November returns for the S&P 500 index (+5.7%) were the strongest of the year, benefiting from a post-election rally. Government tax reform, deregulation, and improvements in government efficiencies launched the S&P 600 Small Cap index (+11.1%), while the 20Y+ Government Bond (+2.0%) ended its steep price decline as the rise in long-term yields moderated. Traditionally, yield curve normalization has favored stocks. Meanwhile, corporate earnings remain strong. 3rd quarter earnings for the S&P 500 index came in at +5.8% growth year-on-year, and analysts continue to project 12% annual earnings growth for the index in the 4th quarter. Net income growth is being led by banking, semiconductor, pharmaceutical, interactive media, and broadline retail industries.

The following analysis decomposes November returns by asset group, sector, and industry. The aim of the visual summary is to help investors to identify new opportunities and to benchmark their own portfolio returns.

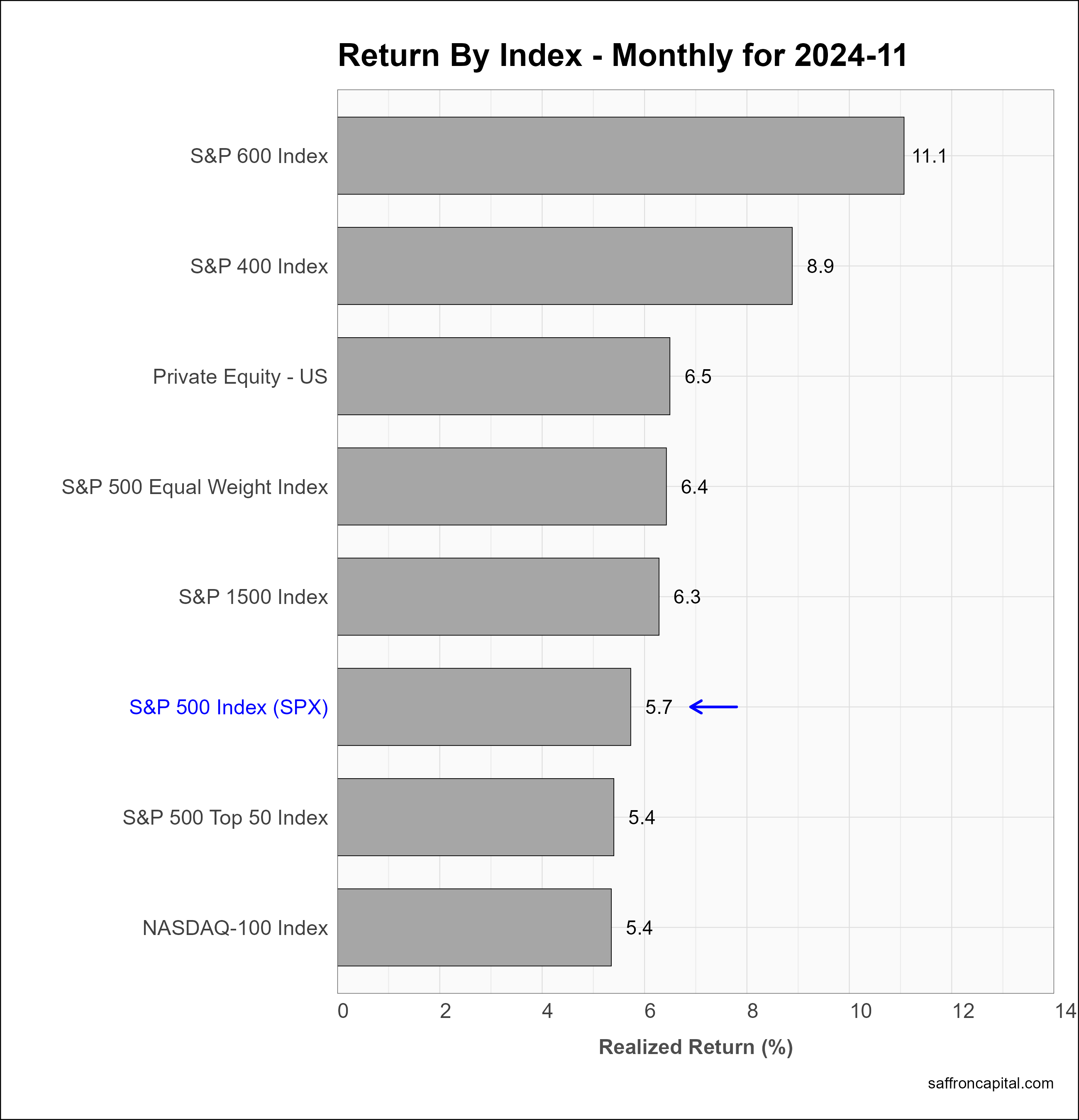

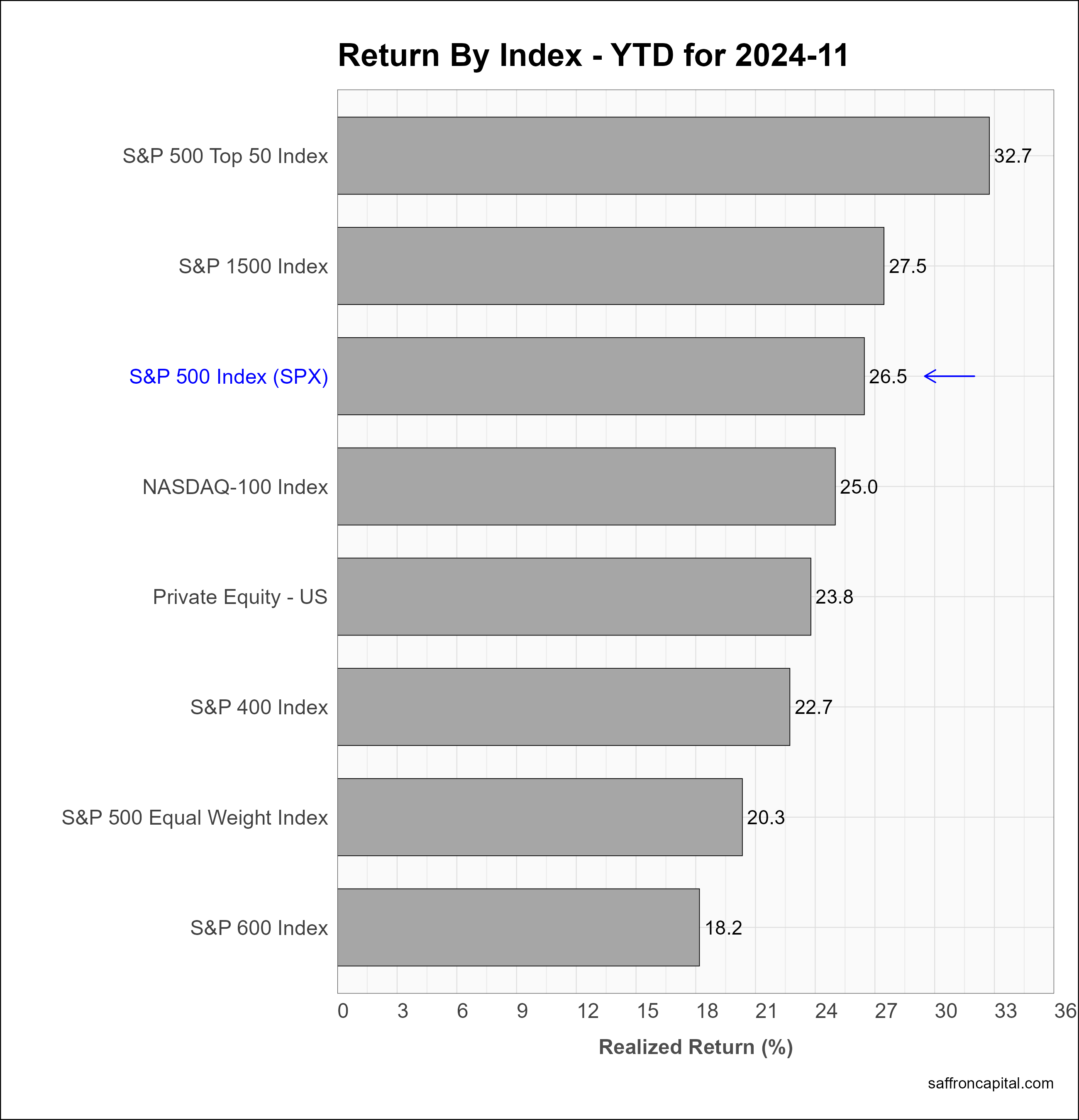

Core US Indices

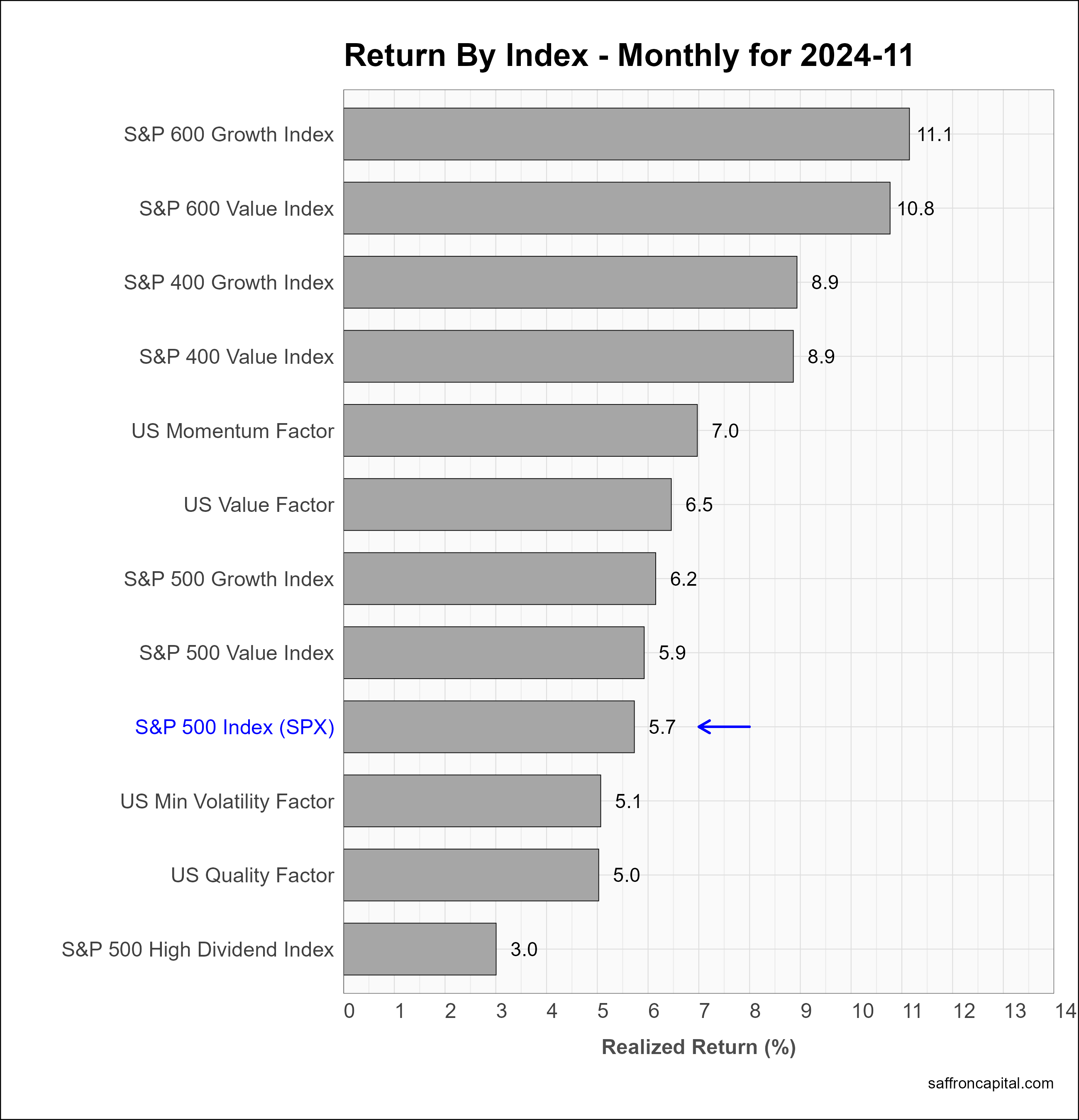

The S&P500 (+5.7%) posted its best month of 2024, closing the month at all-time highs. Top returns were generated by small cap (+11.1%), mid-cap (+8.9%), and private equity shares (+6.5%). The equal-weighted S&P 500 index (+6.4%) beat large cap stocks, notably the the S&P500 Top 50 index (+5.4%) and the NASADAQ-100 (+5.4%). Year-to-date (YTD), the S&P 500 index (+26.5%) continues to be led by the top 50 companies (+32.7%).

Click to enlarge

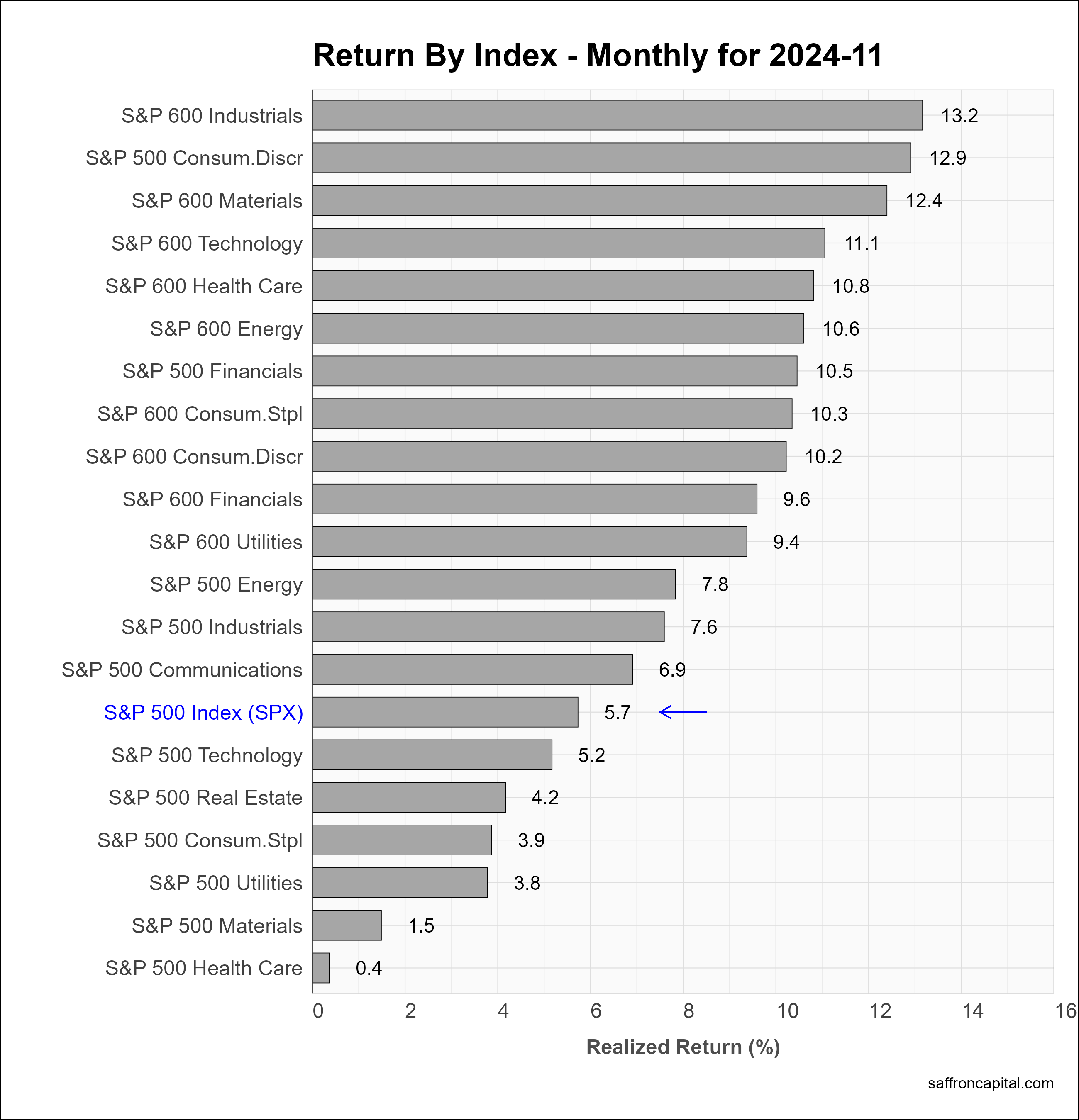

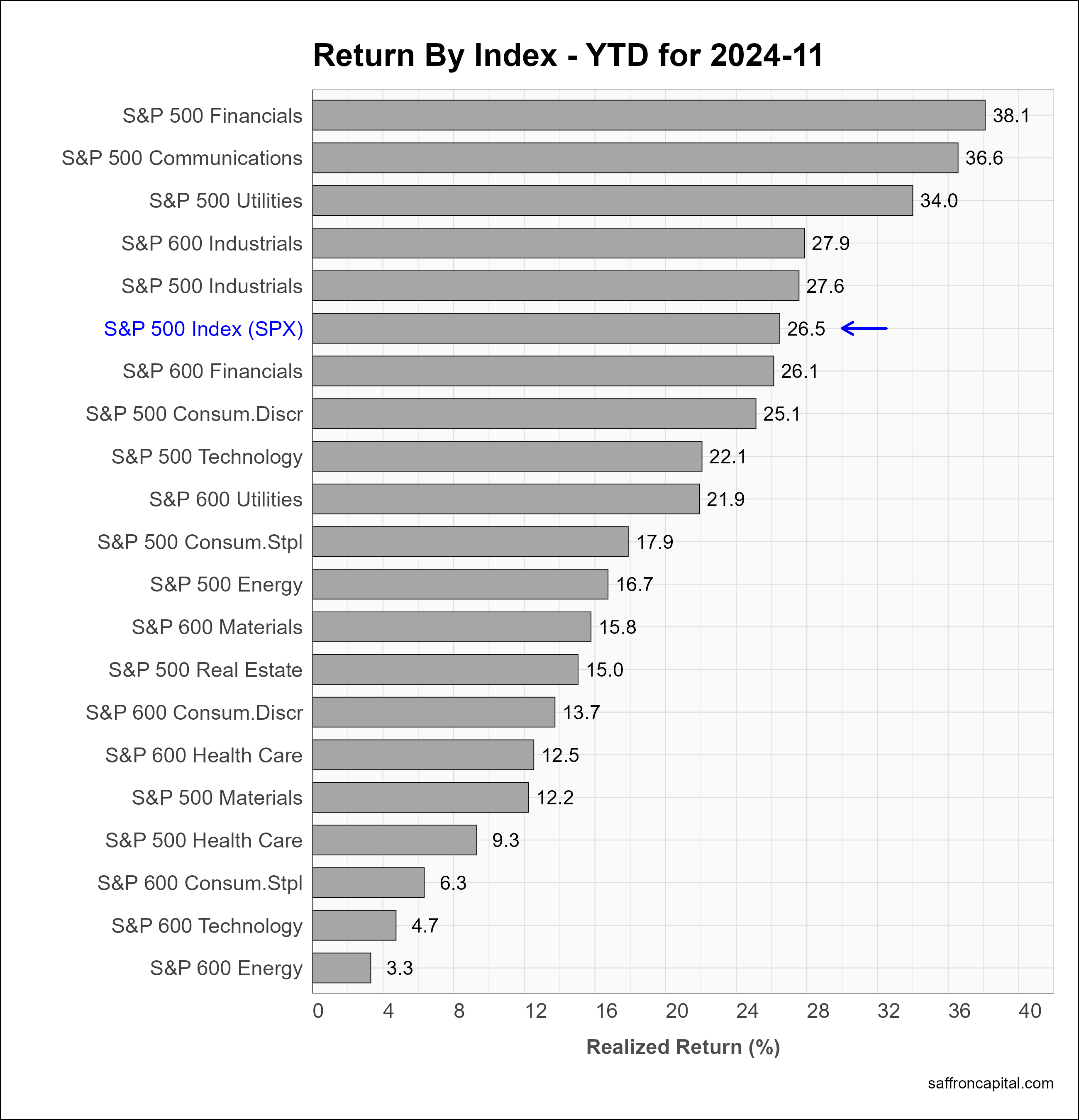

US Sector Indices

All select sectors posted positive November returns. Small cap sectors dominated the list with Industrials (+13.2%), Materials (+12.4%), and Technology (+11.1%) topping the list. The top large-cap sectors were Consumer Durables (+12.9%), Financials (+10.5%) and Energy (+7.8%). The weakest sectors were large-cap Utilities (+3.8%), Materials (+1.5%), and Health Care (+0.4%). As pointed out last month, the high number of sectors beating the S&P 500 index is ongoing evidence market breadth is expanding.Since January, the top sectors are large cap Financials (+38.1%), Communications (+36.6%) and Utilities (+34.0%).

Click to enlarge

US Factor Indices

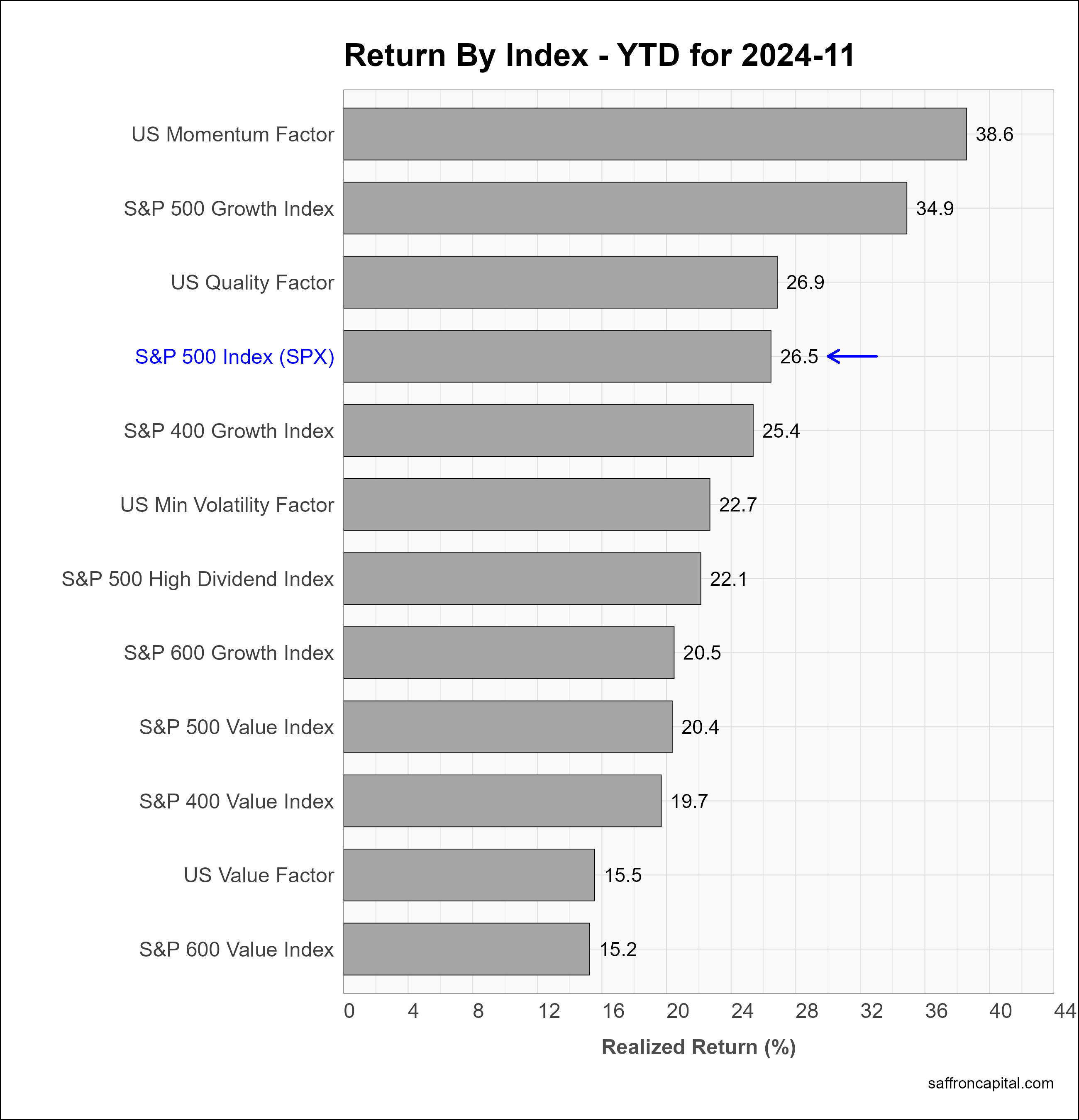

Factor portfolios are constructed to emphasize the core drivers behind returns, such as company size, value, profitability, growth, and momentum. Multi-factor portfolios combine two or more factors. During November, US factor returns were broadly positive. Top factor returns included the Small Cap Growth (+11.1%), Small Cap Value (+10.8%), and mid Cap Growth (+8.9%). Since the start of the year, the US Momentum Factor (+38.6%) continues to lead all factor indices. Other top performers include the S&P500 Growth index (+34.9%), and the U.S. Quality factor (+26.9%).

Click to enlarge

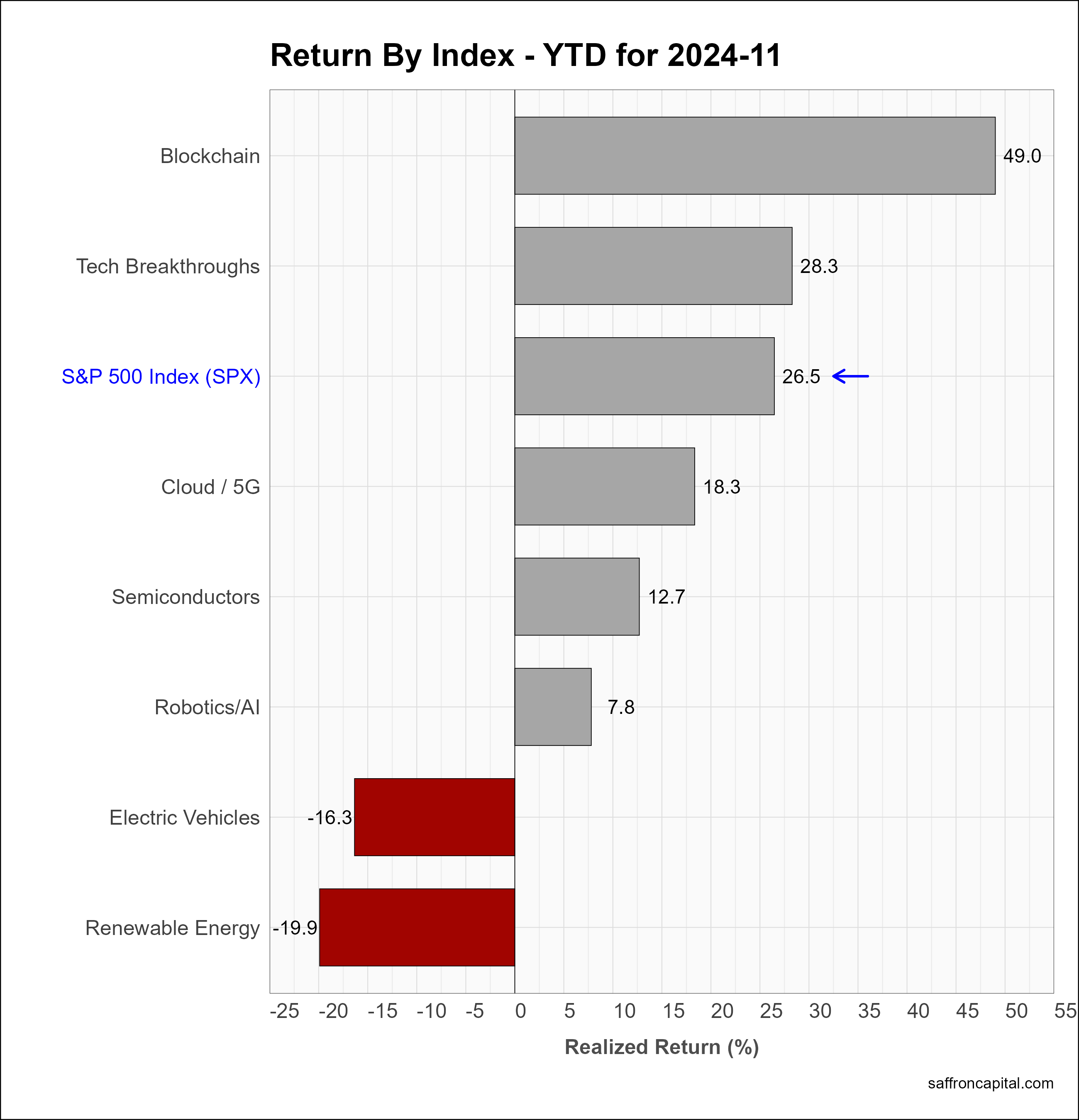

US Megatrend Equities

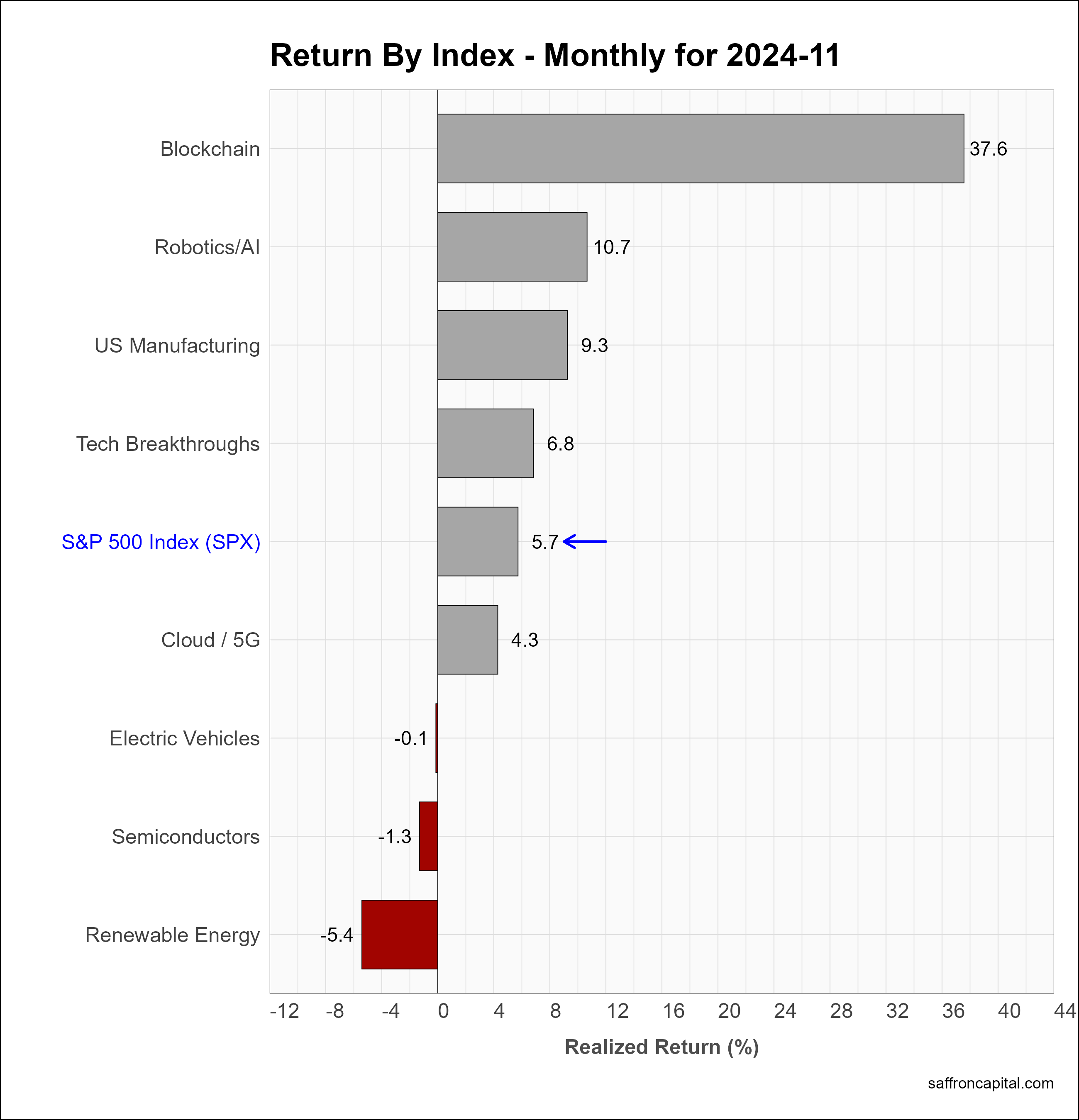

US megatrend equities are thematic growth portfolios. The aim is to select shares that capture the primary secular trends of the U.S. economy. . November returns were led by Blockchain shares (+37.8%), Robotic/AI shares (+10.7%), and U.S. Manufacuring (+9.3%). Negative returns were posted for Renewable Energy shares (-5.4%), Semiconductors (-1.3%), and Electric Vehicles (-0.1%). Since January, Blockchain shares (+49.0%) and Tech Breakthroughs (+28.3%) are outperforming the S&P 500 index. Underperformance is most evident in shares for Renewable Energy (-19.9%) and Electric Vehicles (-16.3%).

Click to enlarge

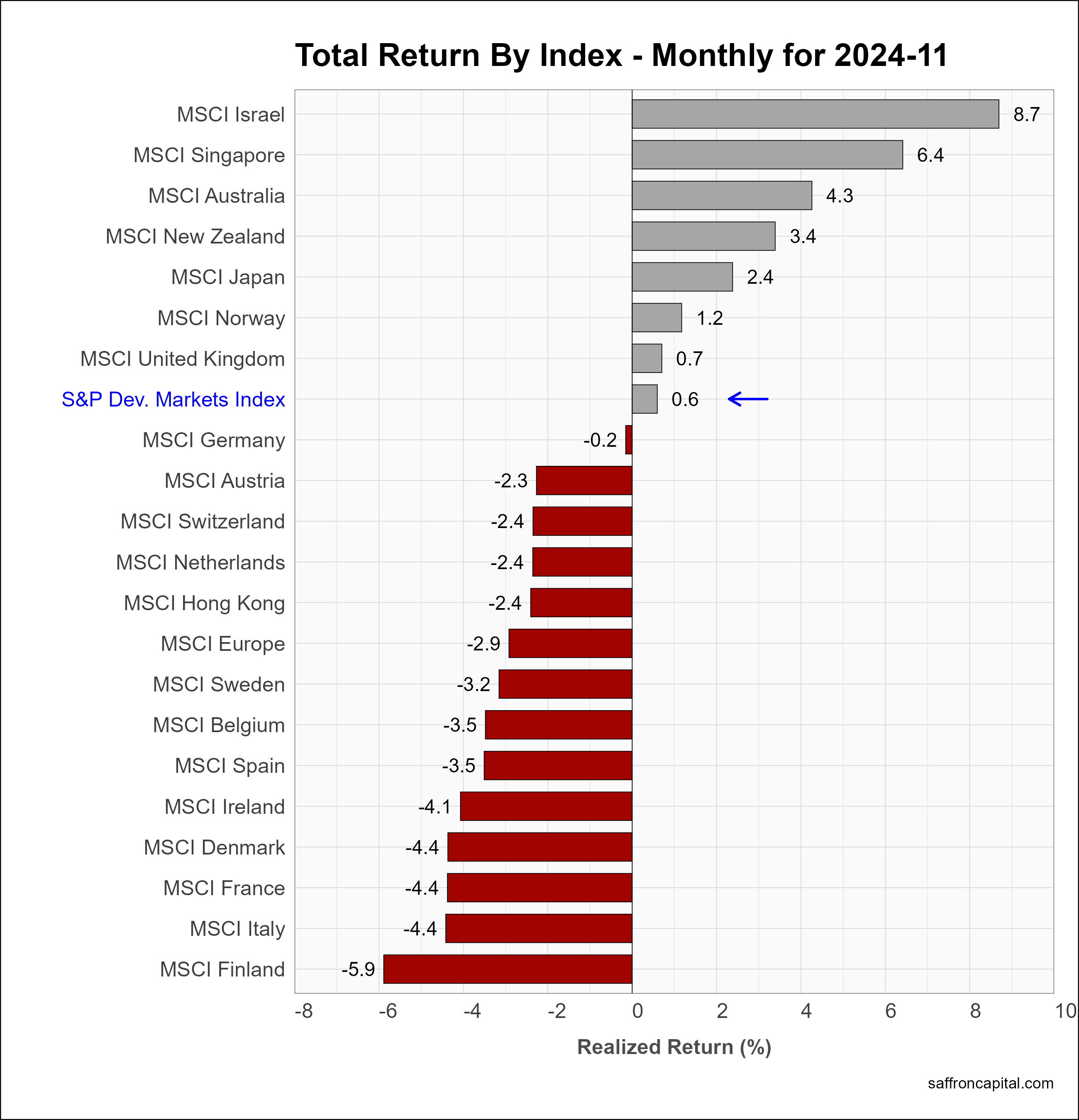

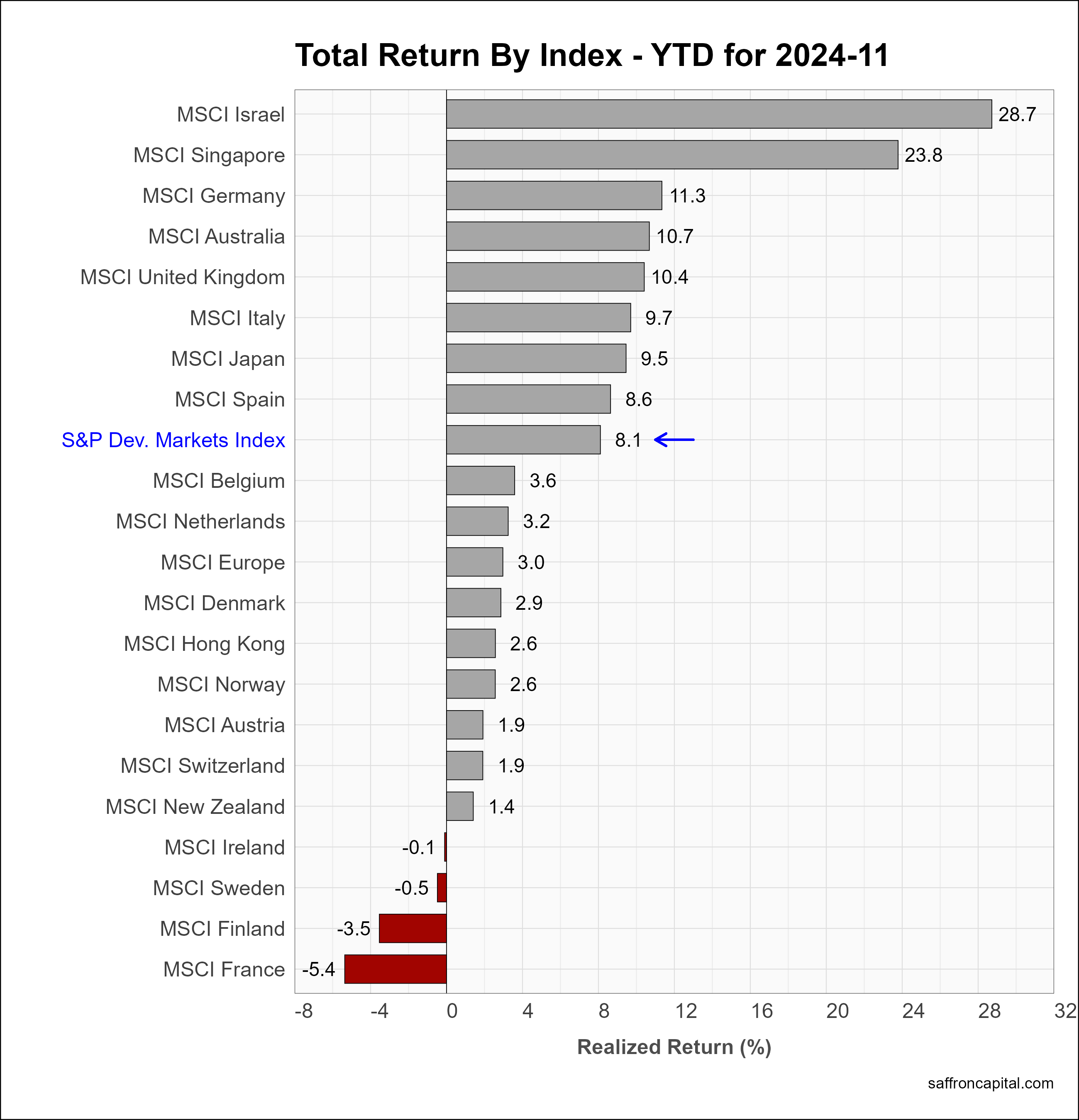

Developed Market Equities

International developed markets (+0.8%) were lackluster on average, but several markets outperformed the U.S., notably Israel (+8.7%), Singapore (+6.4%) and Australia (+4.3%). Theses top performers are also among the top performing developed markets in 2024, which include Israel (+28.7%), Singapore (+23.8%), and Germany (+11.3%).

Click to enlarge

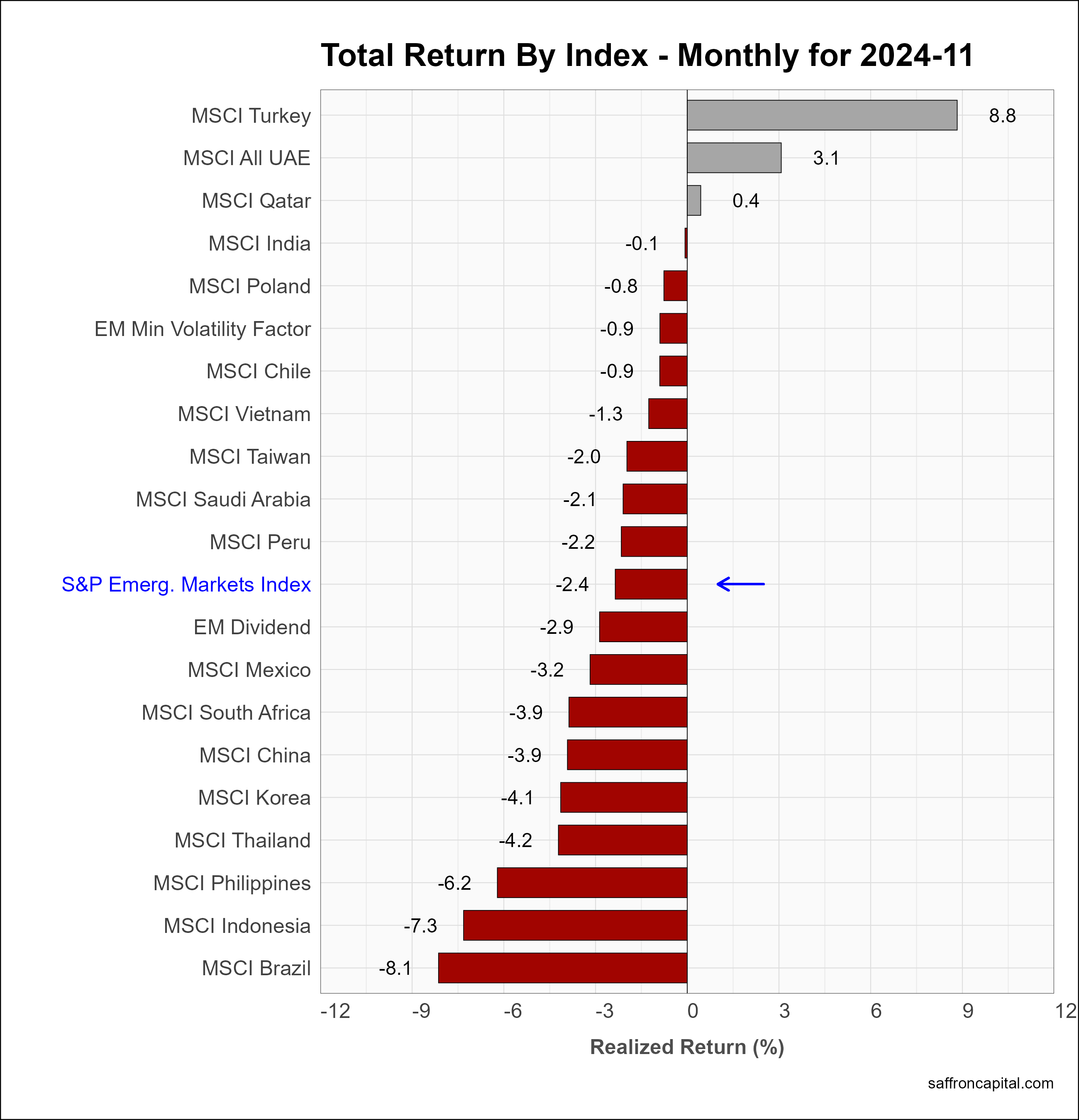

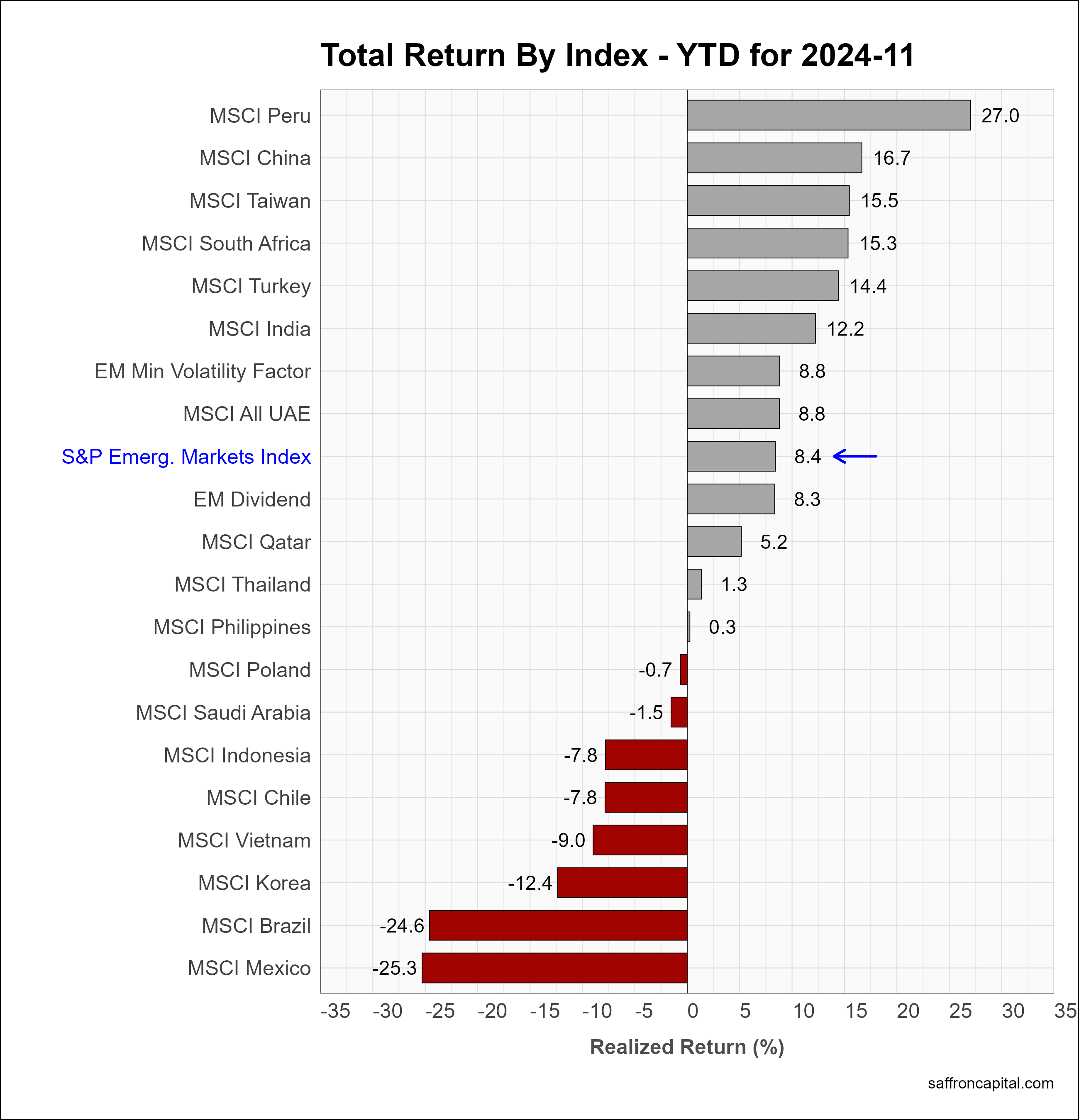

Emerging Market Equities

The S&P Emerging Markets Index (-2.4%) posted negative returns in November. The only countries with positive returns were Turkey (+8.8%), the UAE (+3.1%) and Qatar (0.4%). India was unchanged (-0.1%), while China (-3.9%) failed to sustain gains after supporting fiscal stimulus. Nothwistanding, year-to-date performance for China (+16.7%) is near the top of the list, as is Taiwan (+15.5%), and India (+12.2%). Last year’s stars, Mexico (-25.3%) and Brazil (-24.6%), are now at the bottom of the annual rankings.

Click to enlarge

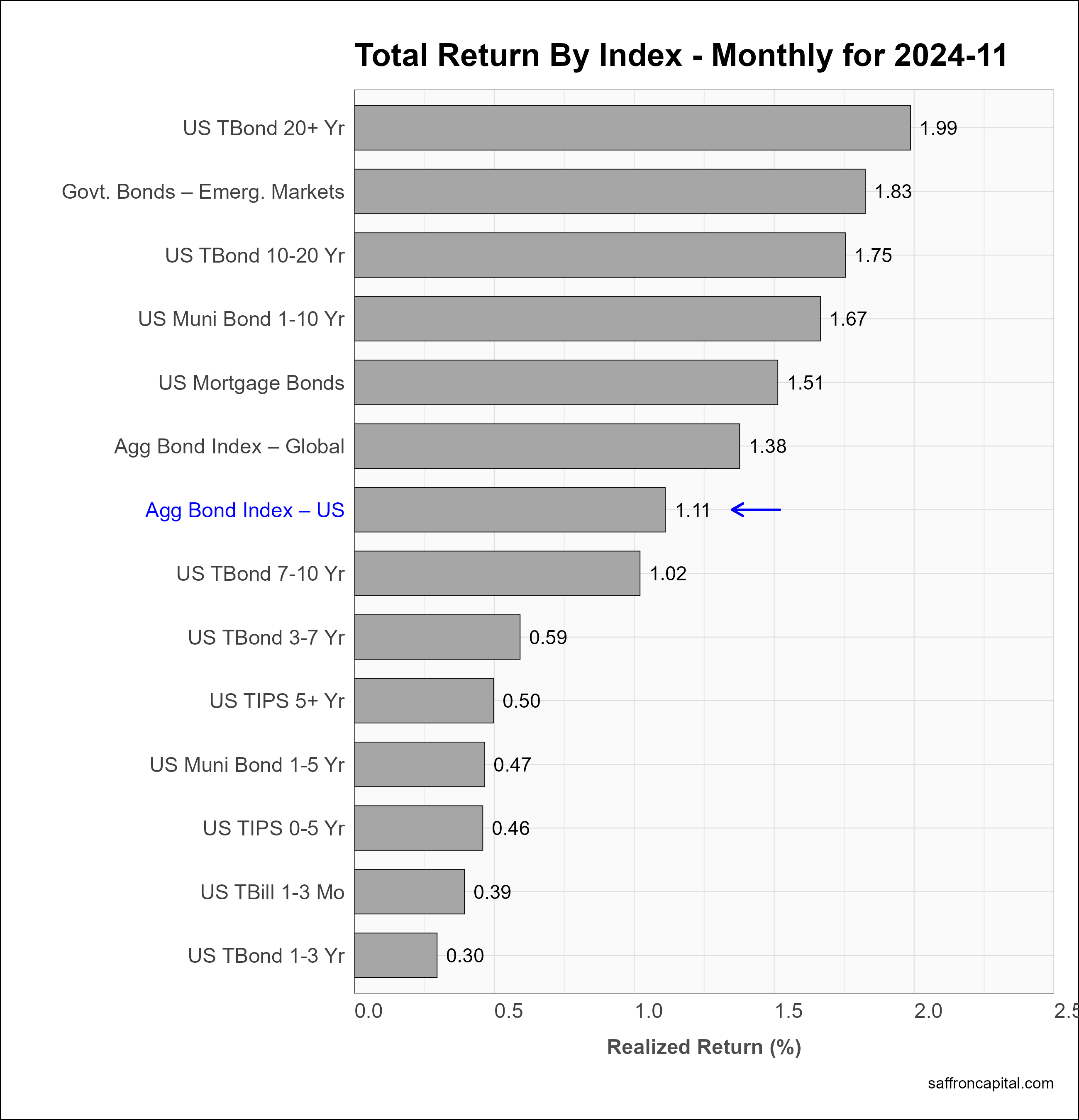

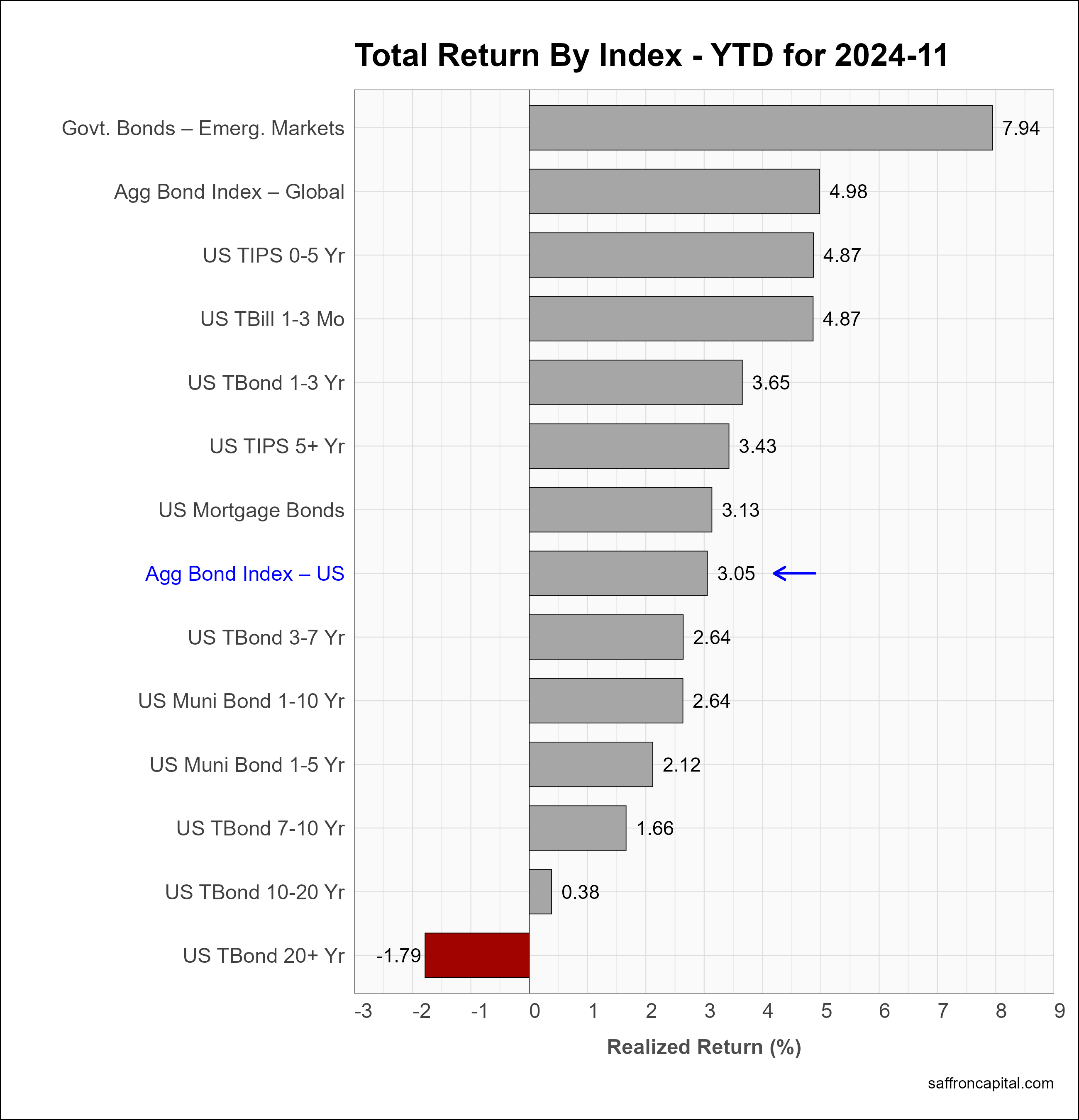

Government Bonds

The US fixed income markets turned positive in November. The FOMC voted unanimously at their November meeting to cut the target range for the fed funds rate to 4.50‐4.75%. Committee minutes confirm the U.S. economy is performing remarkably well, with the labor market “normalizing” and inflation cooling off. The Aggregate Bond Index (+1.11%) was led by the long duration 20Y+ T-Bond (+1.99%). Year-to-date, the US Aggregate Bond index (+3.05) is yet to recover the peak performance seen earlier in the year. In comparison, Emerging Market Government Bonds (+7.94%) have twice the returns of the U.S. market in 2024. As a result, the Global Aggregate Bond Index (+4.98%) is outperforming the US index.

Click to enlarge

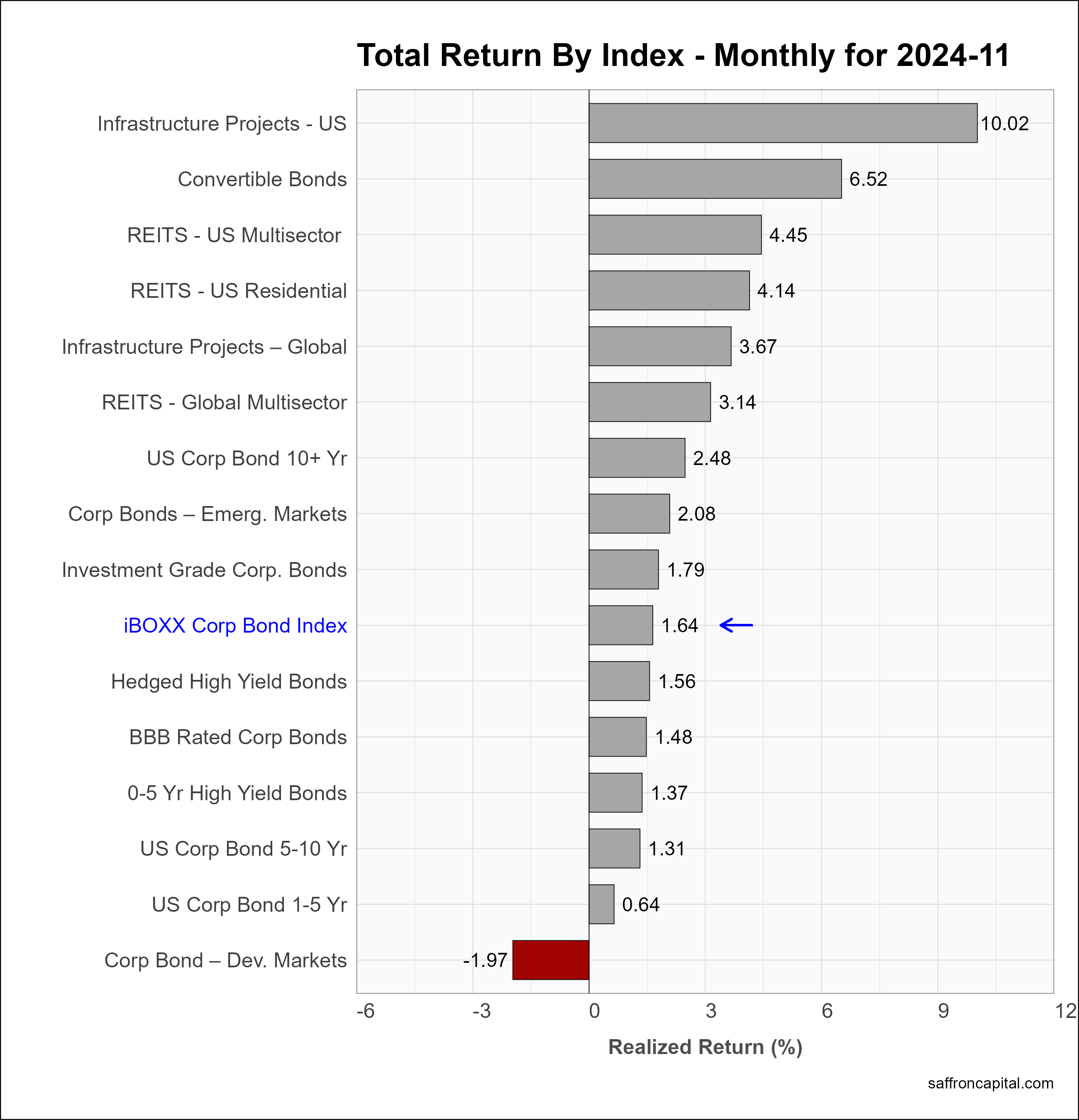

Corporate & Infrastructure Bonds

The iBoxx Corporate Bond Index (+1.64%) outperformed the government Aggregate Bond index (+1.11%). Bonds for US Infrastructure projects (+10.02%) topped the list, with aggressive buying again returning to REITS, both US Multisector (+4.45%) and Residential (+4.14%). Global infrastructure projects (3.67%) and Global Multisector REITS (+3.14%) also had strong returns for the fixed income space. Year-to-date, the IBOOX Corp Bond index (+8.82%) has yielded more than twice the return of low-risk government bonds. The key driver has been industries critically sensitive to interest rates, notably infrastructure and real estate. Returns on US infrastructure projects (+29.8%) are followed by returns on US Residential REITS (+22.92%) and Global Infrastructure projects (+20.39%).

Click to enlarge

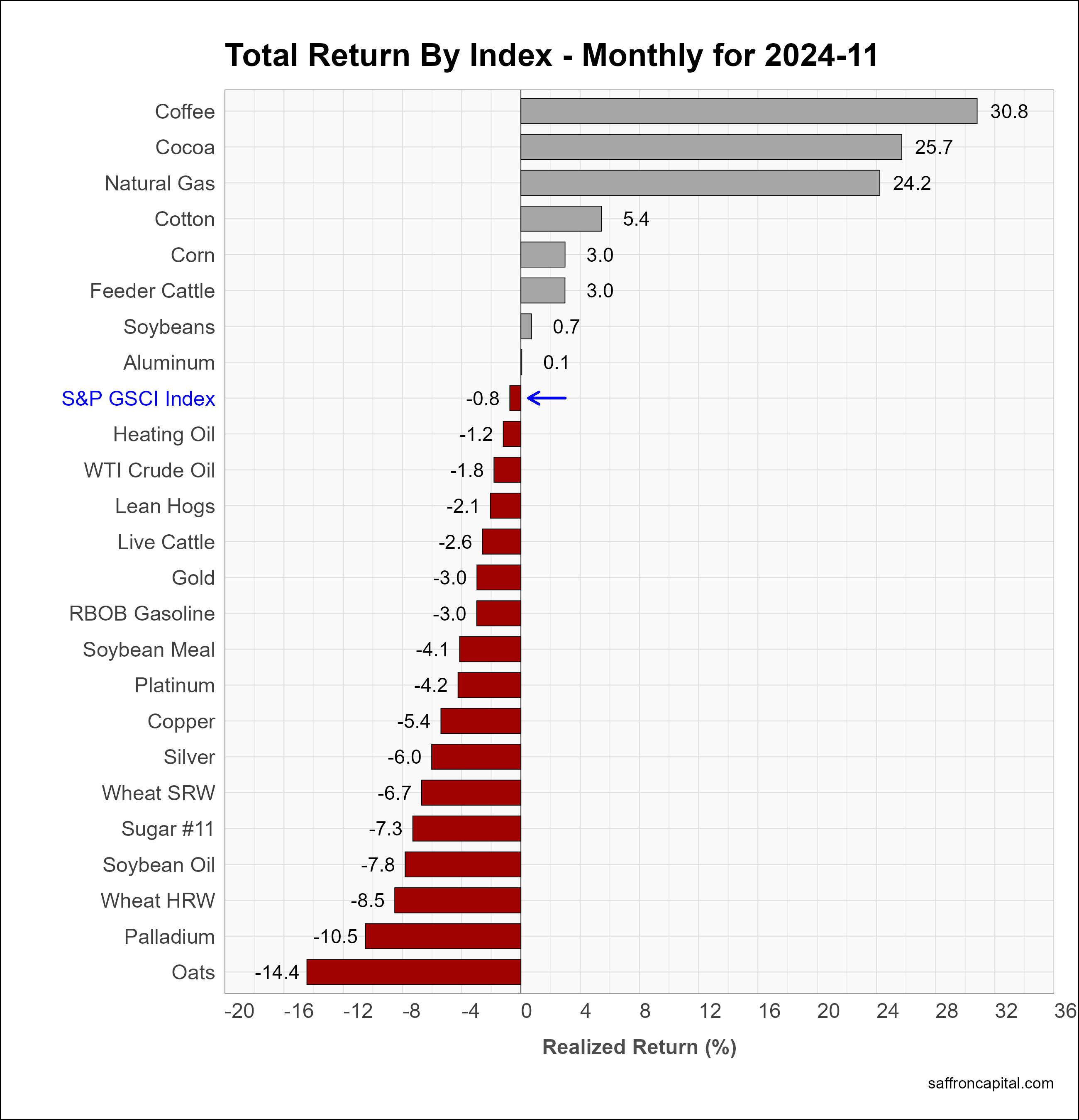

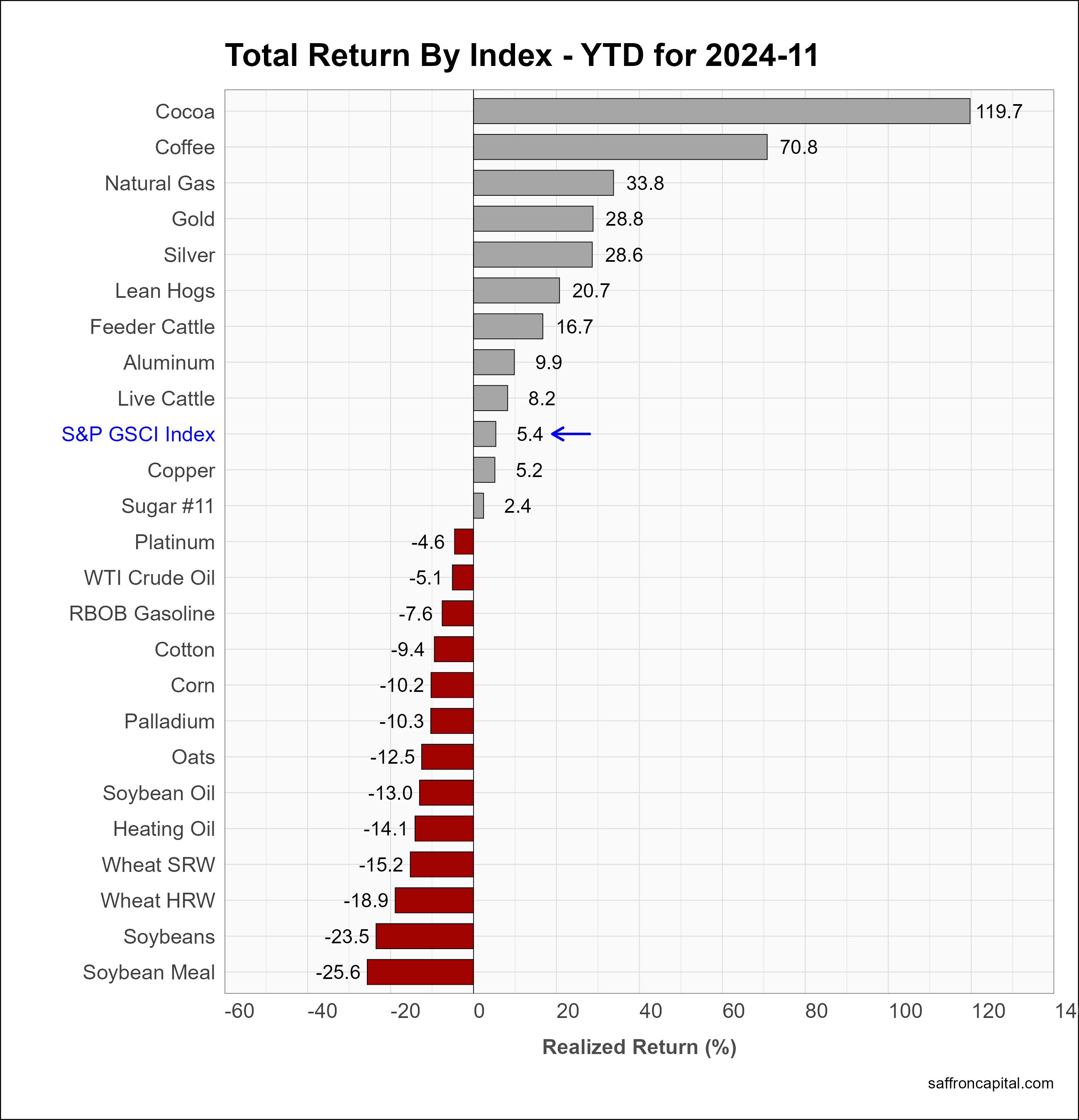

Commodities

Commodities, as measured by S&P GS Commodity Index (-0.8%) were flat for the month, though a wide range of results are seen across commodities. Coffee (+30.8%), Cocoa (+25.7%) and Natural Gas (+24.2%) easily topped the list. Price declines were most evident in Oats (-14.4%), Palladium (-10.5%), and Wheat HRW (-8.5%). In 2024, the GS commodity index is up 5.4%.

Click to enlarge

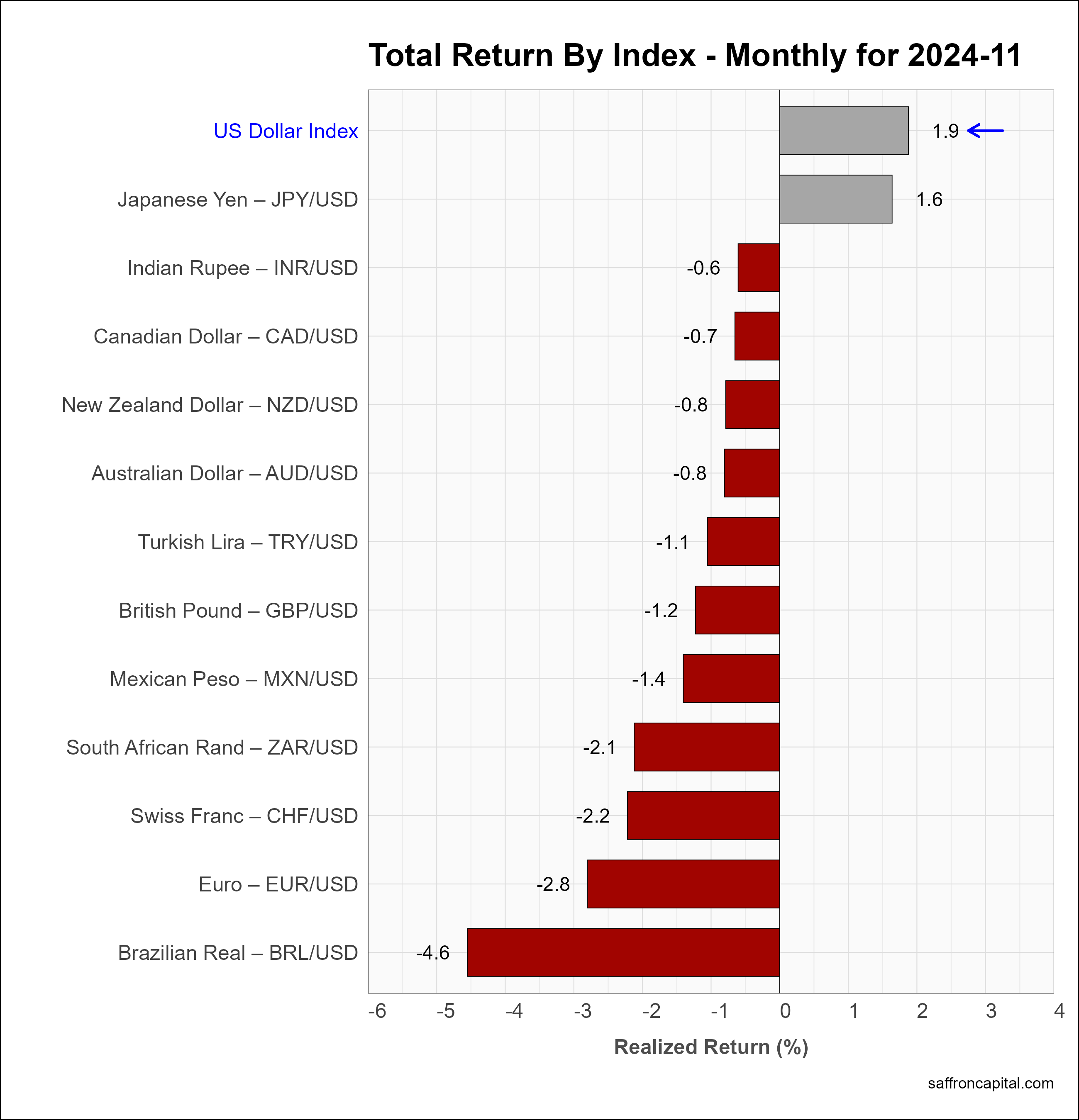

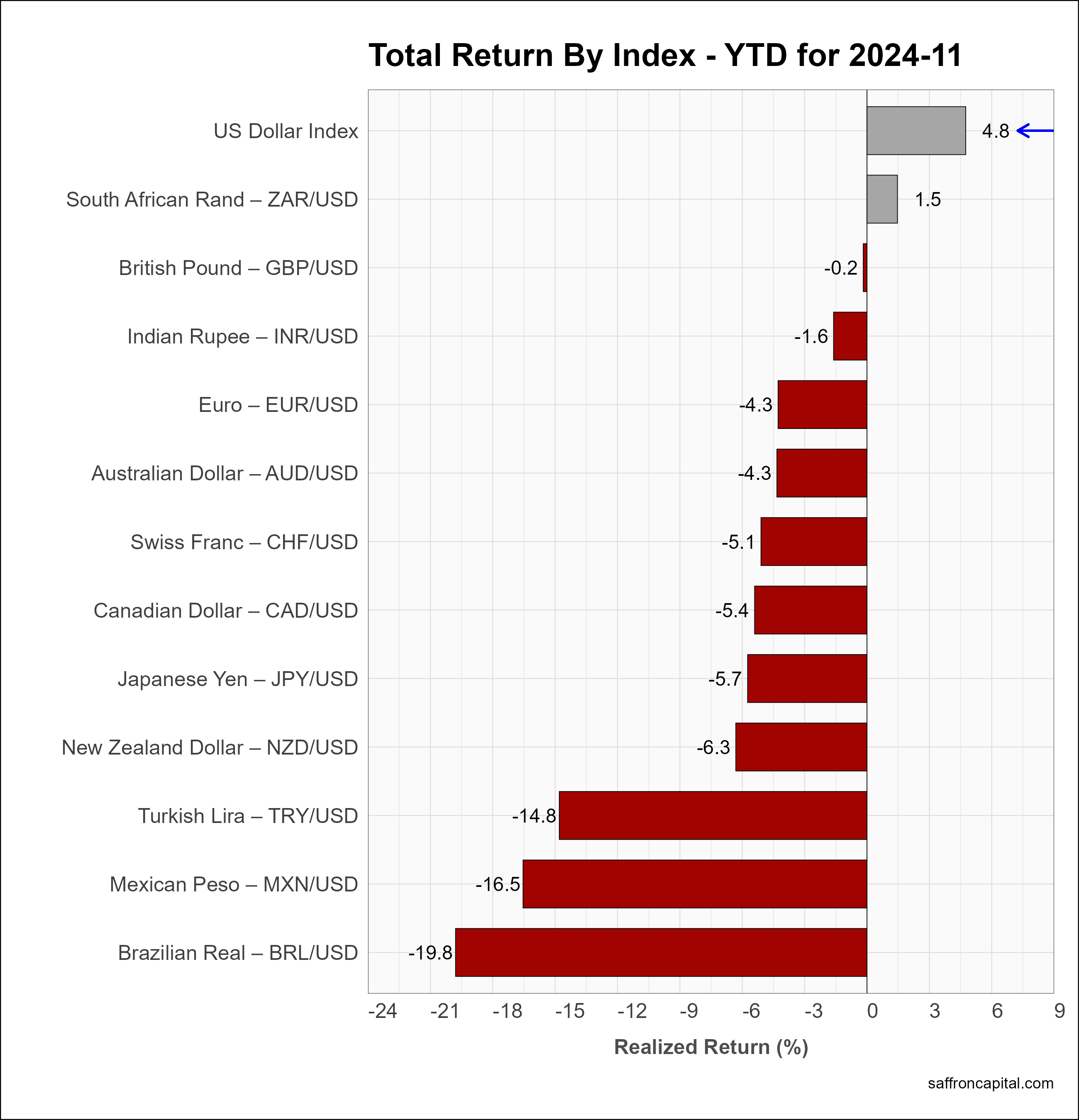

Currencies

The U.S. Dollar index (+1.9%) was strong in November. The Japanese Yen (+1.6%) led currency gains, while the Euro (-2.8%) was down sharply, along woith the Brazilian Real (-4.6%). Year-to-date returns for the U.S. Dollar index (+4.8%) remain strong.

Click to enlarge

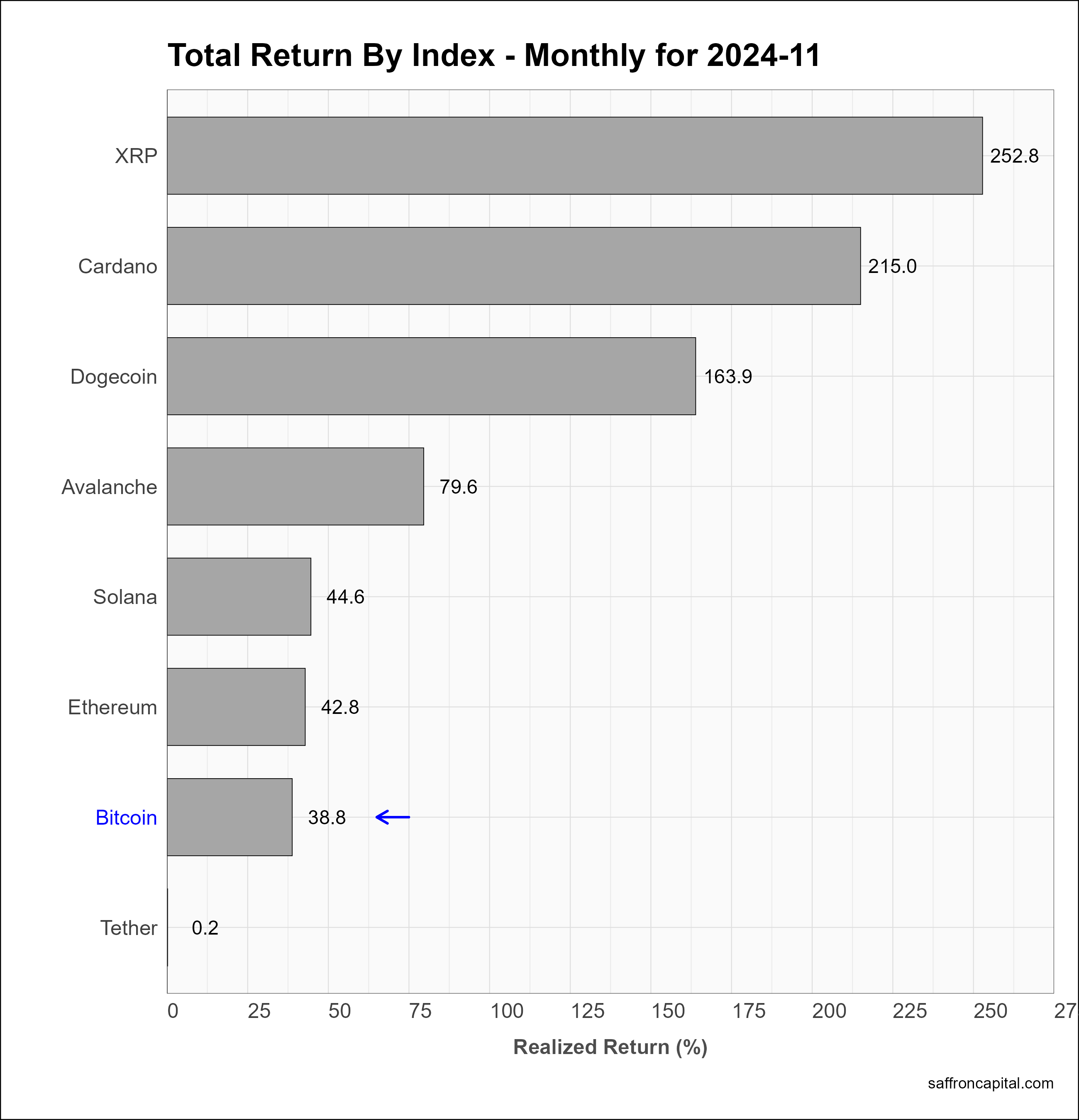

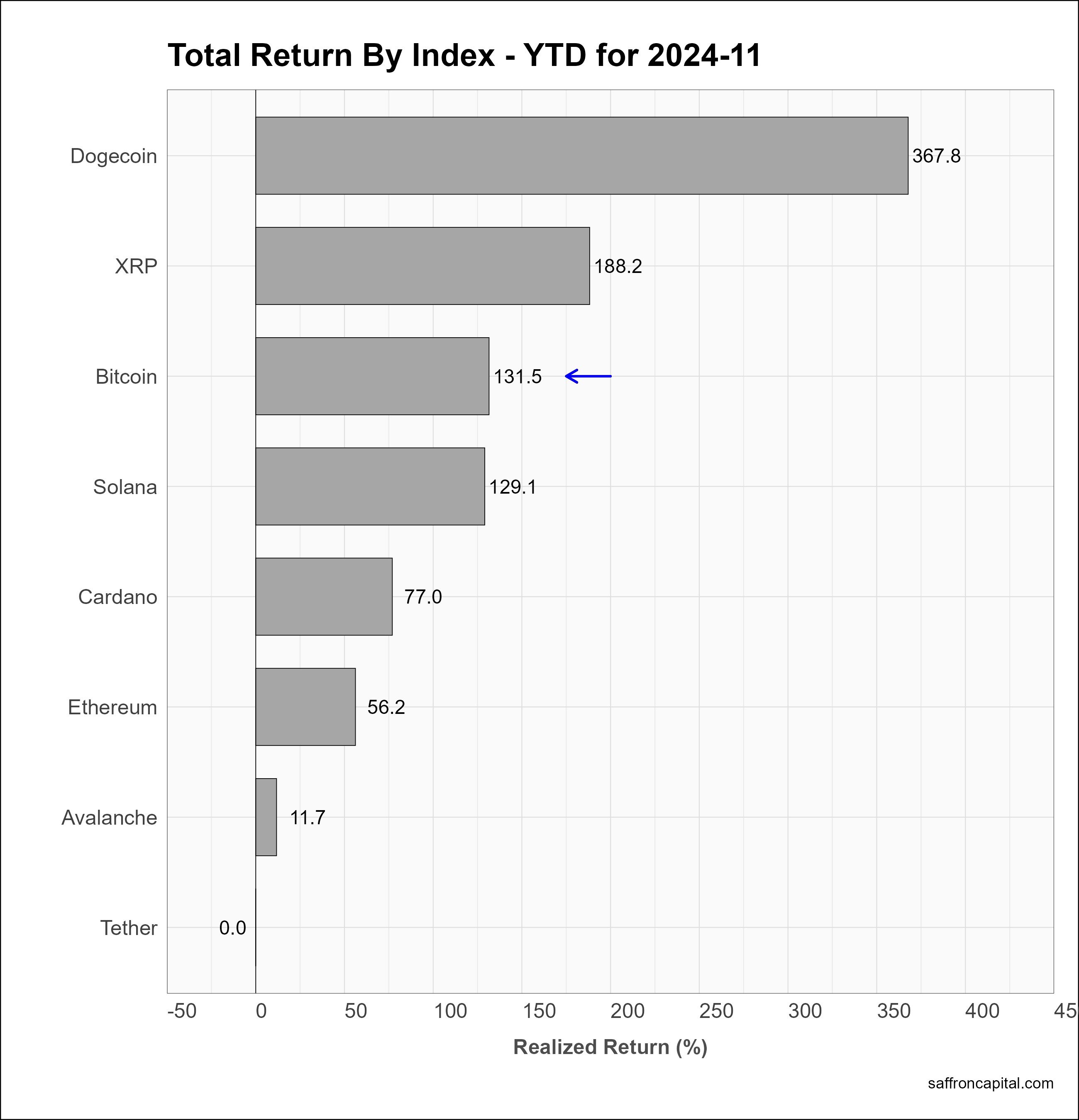

Cryptocurrencies

Cryptocurrencies had positive November returns with XRP (+252.8%), Cardano (+215.0%), and Dogecoin (+163.9%) leading the asset group. Bitcoin (+36.8%) serves as a benchmark and trailed the top performers. Year-to-date, gains on Bitcoin (+131.5%) remain impressive.

Click to enlarge

Have questions or concerns about the performance of your portfolio? Could you benefit from a custom portfolio formulation that better reflects your goals and risk appetite? Whatever your needs are, we are here to listen and to help. You can contact us here.

Saffron Capital LLC is a registered investment advisor that is employee-owned and Minnesota-based. The company uses Interactive Brokers as its bank custodian and clearing merchant.

{kind=link}

{kind=link}