Morning Update

U.S. Treasuries firmed overnight as growth cooled and policy uncertainty increased. ISM manufacturing fell to 48.7 in October as new orders/production weakened and prices eased. Meanwhile, the Treasury cut its Q4 borrowing estimate to $569B, an additional tailwind for duration. Markets now eye Wednesday’s Treasury refunding strategy.

Fed speakers kept December “alive” but also pushed back on automatic cuts, clouding the rate-path. Yields lower this morning with most of the drop in the front: 2’s are 3.578%, 10’s are 4.097%, and 30’s trade 4.680%.

Abroad, eurozone yields are tracking Treasuries lower. In Japan, officials jawboned the yen and JGB yields edged up. Canada’s PMI improved to 49.6, and Australia’s RBA held at 3.6%, rounding out a mixed global PMI.

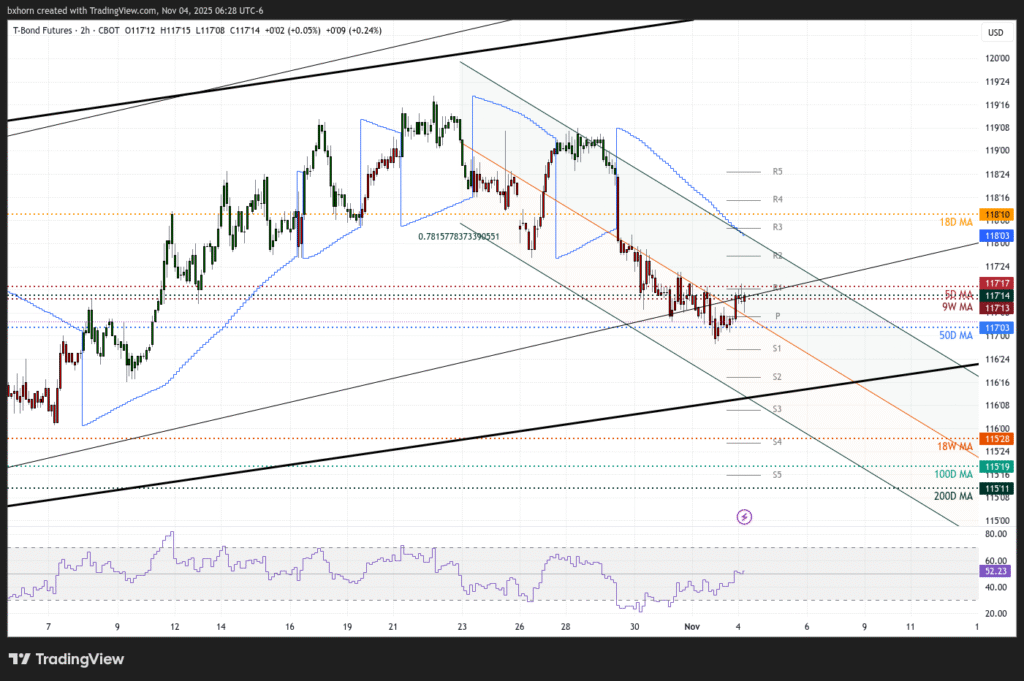

Prices for T-Bond futures $ZB are up after testing the 50D MA support at 117-03. In pre-open trade, Prices are now testing a key resistance zone between 117-13 and 117-17.

Daily momentum indicators continue to point downward, but hourly indicators have reversed in oversold territory.

Haven flows from equities could gain pace if a VIX breakout materializes. However, into the Quarterly Refunding, we will fade extremes and keep positions light. Hence, we like buying dips into deep support at 116-17, while selling rallies into resistance at 117-29.

Short-term through Wednesday, we expect two-way trade and ongoing consolidation. Long-term through month-end, we are positioned for a potential uptick in bond volatility given headline uncertainty tied to refunding, the government shutdown, and tariffs.

Technical chart below.

{kind=link}

{kind=link}

{kind=link}