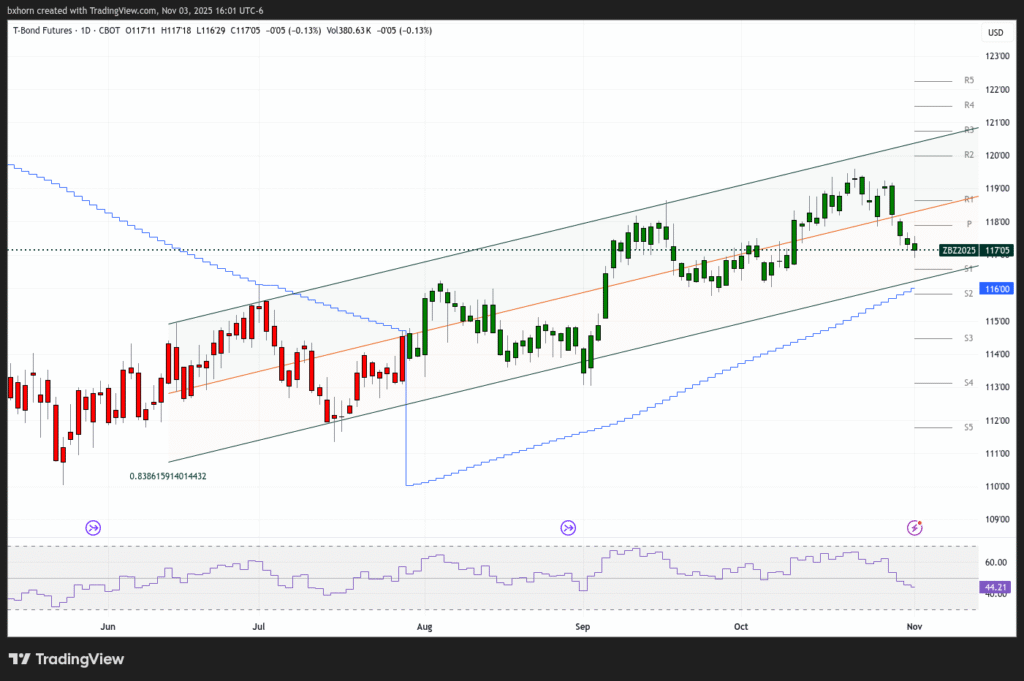

After last week’s hawkish pushback from Chair Powell, bond markets are looking for direction in private-sector data (ISM today; ADP/ISM Services mid-week), as well as the Treasury Department’s Quarterly Refunding Announcement.

Prior to the NY open, yields are up with 2’s printing 3.592%, 10’s at 4.108%, and 30’s up the most at 4.687%. The bond market yield curve is modestly inverted in the belly and steepest from 10s to 30s.

European markets remain supportive for long duration bonds with euro-area inflation lower to 2.1% y/y in October, with the ECB on hold, and Bund yields at 2.65%. The UK confronts the BoE rate decision this week with gilts around 4.4%.

Treasuries are range-bound since the macro board is mixed and there is no clear catalyst to start the week.

In response, December T-Bond futures (ZB) are down-trending short-term with the playbook tilted to selling rallies ahead of the refunding update. The short position bias is reinforced by multiple closes below the 18D MA and daily momentum indicators that are negatively sloped at mid-range. Downside potential will be reinforced on a firmer ISM/BoE-holds narrative or any refunding language that tilts supply toward coupons.

First support is 117-01 (the 50D MA) and our downside target is 116-19. Key resistance levels are 117-19 and 117-29 (the 5D MA).

Our short bias could be revised given a soft ISM/ADP beat to the downside or dovish Fed-speak that nudges the 30-year below 4.60%. We see potential for a short squeeze, but only on a decisive yield break sub-4.55%. We begin the week by keeping position sizes tight into Wednesday’s refunding news.

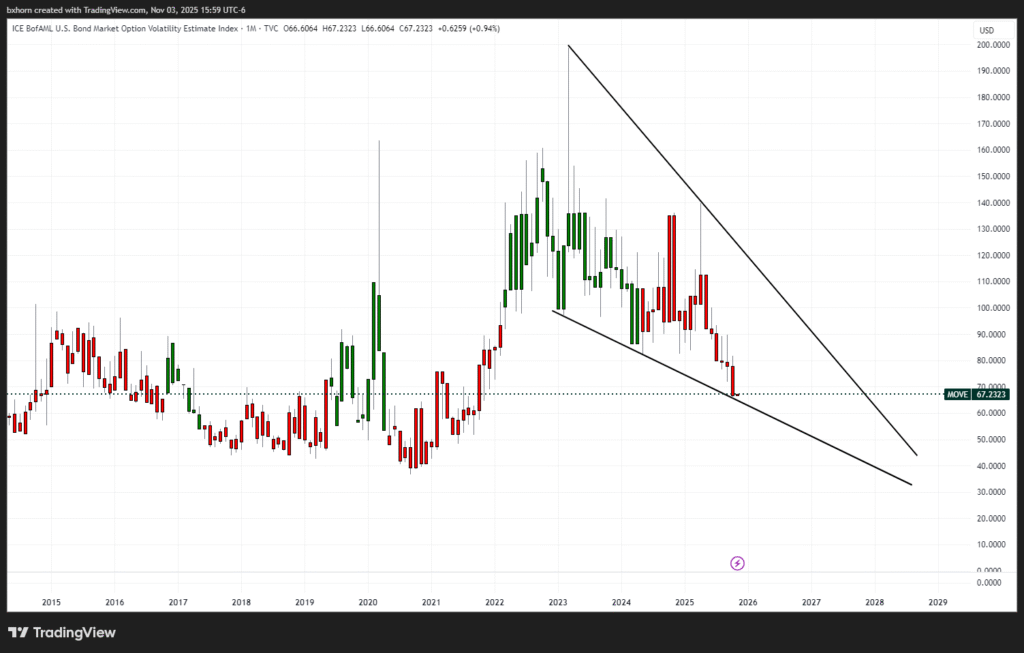

Move Index

Bond market volatility is also at its lowest since 2022, as shown below:

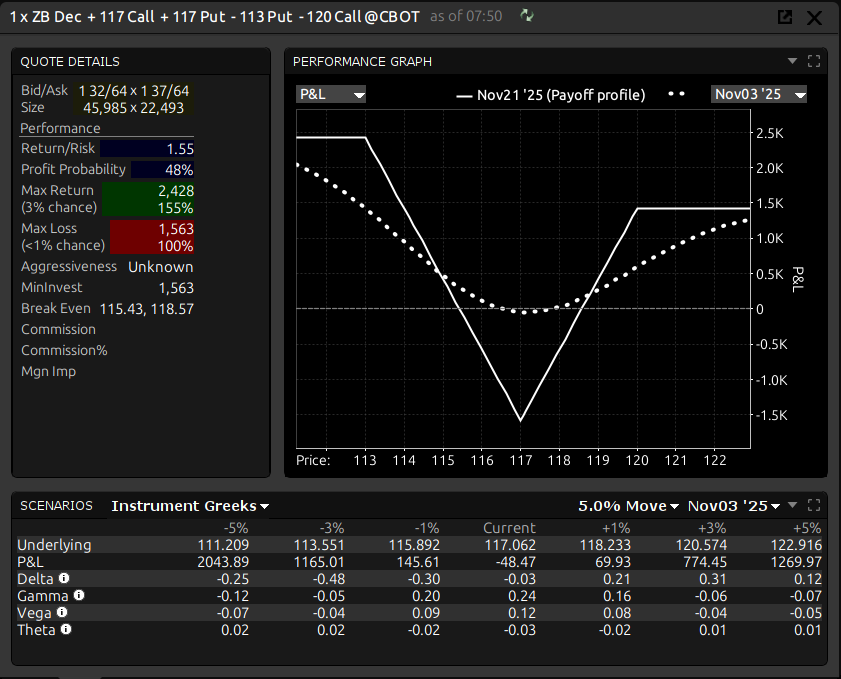

Option Strategy

The following table profiles the risk/reward for a long volatility strategy using options on December T-Bond futures expiring November 21, 2025.

{kind=link}

{kind=link}

{kind=link}