February returns for the S&P 500 index (-1.4%) saw two all-time highs followed by sell-off at month-end tied. The market turned on new fiscal tightening, pending tariffs, consumer confidence declines, and forward projections of lower GDP and earnings growth. A shift in concern from resurgent inflation to slow growth benefited the Aggregate Bond Index (+2.2%), European shares (+3.6%), multi-sector REITS (+3.6%), and high dividend shares (+5.3%). The S&P 600 Small Cap index (-5.6%) proved to be most vulnerable to economic slowing.

The following analysis reviews January returns by asset group, sector, and the key factors that drive returns. The aim of the visual summary is to help investors to identify new opportunities and to benchmark returns for your portfolio.

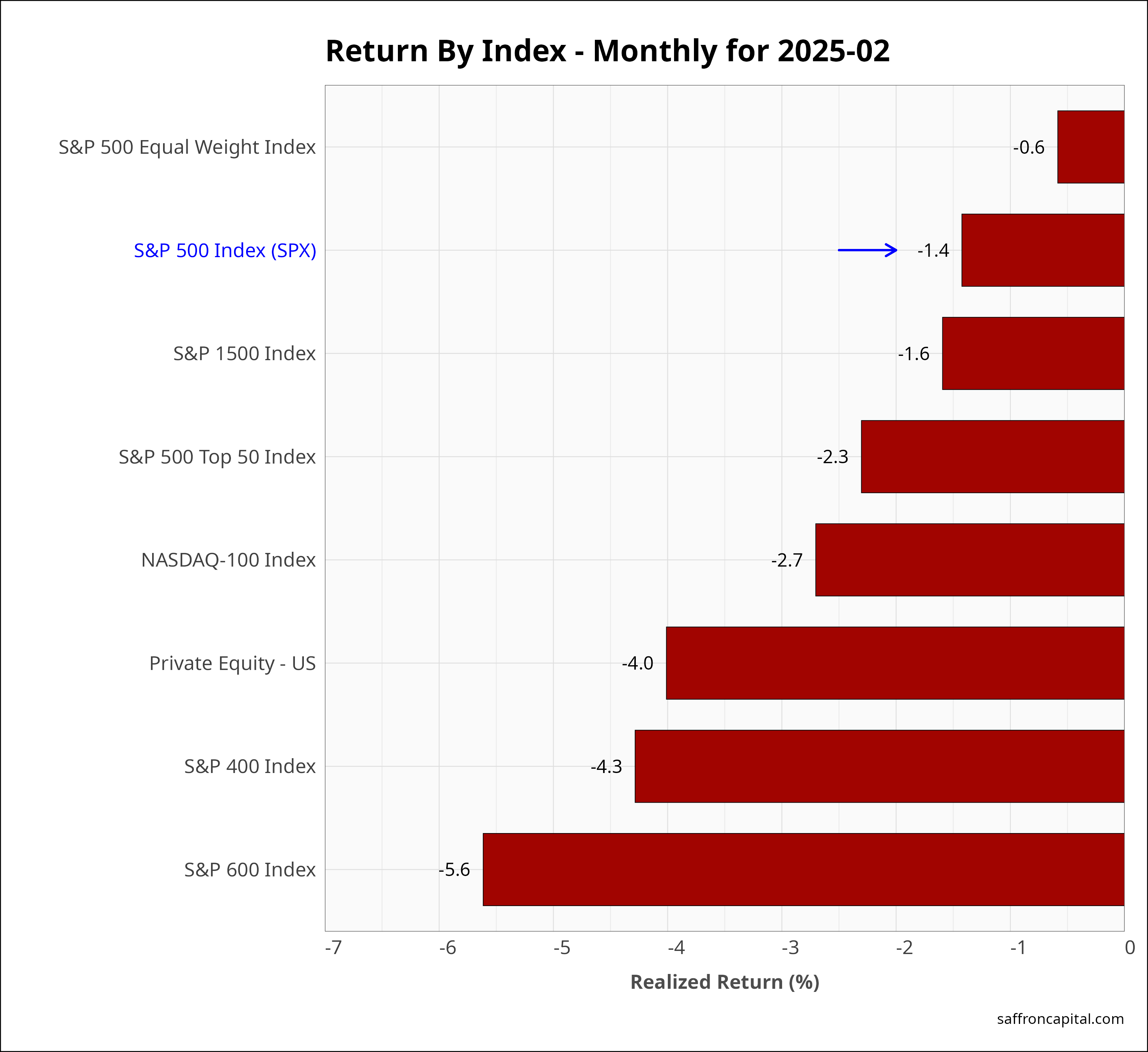

Core US Indices

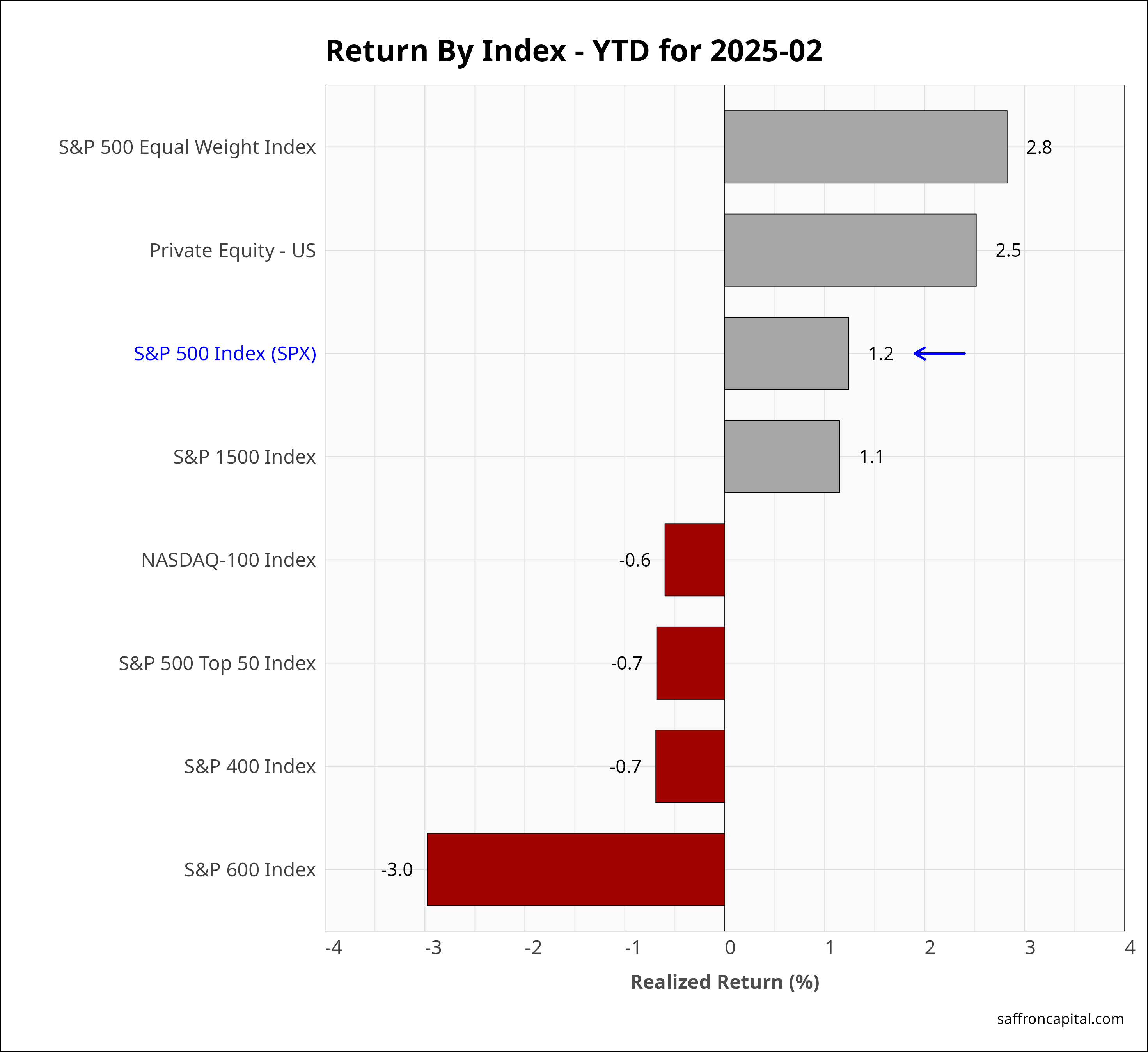

The all-time highs in February were well justified. 4Q.2024 annual earnings growth for the S&P 500 index was confirmed to be +17.8% with all members reporting, the highest level in 3 years. However, market confidence eroded given increased policy uncertainty, fiscal restraint, and steady declines in forecast earnings for the S&P 500 in 2025. Large-cap shares where the biggest detractors from Performance in February. The S&P 500 Equal Weight Index (-0.6%) outperformed, which is typical when mega-caps weaken. The Equal-Weight S&P 500 index has year-to-date gains of +2.8% versus the cap-weighted index at +1.2%.

Click to enlarge

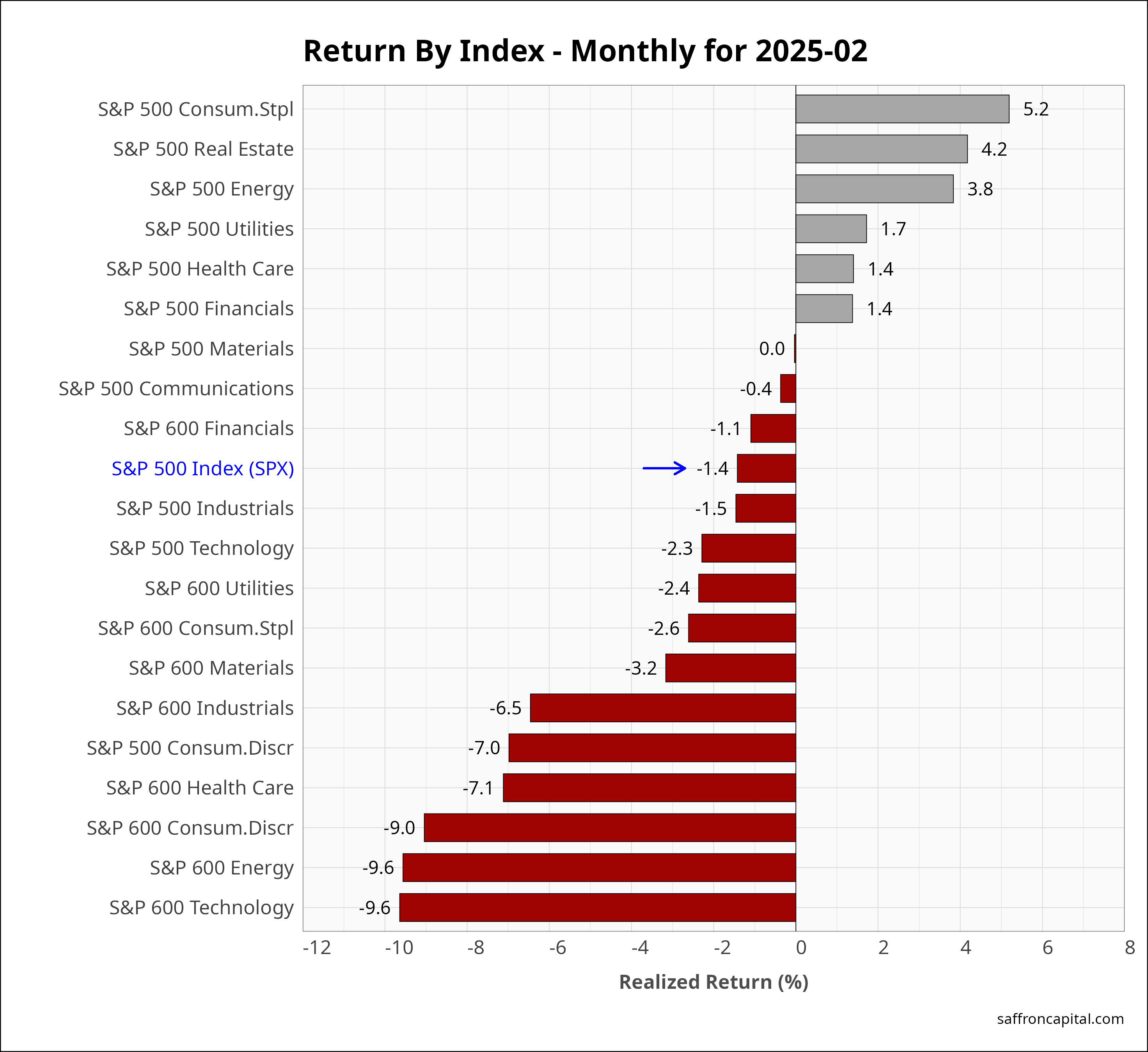

US Sector Indices

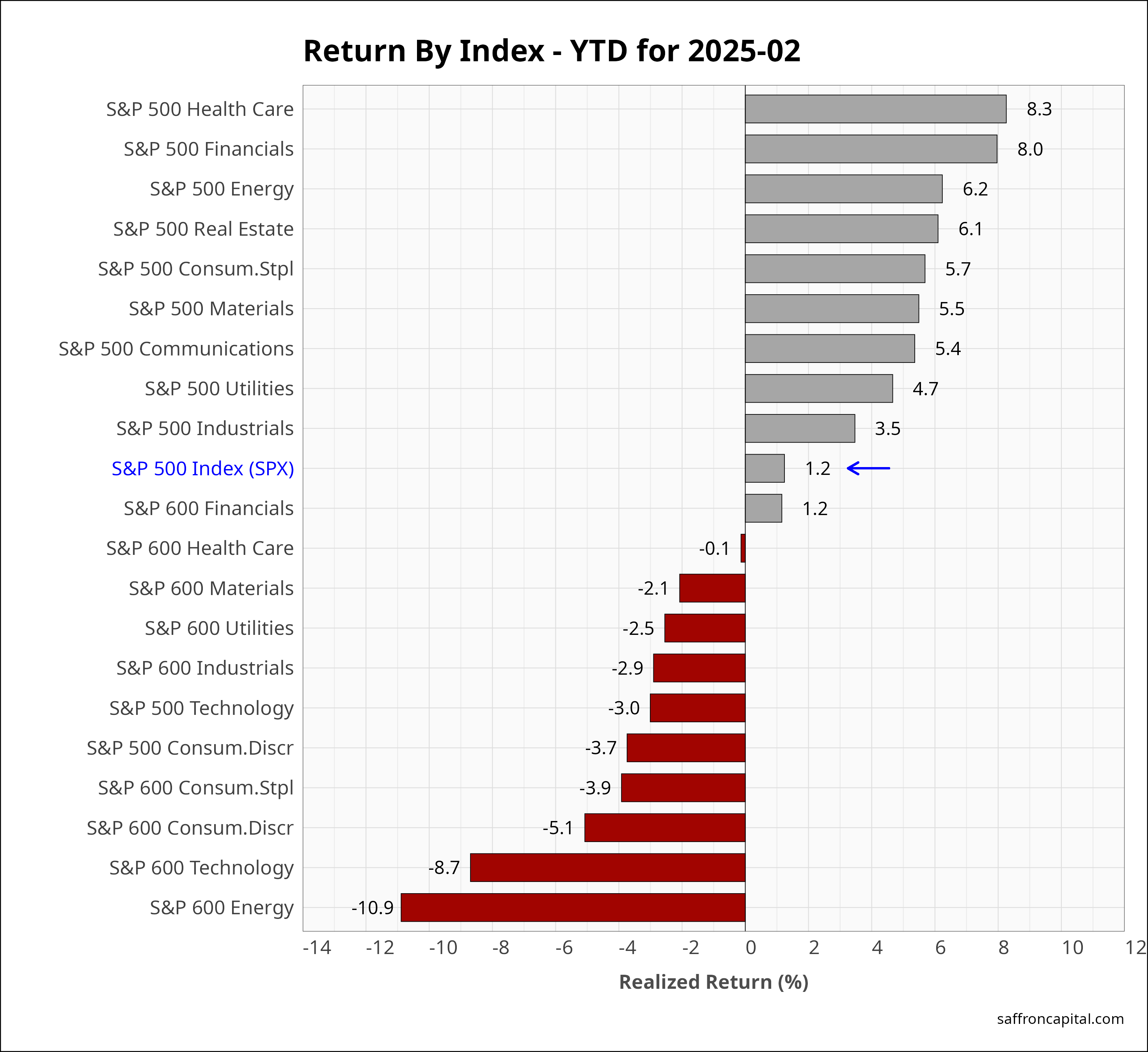

February returns by sector were mixed. Defensive sectors outperformed, lead by Consumer Staples (+5.2%), Real Estate (+4.2%) and Energy (+3.8%). Industrials (-1.5%), Technology (-2.3%), and Consumer Discretionary (-7.0%) shares lagged. Defensive sectors also lead year-to-date performance, led by Health Care (+8.3%), Financials (+8.0%), Energy (+6.2%) and Real Estate (+6.1%). Technology (-3.0%) and Consumer Discretionary (-3.7%) have struggled the most since December.

Click to enlarge

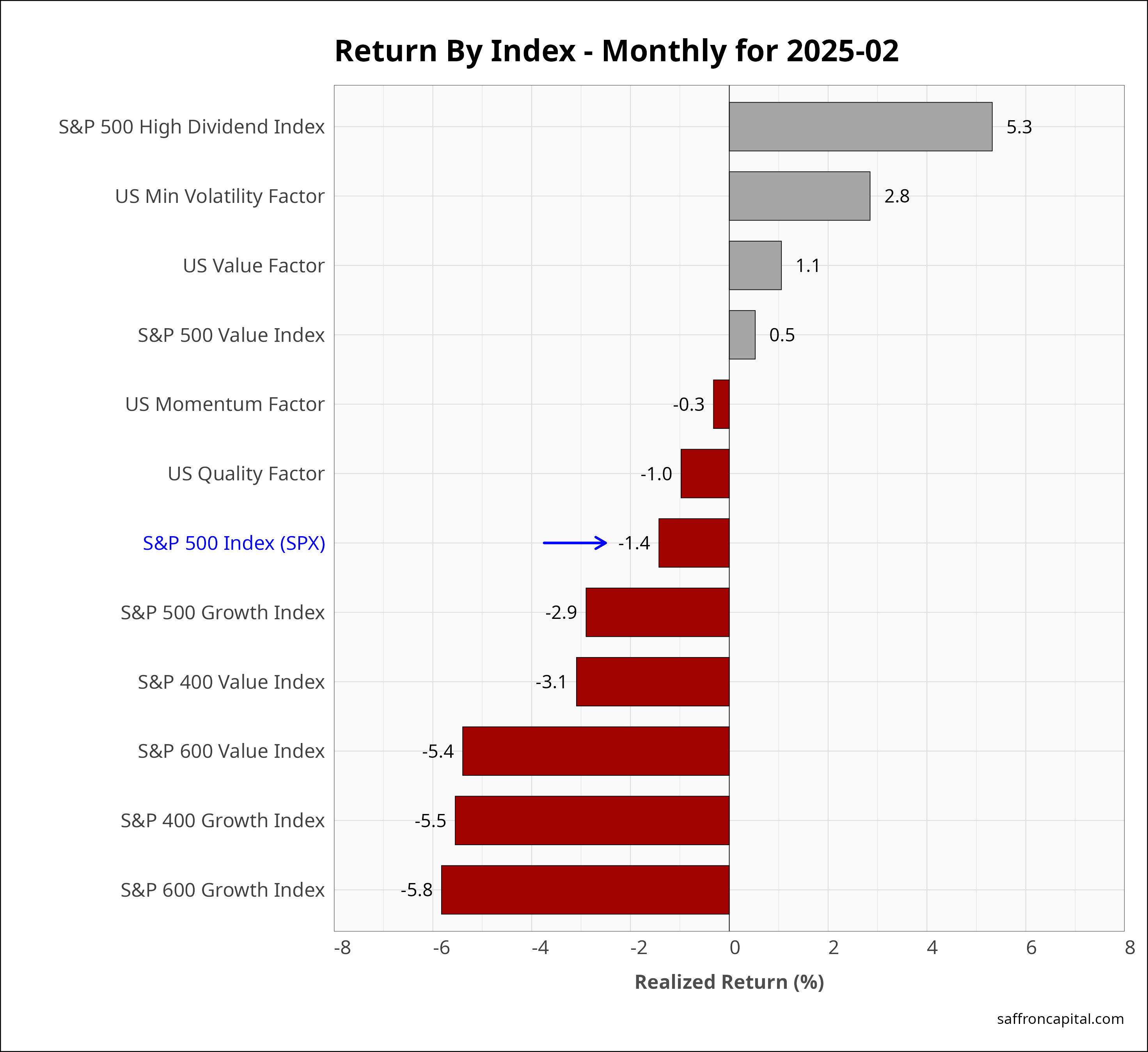

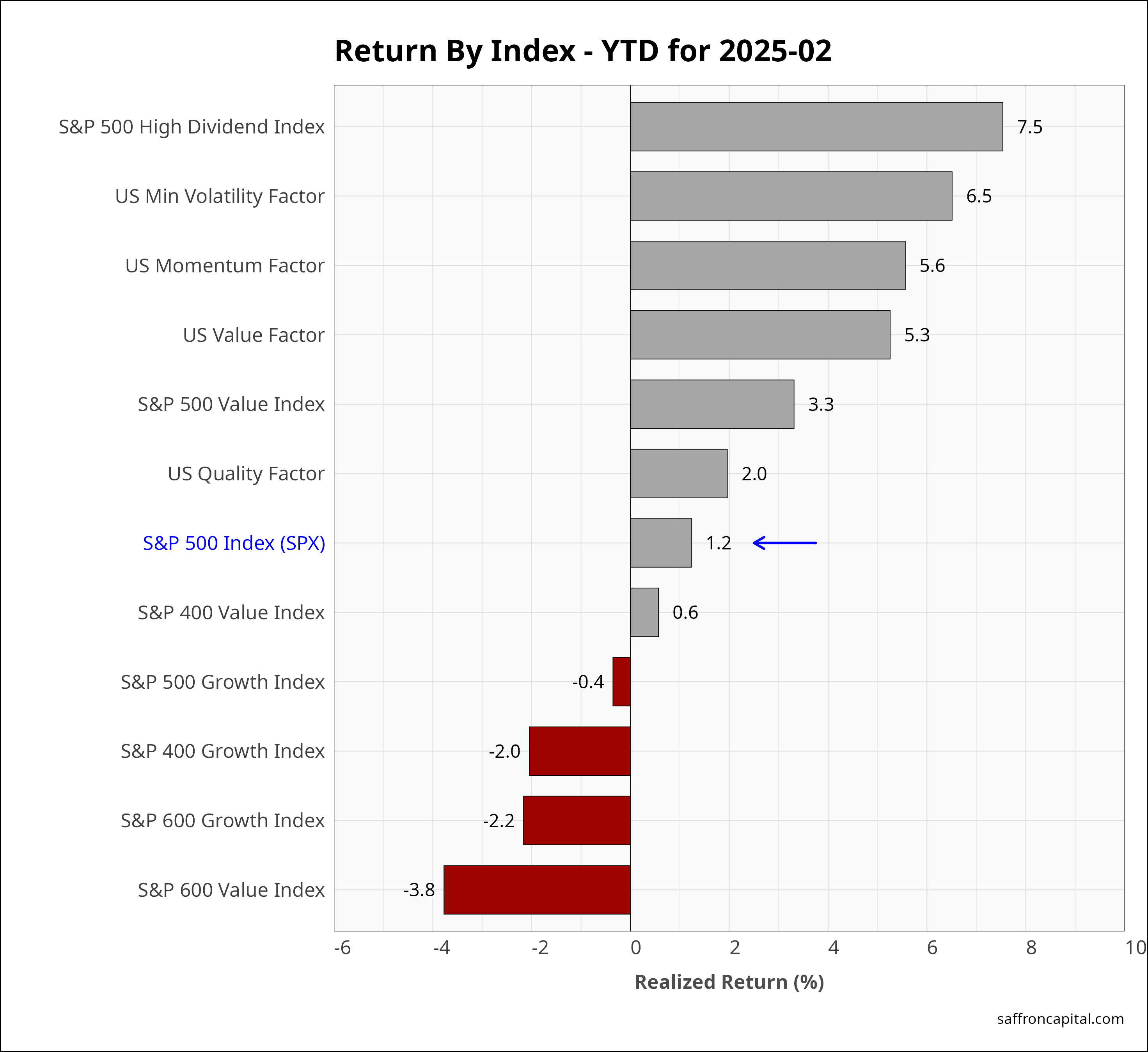

US Factor Indices

Factor portfolios are constructed to emphasize the core drivers behind returns, which include company size, relative value, profitability, growth, and momentum. Multi-factor portfolios combine two or more factors. The chart below shows 6 factor portfolios outperformed the S&P 500 index in February, including the S&P 500 High Dividend Index (+5.3%), the US Minimum Volatility Index (+2.8%), and the US Value (+1.1%) portfolio. Laggards included Small-cap Growth (-5.8%) and Mid-cap Growth (-5.5%). Year-to-date, the High Dividend index (+7.5%) is leading performance.

Click to enlarge

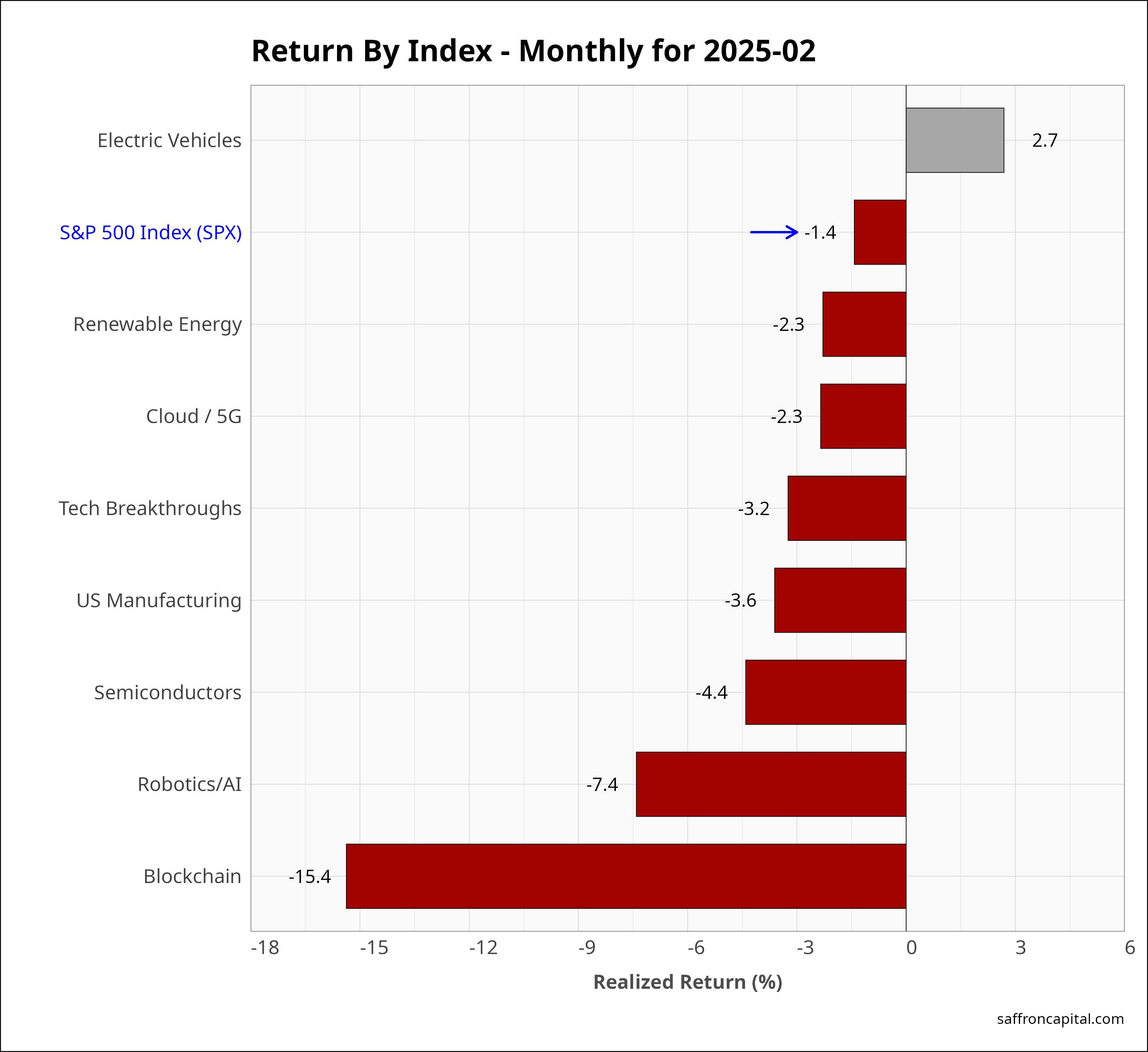

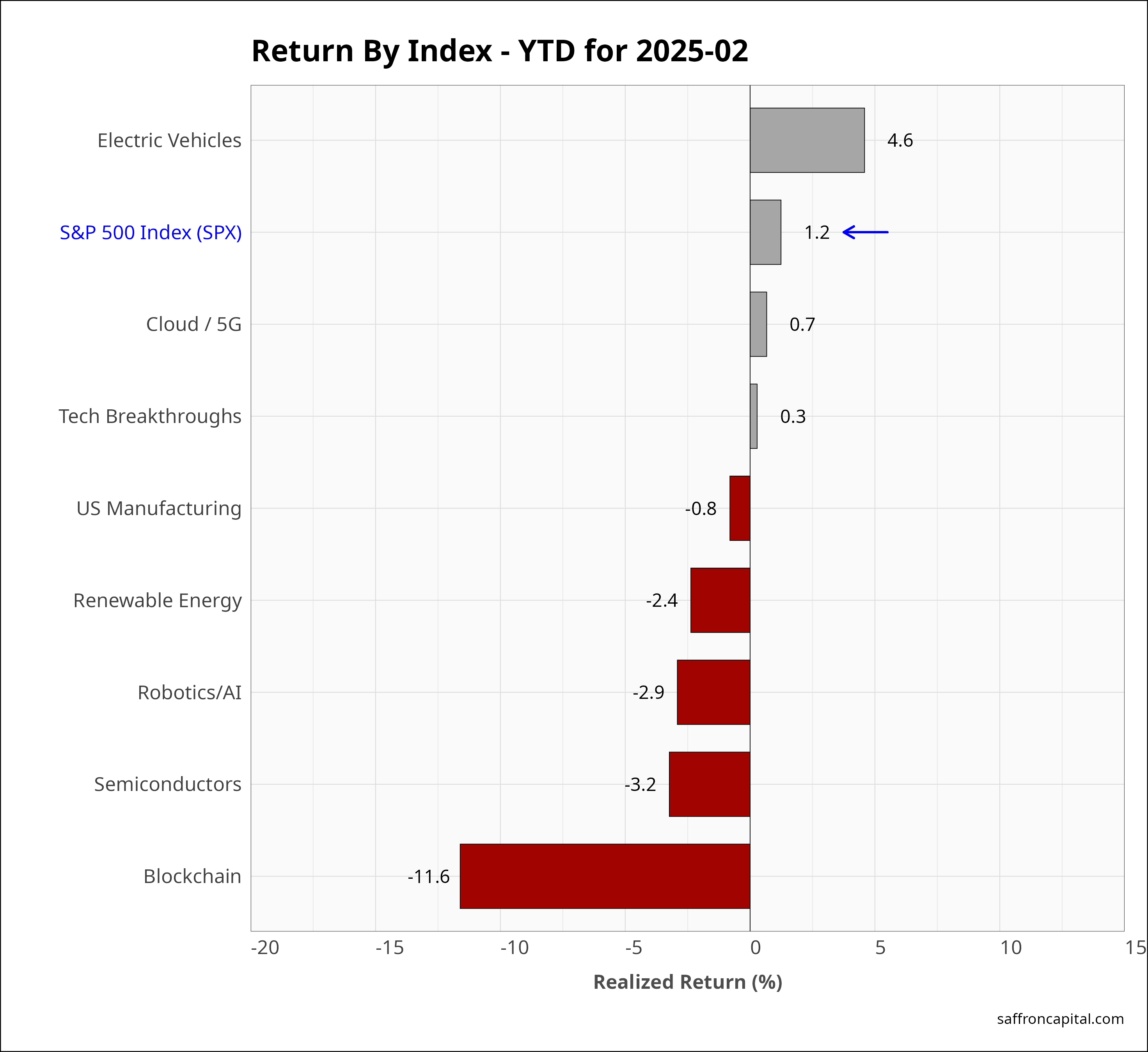

US Megatrend Equities

US megatrend equities are thematic growth portfolios that capture the primary growth trends of the U.S. economy. February returns were led by Electric Vehicles (+2.7%). All the other thematic portfolios were down for the month. The steepest losses were seen in Blockchain (-15.4%) shares. Since the start of the year, positive portfolios include Electric Vehicles (+4.6%) and Cloud/5G services (1.2%).

Click to enlarge

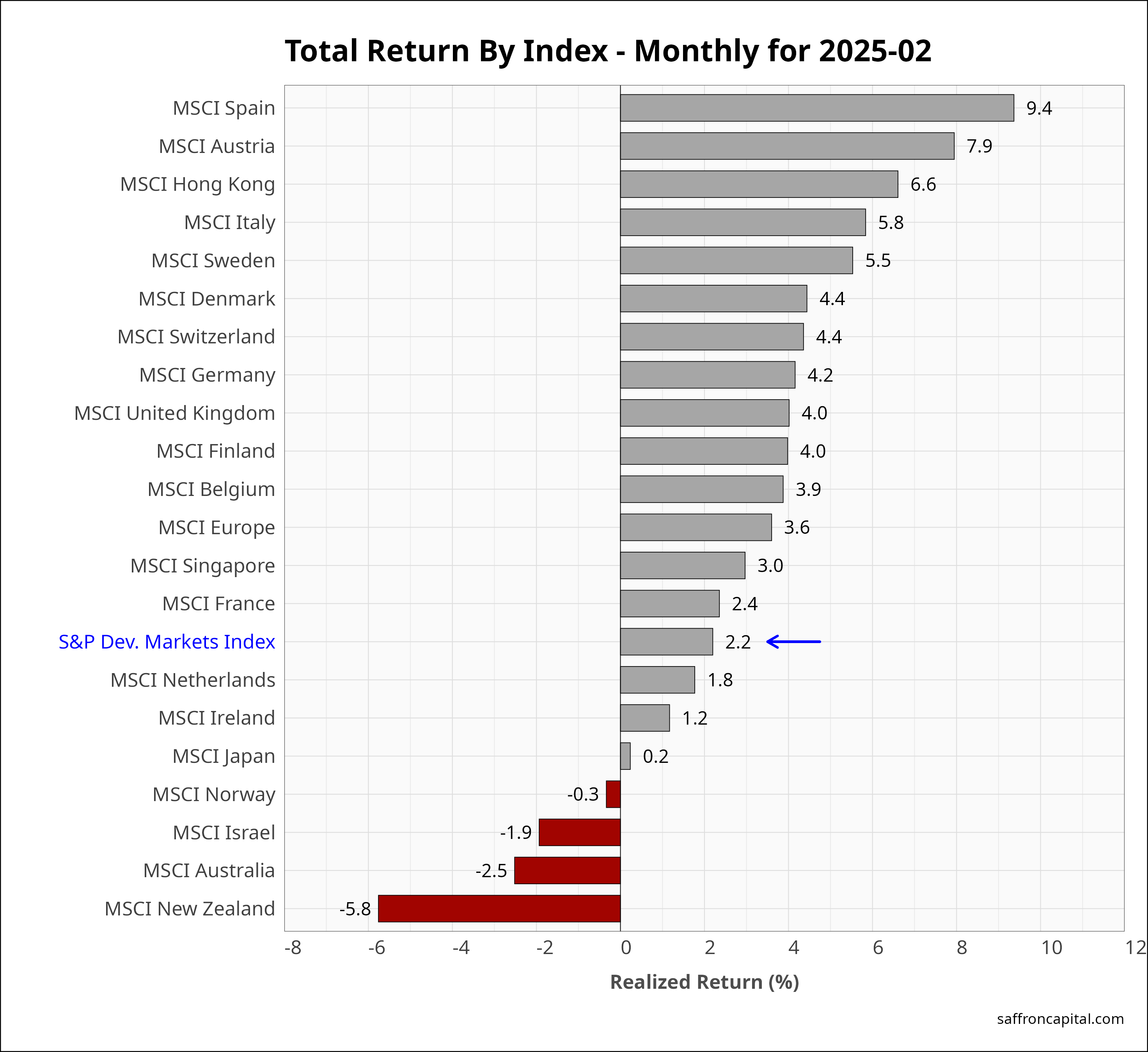

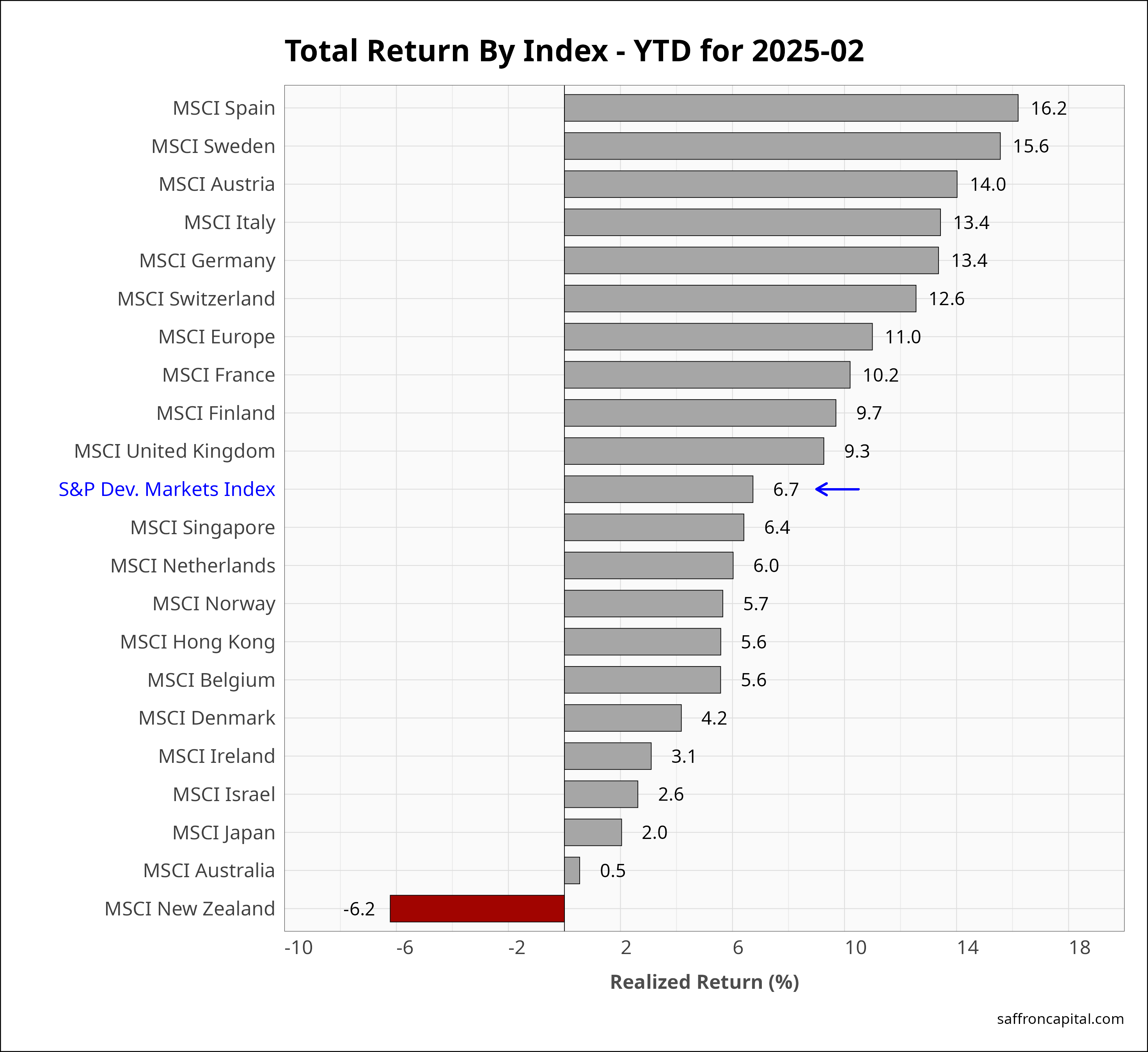

Developed Market Equities

International Developed Markets index (+2.2%) led equity returns in February The MSCI Europe index (+3.4%) again outperformed the US. Typically, when international shares outperform the US in the first two months, they tend to outperform over the entire year. Since December, the Developed markets index (+6.7%) is outperforming significantly, led by Spain (+16.2%), Sweden (+15.6%) and Austria (+14.0%).

Click to enlarge

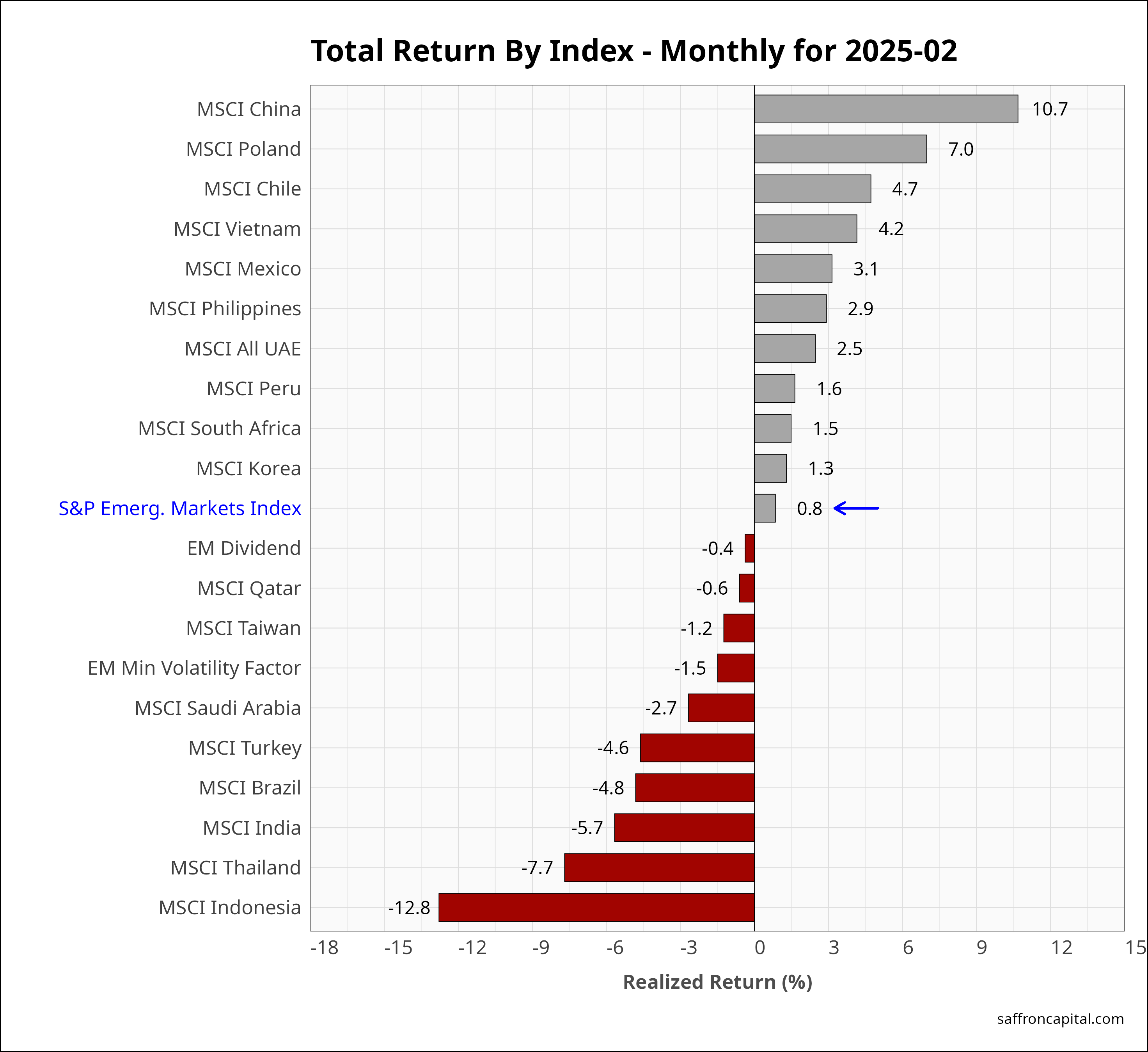

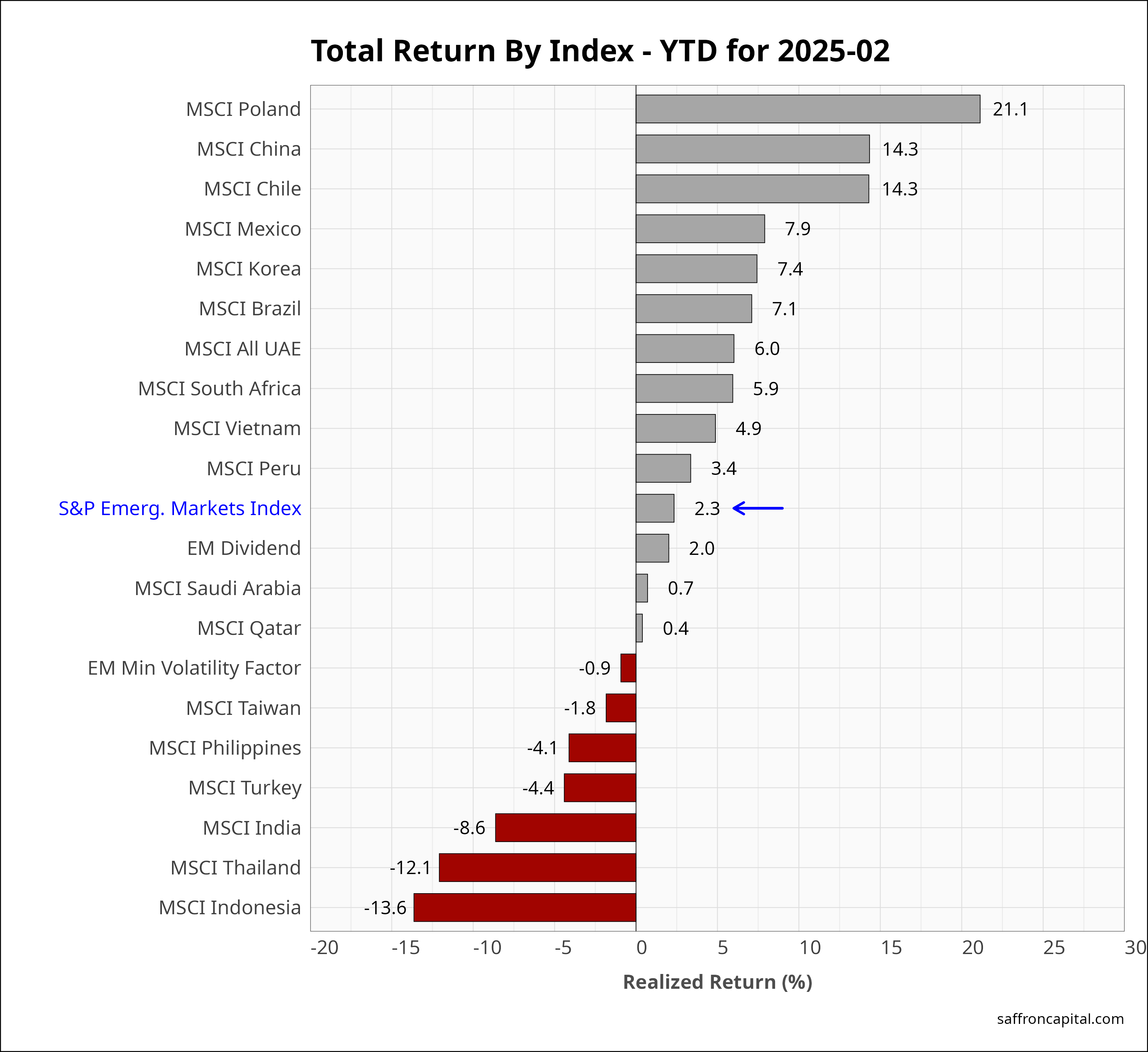

Emerging Market Equities

The S&P Emerging Markets Index (+0.8%) was essentially flat but did well versus U.S. benchmarks. China (+10.7%), Poland (+7.9%), and Chile (+4.7%) topped the chart in February. Korea (+1.3%) earned a positive return, Japan was essentially flat (+0.2%), while India (-5.7%) continued to disappoint on reduced earnings outlooks. Year-to-date, Poland (+21.1%) is the top performing stock market in the world, followed by China (+14.3%) and Chile (+14.3%).

Click to enlarge

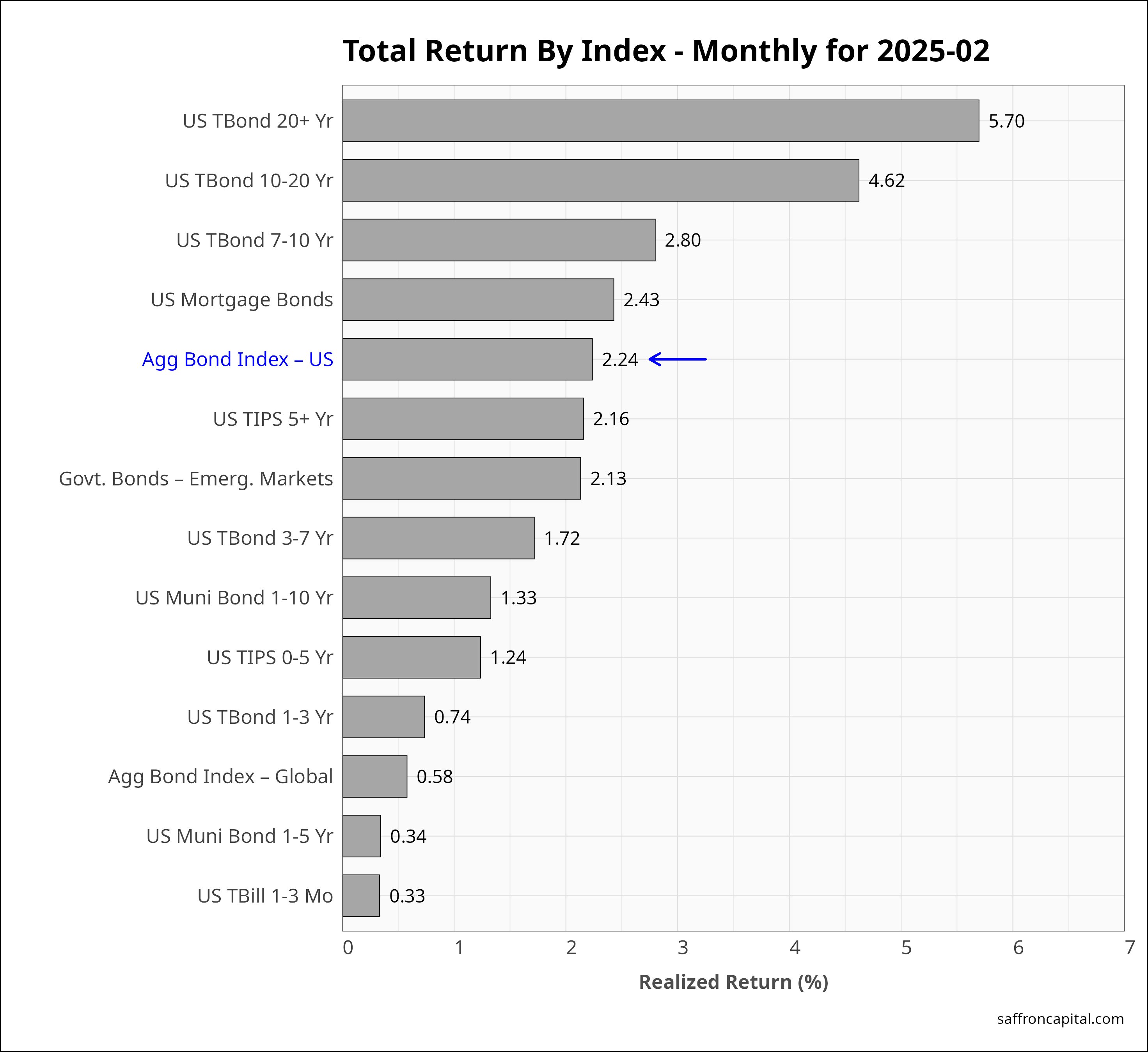

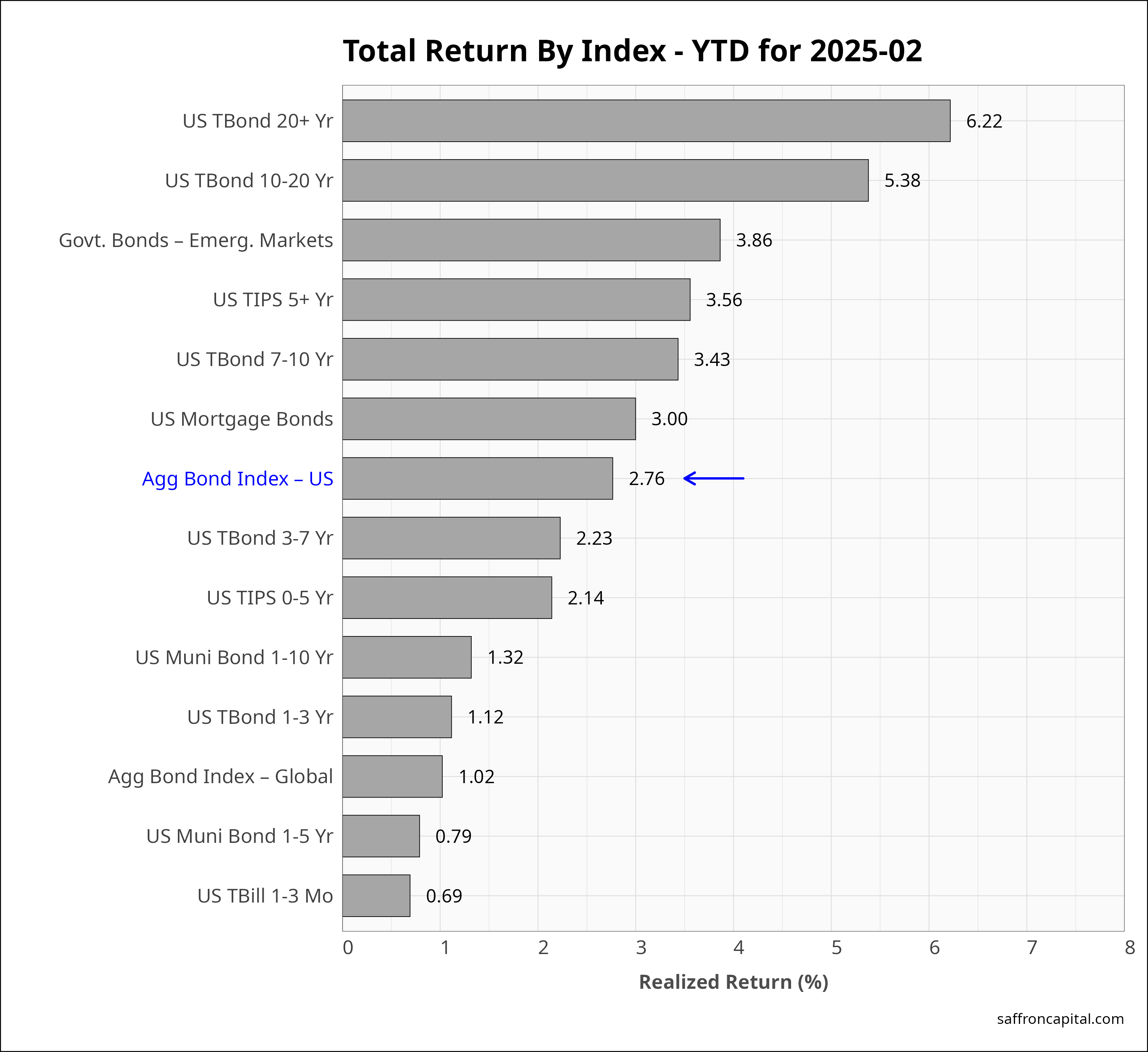

Government Bonds

During February, the yield-to-maturity on the 10-year Treasury Note fell from a high of 4.66% to 4.19%. As a result, the US fixed income markets remained positive. February returns on the US Aggregate Government Bond Index (+2.24%) outperformed Global Government Bonds (+0.58%) US 20Y+ bonds (+5.7%) had strong returns, as did the other mid- and long-dated bonds. Year-to-date, the Aggregate Bond Index (2.76%) is outperforming equities.

Click to enlarge

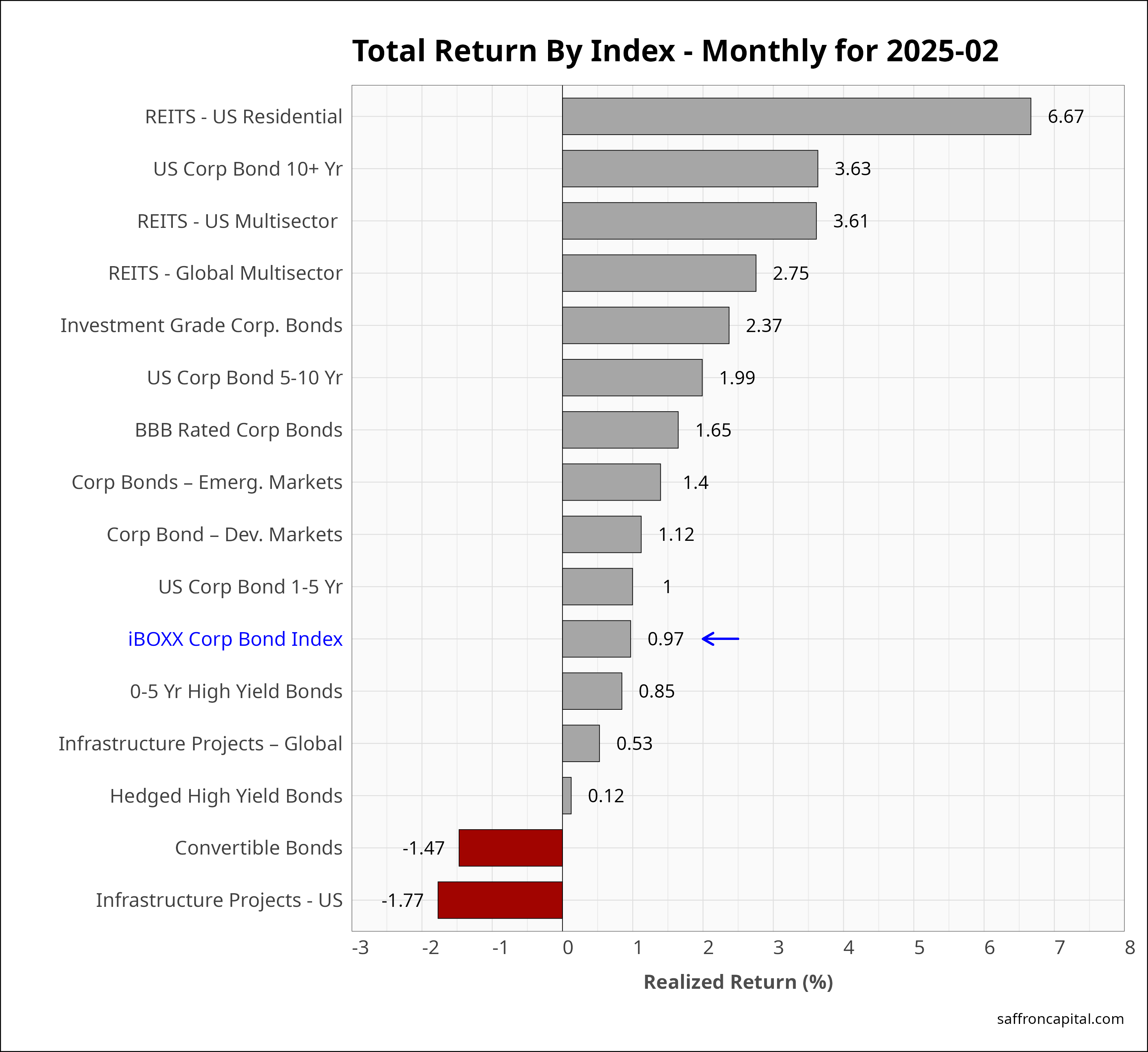

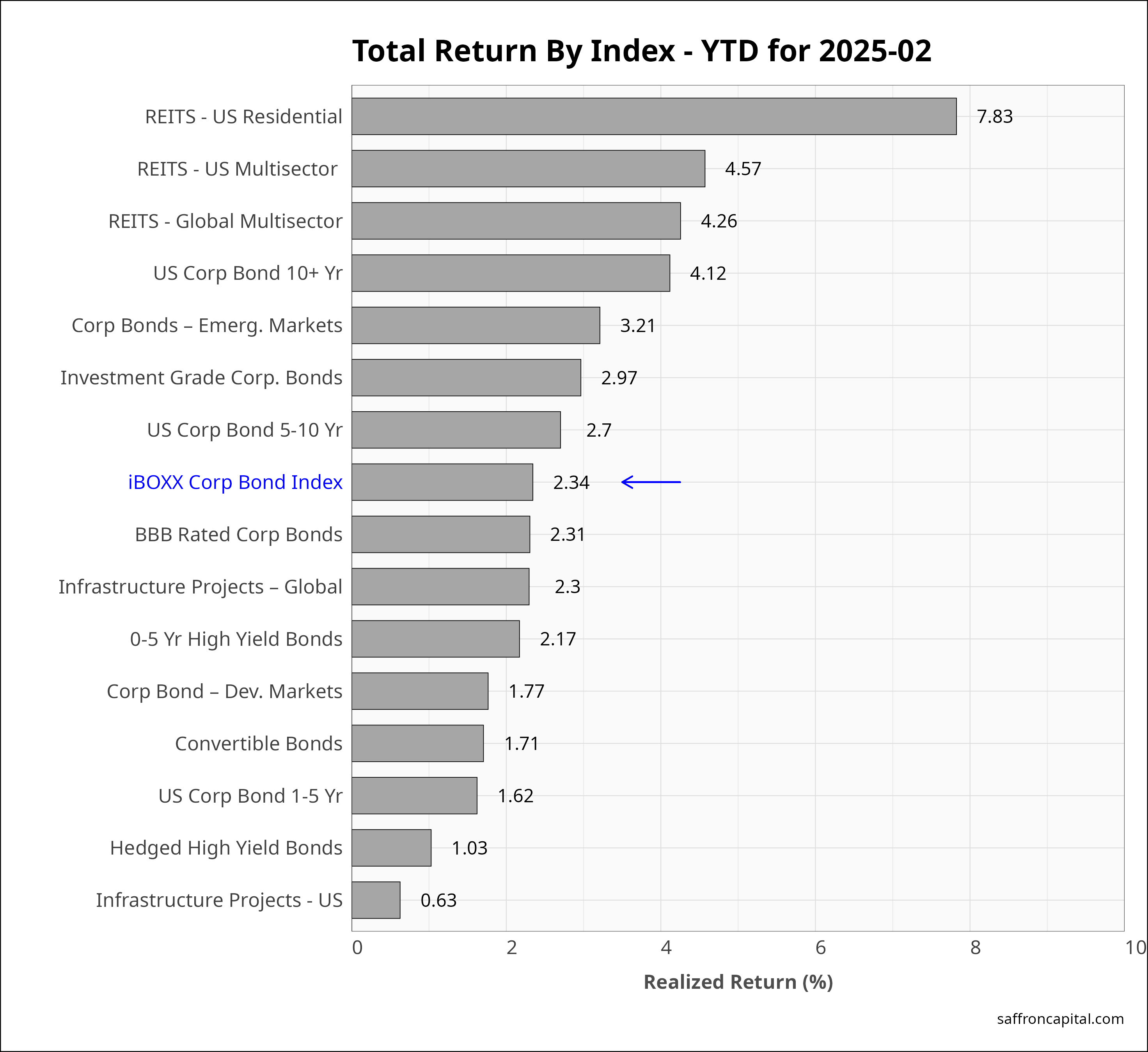

Corporate & Infrastructure Bonds

The iBoxx Corporate Bond Index (+0.97%) was positive in February, but lagged government bond benchmarks. Top sector returns included REITS – US Residential (+6.67%) and long-dated Investment Grade Bonds 10Y+ (+3.61%). US Infrastructure Project Bonds (-1.71%) failed to get a boost from declining rates and fell victim to the risk-off regime in equities. Year-to-date, the iBOXX Corporate Bond Index (+2.34%) is outperforming US equities. REITS are also performing strong with returns ranging from +4.0% to 7.8%.

Click to enlarge

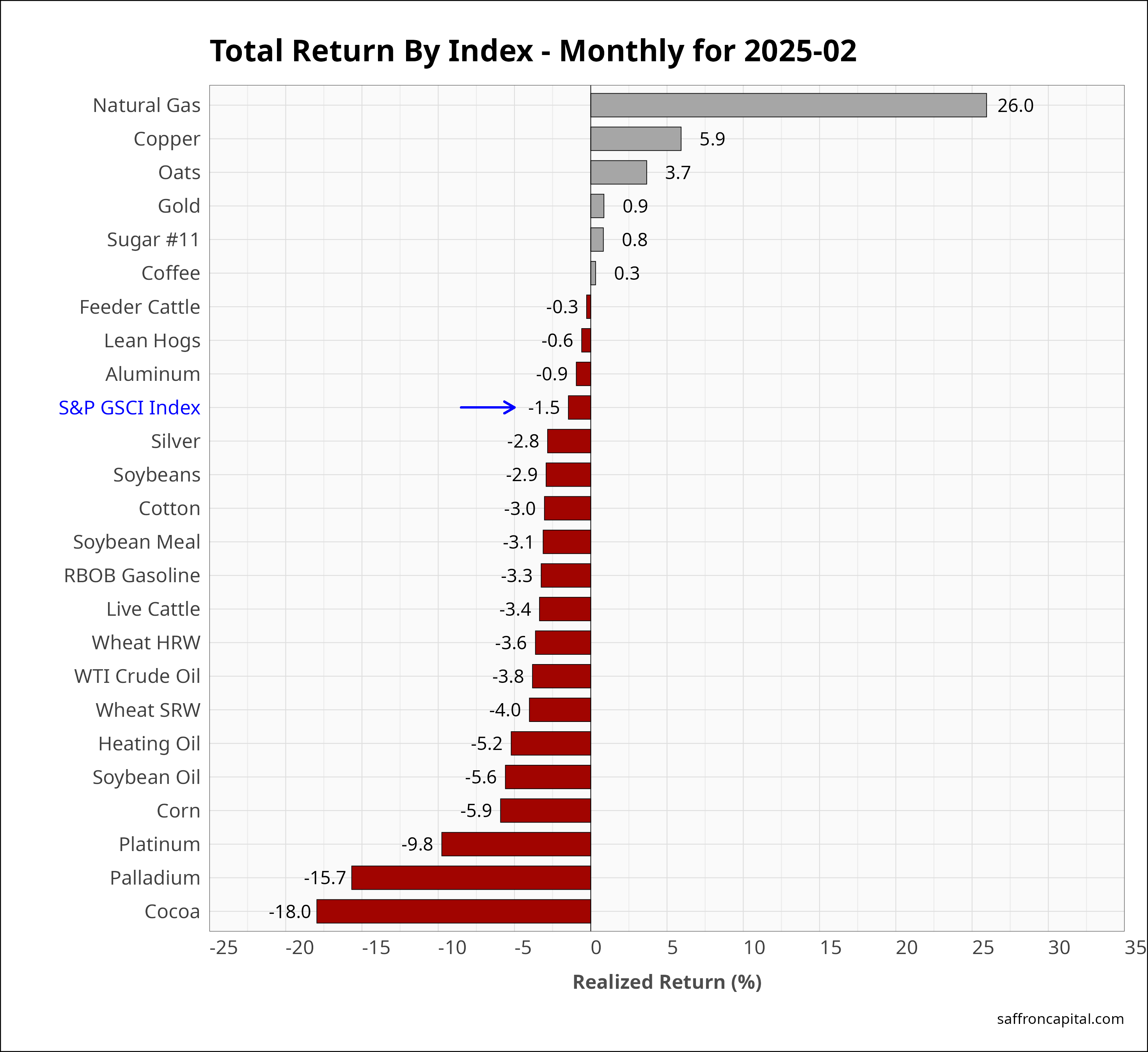

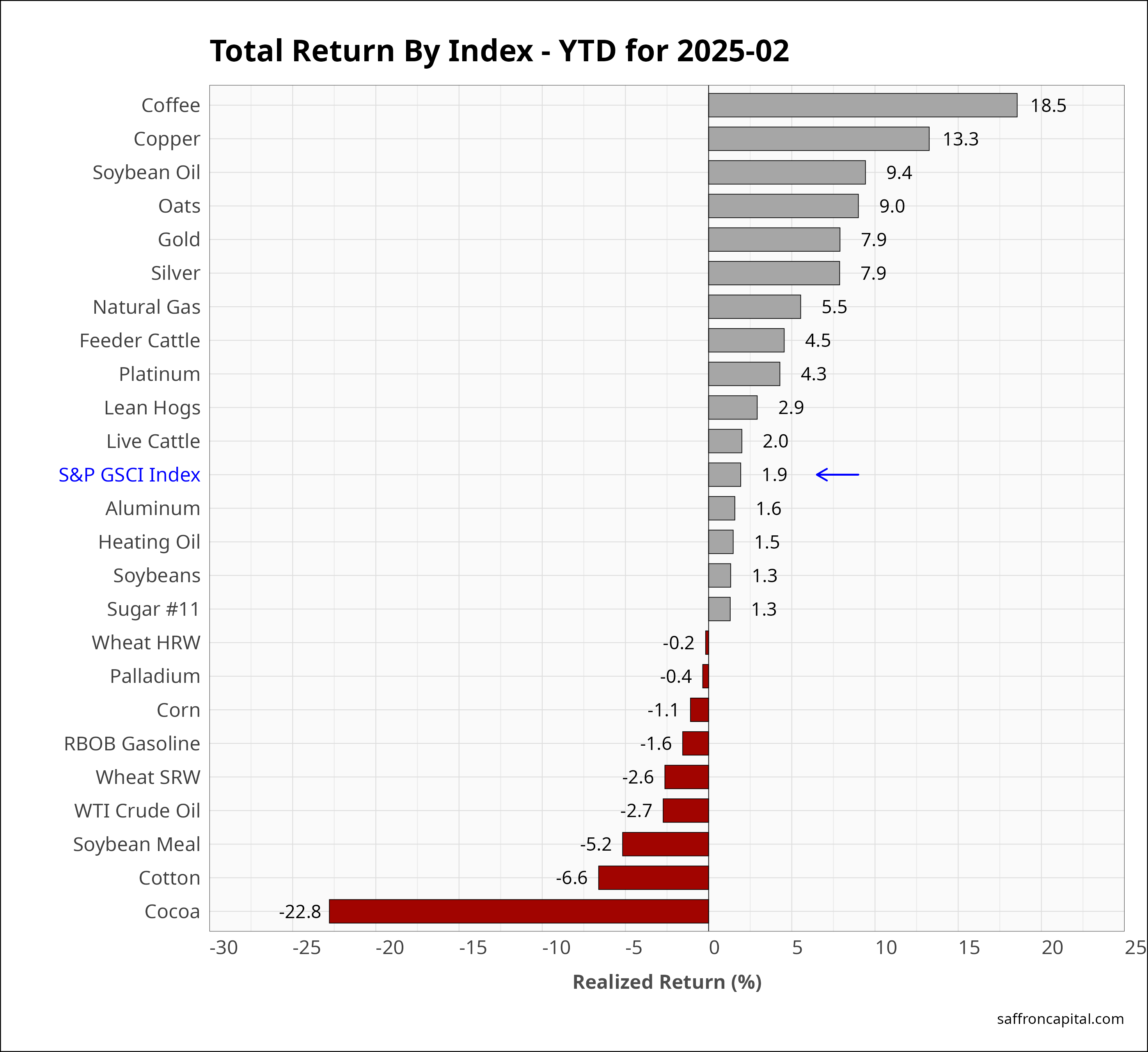

Commodities

Commodities, as measured by S&P GS Commodity Index (-1.5%) were down in February, led by Cocoa (-18.0%) and platinum group metals. The strongest commodities were natural Gas (+26.0%) and Copper (+5.9%). Year-to-date, the commodity index (+1.9%) is benefiting from a weaker dollar and has been led by Coffee (+18.5%) and Copper (+13.5%).

Click to enlarge

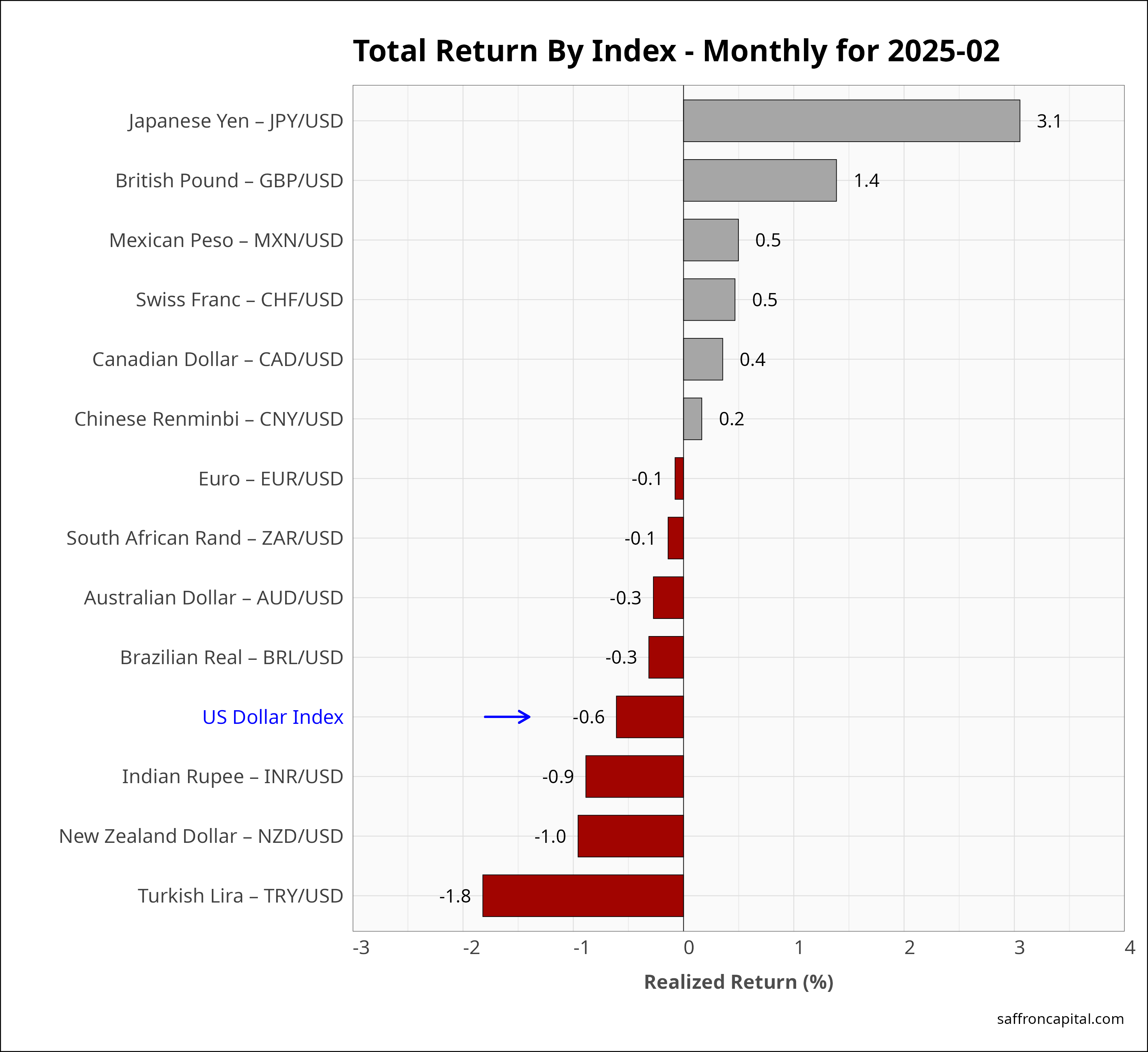

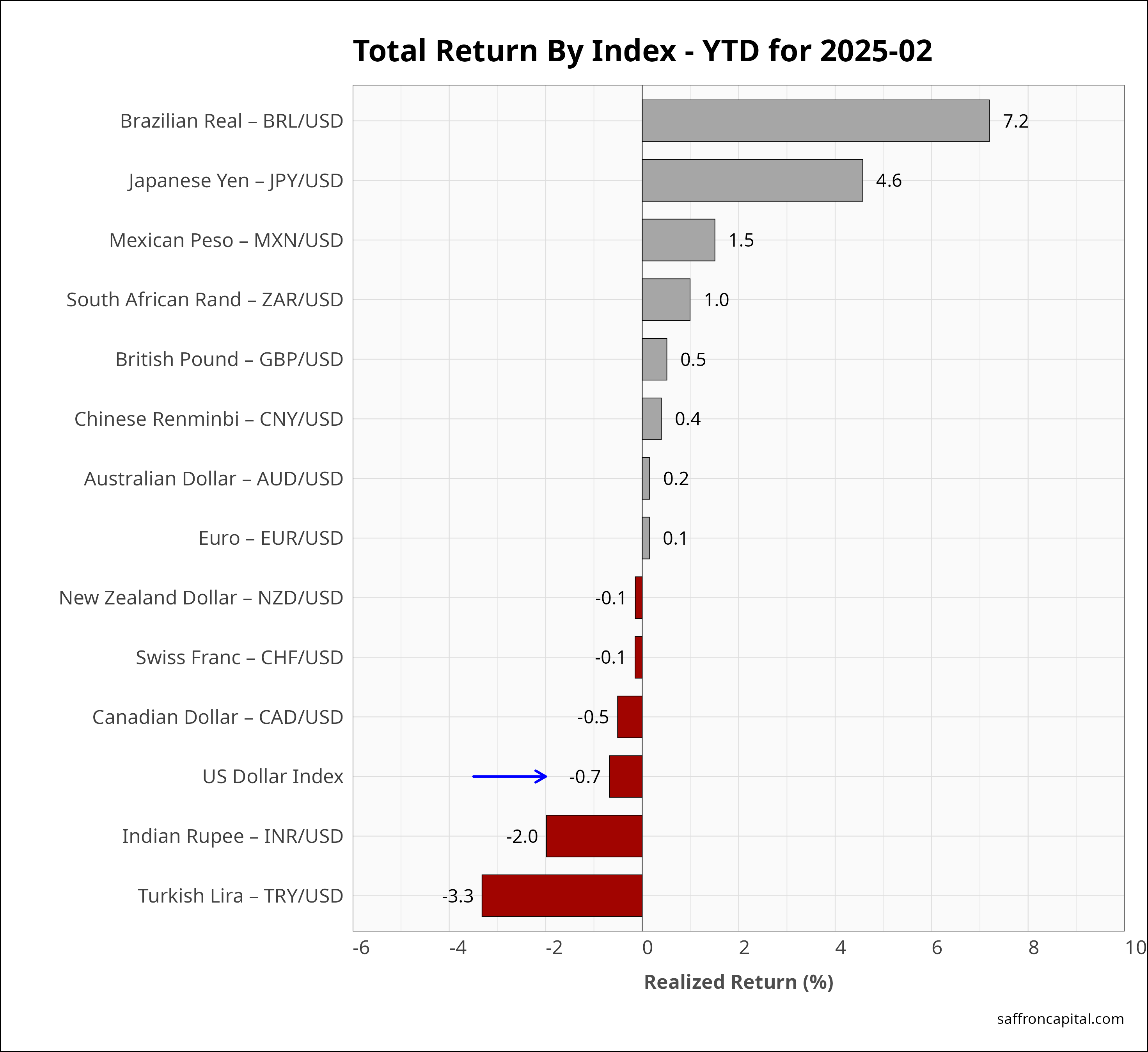

Currencies

The U.S. Dollar index (-0.6%) was basically modestly down in February with the Japanese Yen (+3.1%) posting the strongest monthly returns for the second month in a row. The Brazilian real (+7.2%) and the Japanese Yen (+4.5%) lead year-to-date performance.

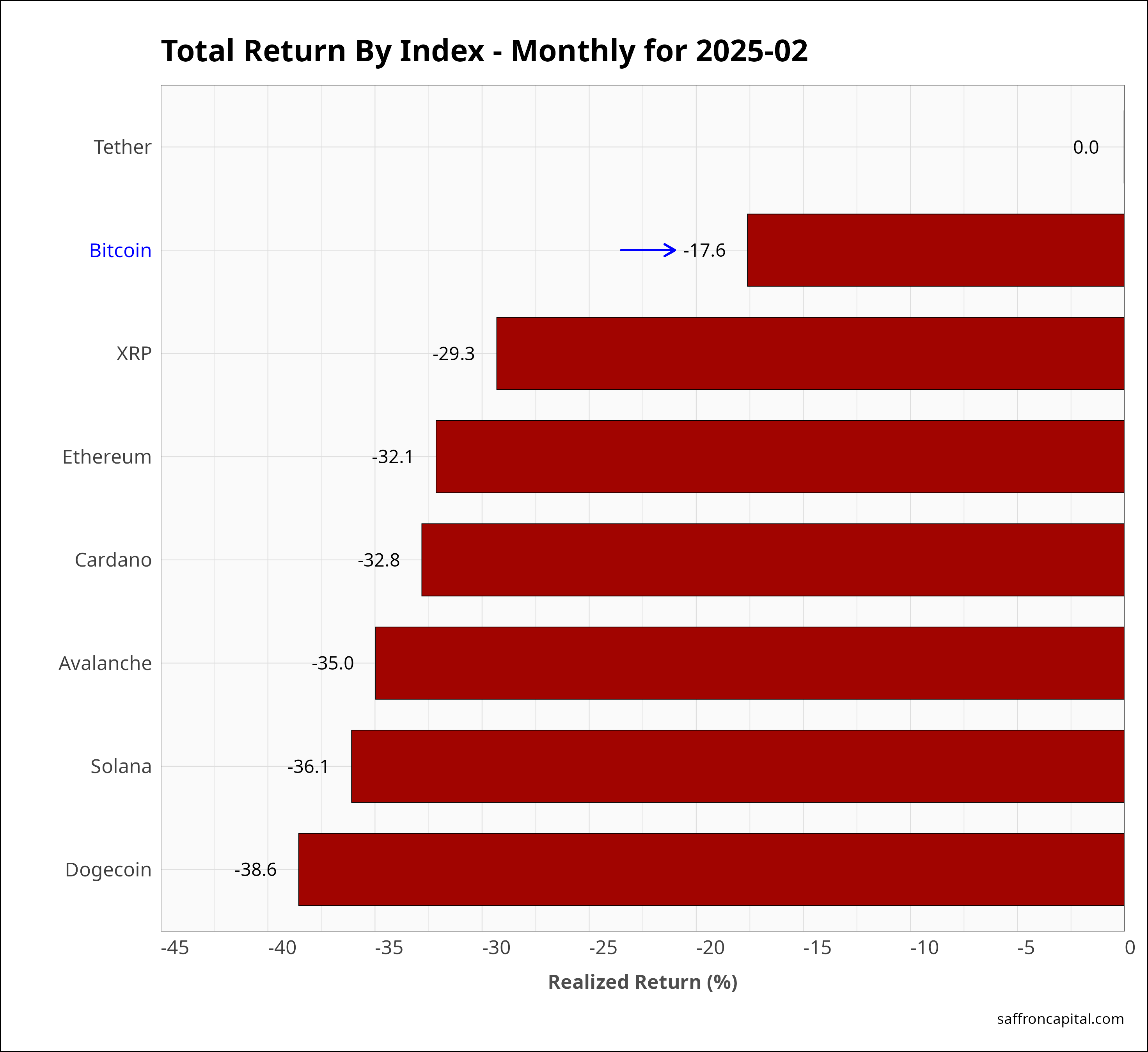

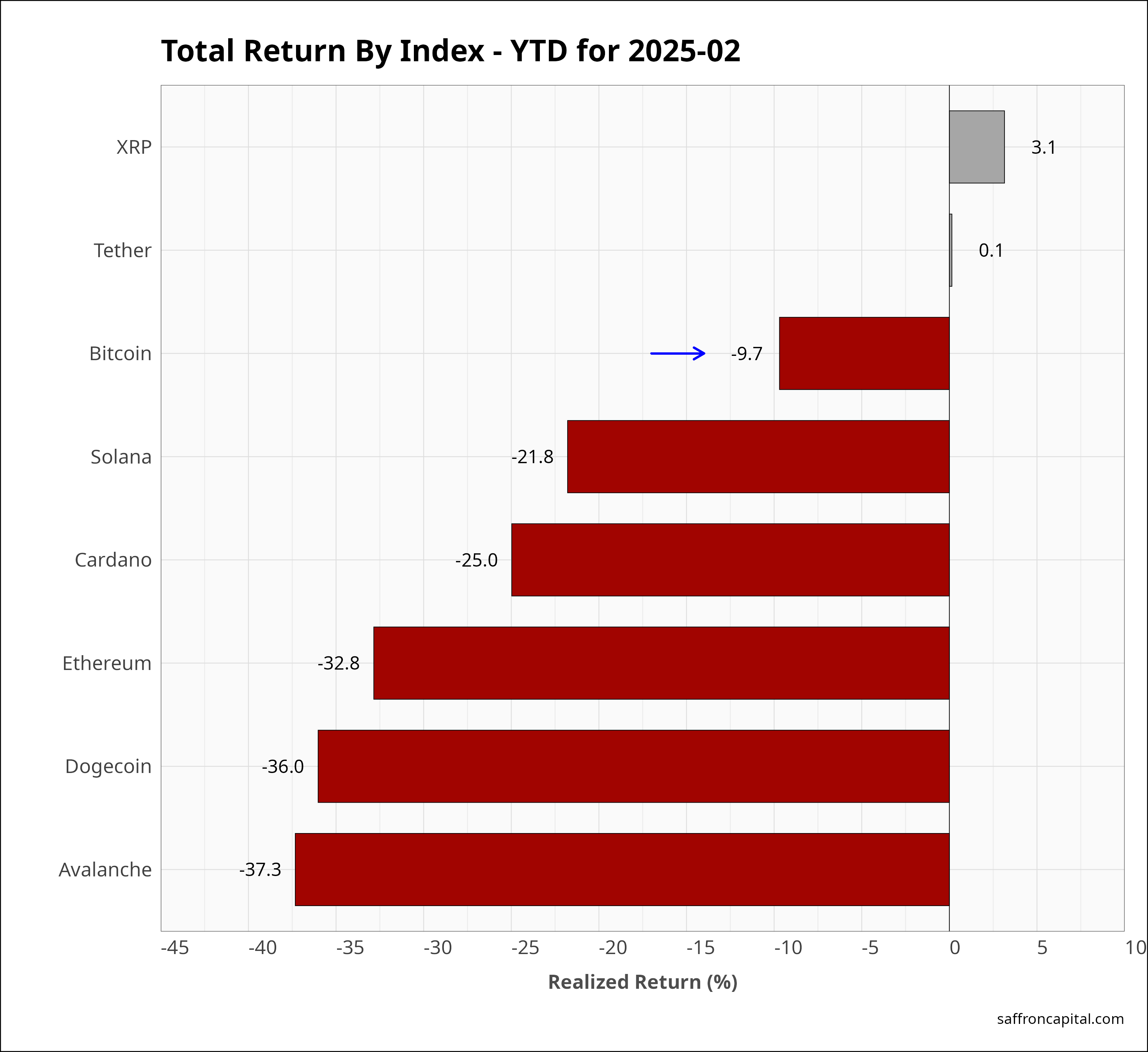

Cryptocurrencies

Cryptocurrencies revealed the extent of downside ‘tail risk’ they are prone to in February, undermining any claim to being a store of value. Benchmark Bitcoin (-17.6%) had modest losses compared to Dogecoin (-38.6%). Year-to-date, Bitcoin is down -9.7%.

Click to enlarge

Have questions or concerns about the performance of your portfolio? Could you benefit from a custom portfolio formulation that better aligns to your risk appetite? Whatever your needs, we are here to listen and to help. Contact us to schedule a meeting.

Saffron Capital LLC is a registered investment advisor that is employee-owned and Minnesota-based.

{kind=link}

{kind=link}

{kind=link}