June 2024 returns for the benchmark S&P 500 index (+3.50%) deflected concerns about inflation, market breadth, government debt levels, and large bond auctions by the U.S. Treasury. The index is now up +14.5% year-to-date and the United States continues to have the best growth and economic stability globally. Strong government spending, high employment, and improving productivity are all expected to help the S&P 500 index to achieve its highest year-over-year earnings growth rate (+8.8%) in more than two years for the second quarter. Moreover, the S&P 500 index is also on track to achieve double-digit earnings in 2024 (+11.3%) and the outlook for 2025 earnings (+14.4%) is also strong.

The following brief decomposes asset group returns for June. The visual summary of returns across and within the asset groups is intended to help investors to identify new opportunities and to to quickly benchmark their own portfolio returns.

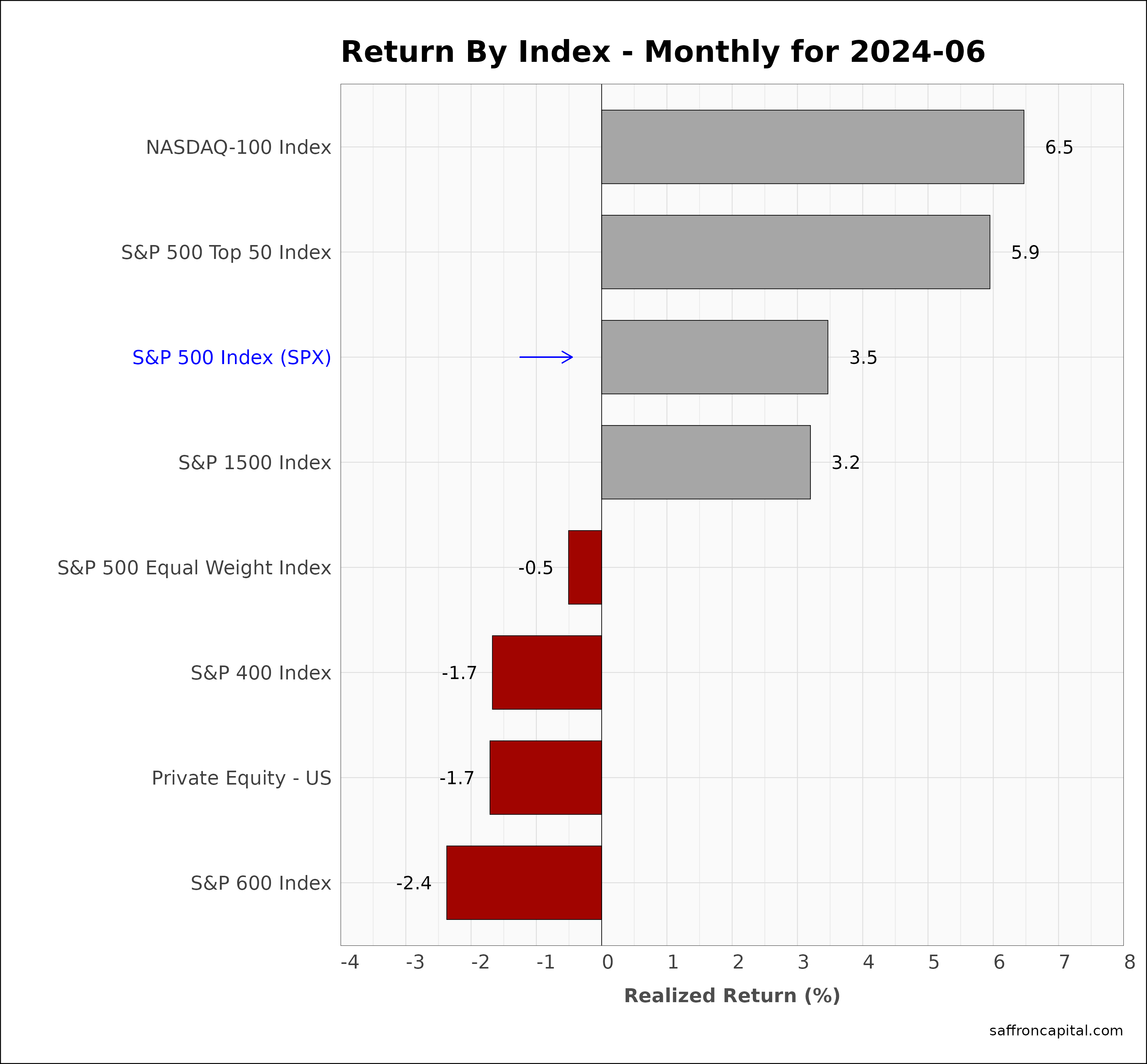

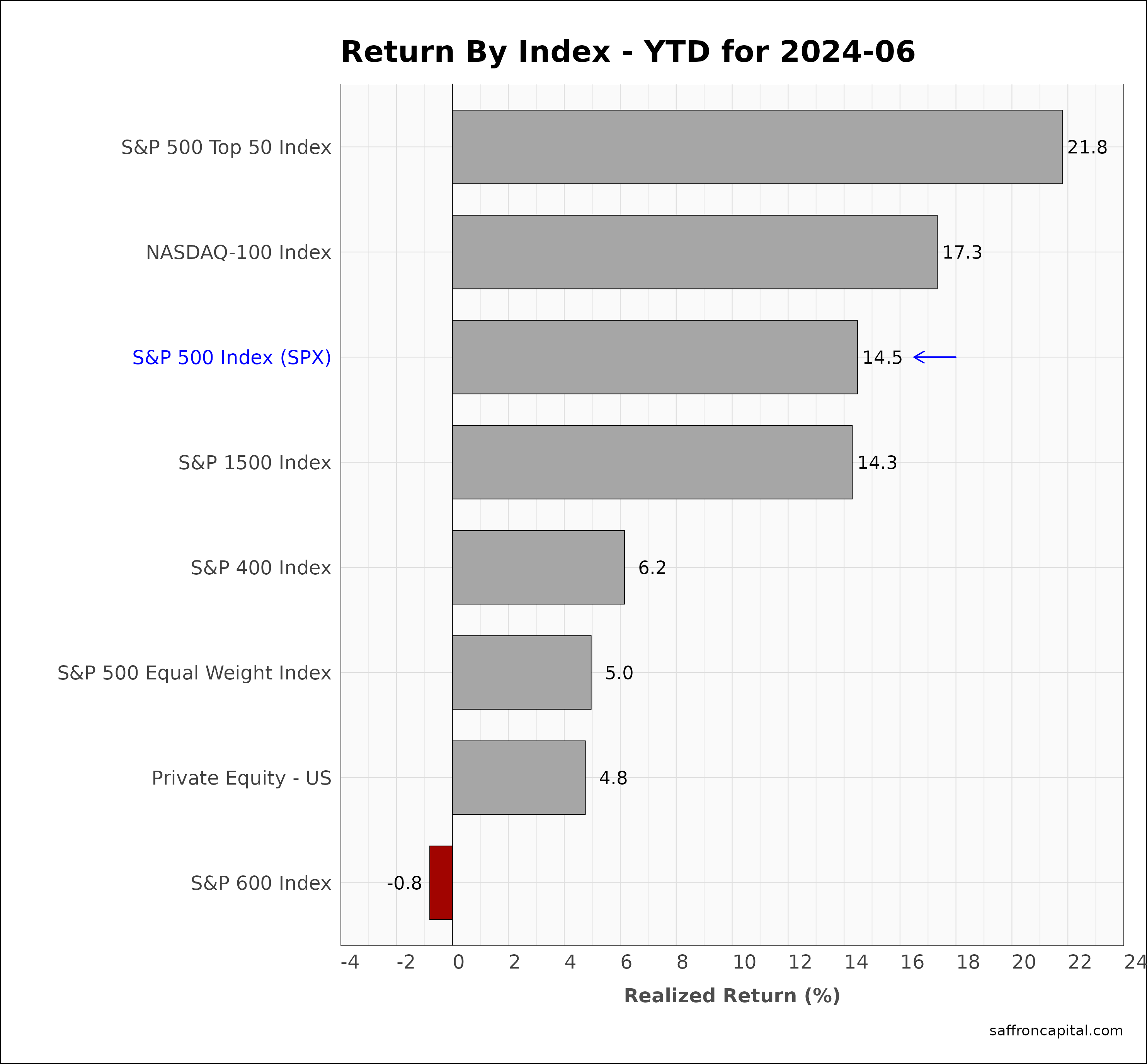

Core US Indices

The large-cap S&P 500 index (+3.5%) trailed the NASDAQ-100 index (+6.5%) in June. The large cap index also trailed the S&P 500 Top 50 index (+6.5%) as market breadth was limited. Weak market internals are best seen int he eprformance of the the S&P 400 Mid Cap Index (-1.7%) and S&P 600 Small Cap index (-2.4%). Year-to-date (YTD), the S&P 500 (+14.5%) continues to trail the the NASDAQ-100 index (+17.3%) and mega large-cap S&P 500 top 50 index (+21.8%).

Click to enlarge

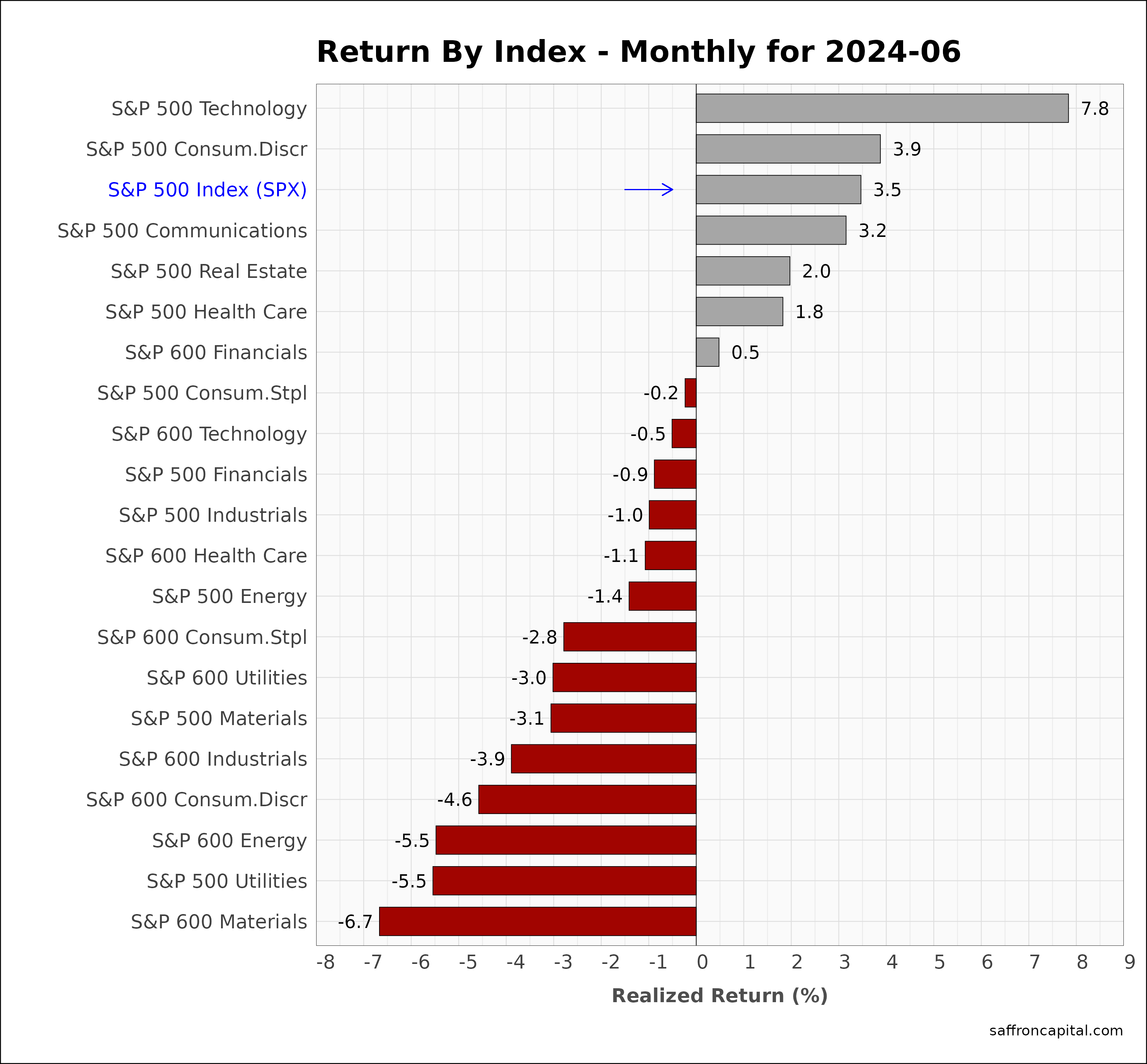

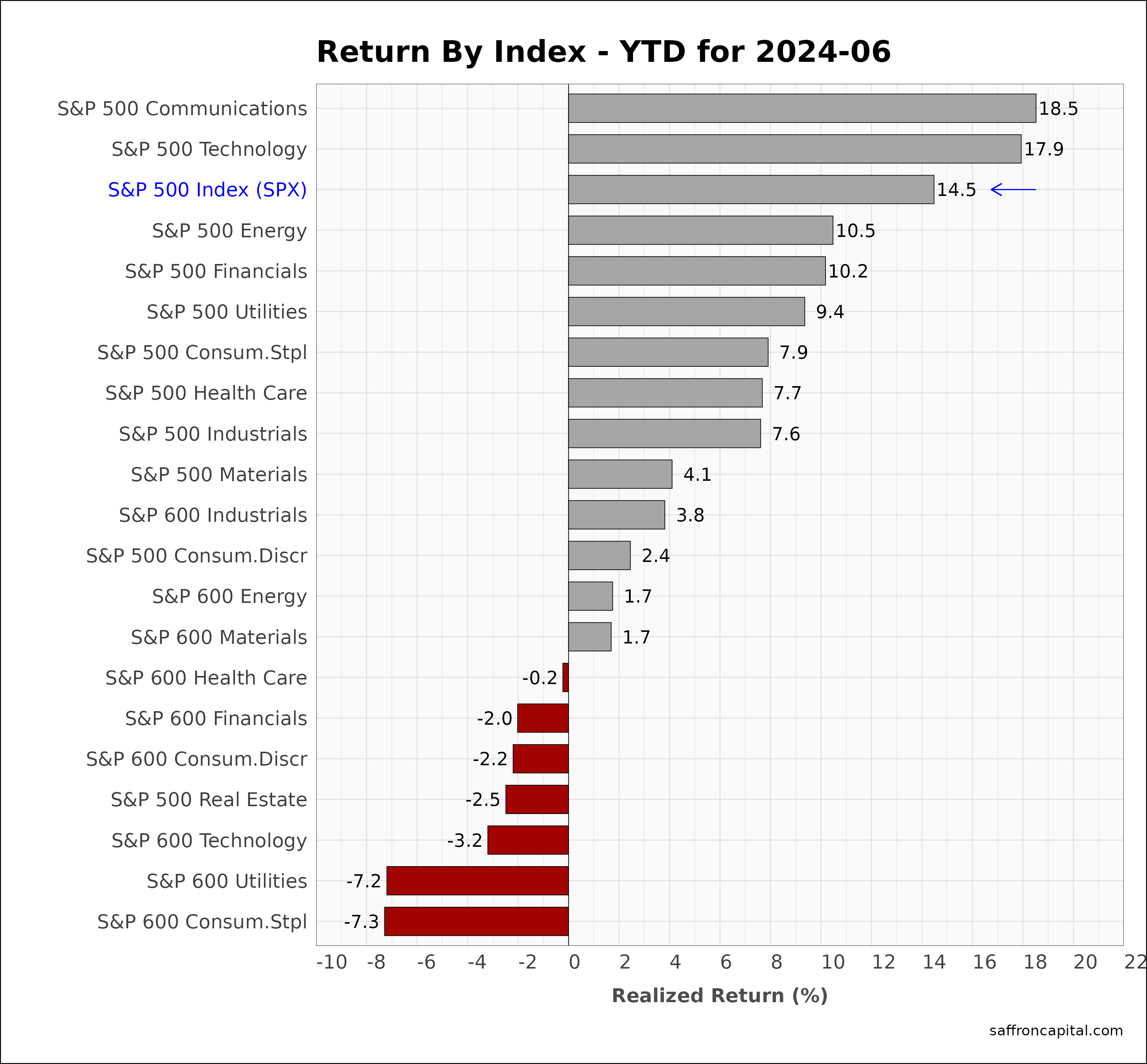

US Sector Indices

June returns for the the top sectors were led by large cap Technology (+7.8%) and Consumer Discretionary shares (+3.9%). The low number of sectors beating the index is further evidence market breadth was limited. The weakest sectors were small cap Materials (-6.7%), large cap utilities (-5.5%), and small cap Consumer Discretionary stocks (-5.5%). Since January, Communication Services (+18.5%), Technology (+17.9%) and Energy (+10.5%) topped the sector rankings.

Click to enlarge

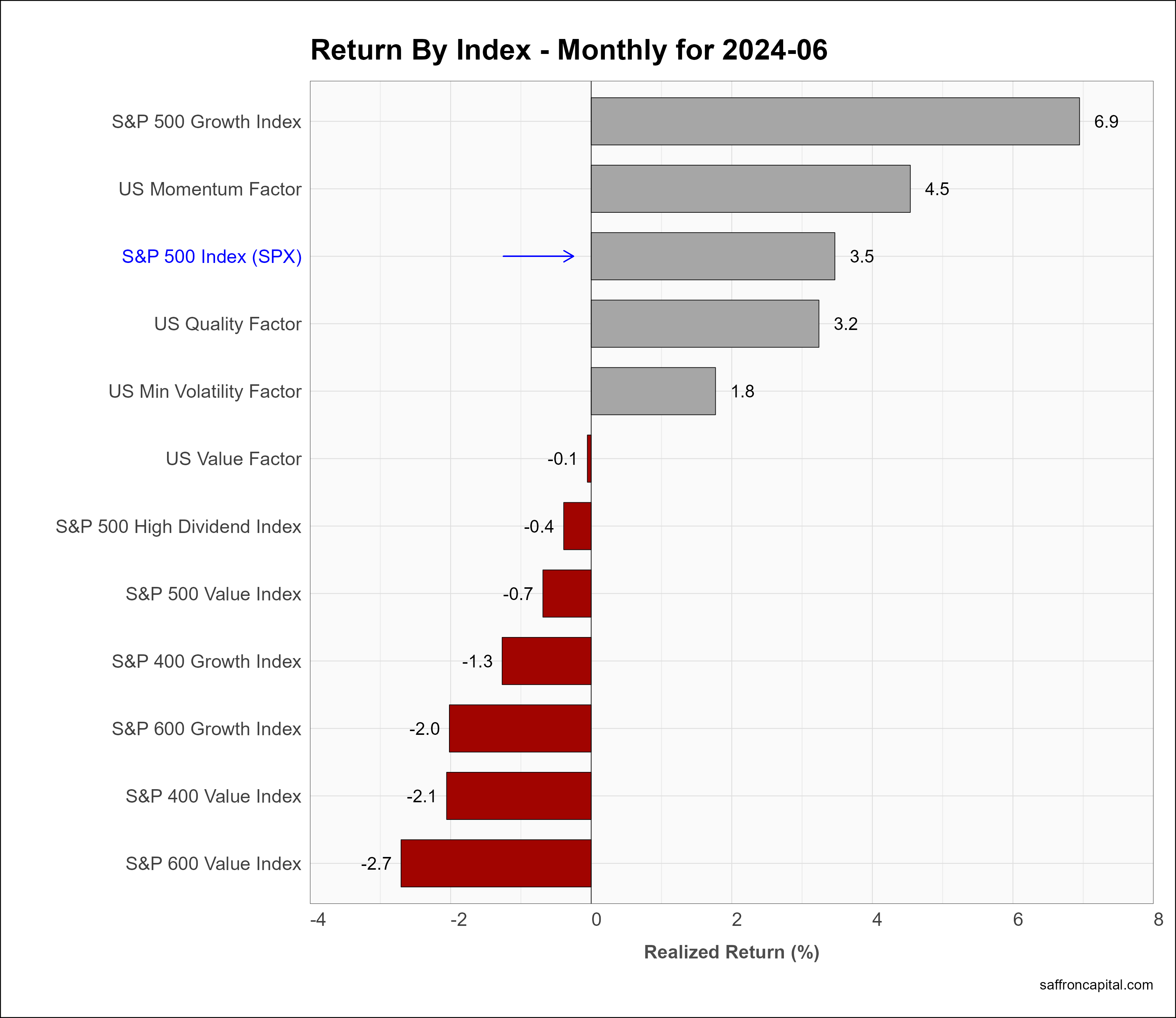

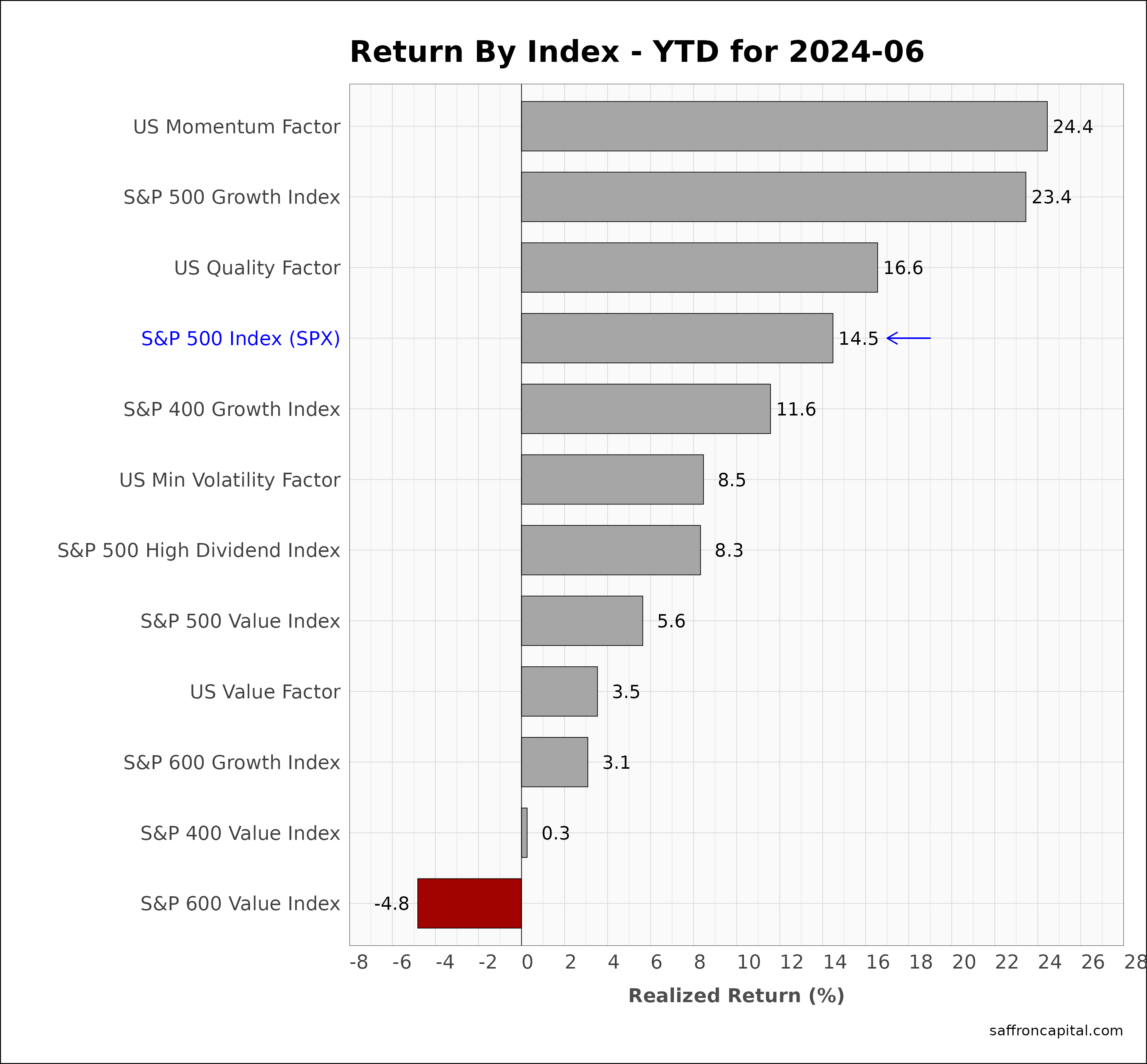

US Factor Indices

Factor portfolios are constructed to focus on the core drivers behind returns, such as company size, value, profitability, growth, and momentum. Multi-factor portfolios focus on two or more factors when selecting shares. During June, returns were lead by the S&P 500 Growth Index (+6.9%), the US Momentum Index (+4.5%), and the U.S. Quality factor (+3.2%%). Small-cap value, mid-cap value, and small-cap growth indices all under-performed the benchmark S&P 500 index by large margins. Since the start of the year, the US Momentum Factor (+24.4%) continues to lead all factor indices. Other performers include the S&P500 Growth index (+23.4%), and the U.S. Quality factor (+16.6%).

Click to enlarge

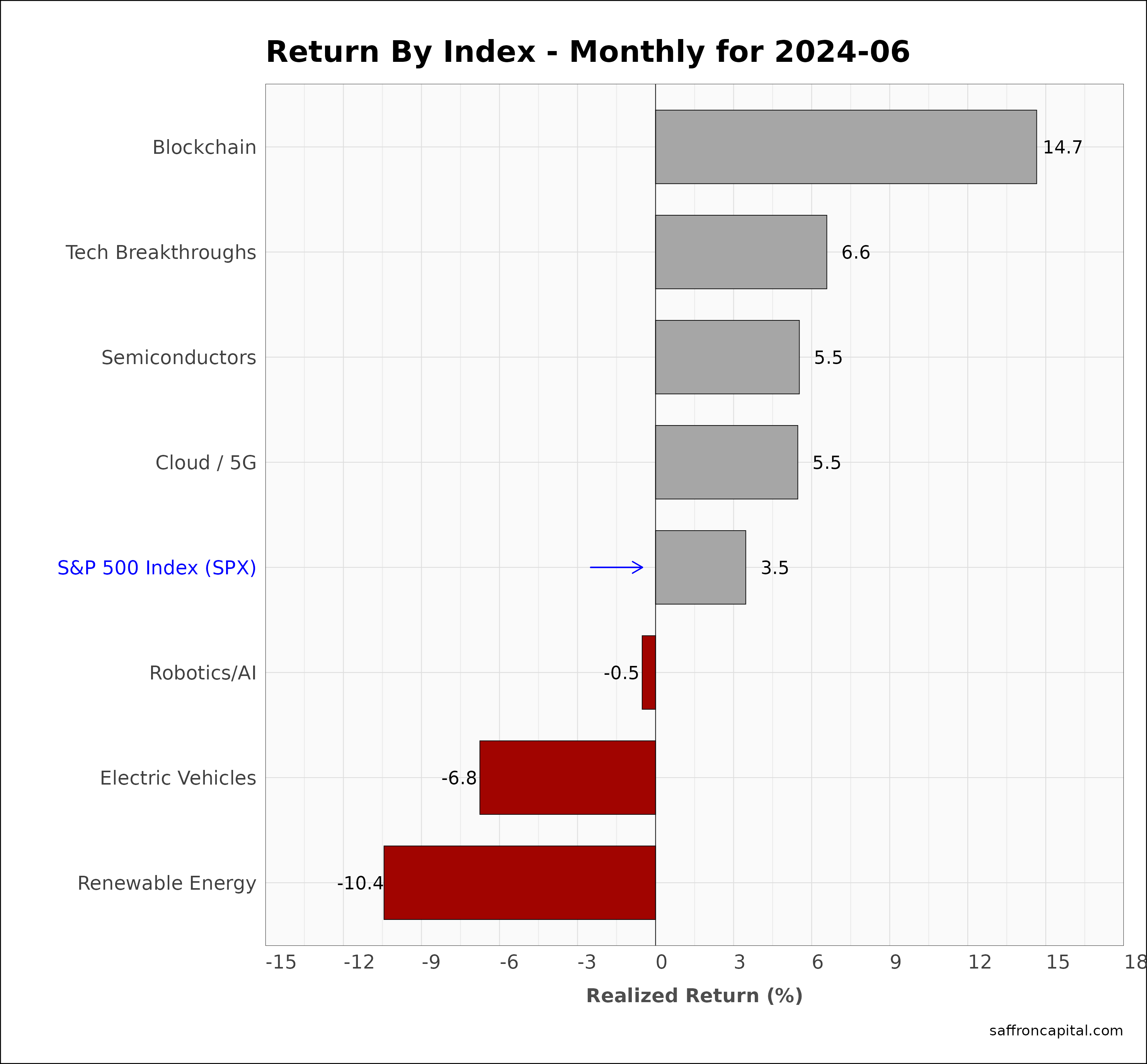

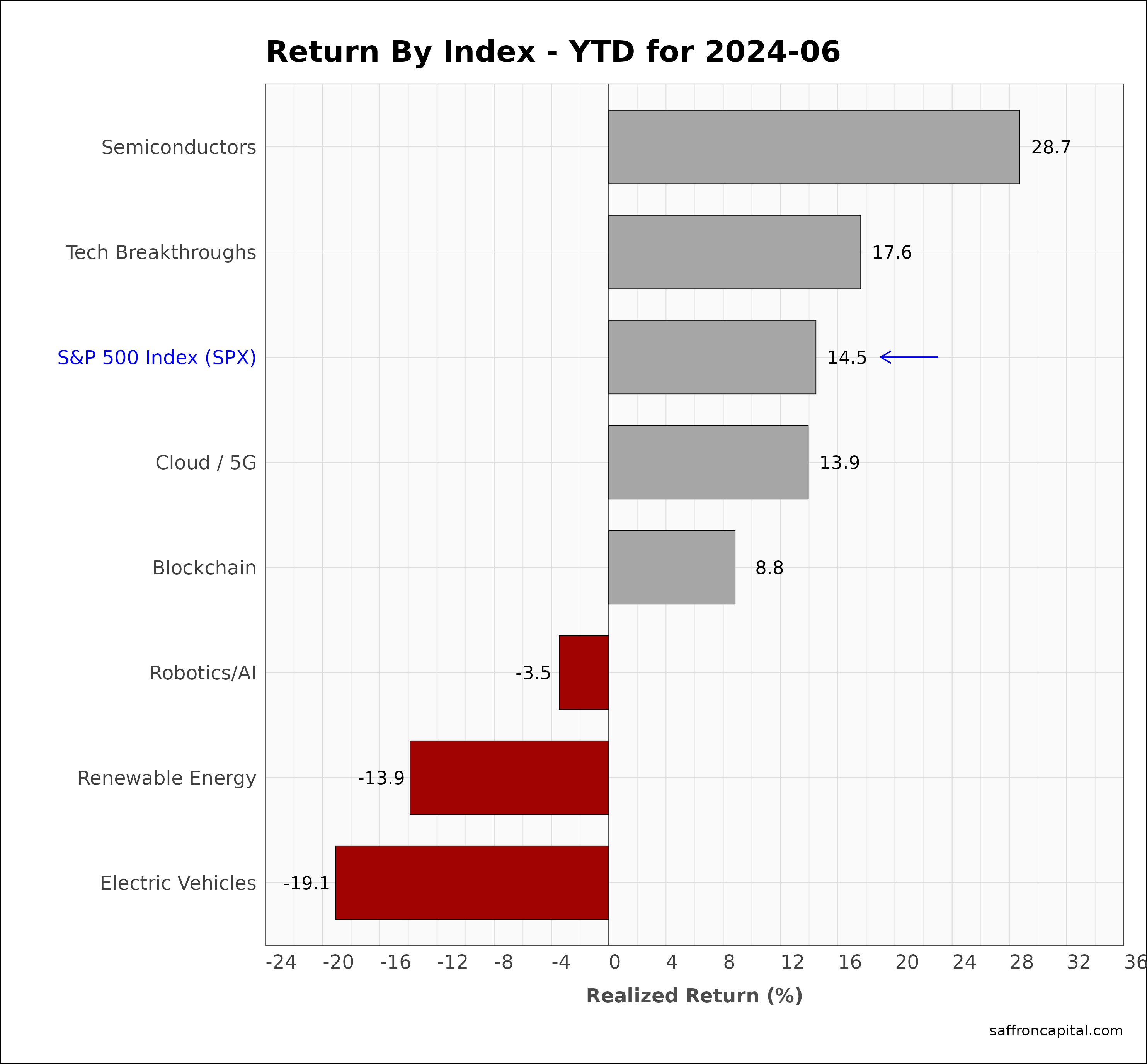

US Megatrend Equities

US megatrend equities are thematic growth portfolios that seek to capture the primary secular trends of the market. June returns were lead by shares in Blockchain companies (+6.9%), Tech Breakthroughs (+6.6%), and Semiconductors (+5.5%), all of which beat the the benchmark S&P 500 index. Renewable Energy (-10.4%) and Electric Vehicles (-6.8%) continue to have multi-month losses. Since January, top performers include Semiconductors (+28.7%), Technology Breakthroughs (+17.6%), and the Cloud/5G portfolio (+13.9%).

Click to enlarge

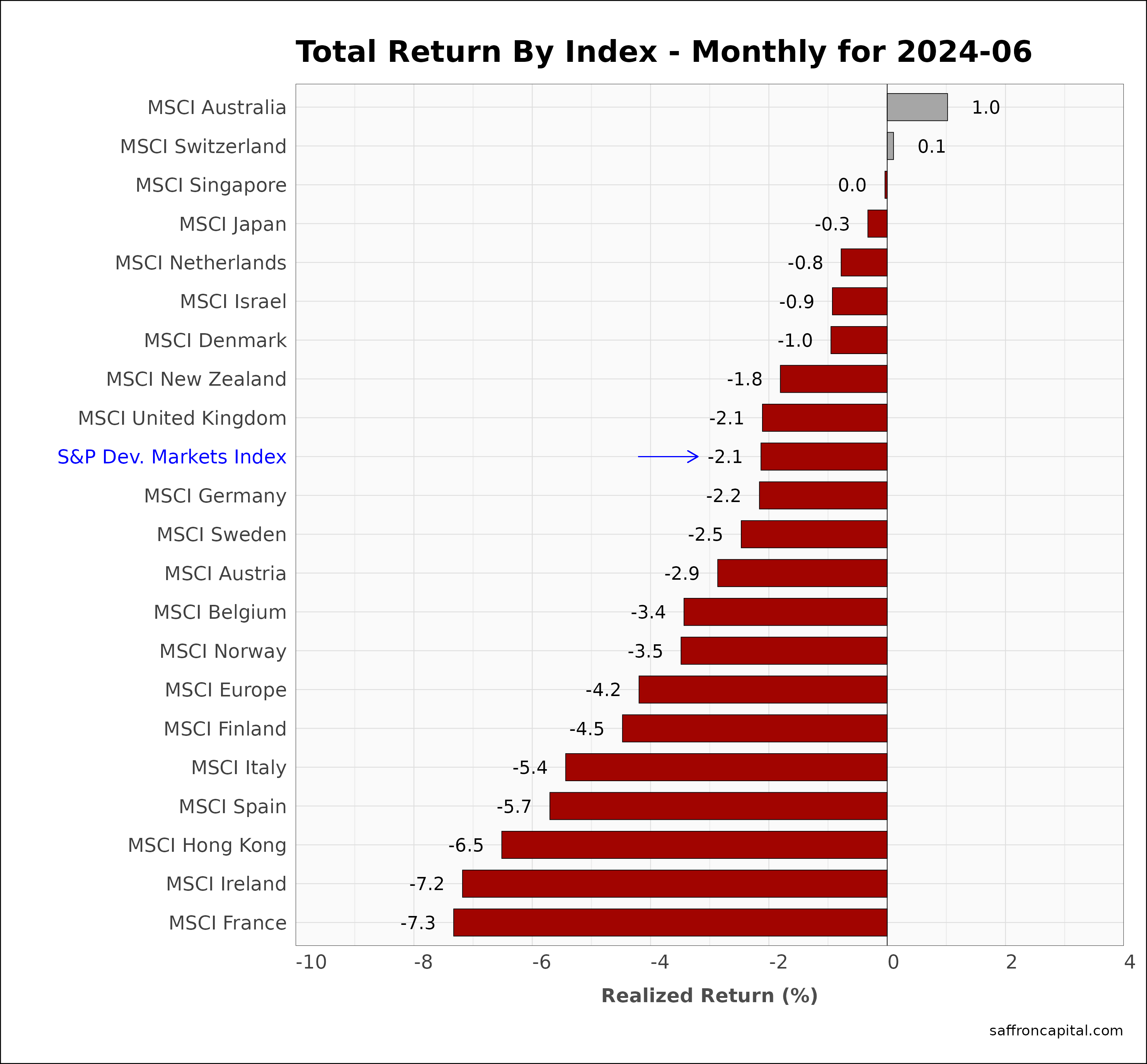

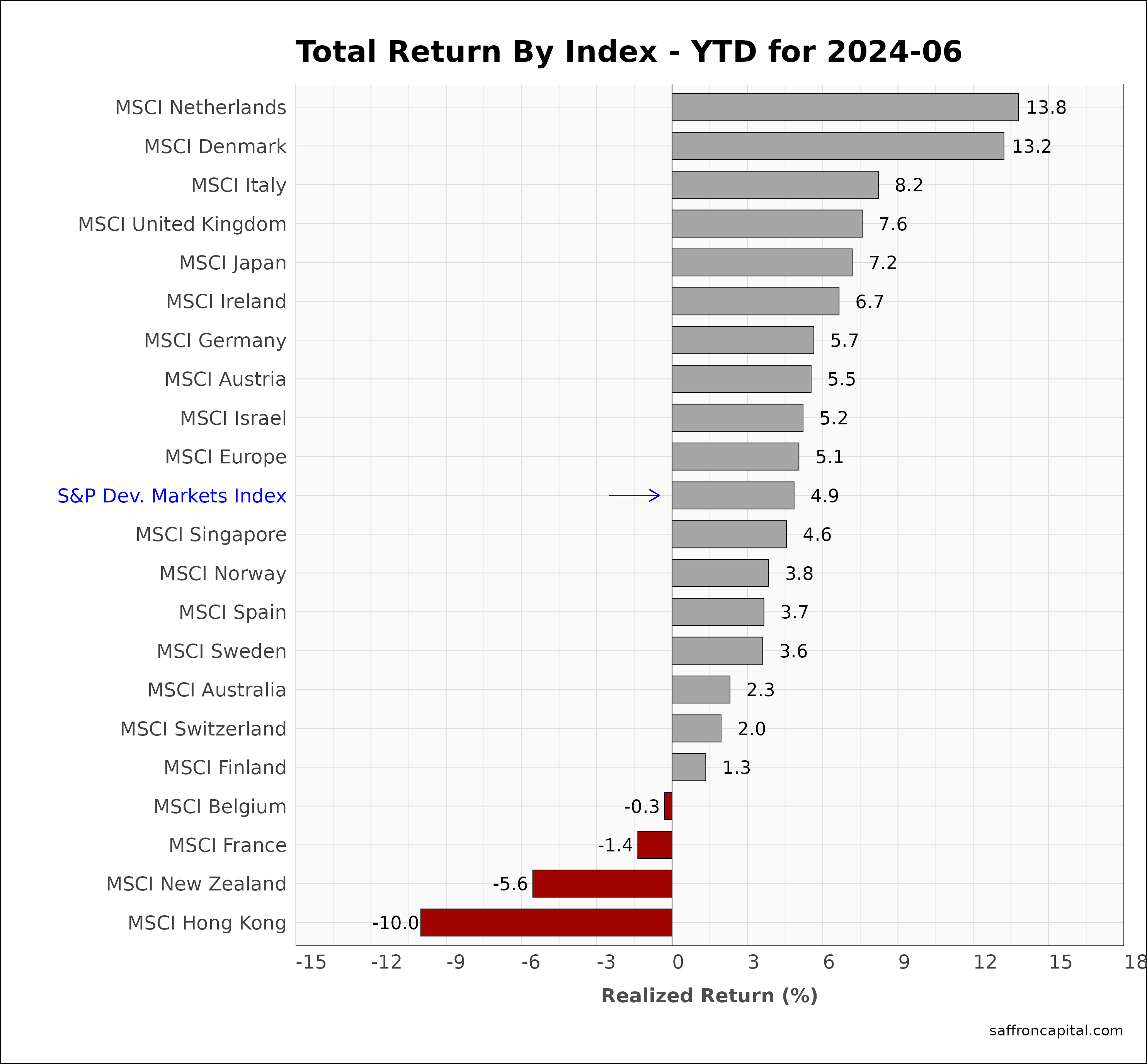

Developed Market Equities

International developed markets (-2.1%) were draped in red ink in June. The only markets to put in positive gains were Australia (+1.0%) and Switzerland (+0.1%) . Japan (–0.3%) reversed course in June while the EU (-4.2%) lagged the US even after a central bank rate cut. Laggards included France (-7.3%), Ireland (-7.2%), and Hong Kong (-6.5%). The best performing developed markets in 2024 are the Netherlands (+13.8%), Denamrk (+13.2%) and Italy (+8.2%).

Click to enlarge

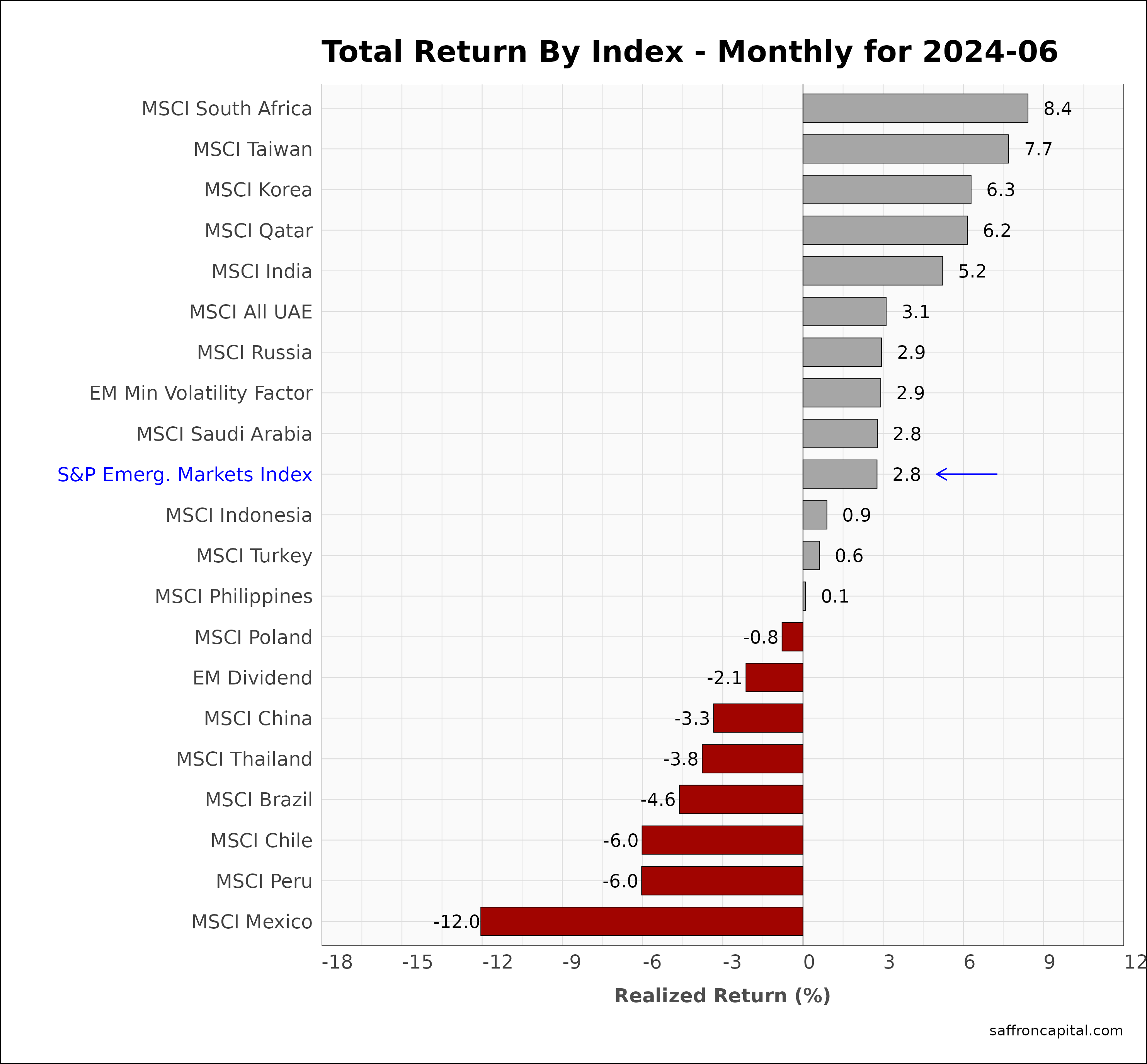

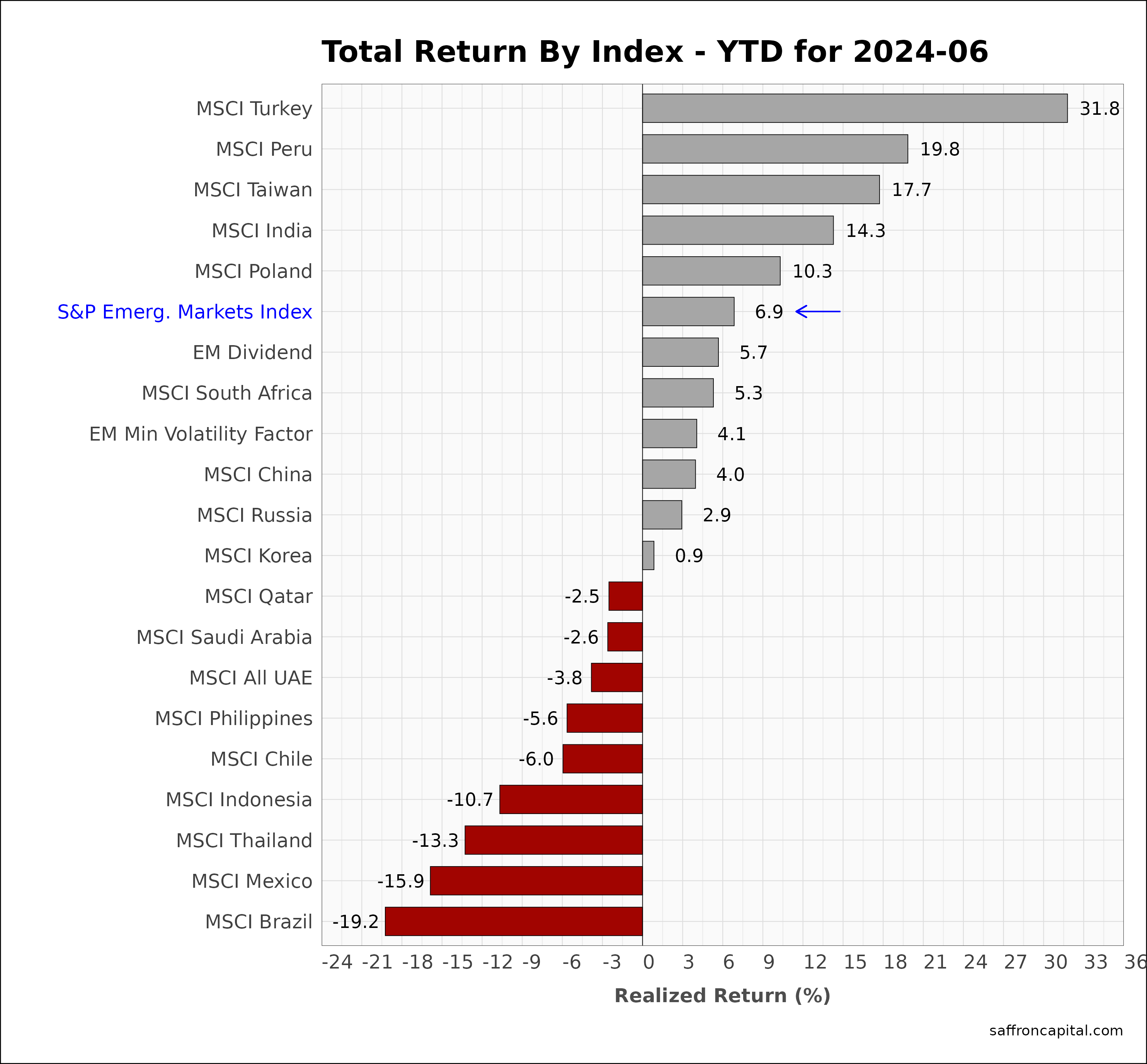

Emerging Market Equities

June returns for the S&P Emerging Markets Index (+2.8%) beat the Developed market index for the fourth month running. Top performers were South Africa (+8.4%), Taiwan (+7.7%) and Korea (+6.3%). India (+5.2%) beat the US large cap index and continues to climb the leader board on strong foreign direct investment, while China (-3.3%) investment flows are drying up. Year-to-date, Turkey (+31.8), Peru (+19.8%) and Taiwan (+17.7%) are outperforming the S&P 500 index, while India (+14.5%) is tied with the U.S.

Click to enlarge

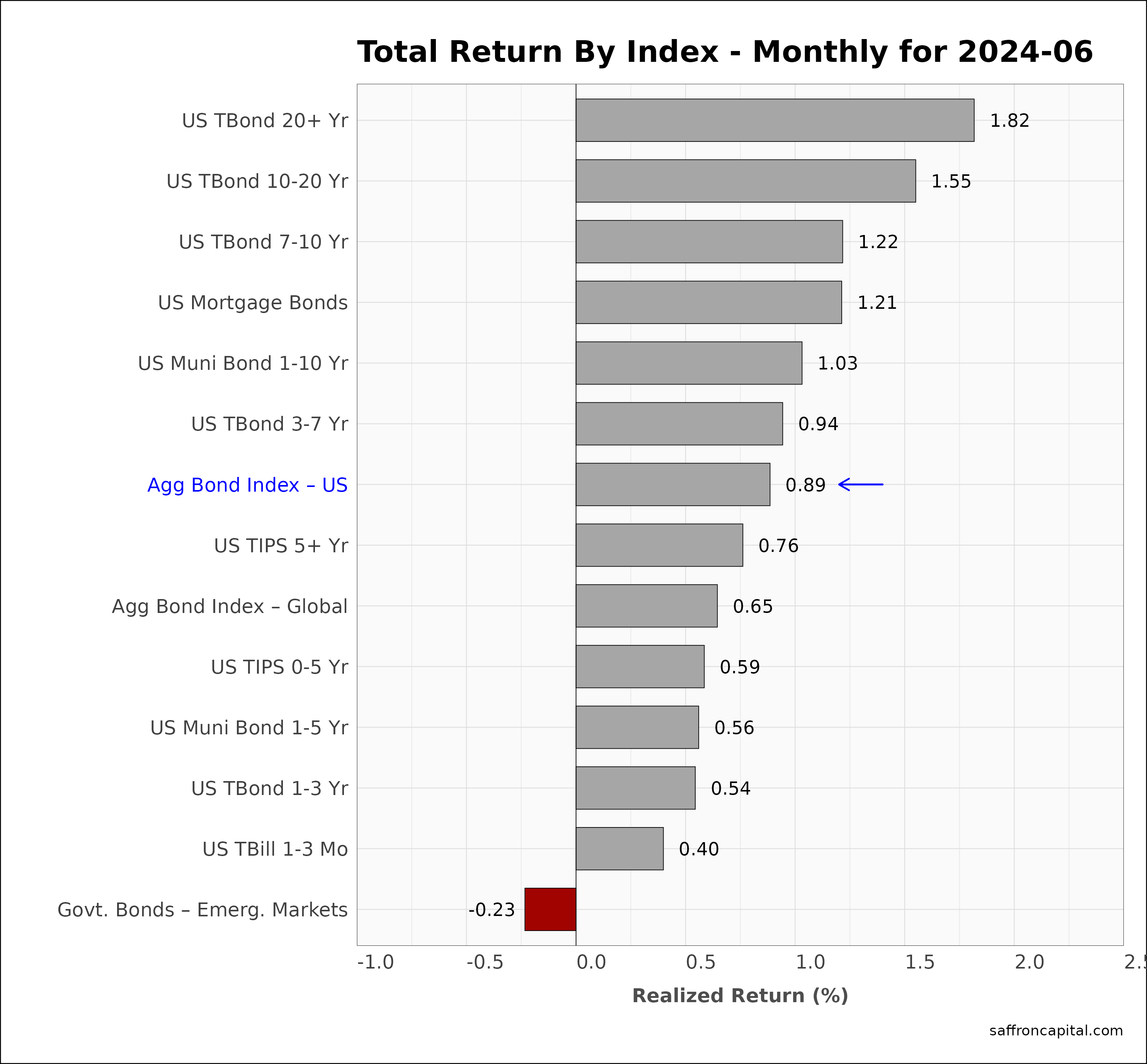

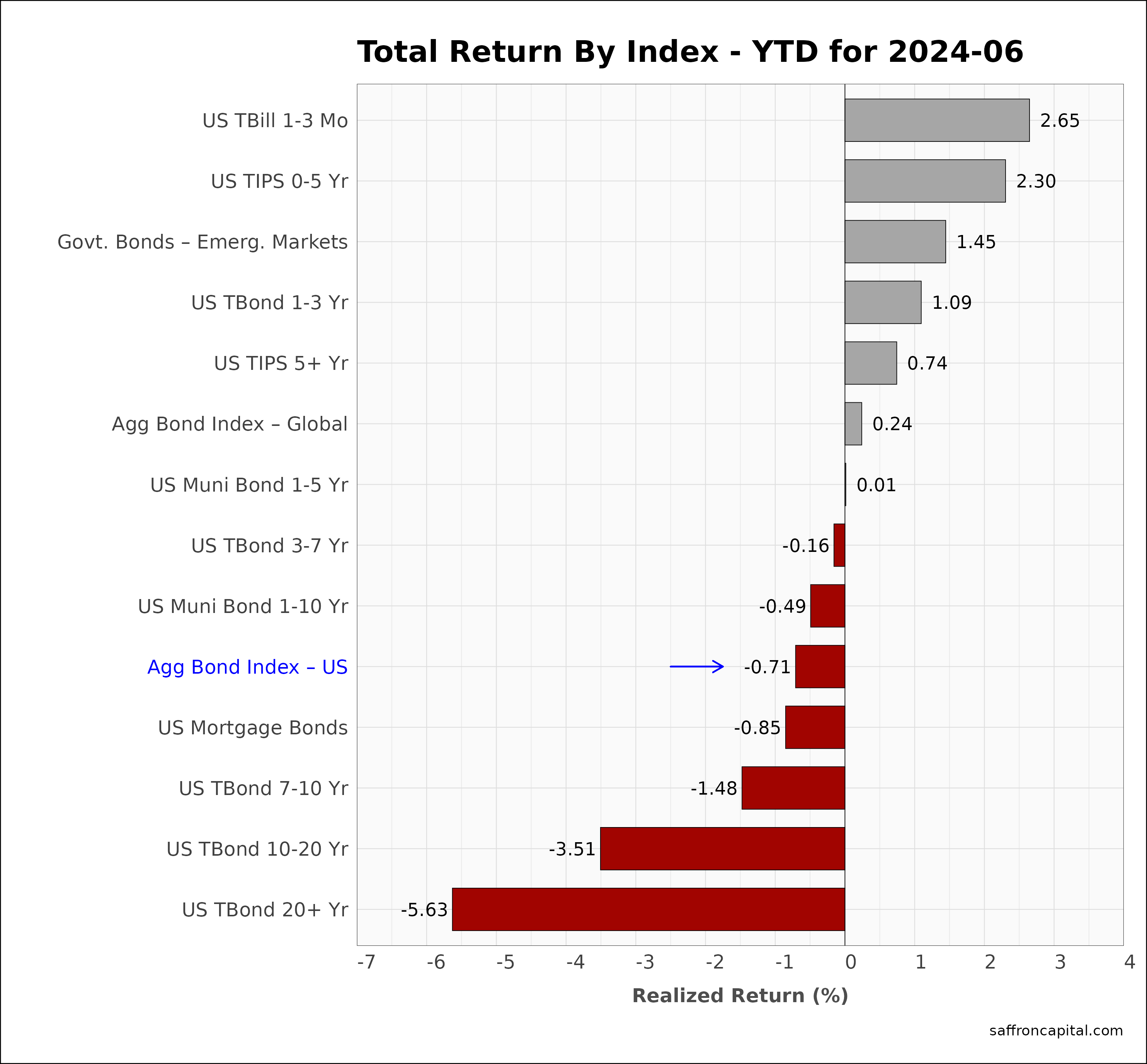

Government Bonds

The US fixed income markets were up modestly in June as seen by the Aggregate Bond Index (-0.89%). The 20+ year bond (+1.82%) lead gains across the yield curve. The Global Agg index (+0.65%) trailed the US, as did Emerging market sovereign bonds (-0.23%). The 10Y Treasury Note ended the quarter with a yield of 4.3%, while a blend of ratings that make-up corporate investment grade bonds had a yield of 6.2%. Year-to-date, the total return for the US Aggregate Bond index (-0.71%) is below the total return for the Global Aggregate Bond index (+0.24%), as well as the returns for Emerging Market Government Bonds (+1.45%).

Click to enlarge

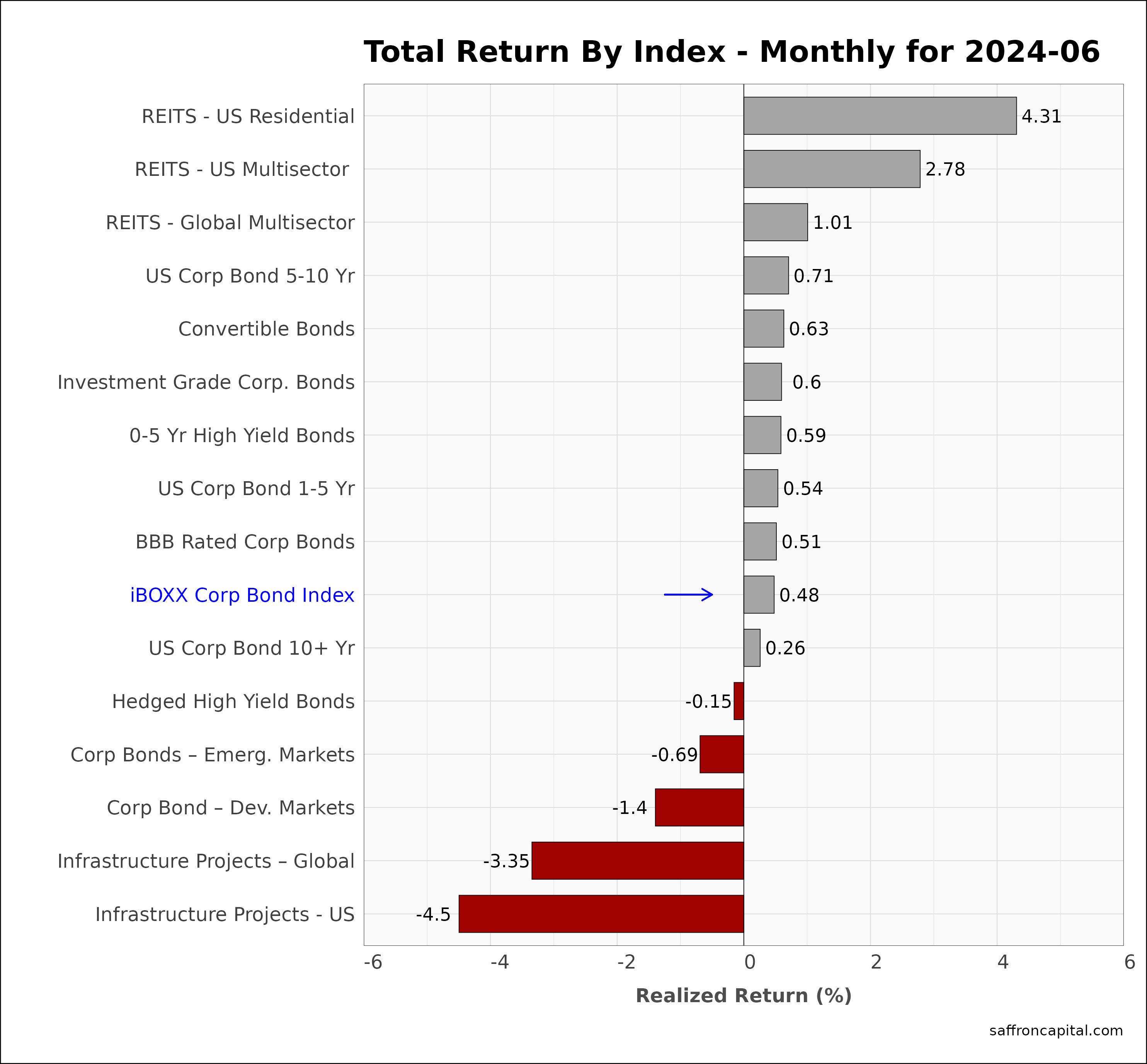

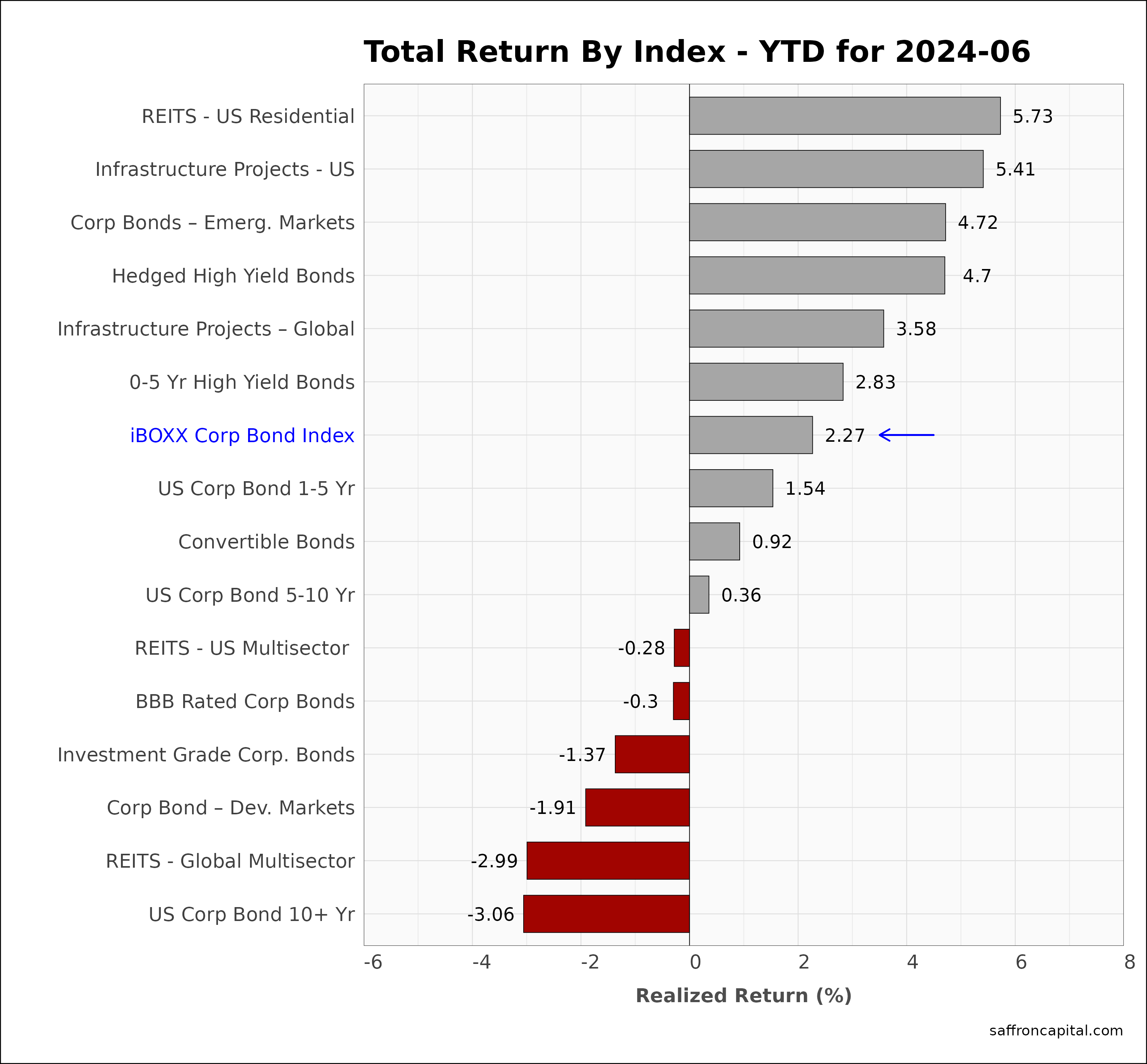

Corporate & Infrastructure Bonds

The iBoxx Corporate Bond Index (-1.35%) had a lackluster month in June. However, US Residential Real Estate Investe,nt Trusts (+4.31%) had a much better month, as did multi sector REITS (+2.78%). US infrastructure Project Bonds (-4.50%) and Global projects (-3.35%) failed to keep pace with the group benchmark, and under performed US equities. Since January, US Residential REITS (+5.73) were the strongest in the group, followed by IS Infrastructure projects (5.41%). Hedged High Yield Bonds (+4.70%) continue to do well.

Click to enlarge

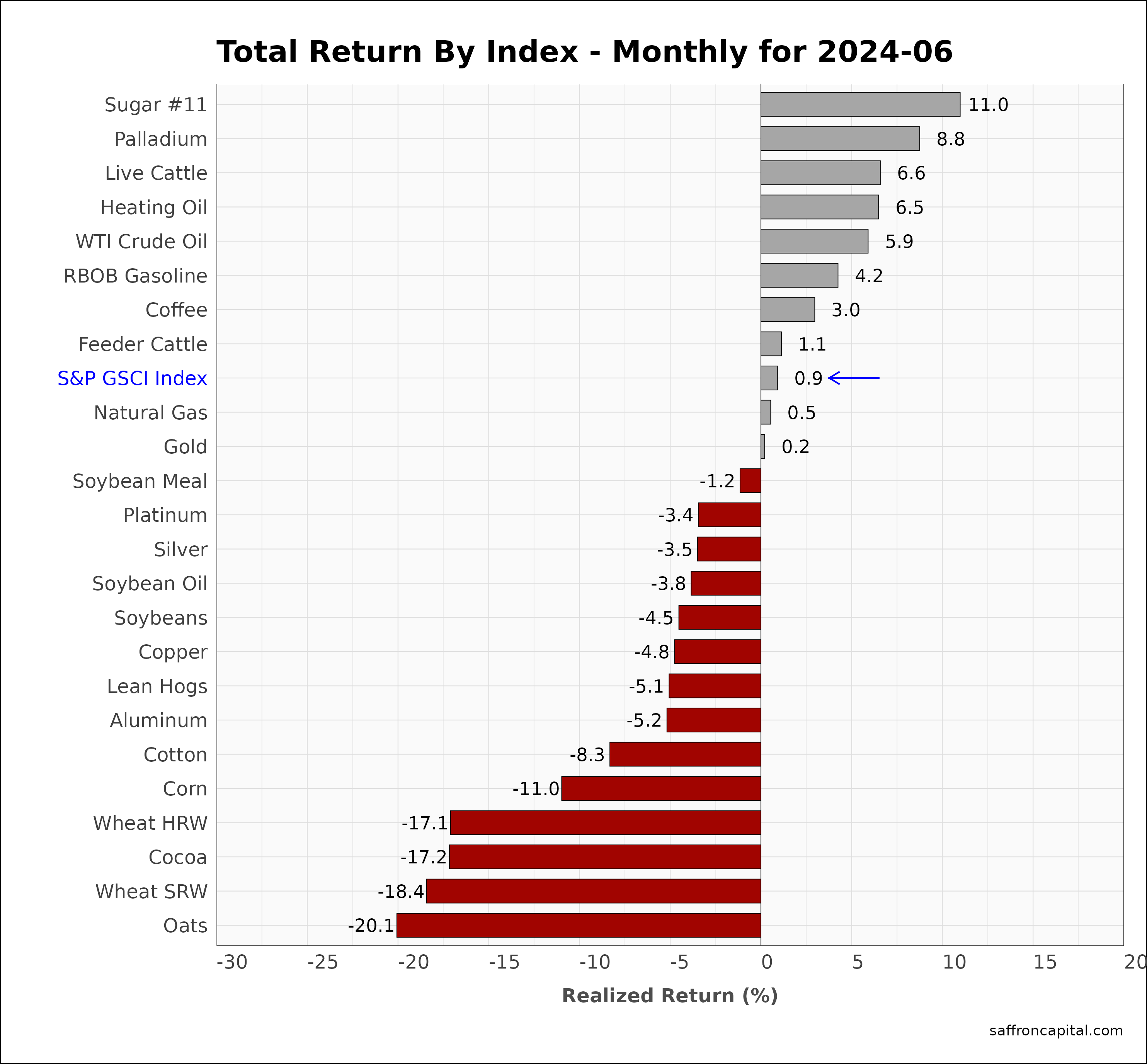

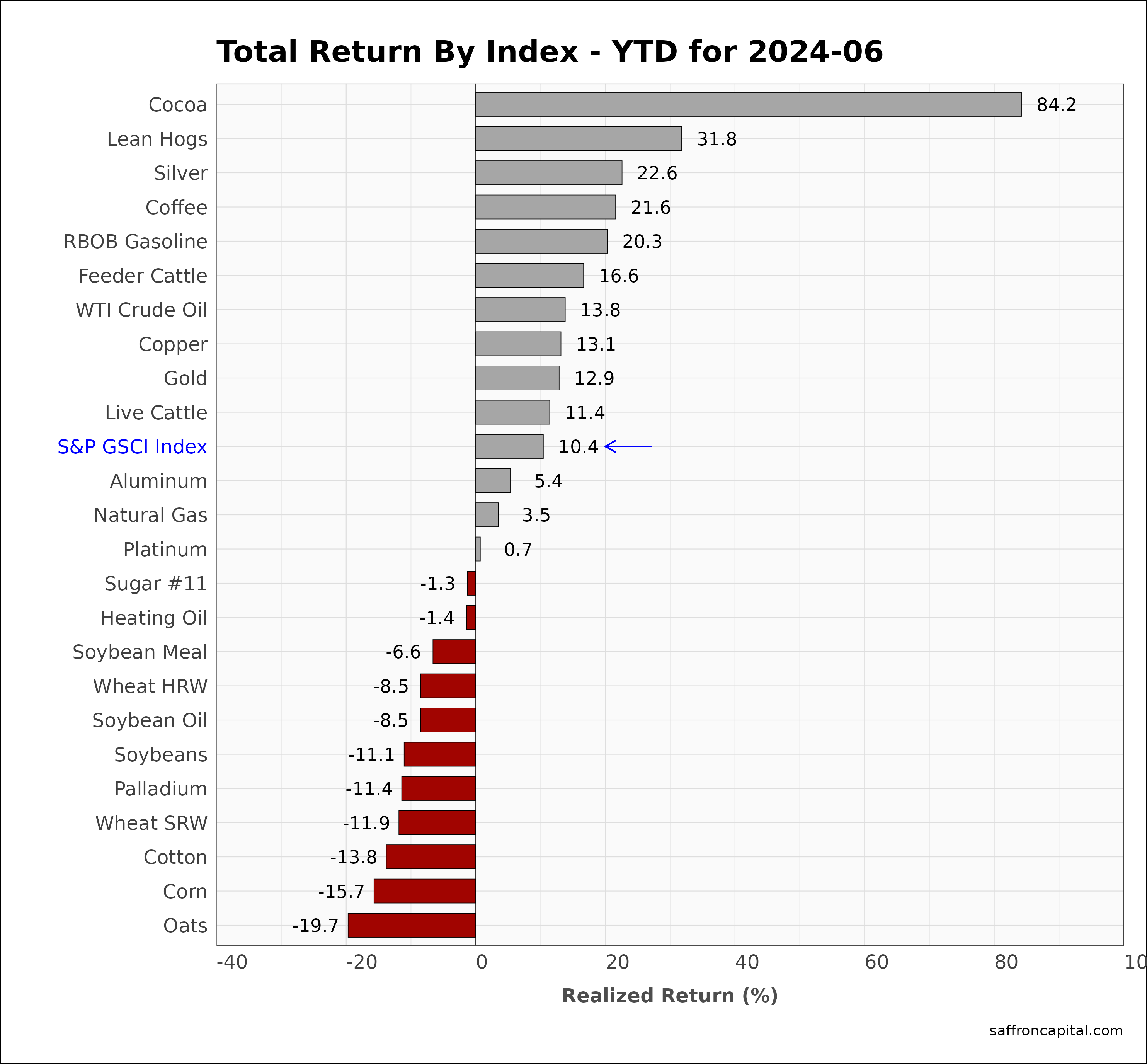

Commodities

Commodities, as measured by S&P GS Commodity Index (+0.9%) has struggled to gain traction as the US economy softens. Sugar (+11.0%) was an exception, as was Palladium (+6.8%). Heavy rains in the Midwest proved to be very favorable to grains as seen by sharp price declines for Oats (-20.1%), Wheat SRW (-18.4%) and corn (-11.0%) Even drought-prone cotton (-8.3%) has been weighed down. Since December, the GS commodity index is up 10.4%. Cocoa (+84.2%) leads YTD return, followed by Lean Hogs (+31.8%) and Silver (+22.6%).

Click to enlarge

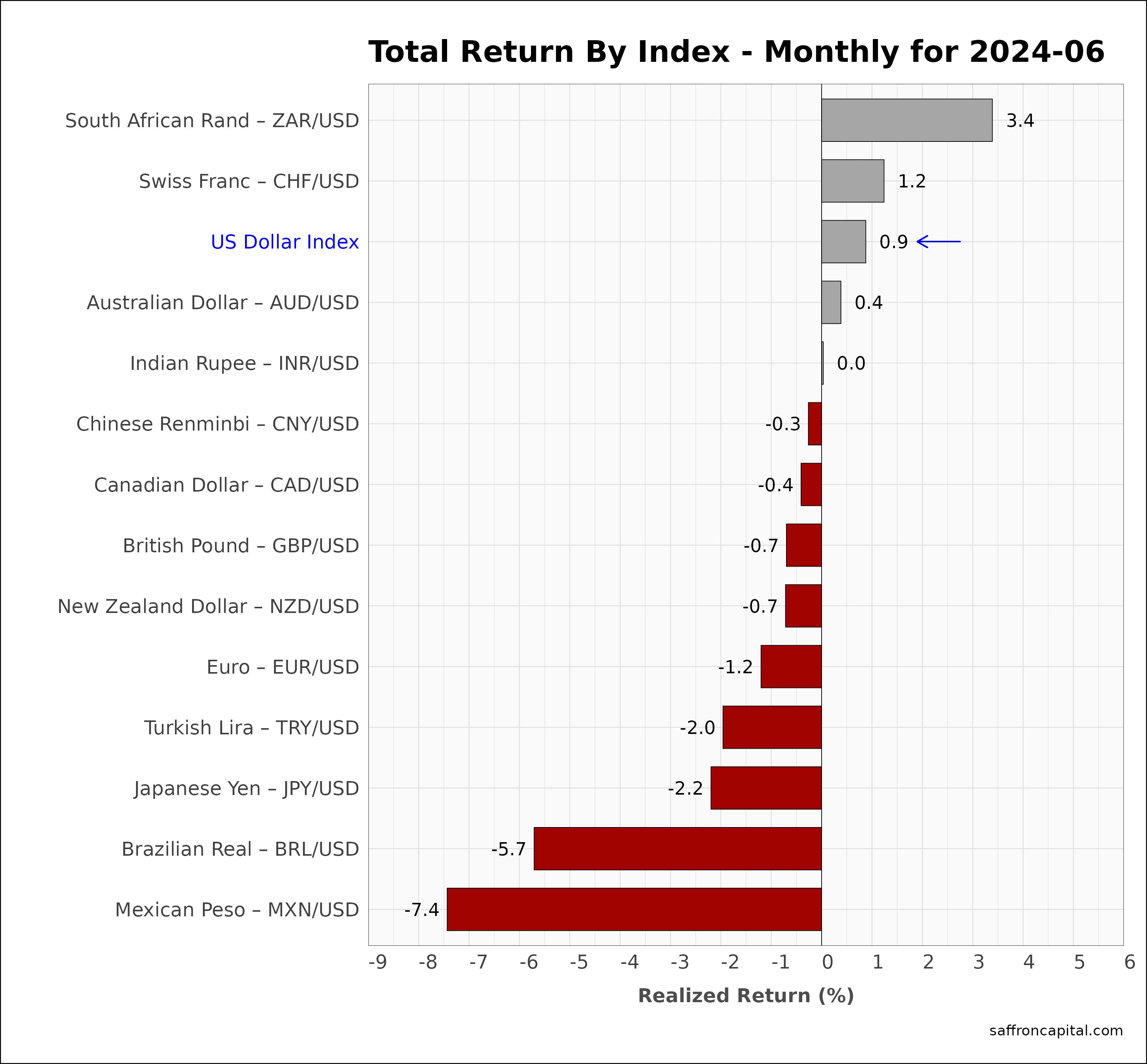

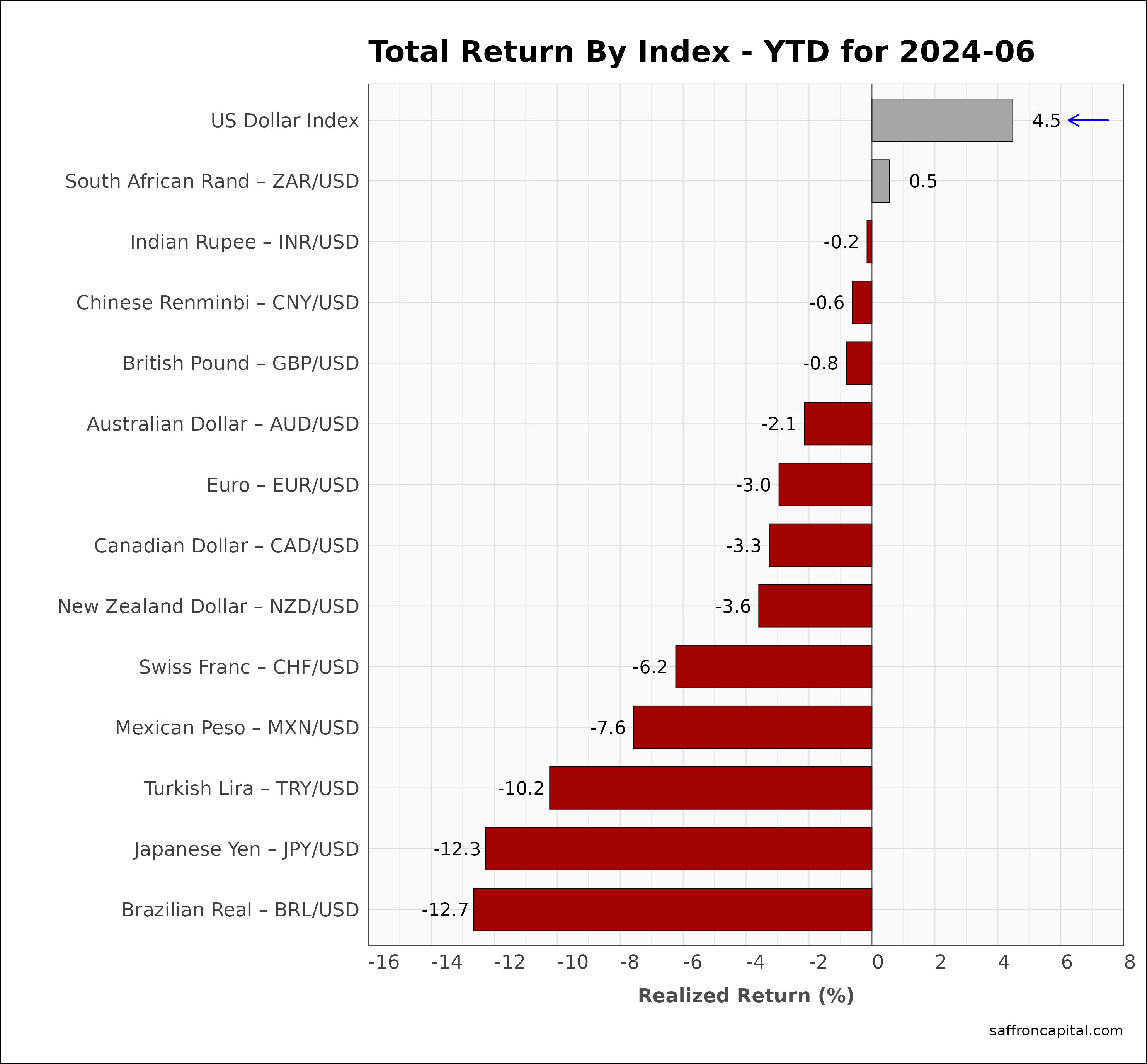

Currencies

The U.S. Dollar (+4.5%) continues to dominate returns on a year-date-basis. The weakest currencies since the first of the year include the Brazilian Real (-12.7%), the Japanese Yen (-12.3%) and the Turkish Lira (-10.2%).

Click to enlarge

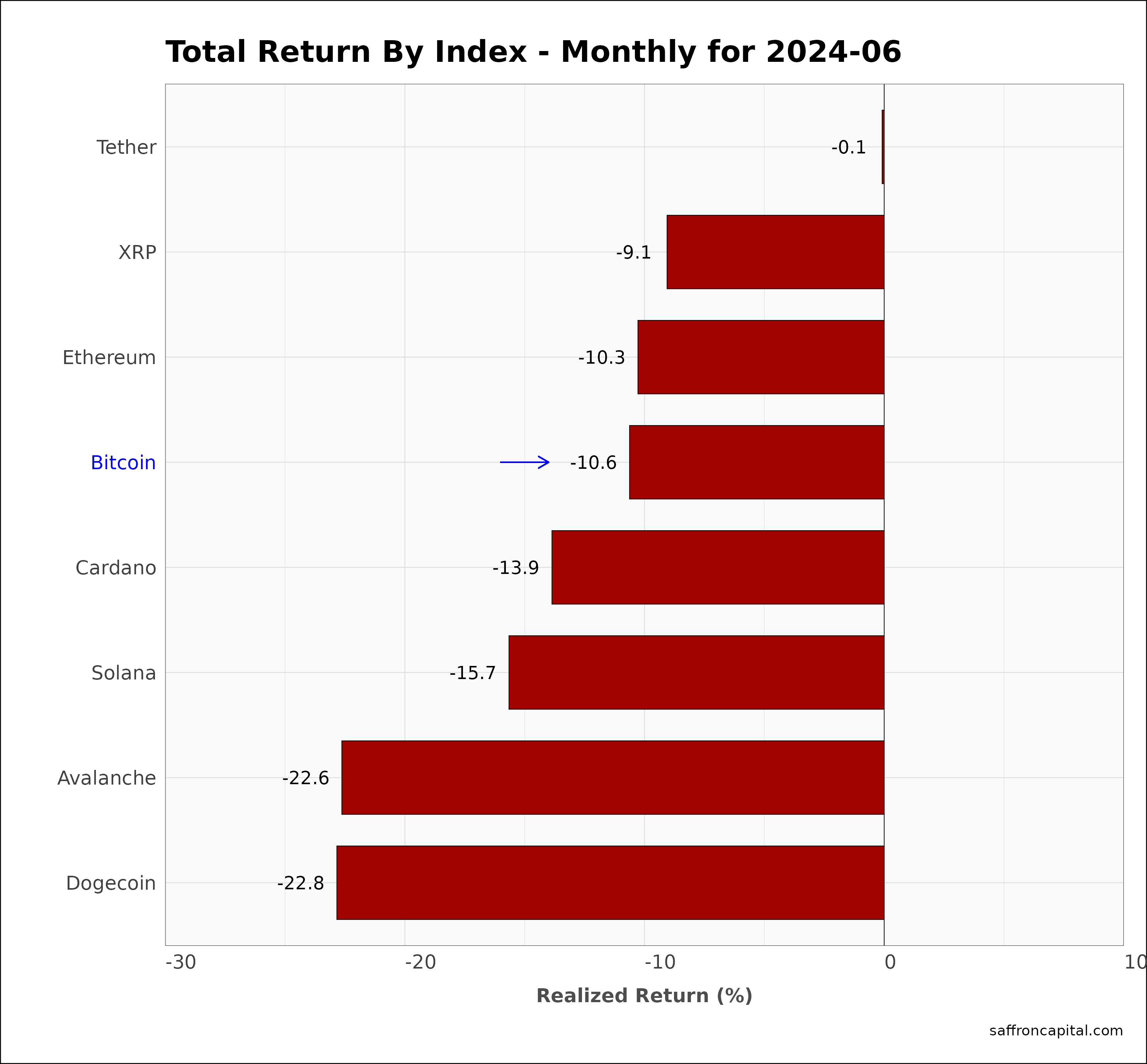

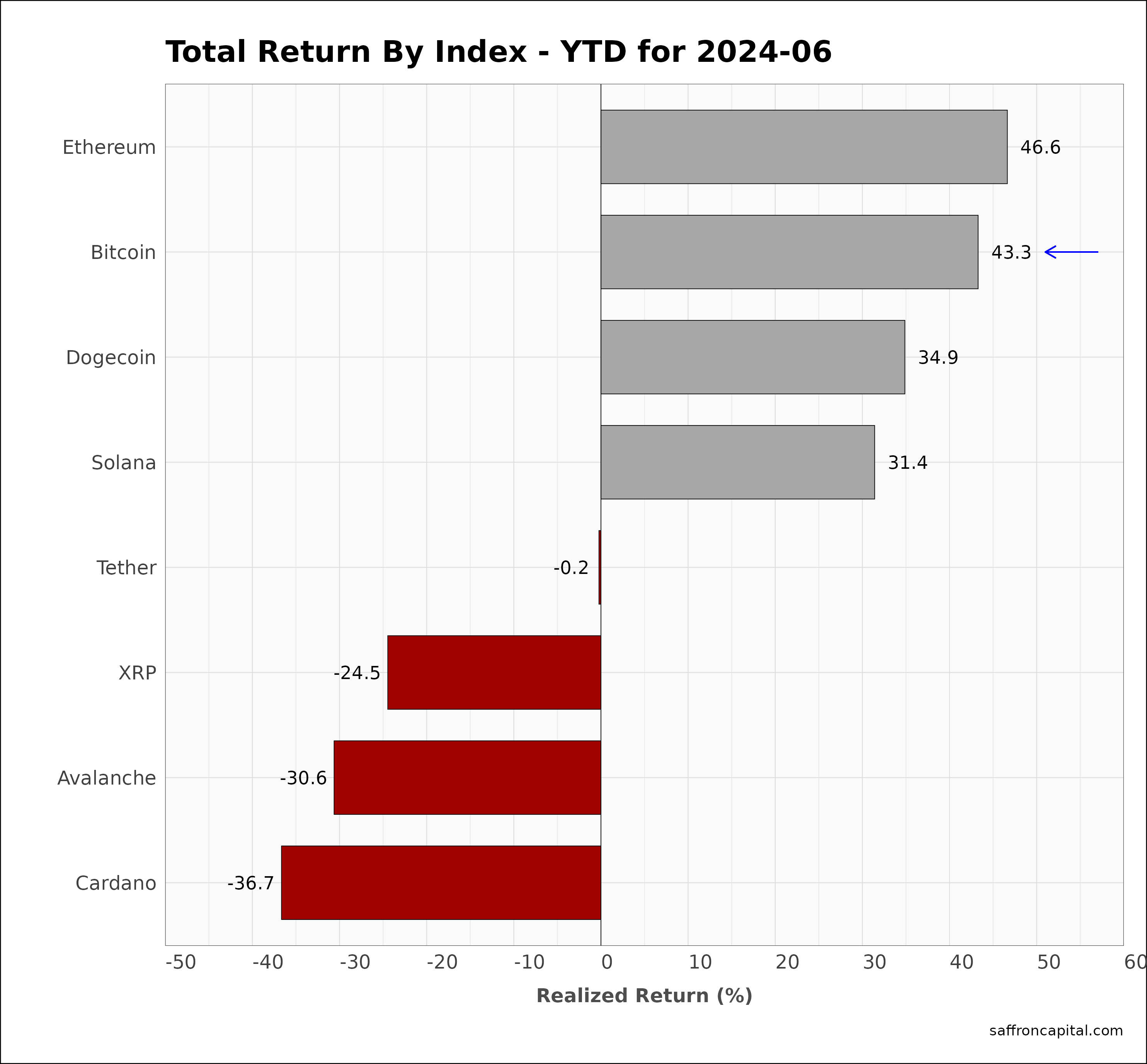

Cryptocurrencies

Cryptocurrencies were notably weak in June. Bitcoin (-10.6%) was topped by Etherium and XRP in June, and Dogecoin (-22.6%) was down the most. All the other mainstream cryptocurrencies were down significantly with Avalanche (-22.6%) also down. Year-to-date, Etherium (+46.6%) leads the pack, followed by Bitcoin (43.3%).

Click to enlarge

Have questions or concerns about the performance of your portfolio? Could you benefit from a custom portfolio formulation that better reflects your goals and risk appetite? Whatever your needs are, we are here to listen and to help. To schedule a call with us, please contact us here.

{kind=link}

{kind=link}