The 3Q earnings season is off to a strong start with 7% of firms reporting. In aggregate, actual earnings reported are 10% above consensus estimates. As a result, the annual earnings growth rate for the S&P 500 index has increased from 0% growth at the end of second quarter to 0.4% more recently. As a result, the quarter is shaping up to be the first quarter with positive earnings since 3Q.2022. Moreover, it is also likely that the second quarter was the bottom in U.S. earnings. For example, the consensus estimate for year-on-year earnings growth for the S&P 500 Index remains

stubbornly optimistic and is forecast to be positive for the next eight quarters.

Sector Earnings

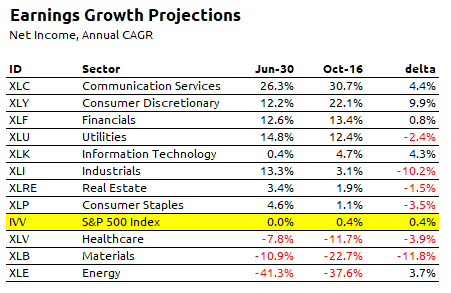

Presently, 8 of the 11 sectors in the Index are expected to report year-over-year earnings growth in the third quarter, as shown above. 3Q earnings growth is led by shares in the Communication Services (+30.7%), Consumer Discretionary (22.1%), and Financial (13.4%) sectors. In contrast, 3 of 11 sectors are expected to report annual declines in 3Q earnings, led by Energy (-37.6%), Materials (-22.7%) and Health Care ( -11.7%).

The bottom-up consolidation of earnings estimates by company shows some interesting changes in earnings since the end of second quarter. Specifically, earnings growth updates with the largest positive delta by sector include Consumer Discretionary (+9.9%), Communication Services (+4.4%), Information Technology (+4.3%) and Energy (+3.7%). Over the past 10 years, the consensus estimate for earnings has underestimated actual earnings by as much as 660 basis points. Over the last year, consensus forecasts have underestimated actuals by as much as 440 basis points. As a result, corporate earnings changes are likely to have additional upside as actual earnings are reported.

Click to enlarge

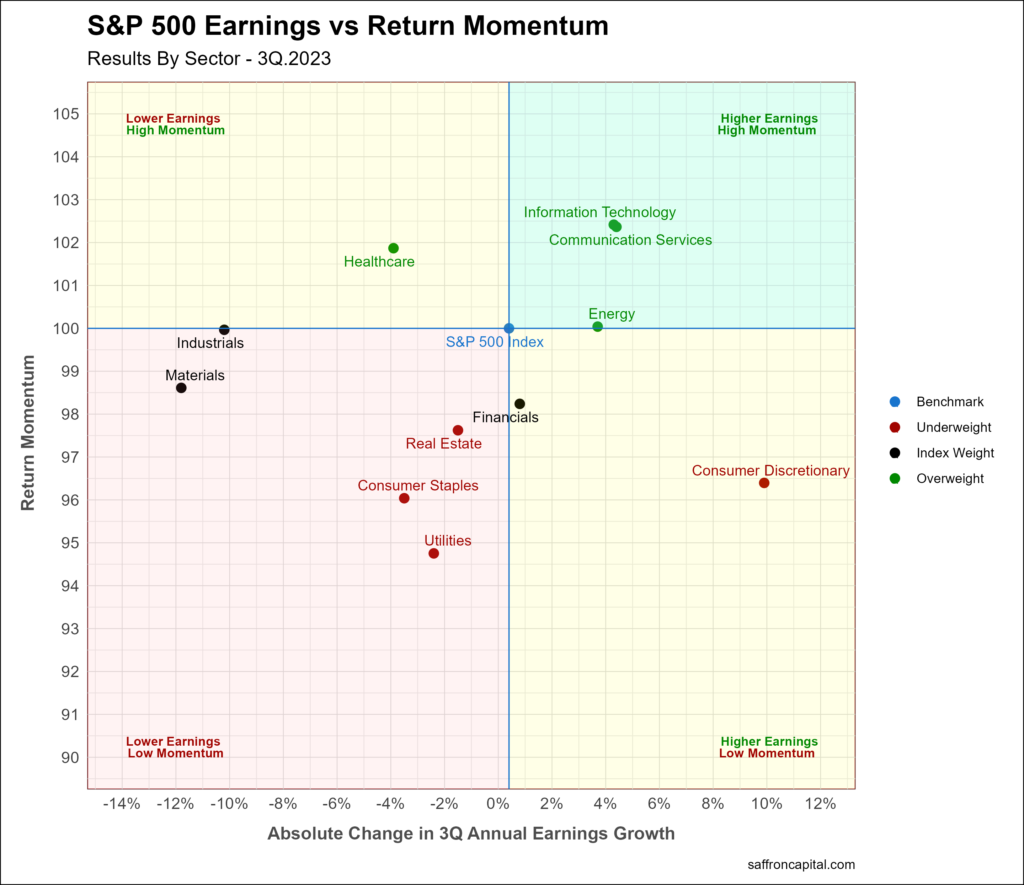

3Q Earnings vs Return Momentum

The next chart shows changes in 3Q earnings versus relative return momentum by sector. Normally, high return momentum is associated with sectors with positive changes in earnings outlooks. We also tend to see low return momentum for sectors with declining earnings growth. The data strongly supports the positive relationship between earnings and returns. In particular, sectors with the strongest return momentum relative to Index include Information technology (XLK), Communications Services (XLC), Health Care (XLV), and Energy (XLE). 3 of these 4 sectors also had the highest earnings changes since June-30. The market again rewards outsized earnings changes with outsized returns.

Click to enlarge

See and Understand the Signals

Contact us if you have questions about this report and how our model portfolios can help you. Need a risk-managed portfolio strategy to grow and protect your savings? Whatever your needs are, we are here to help. You can contact us here.

Important Notice

Saffron Capital provides capital market research and insight reporting for informational and educational purposes only. The report does not constitute a solicitation to buy or sell securities. We only provide investment advice to people or entities subject to an investment advisory agreement and given a formal assessment of your financial goals and risk appetite.

Caution Regarding Forward-Looking Statements Forward projections are valid inputs in any planning or investment process. However, they are not a guarantee of future returns or market performance. Any opinion about future events (such as market and economic conditions, company performance, security returns, or future security offerings) are forward-looking statements. Forecasts and forward-looking statements, by definition, involve risk or uncertainties, and do not reflect actual knowledge about the future.

{kind=link}

{kind=link}

{kind=link}