December returns for the S&P 500 index (-2.7%) were down, but lead global markets by a wide margin for the year (+23.3%). US government bonds (-1.7%) were also down in December, struggling to stay positive in 2024, but ending the year with modest gains (+1.6%). Similarly, December returns for corporate and infrastructure project bonds (-0.7%) were also down, but annual returns (+8.5%) significantly outperformed Treasuries given higher yields and low default rates. The one bright spot in December were commodity prices (+3.7%), which ended the year positive returns (+8.5%).

The following analysis reviews December returns by asset group, sector, and the key factors that drive returns. The aim of the visual summary is to help investors to identify new opportunities and to benchmark your own portfolio returns.

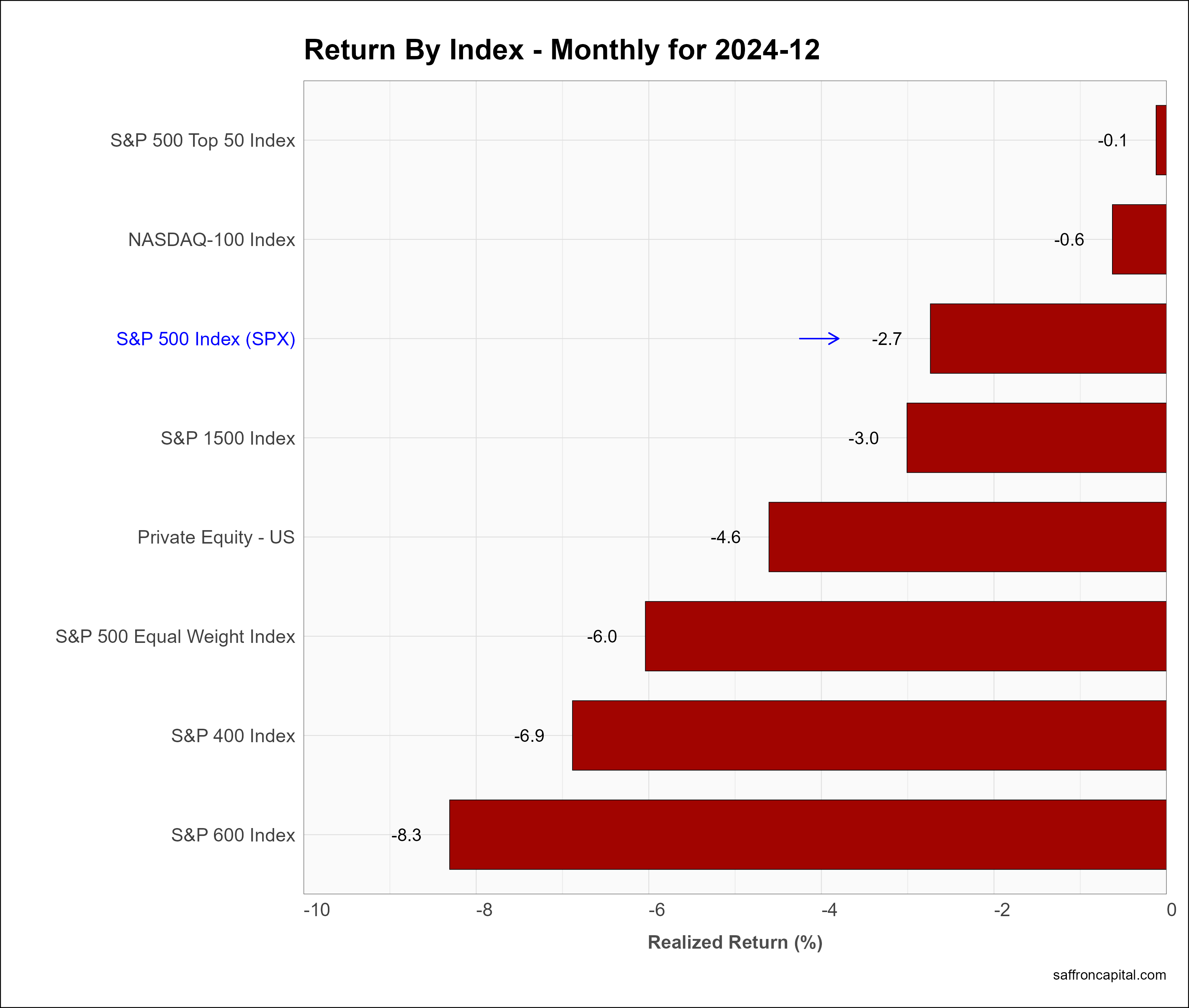

Core US Indices

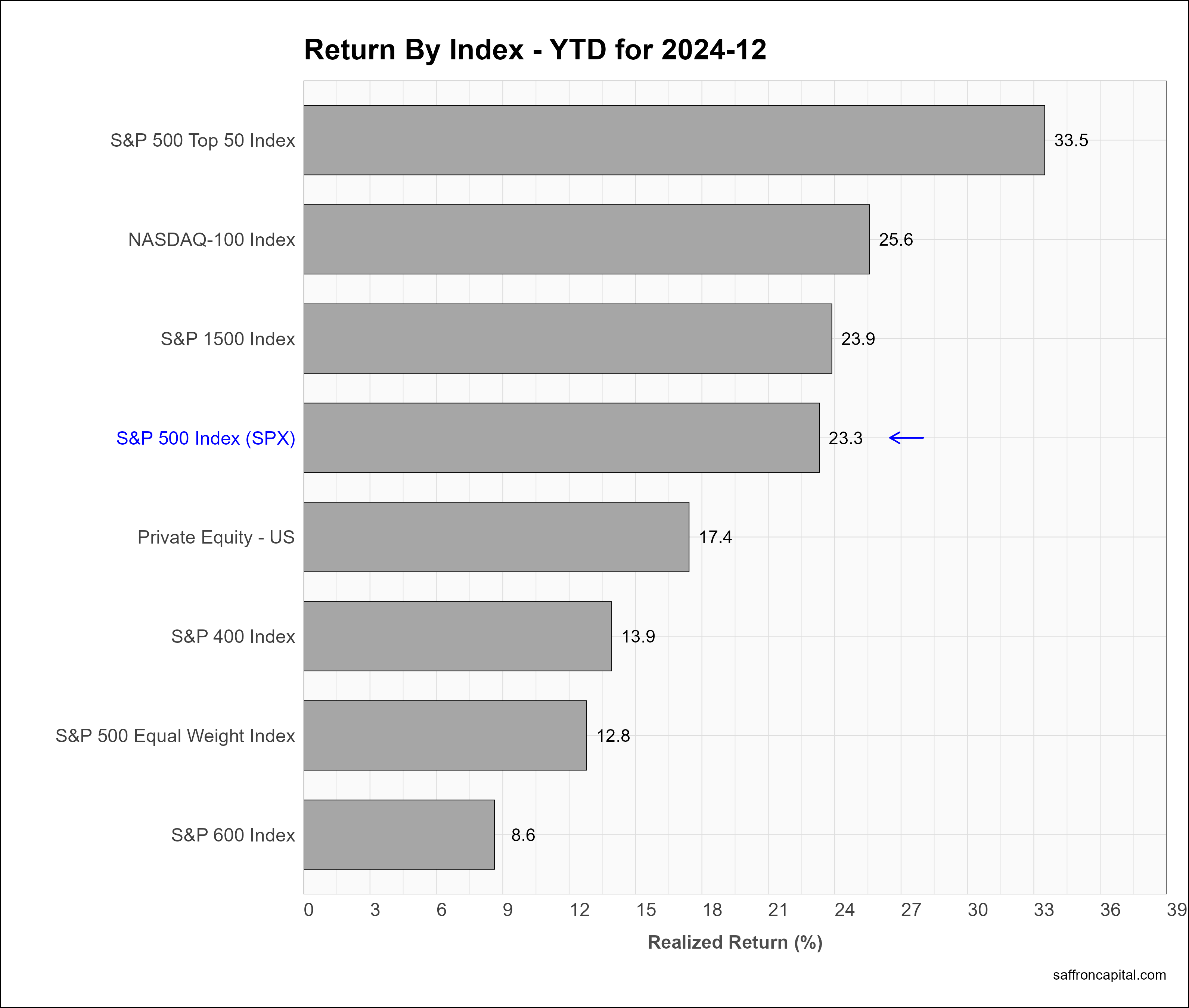

It is fitting that the year started and ended with mega-cap equities in the lead. For example, the top 50 shares in the S&P 500 index (-0.1%) lead returns for the month, driven by strong earnings and the AI-related build-out. In comparison, the broader, large-cap S&P 500 index (-2.7%) failed to keep pace but beat the S&P 500 Equal Weight Index (-6.0%), mid-cap equities (-6.9%), as well as small-caps shares (-8.3%). December returns quickly erased the “Trump bump” given lingering inflation and a revised outlook for Fed interest rate cuts. Regardless, US shares still had an epic year in 2024 and were the upside outlier when compared to other countries. And once again, the top 50 shares in the S&P 500 index (+33.5%) outperformed the broader market as seen in the performance of the equal-weight index (+12.8%).

Click to enlarge

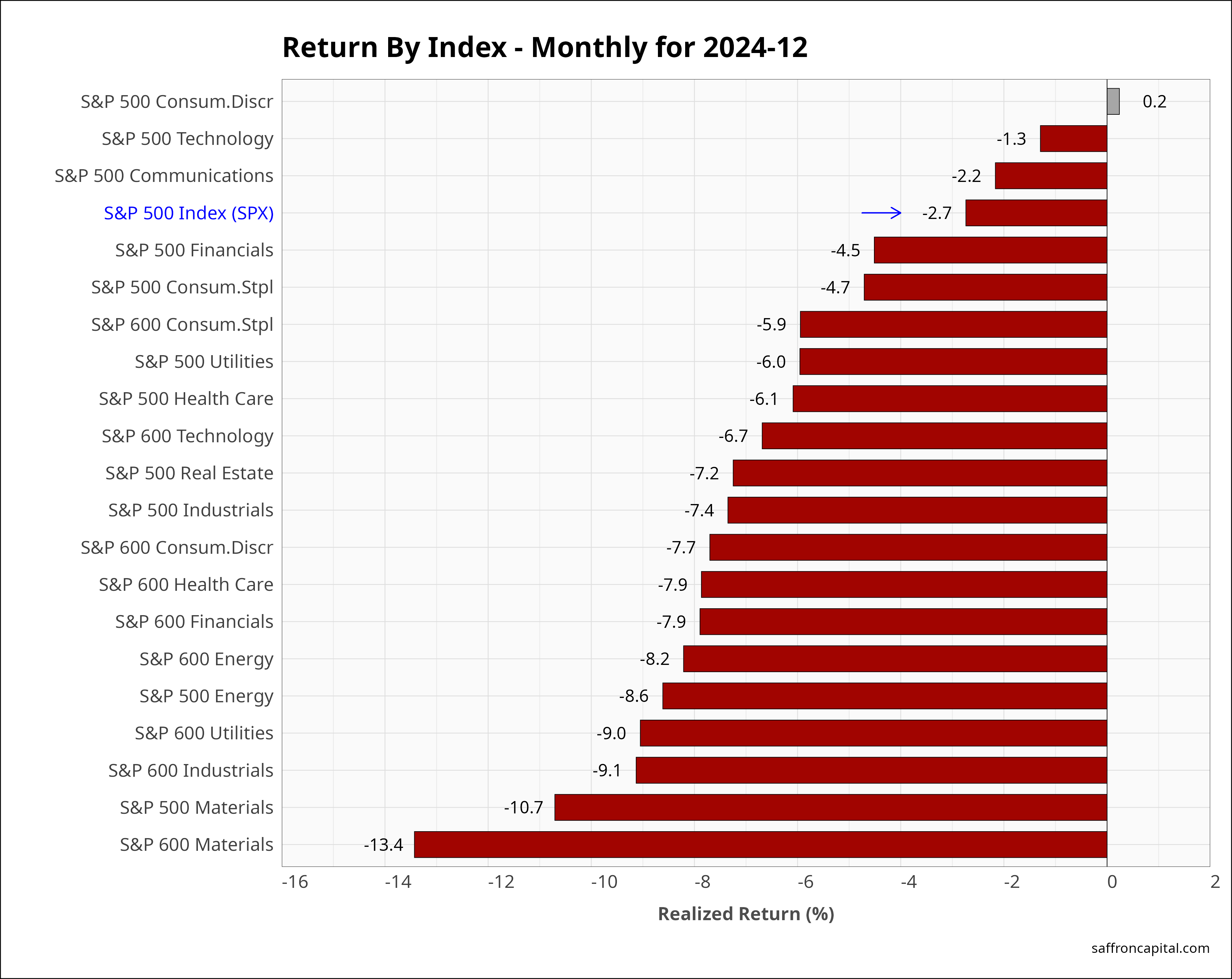

US Sector Indices

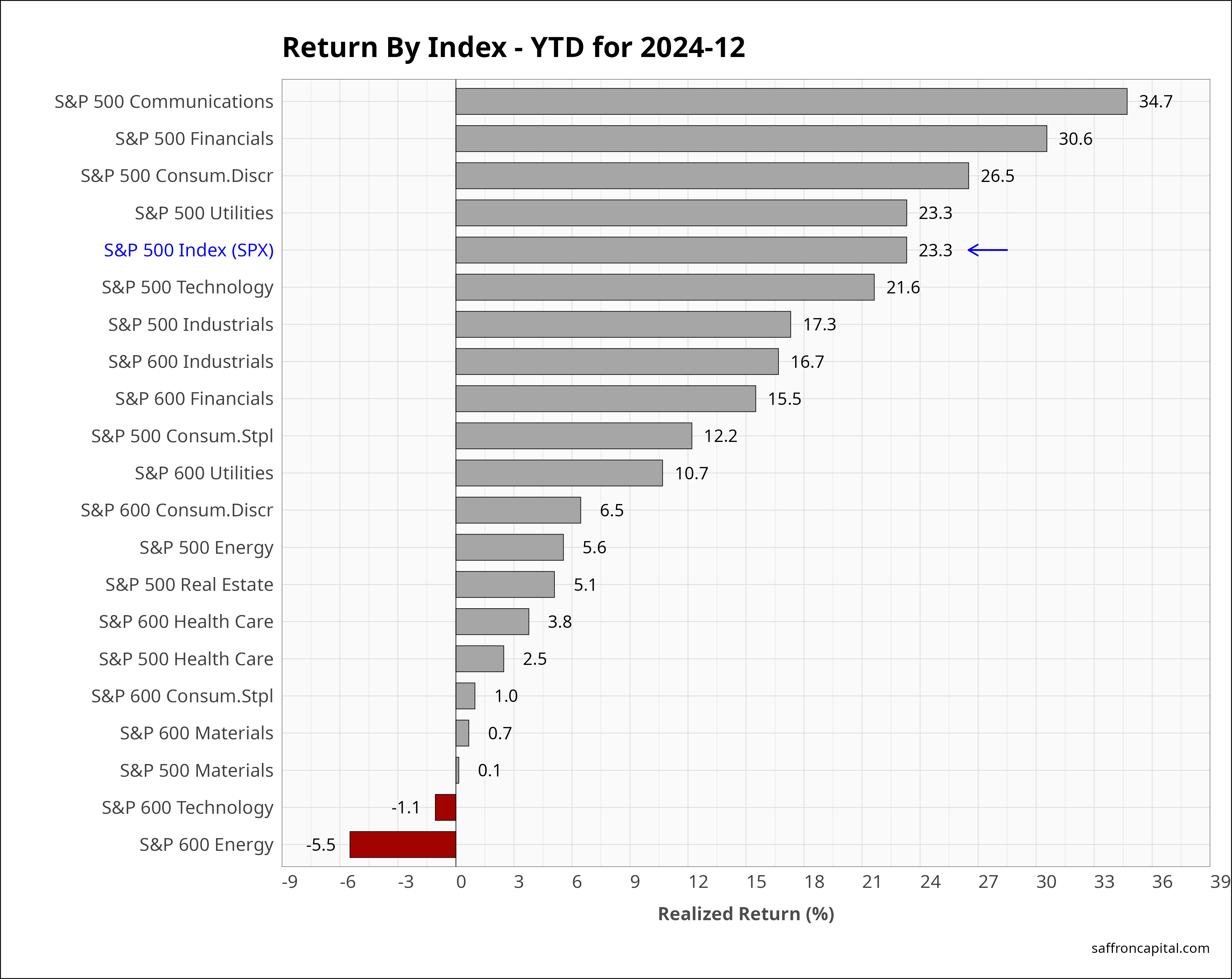

All select sectors were under pressure in December with the exception of the Consumer Discretionary shares (+0.2%). Market breadth was weak with only 3 of 11 sectors beating the broader large-cap index. Technology (-1.3%) and Communication Services (-2.2%) remained among the strongest shares, while Industrials (-10.7%) and Materials (-13.4%) were the weakest. In 2024, all the select sectors posted gains, led by Communication Services (+34.7%), Financial (+30.6%) and Consumer Discretionary (+26.5%) shares.

Click to enlarge

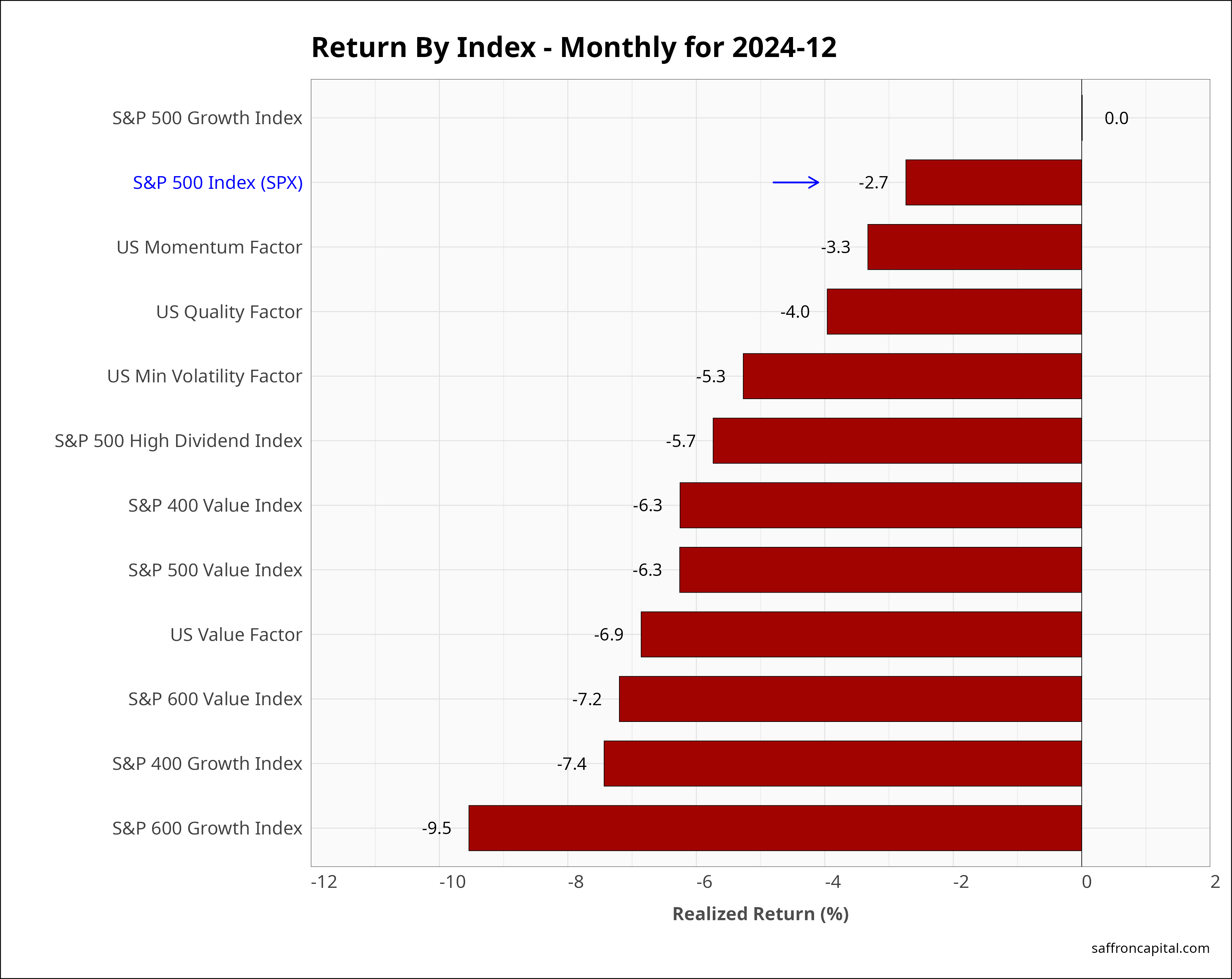

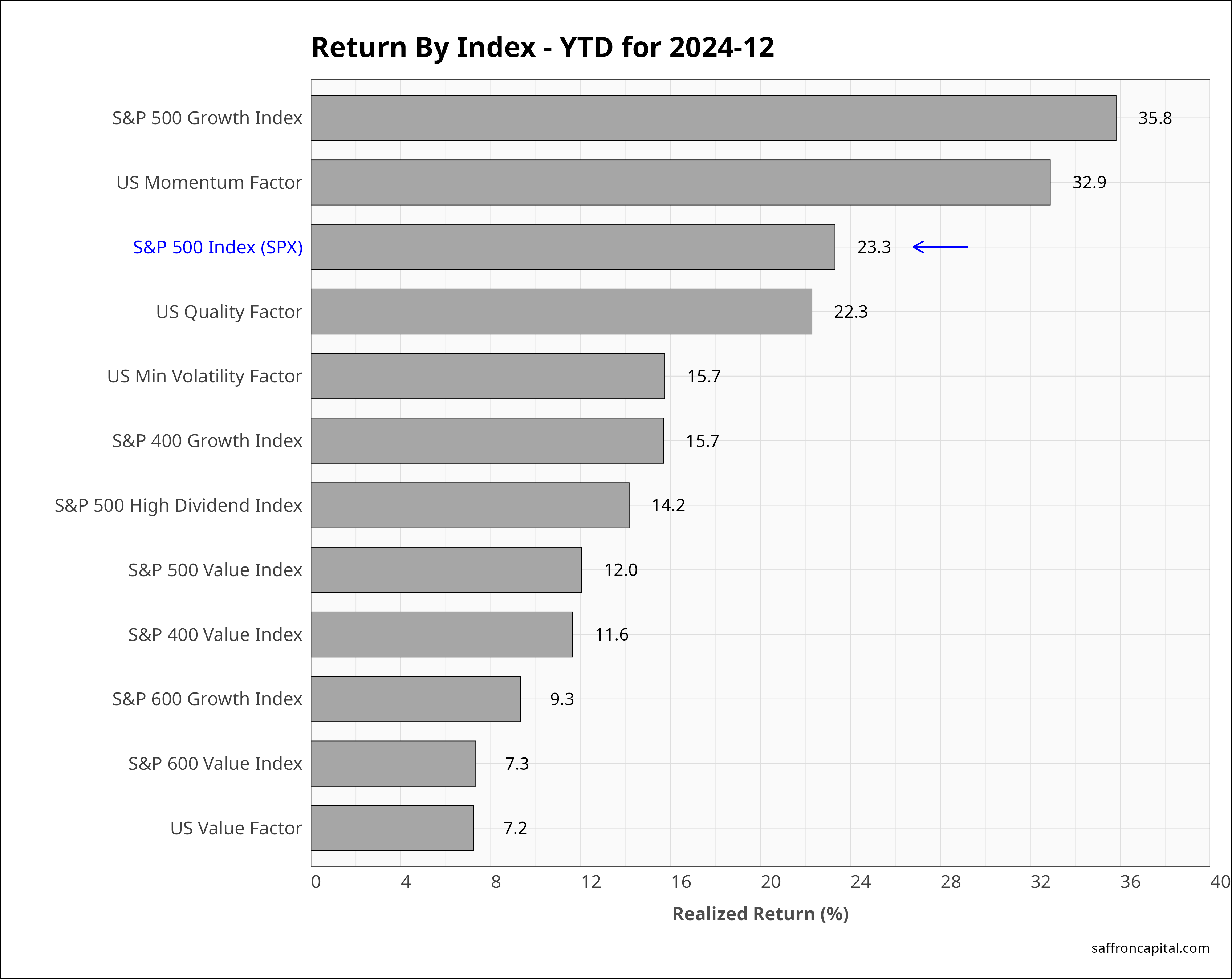

US Factor Indices

Factor portfolios are constructed to emphasize the core drivers behind returns, which include company size, value, profitability, growth, and momentum. Multi-factor portfolios combine two or more factors. During December, US factor portfolios trailed the S&P 500 index. Top performaers included the Momentum (-3.3%), Quality (-4.0%) and the Minimum Volatility (-5.3%) portfolio. Larger losses were seen in the mid-cap growth (-7.4%) and small-cap growth (-8.5%) portfolios. For all of 2024, only the Growth (+35.8%) and Momentum (+32.9%) beat the S&P 500 index. Positive annual returns are seen across all the factor portfolios.

Click to enlarge

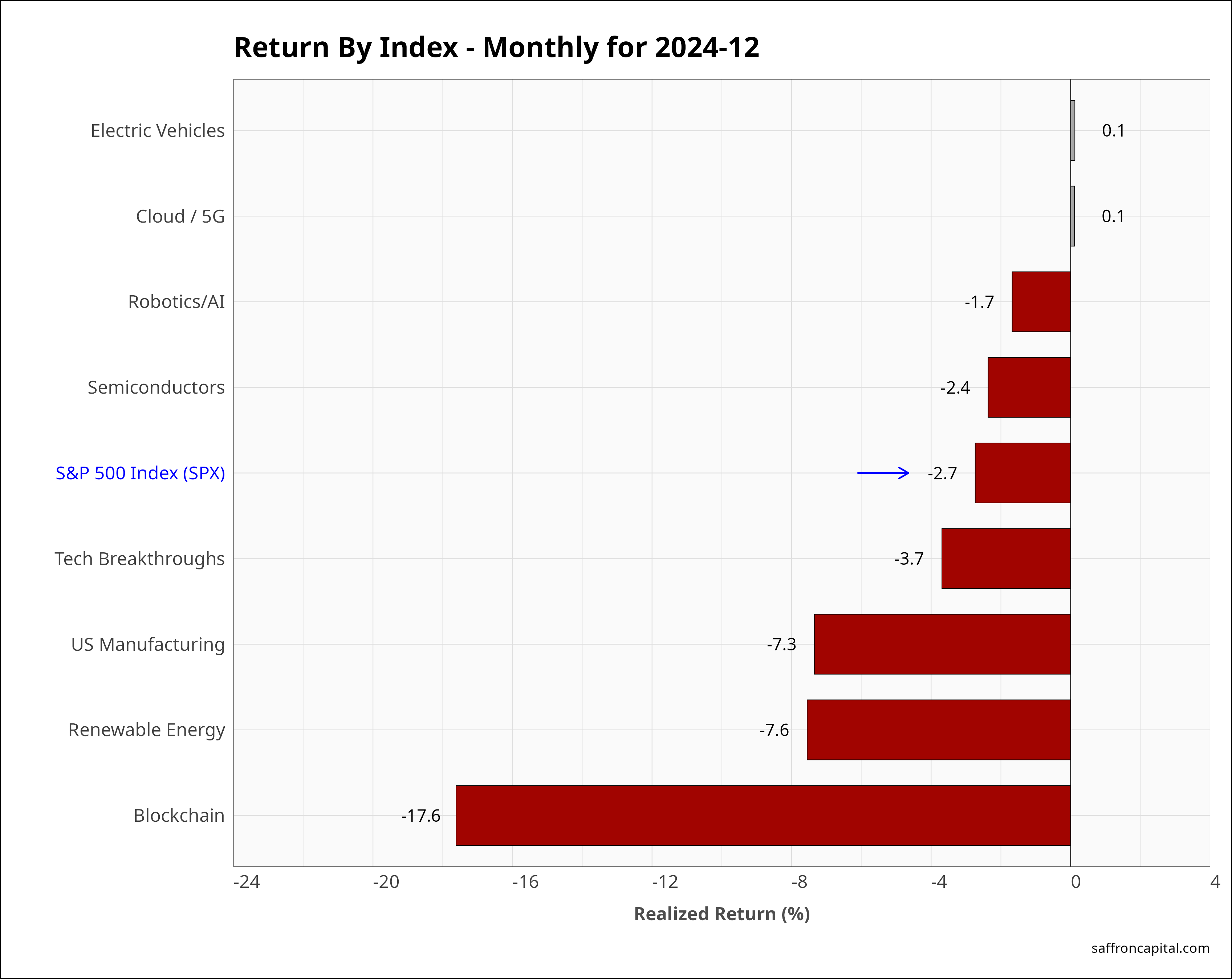

US Megatrend Equities

US megatrend equities are thematic growth portfolios. The aim is to select shares that capture the primary secular trends of the U.S. economy. . December returns were led by shares for Electric Vehicle (+0.1%) and Cloud/5G (+0.1%), while the weakest thematic portfolios included Blockchain (-17.6%) and Renewable energy (-7.6%). Since January, Tech breakthrough shares (+24.4%) outperformed the S&P 500 index. The weakest thematic portfolios in 2024 include Electric Vehicles (-16.0%) and Renewable Energy (-25.7%).

Click to enlarge

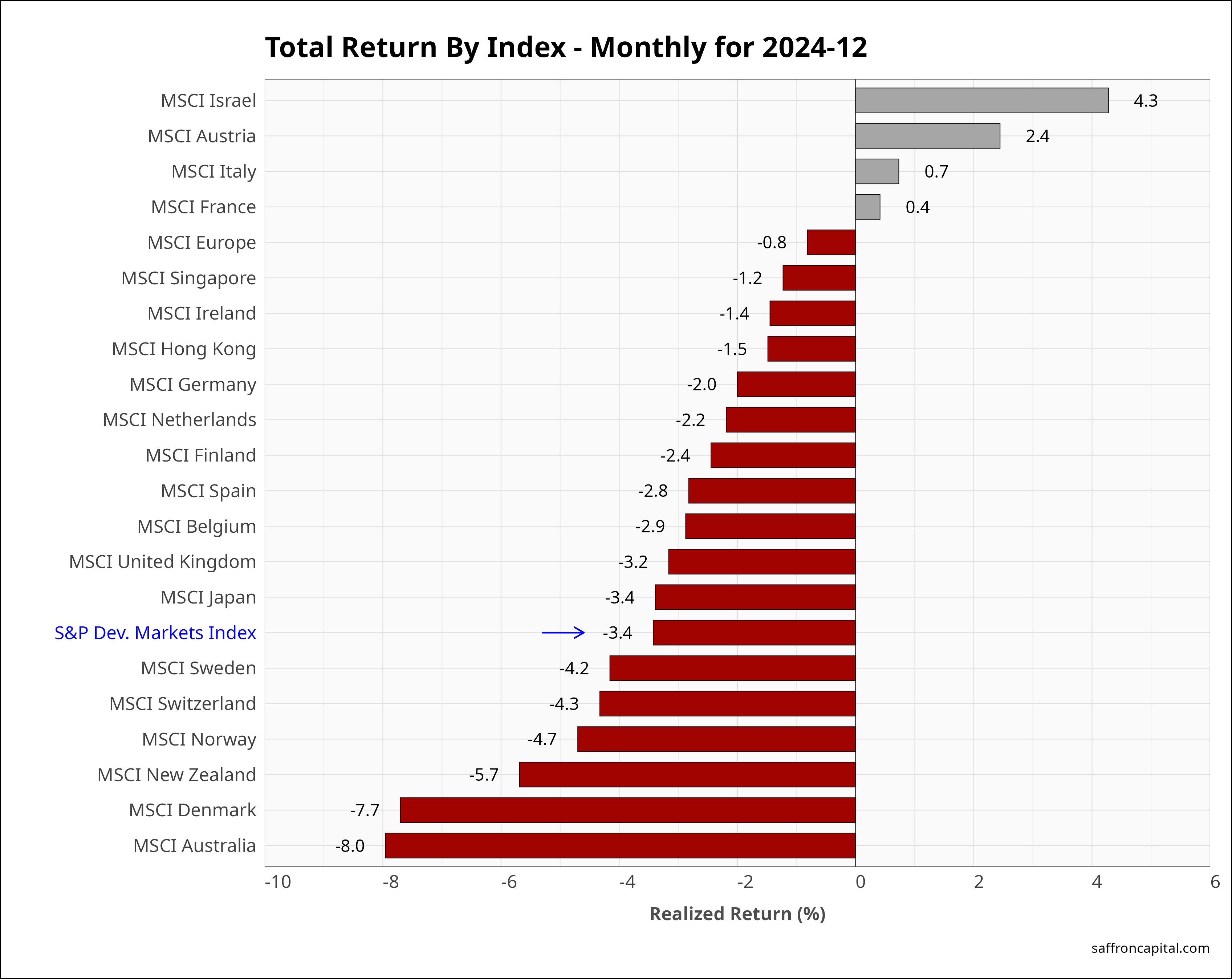

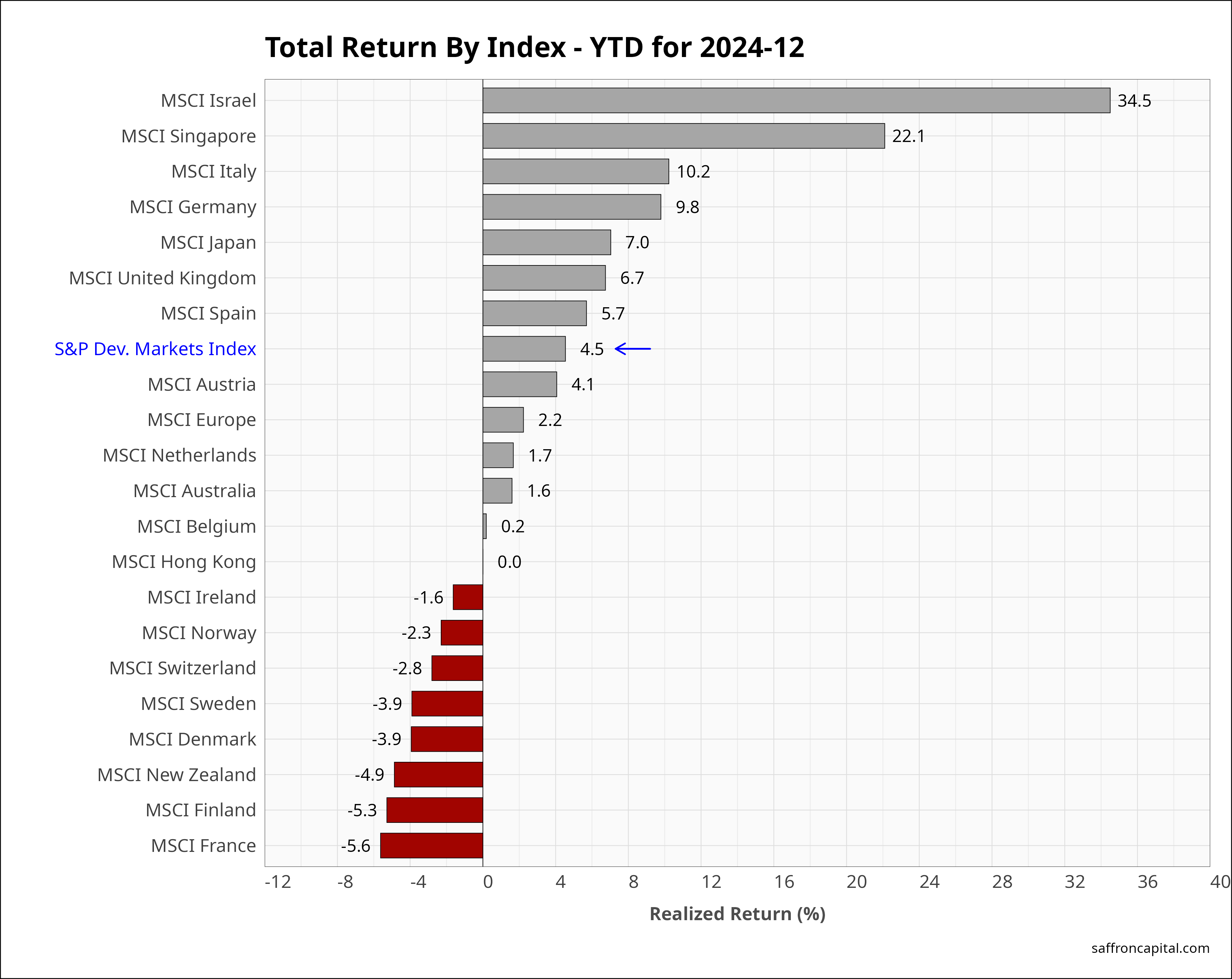

Developed Market Equities

International developed markets (-3.4%) were lackluster in December. The MSCI Europe index (-0.8%) outperformed the US, lead by Austria (+2.4%), Italy (+0.7%) and France (+0.4%). Stocks in Japan (-3.4%) were also weak in December, similar to most Asian shares. Since January, the strongest performers include Israel (+34.5%), Singapore (+22.1%) and Itay (+10.2%). The S&P Developed markets index (+4.5%) was positive for the year but trailed US shares significantly.

Click to enlarge

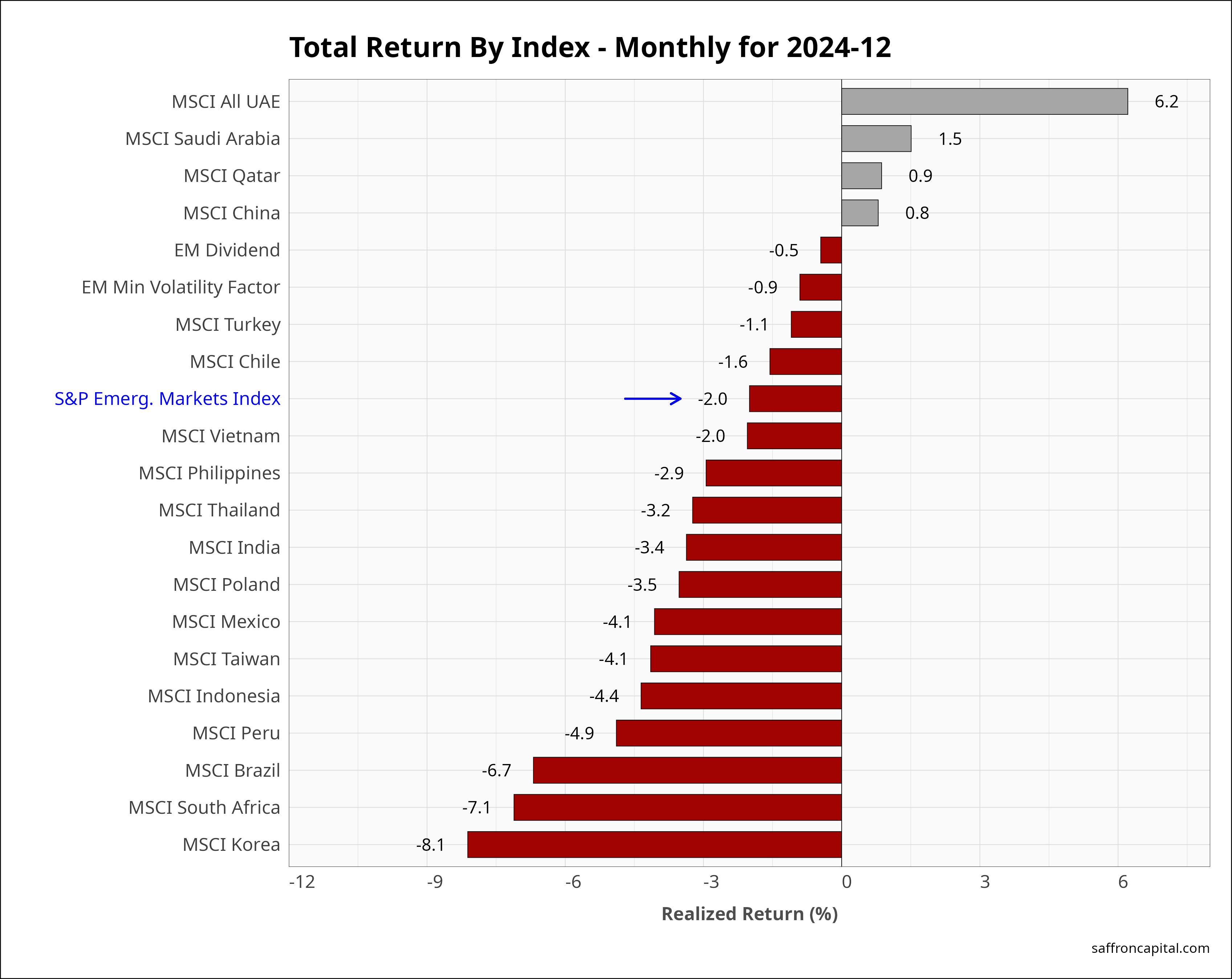

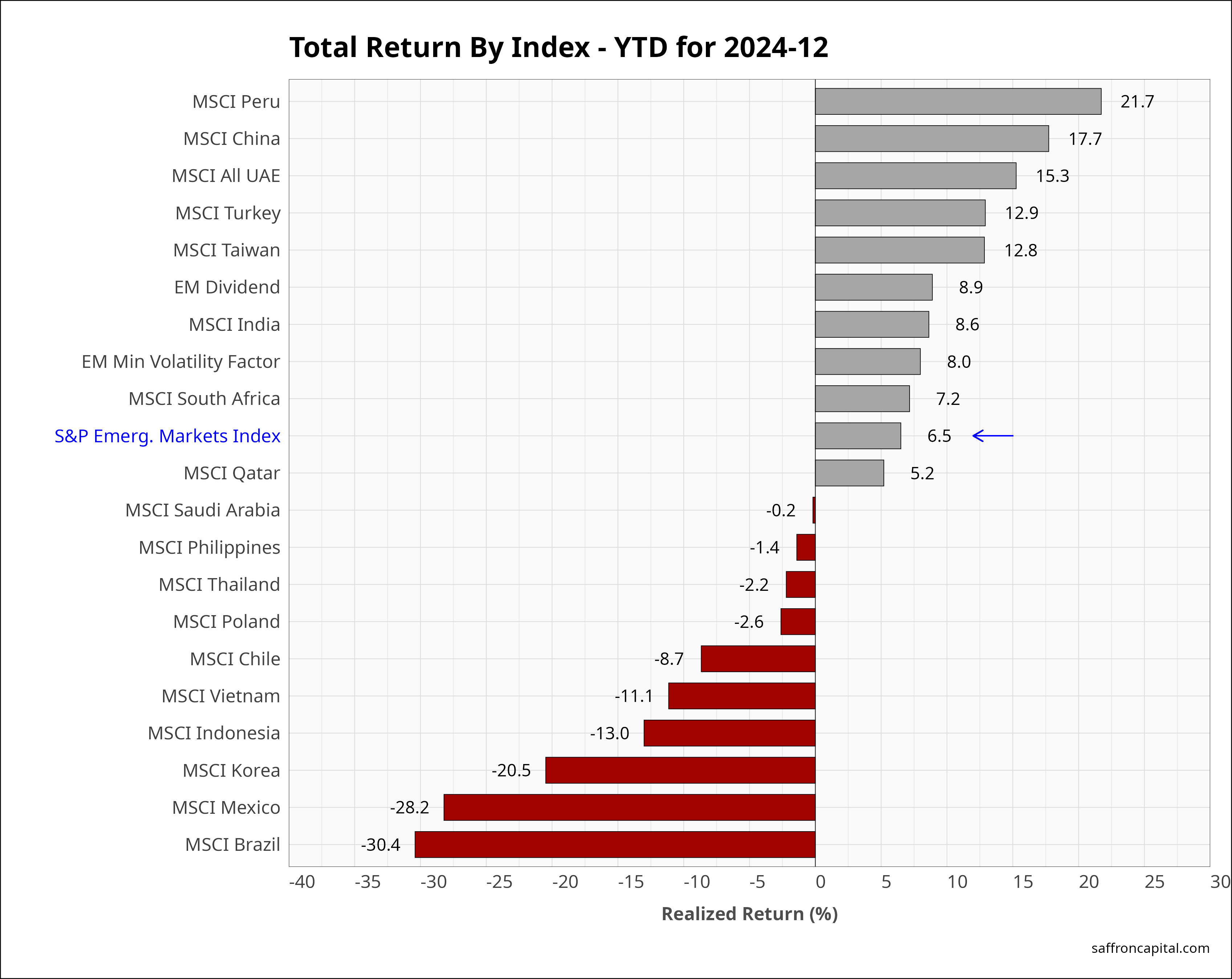

Emerging Market Equities

The S&P Emerging Markets Index (-2.0%) was also pulled down in December but managed to outperform developed markets, including the US. The only countries with positive returns were the UAE (+6.2%), Saidi Arabia (+1.5%) and Qatar (0.9%), all of which benefited from higher energy prices and large infrastructure spending. China (+0.8%) was positive while shares across Asia were broadly negative, as seen by India (-3.4%), Taiwan (-4.1%), and Korea (-8.1%). For 2024, the top emerging markets include Peru (+21.7%), China (+17.7%), and the UAE (+15.3%). The weakest returns were seen in Korea (-20.5%), Mexico (-28.2%), and Brazil (-30.4%).

Click to enlarge

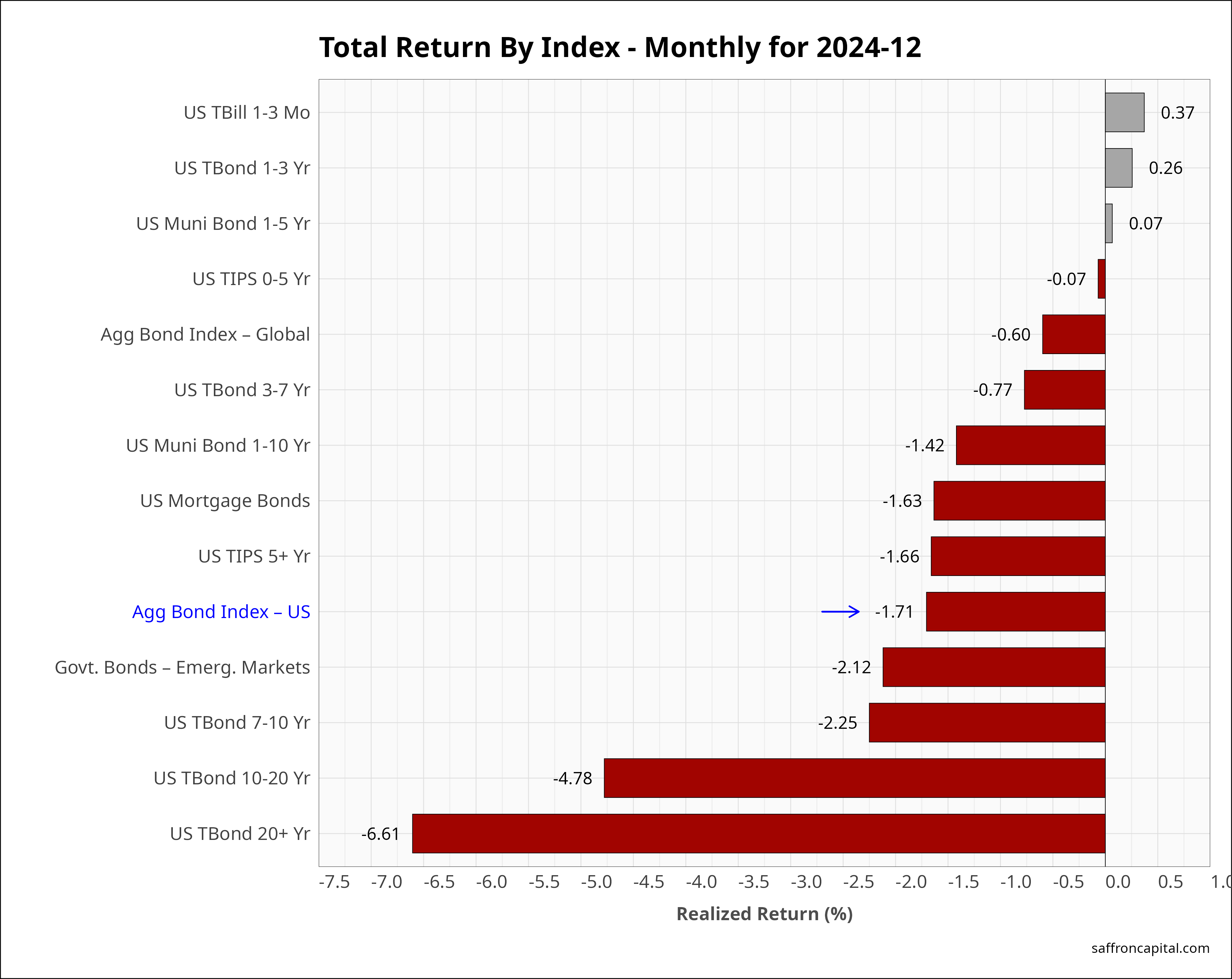

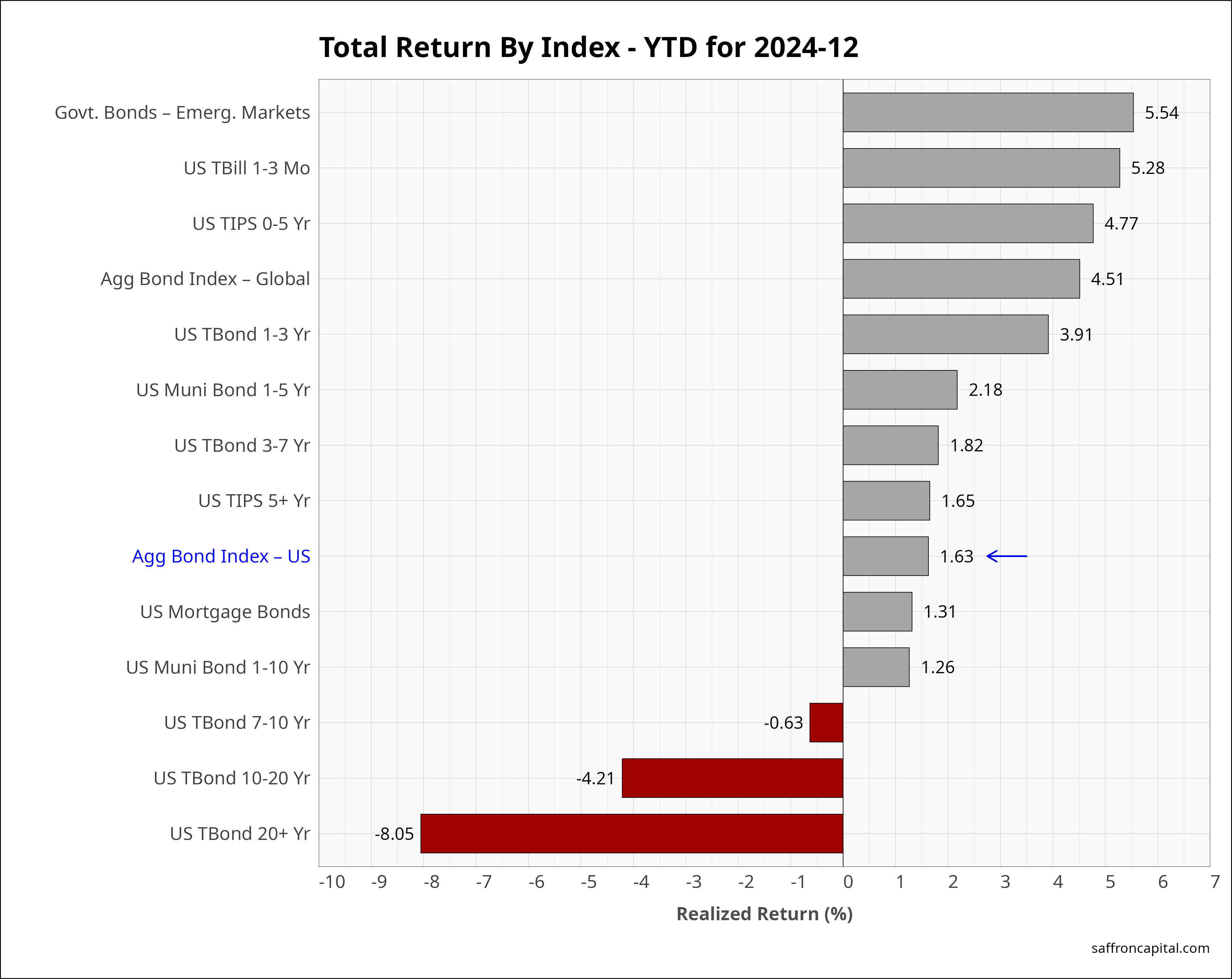

Government Bonds

The US fixed income markets turned negative again in December. The FOMC voted at their December meeting to reduce the number of rate cuts in 2025, while the 10-year yield jumped from 4.15% to 4.62%. As a result, the Aggregate Bond Index (+-1.71%) traded down, while long duration Treasury bonds (-4.78%) fell hard. Year-to-date, the US Aggregate Bond index (+1.63%) generated a modest total return. Emerging market soverign bonds (+5.54%) were the strongest performing of the year, followed by short-term US T-Bills (+5.28%).

Click to enlarge

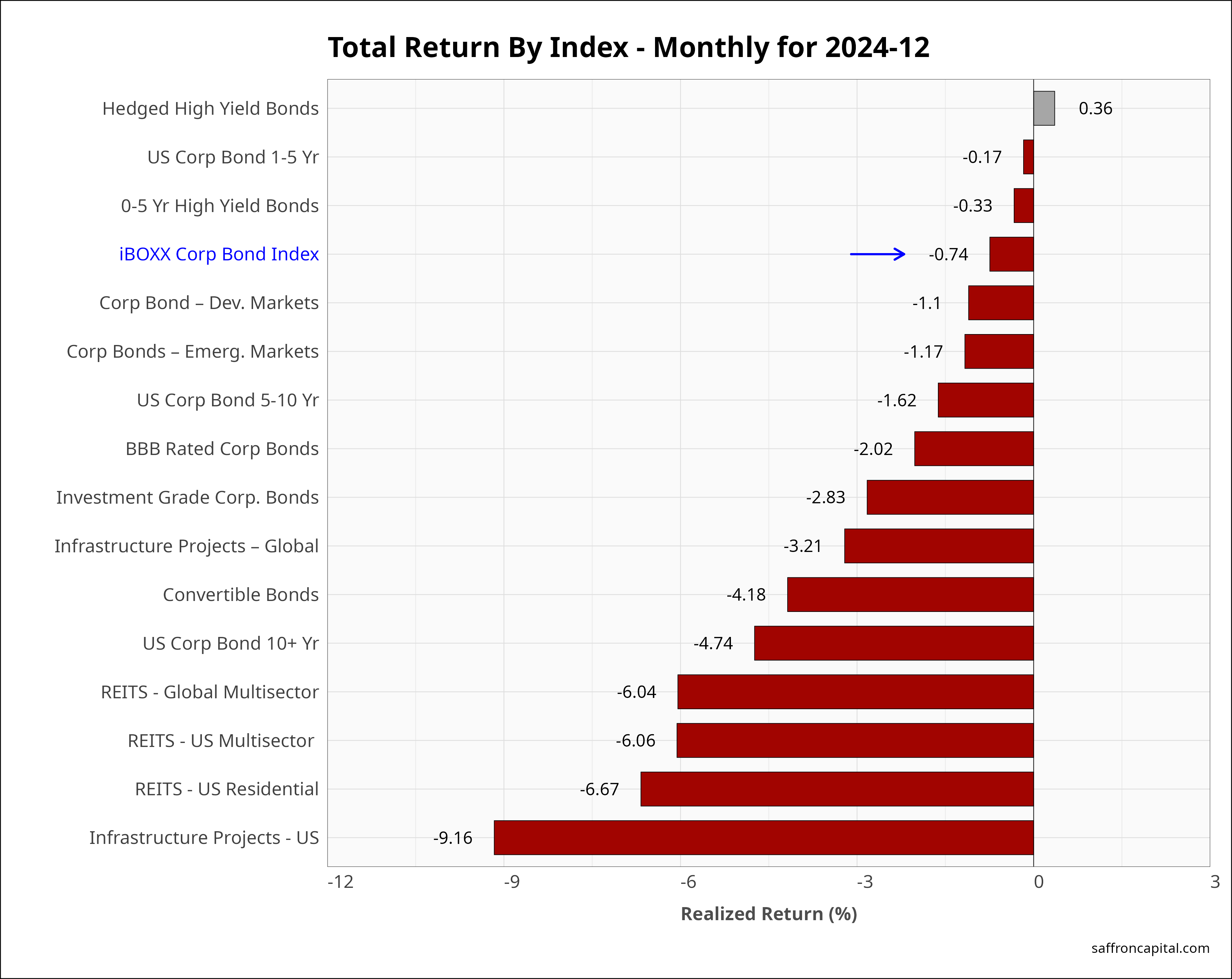

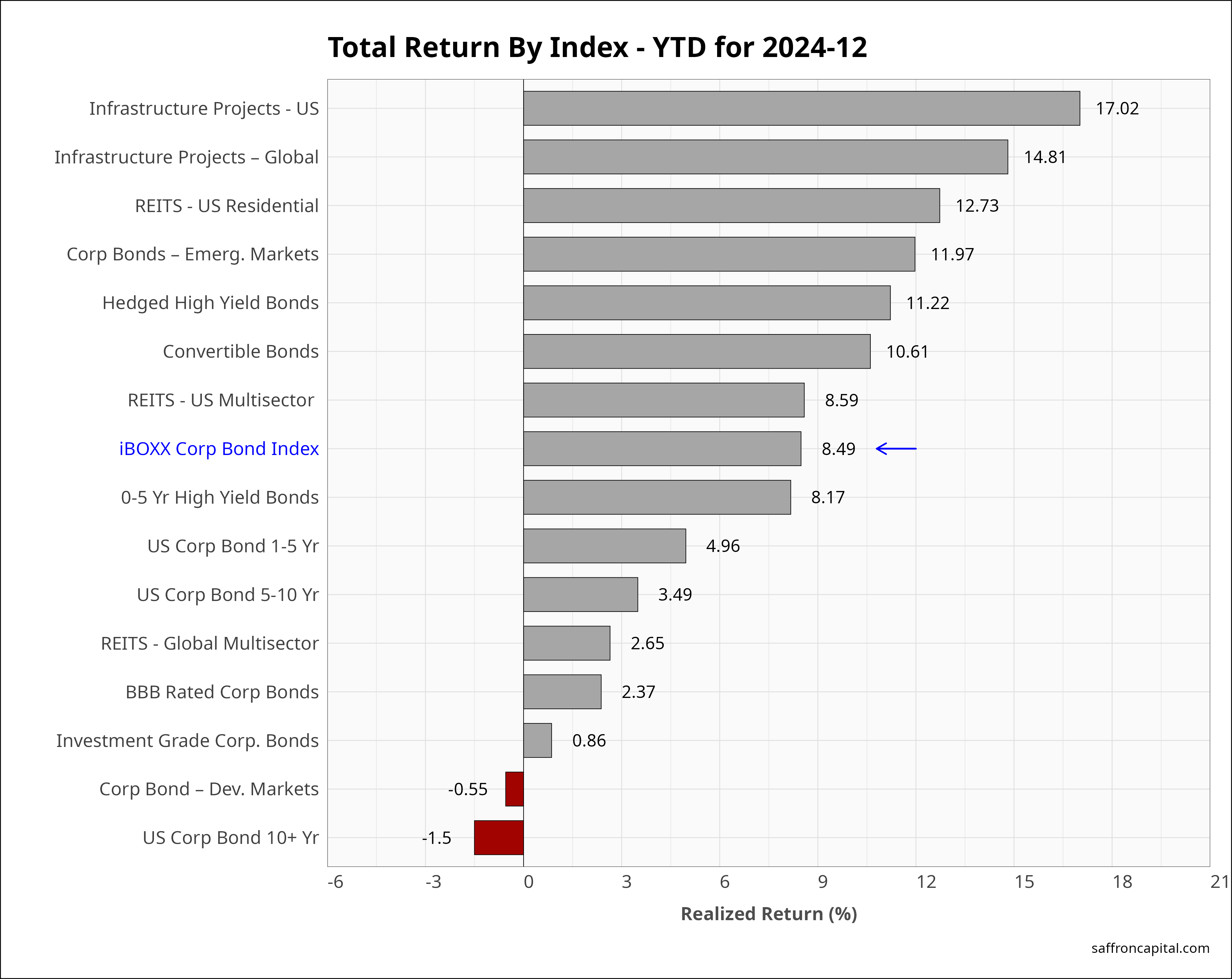

Corporate & Infrastructure Bonds

The iBoxx Corporate Bond Index (-0.74%) had modest losses in December, masking lots of red ink across the sector. For example, investment grade bonds (-2.83%) came under pressure, while REITs (-6.06%) fell further. The greatest losses were seen in US Infrastructure Project bonds (-9.16%), which had major losses after a year of strong gains. For the year, the top performer was US Infrastructure Project bonds (+17.82%), followed by Worl Infrastructure Project bonds (+14.81%). US Corporate boinds with maturities of 10-years fell (-1.5%) in 2024.

Click to enlarge

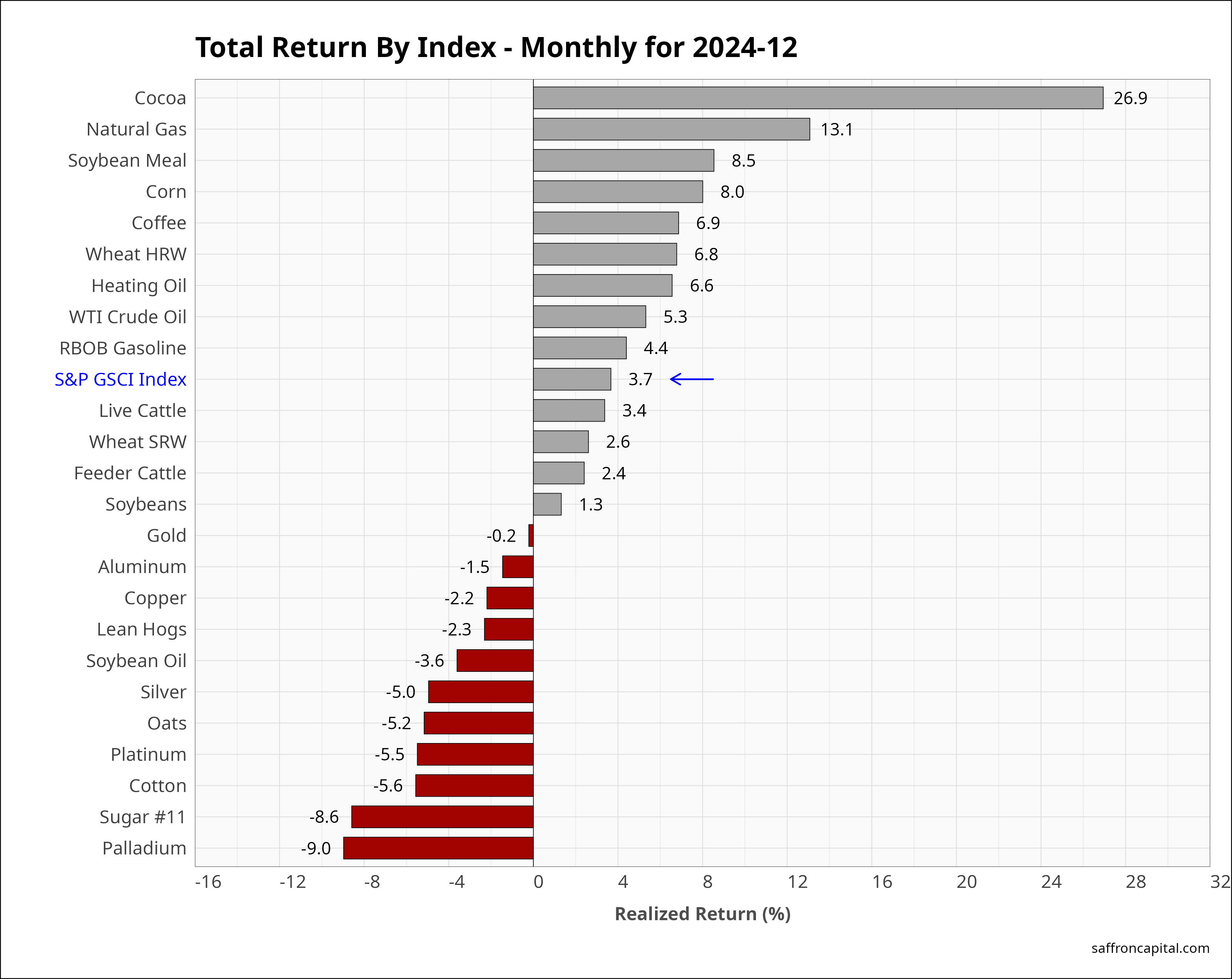

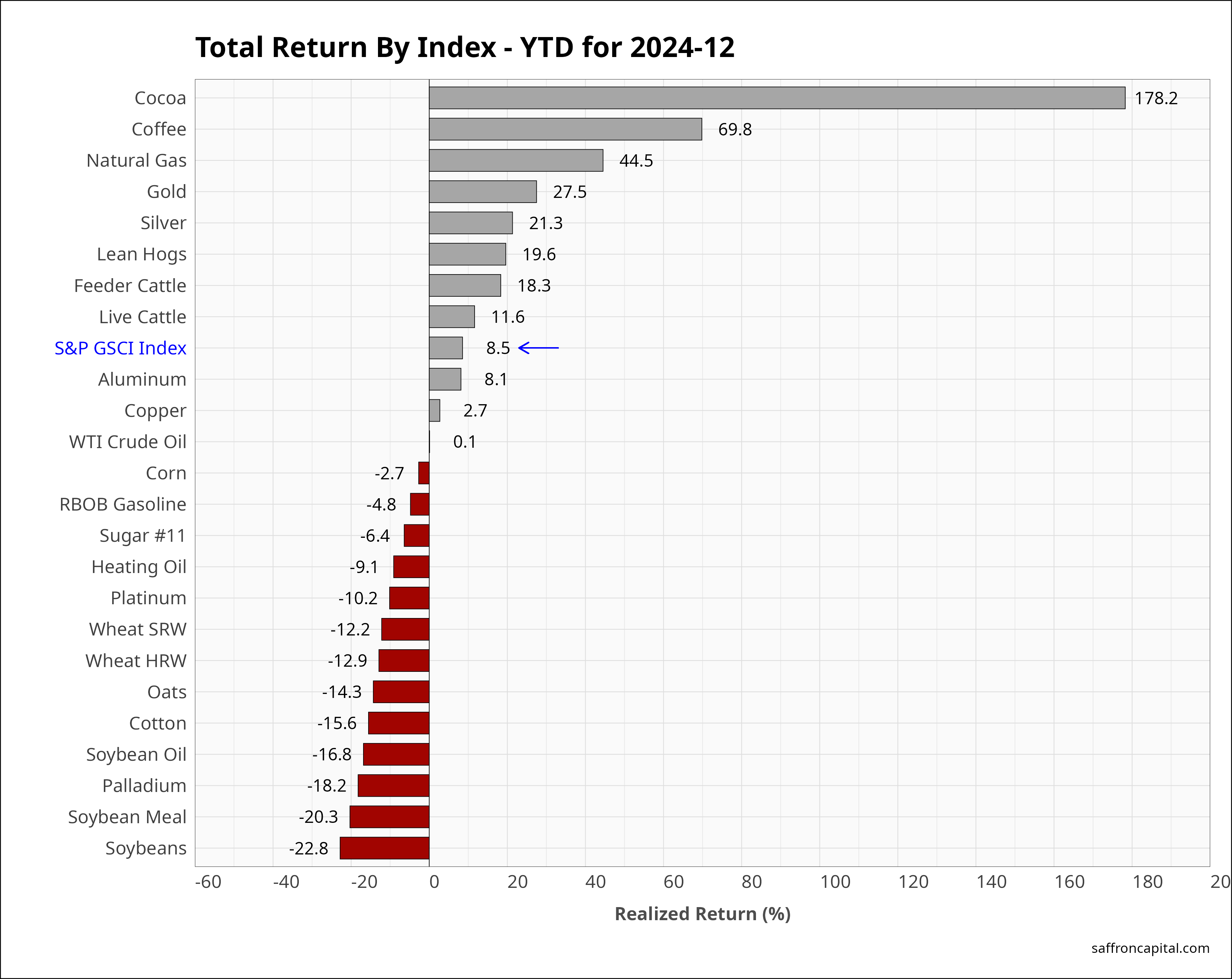

Commodities

Commodities, as measured by S&P GS Commodity Index (+3.7%) had the best gains among December returns. Cocoa (+26.9%) continued to inflate, while natural gas (+13.1%) benefited for seasonal weather. WTI crude oil (+5.3%) reversed recent losses, while gold (-0.2%) was unchanged. For the year, the biggest positive change was in Cocoa (+178.2%), coffee (+69.8%) and natural gas (+44.5%). In 2024, the GS commodity index will end up +8.5%.

Click to enlarge

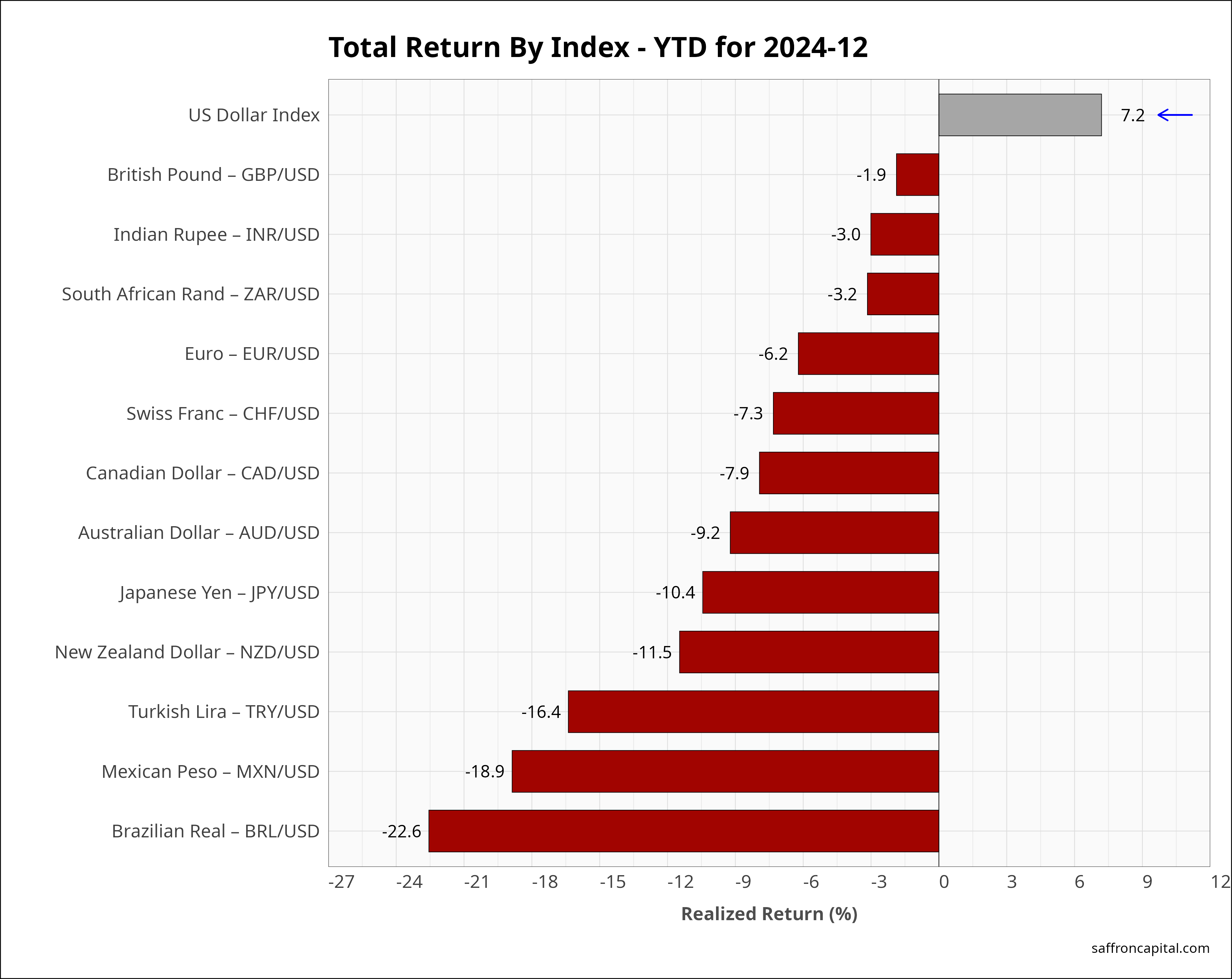

Currencies

The U.S. Dollar index (+1.8%) was again up in December. The Japanese Yen (-5.0%) led currency losses, while the Euro (-1.3%) was also down. Year-to-date returns for the U.S. Dollar index (+7.2%) confirms short-term rate cuts are being ignored and, instead, are linked to long-term yield curve normalization and the rising premium of long-term yields.

Click to enlarge

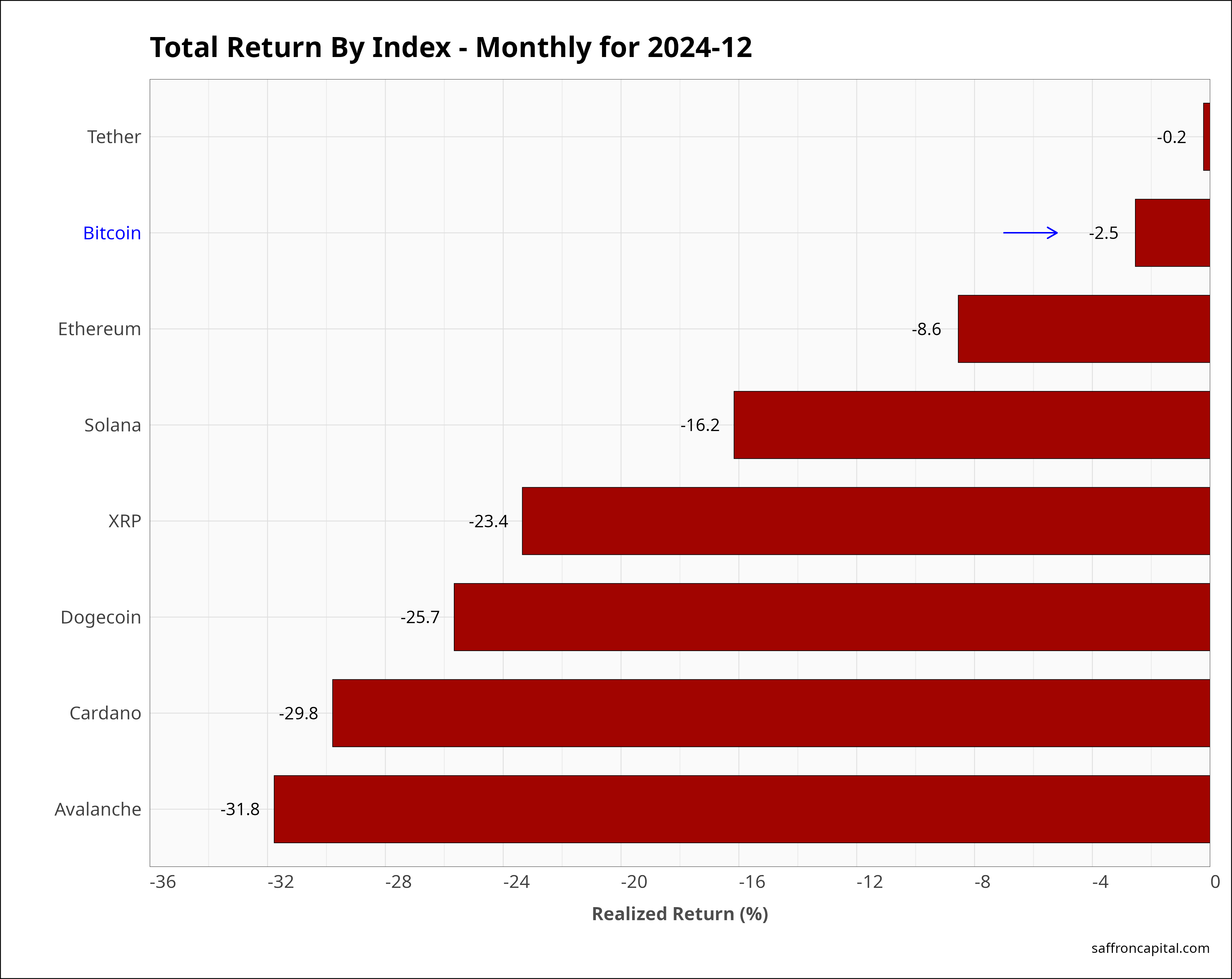

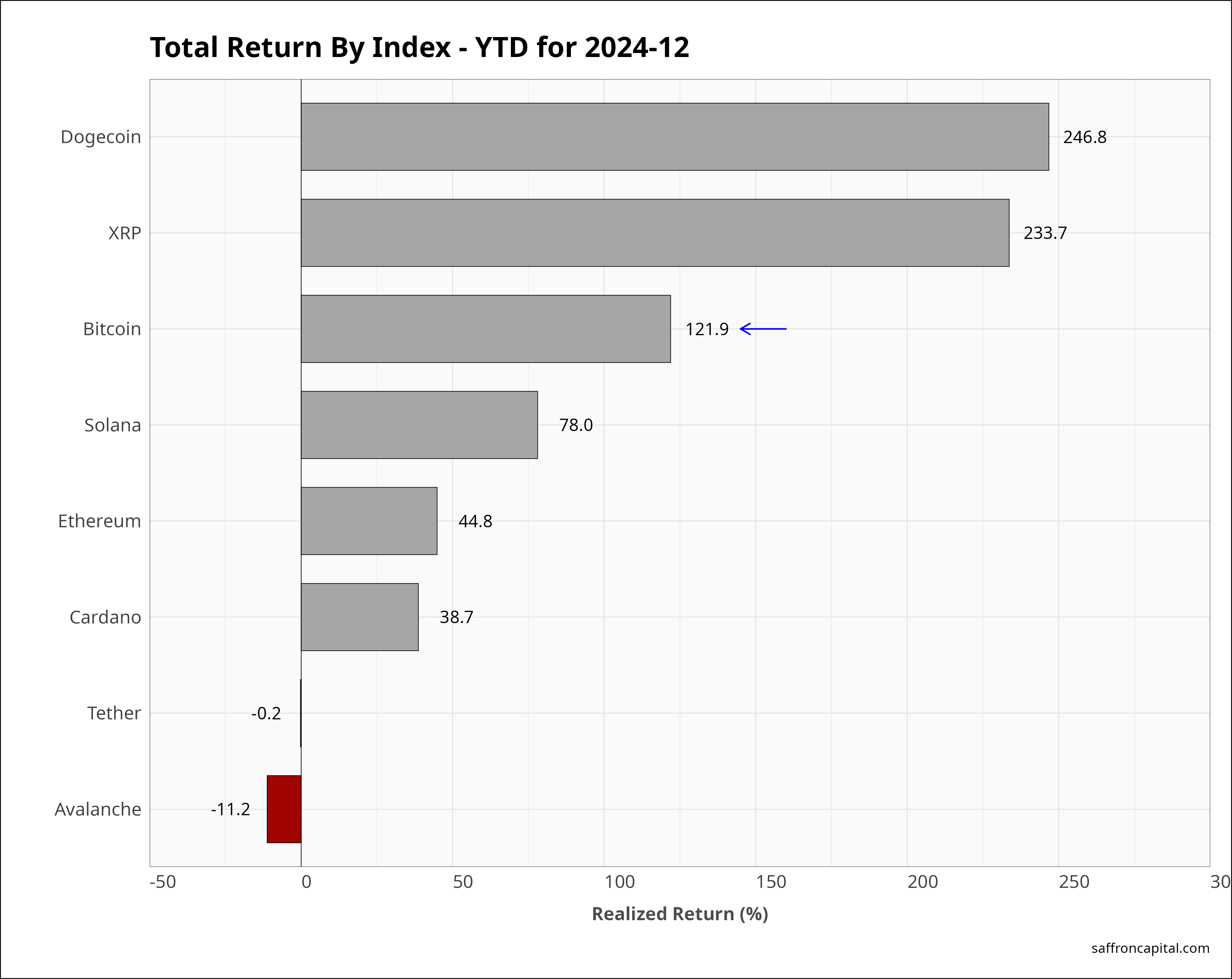

Cryptocurrencies

Cryptocurrencies had a volatile December with Bitcoin (-2.5%) among the strongest of the cryptocurrencies. For example, XRP (-23.4%) was more typical of the price action seen, while Avalanche (-31.8%) was the hardest hit in December. in 2024, Bitcoin (+121.9%) had epic returns, but still trailed XRP (+233.7%) and Dogecoin (+246.8%).

Click to enlarge

Have questions or concerns about the performance of your portfolio? Could you benefit from a custom portfolio formulation that better reflects your goals and risk appetite? Whatever your needs are, we are here to listen and to help. You can contact us here.

Saffron Capital LLC is a registered investment advisor that is employee-owned and Minnesota-based. The company uses Interactive Brokers as its bank custodian and clearing merchant.

{kind=link}

{kind=link}

{kind=link}