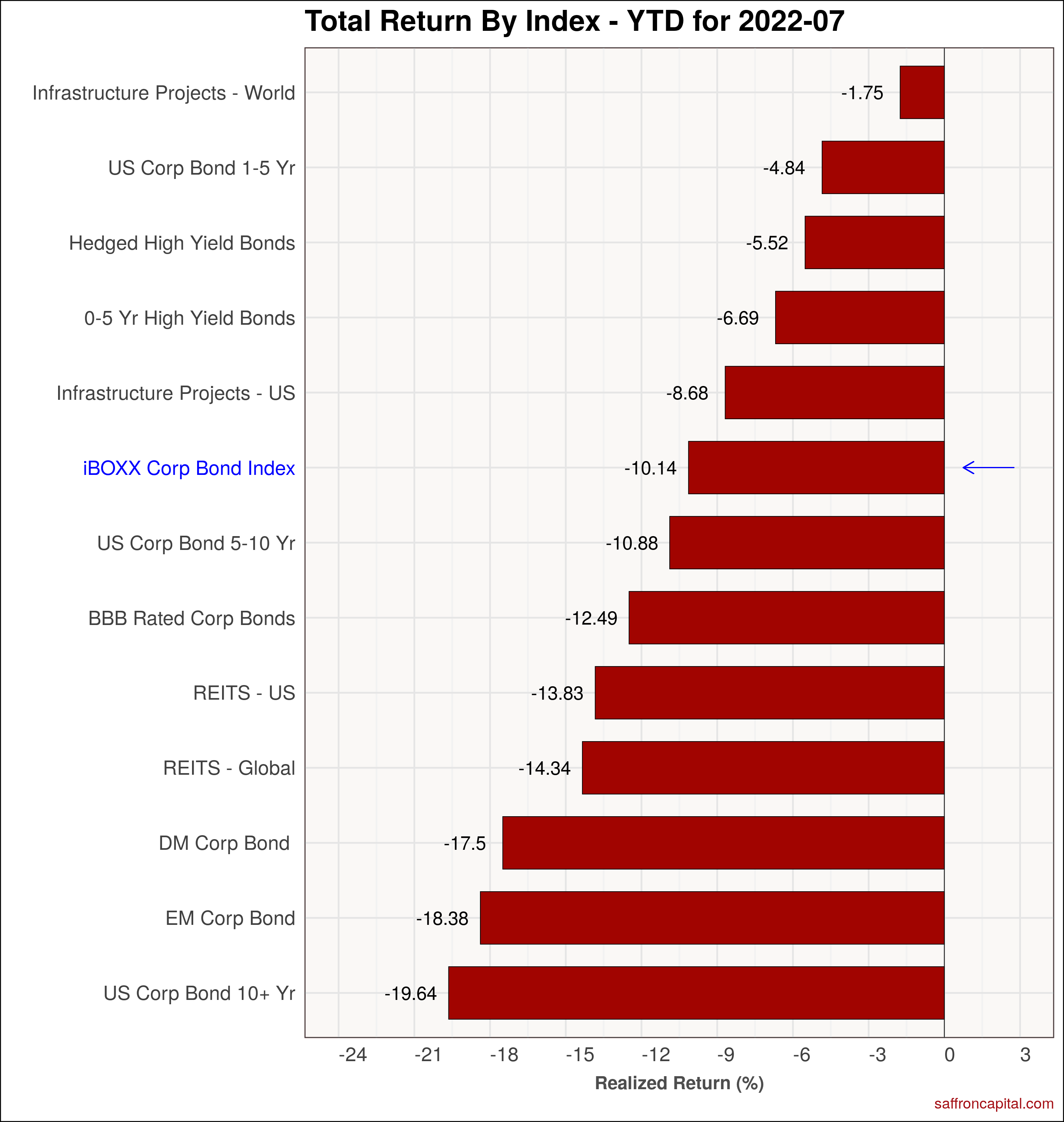

Corporate & Infrastructure Bonds

The iBoxx Corporate Bond Index (+6.22) had good returns in July. The best performers were US infrastructure project bonds (+15.46%) and US REITS (+9.06%), both of which outperformed the S&P 500 index. Since January, the iBoxx index (-10.14) continues to outperform equities. However, the red ink is noticeable with large losses observed for Developed markets corporate bonds (-17.5%), emerging market corporate bonds (-18.38%) and long date US corporate bonds (-19.64%).

Click to enlarge

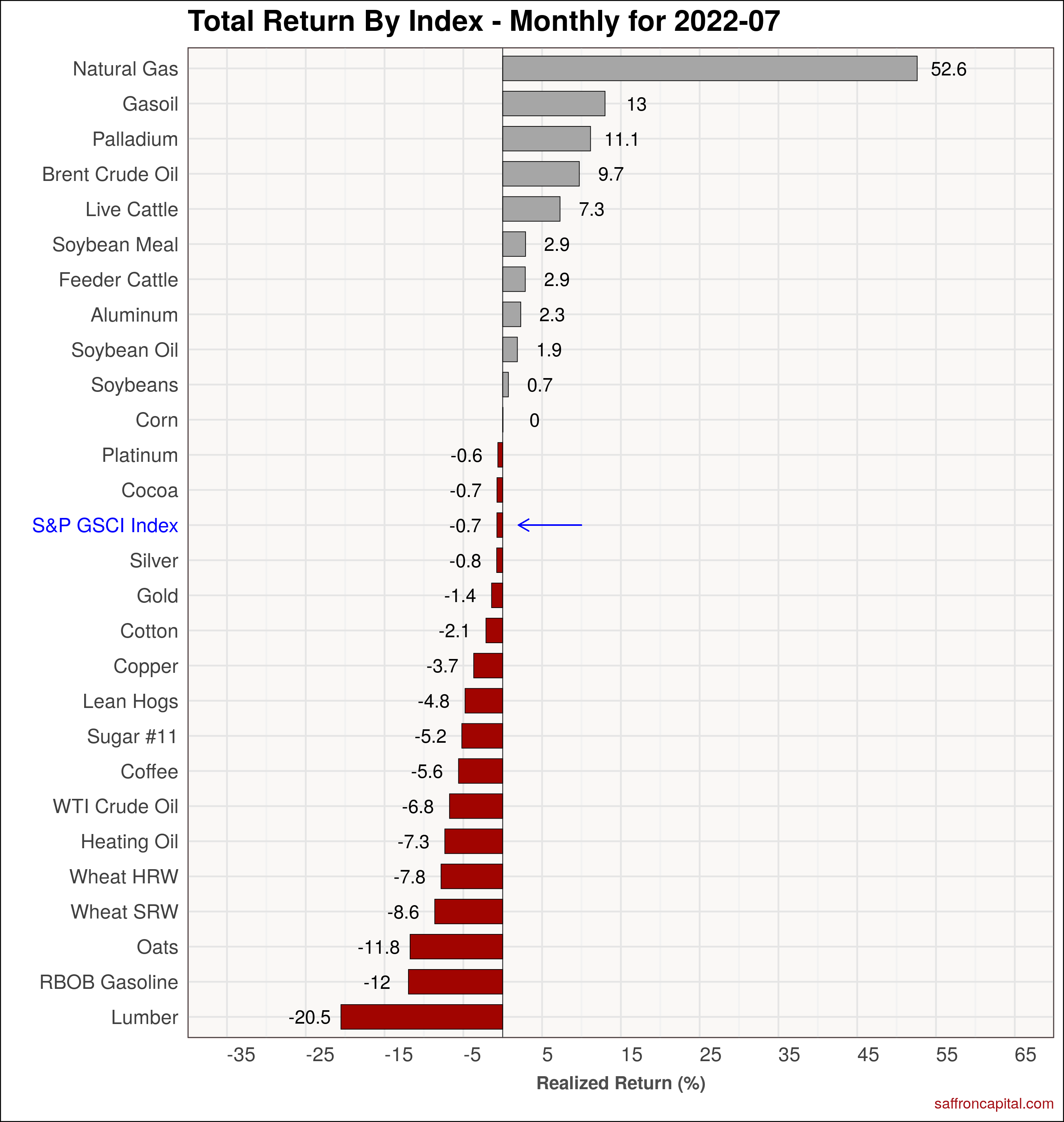

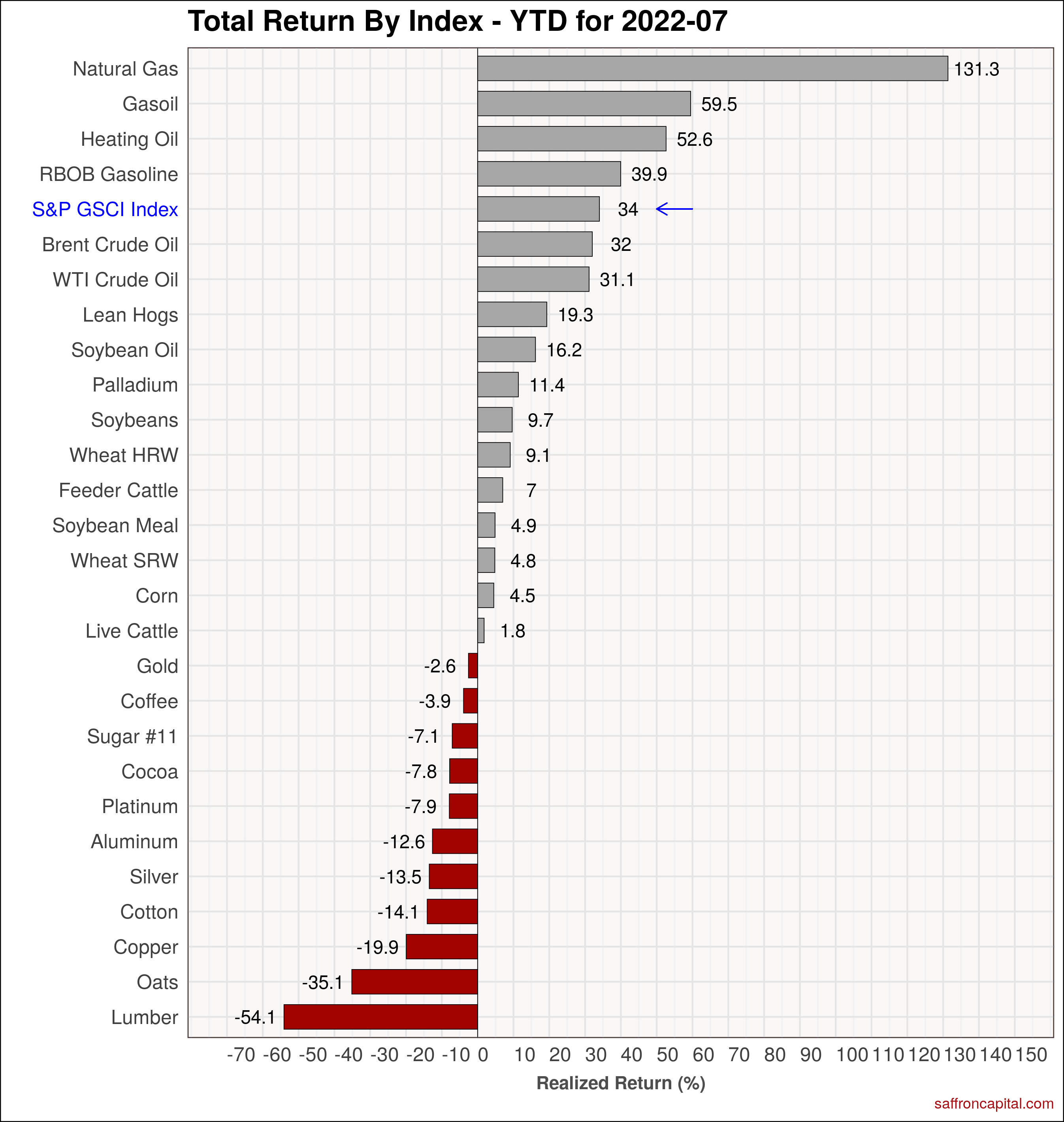

Commodities

June commodity returns were again dominated by energy and metals, notably natural gas (+52.6%), European Gasoil (+13.0%) and Palladium (+11.1%). Overall, the S&P GSCI Index (-0.7%) declined for the second month in a row, lead by declines in lumber (-20.5%), Gasoline (-12.0%) and Oats (-11.8%). The S&P GSCI Index is still up (+34.0%) on a YTD basis, with energy markets outperforming all others.

Click to enlarge

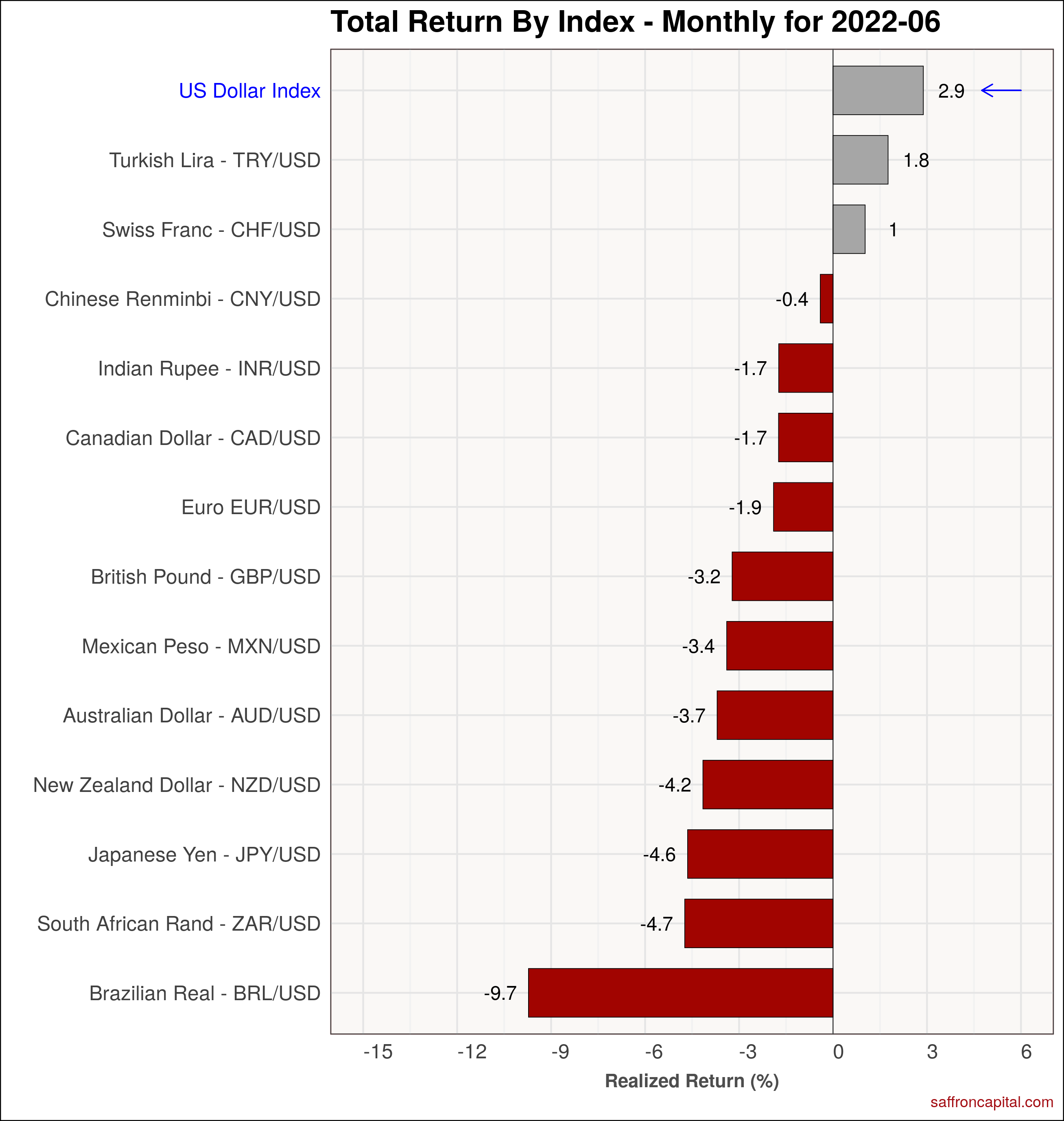

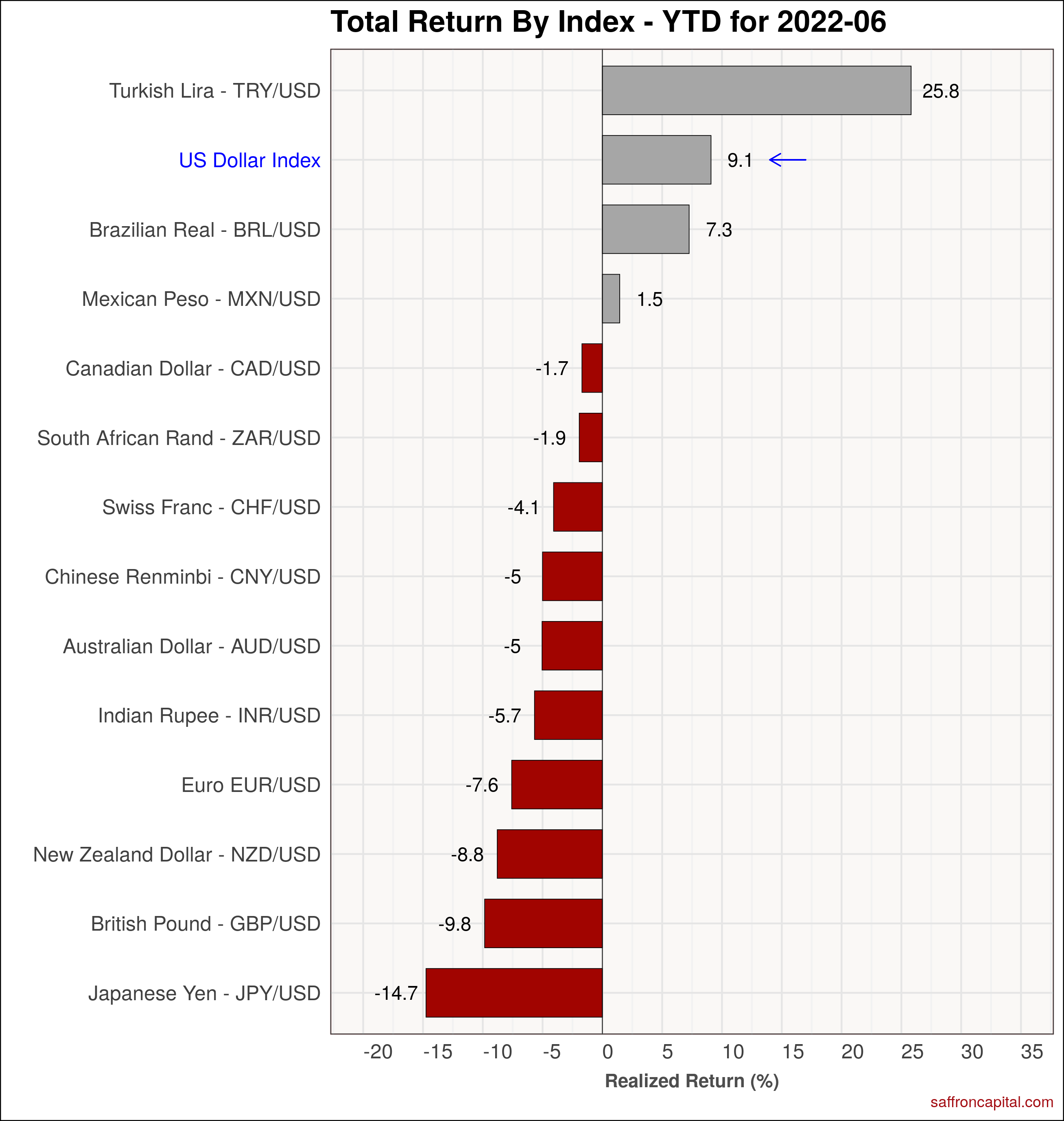

Currencies

The US Dollar (+1.2%) rose in July, but was not the strongest currencies. Returns were led by The Turkish Lira (+7.3%), the Yen (+1.5%) and the Aussie Dollar (+1.3%). The weakest currencies in July were (the Euro (-2.7%) and the Rand (-1.6%) and the Yuan (-0.8%). Since January, the strongest currency has been the Turkish Lira (+35.0%) and the weakest has been the Yen (-13.5%).

Click to enlarge

Have questions about the performance and investment plan for your portfolio? Schedule a call or meeting with us here.

{kind=link}

{kind=link}

{kind=link}