The major asset classes achieved positive returns in December. Value lead growth stocks, consumer defensive beat consumer cyclical stocks, and mid cap outperformed large cap stocks. Total returns on infrastructure project bonds and high yield corporate bonds again outperformed the S&P500, as well as inflation protected Treasuries. Finally, commodities beat all asset classes this month with lumber, gasoline and crude oil posting the strongest gains.

The following analysis provides a visual record of returns across and within the major asset classes. The report is intended for investor portfolio comparisons and performance benchmarking.

US Equities

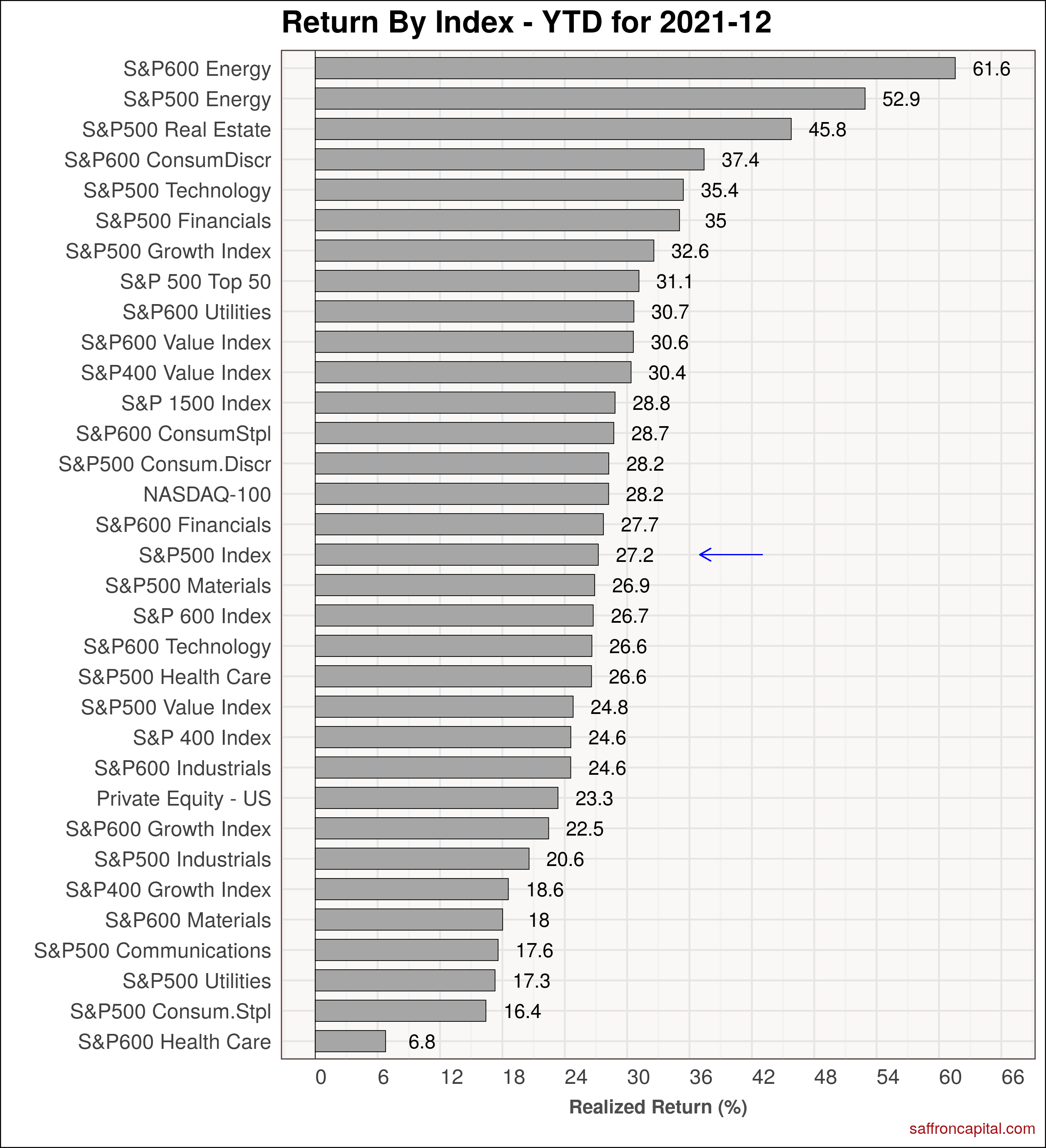

The S&P 500 index was up +6.1% in December with year-to-date (YTD) dividend-adjusted returns of +27.2%. The S&P 500 Real Estate sector (+11.5%) lead all other sectors in the S&P 500 index, followed by Consumer Staples (+10.2%), Health Care (+9.7%) and small cap Utility (+9.2%) stocks. Index underperformance was seen in Technology (+5.2%), Financials (+4.7%) and Energy (+3.8%) shares.

Developed Market Equities

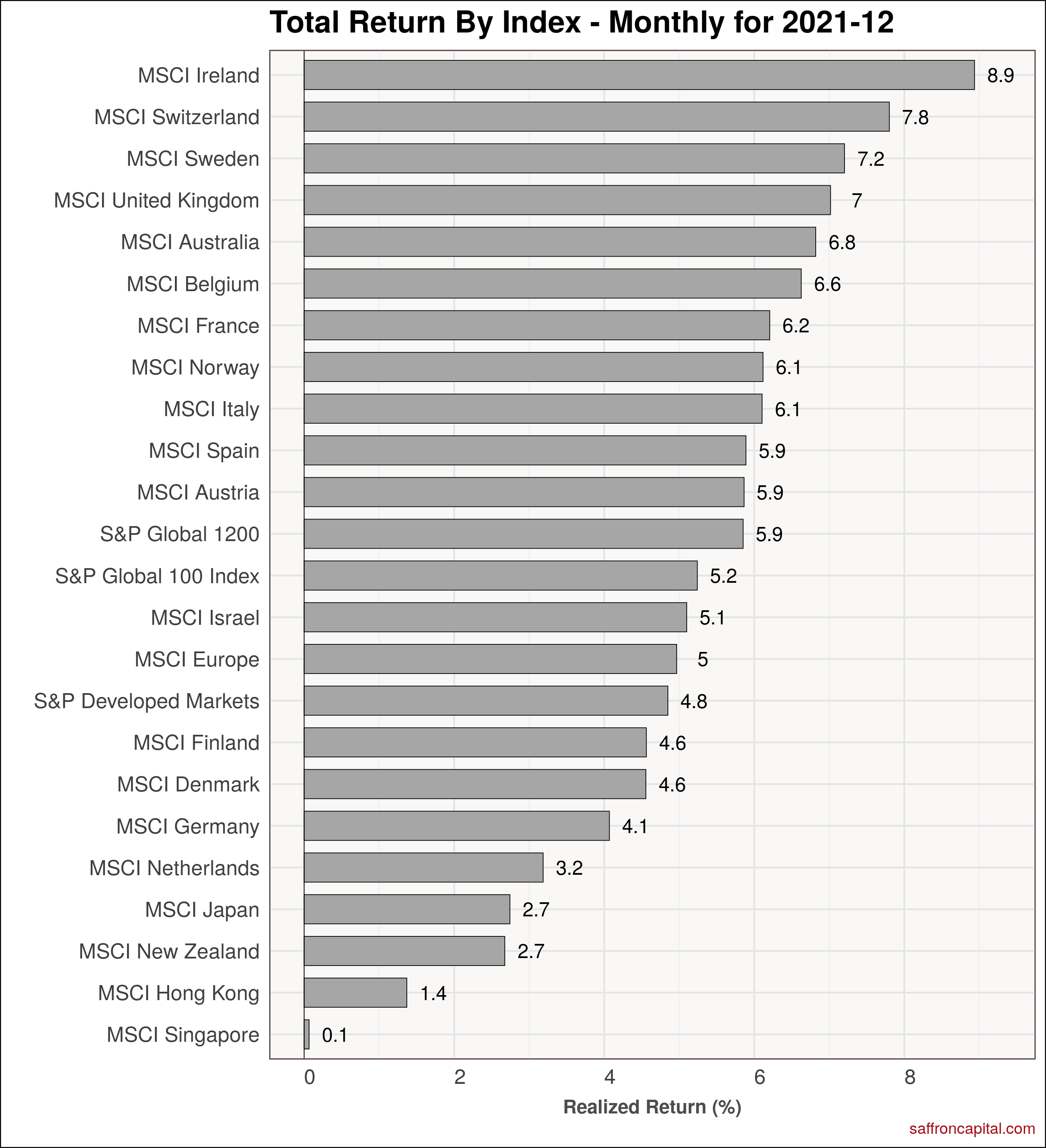

Elsewhere, all the developed market indices were positive for the month, with most European benchmarks outperforming the S&P 500 index. Ireland (+8.9%), Switzerland (+7.8%) and Sweden (+7.2%) to the monthly performance chart. Meanwhile, on a YTD basis, only Austria (+31.0%) beat the S&P 500. The MSCI Europe index finished the year at roughly half the return seen in the US.

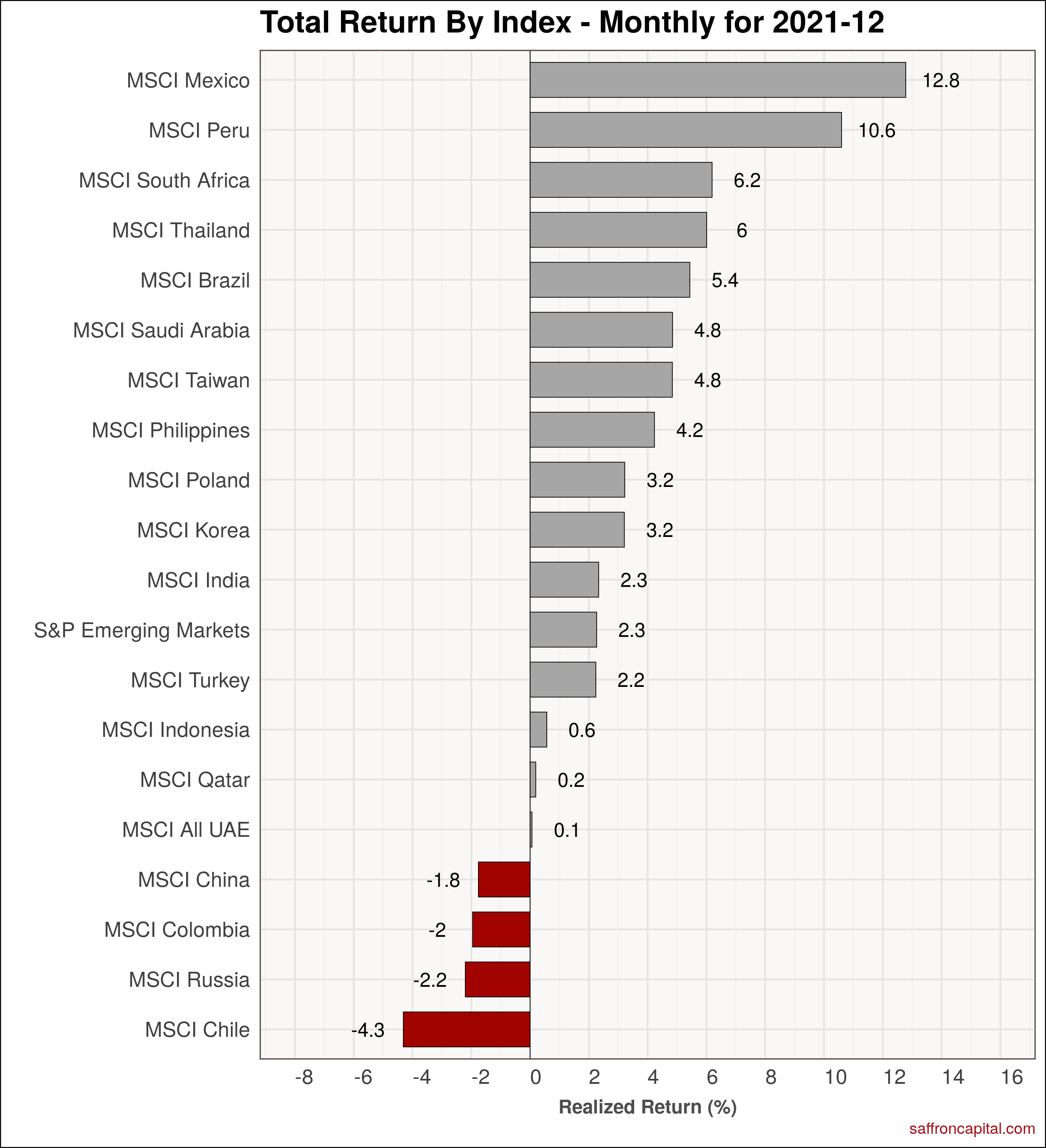

Emerging Market Equities

Mexican stocks delivered a strong December rally (+12.8%), capping the best YTD performance (+20.5%) in more than a decade. Annual country leaders included the UAE (+45.1%), Saudi Arabia (+34.4%), Taiwan (+29.1%) and India (21.2%). China (-21.3%) and Brazil (-20.0%) are both notable for weak annual performance.

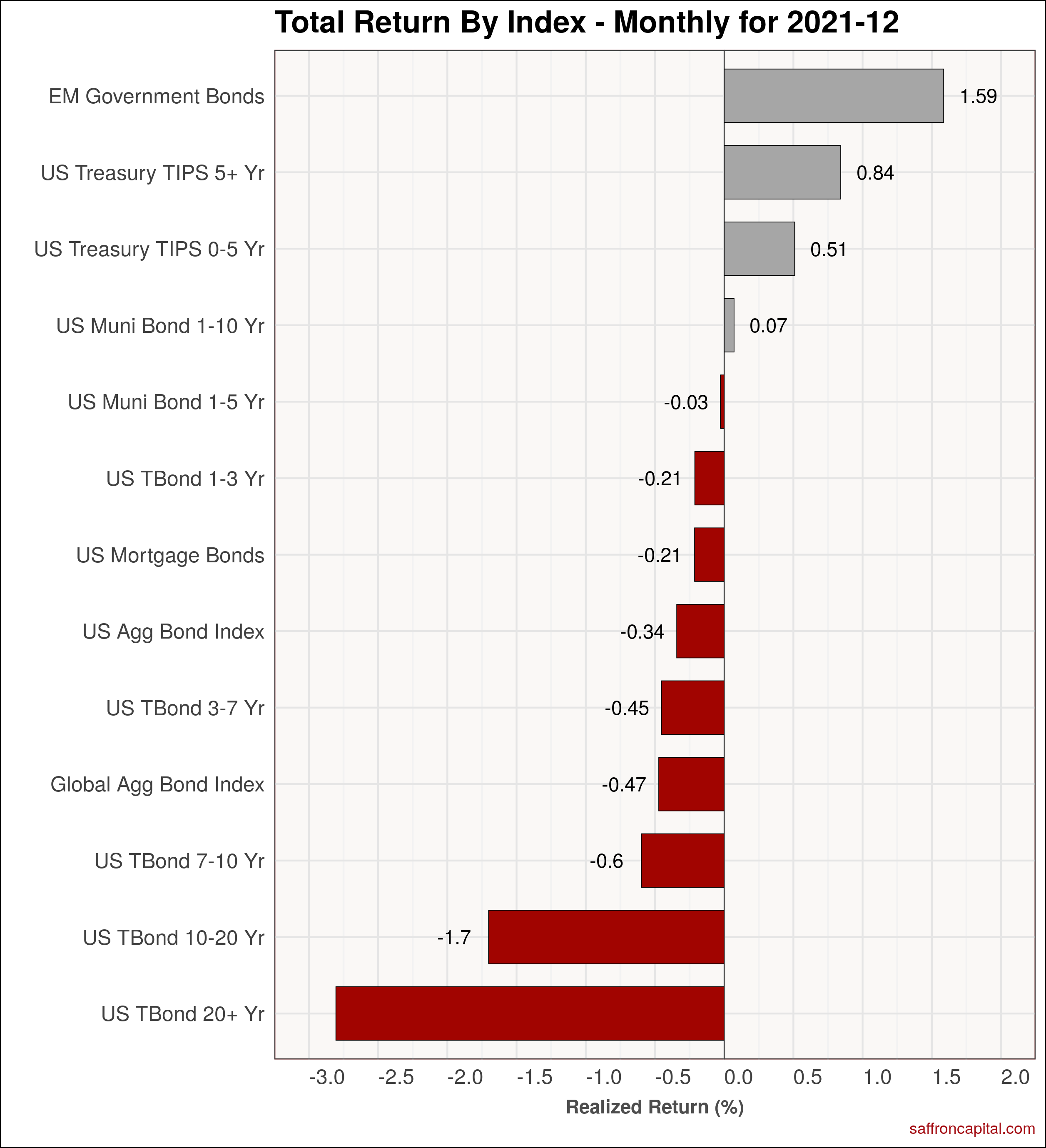

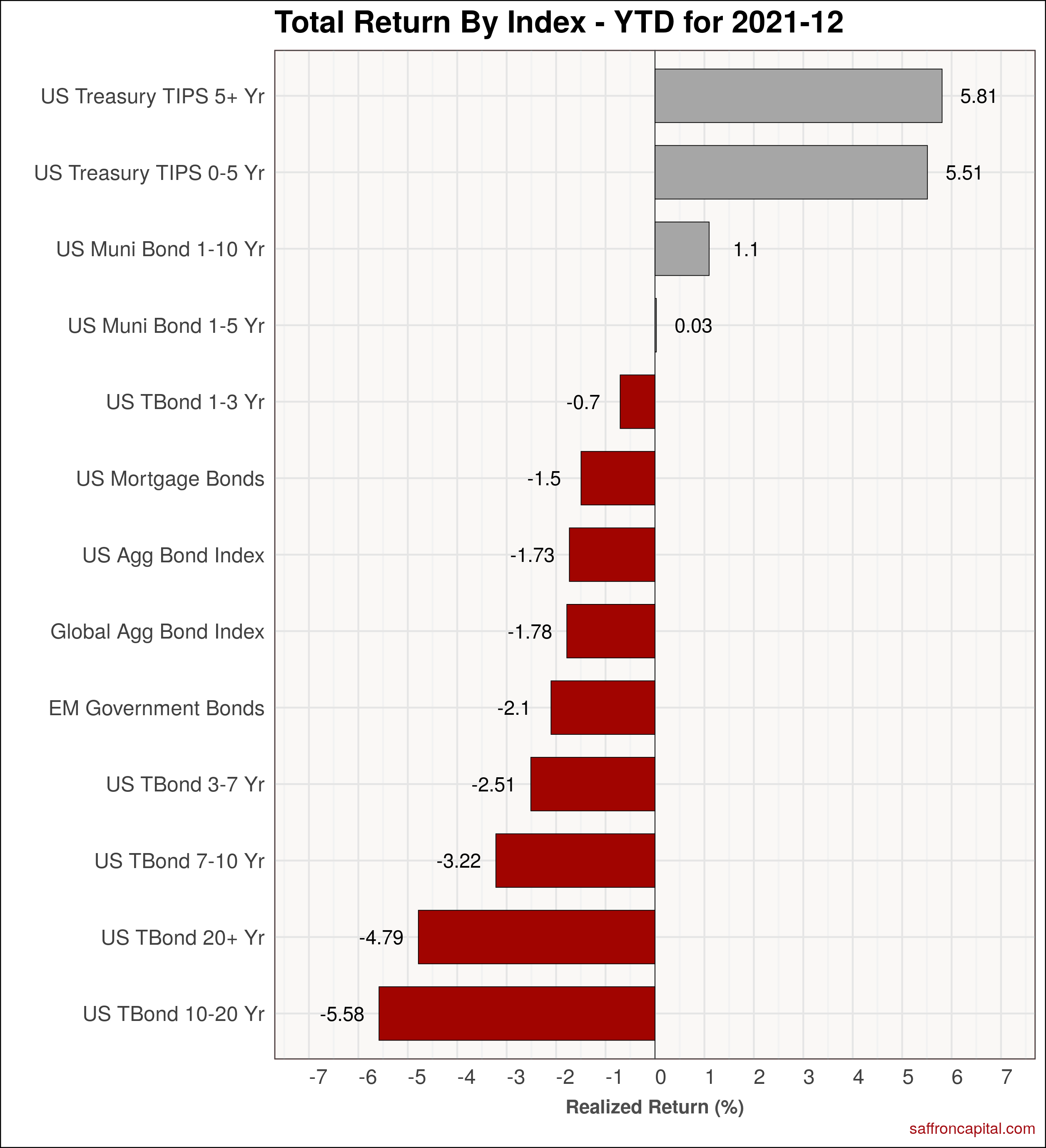

Government Bonds

Total returns for emerging market government bonds (+1.59%) outperformed total returns for the global bond index (-0.47%) and the US aggregate bond index (-0.34). Treasury inflation protected securities also had positive gains (0.51-0.84%) in December.

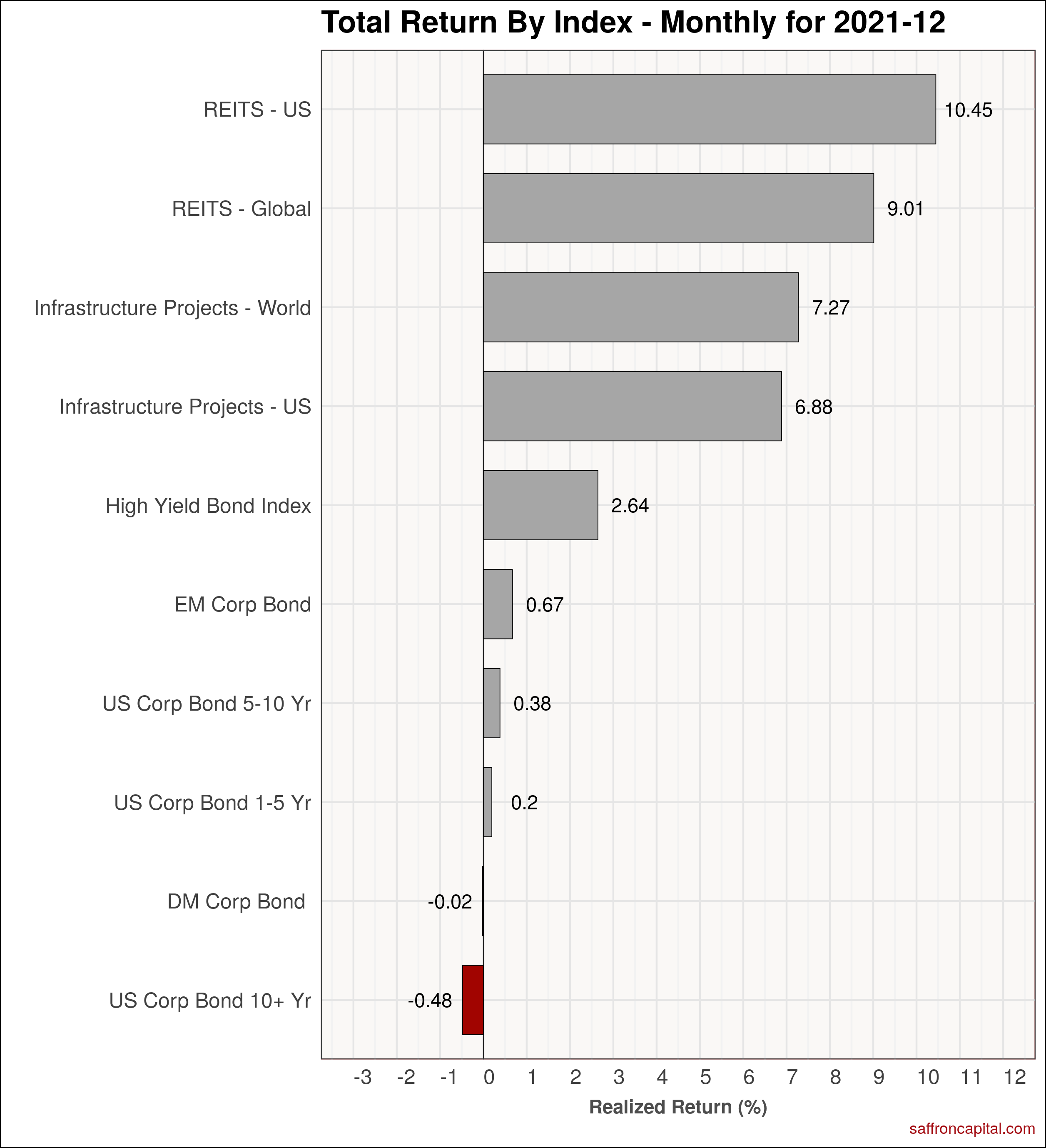

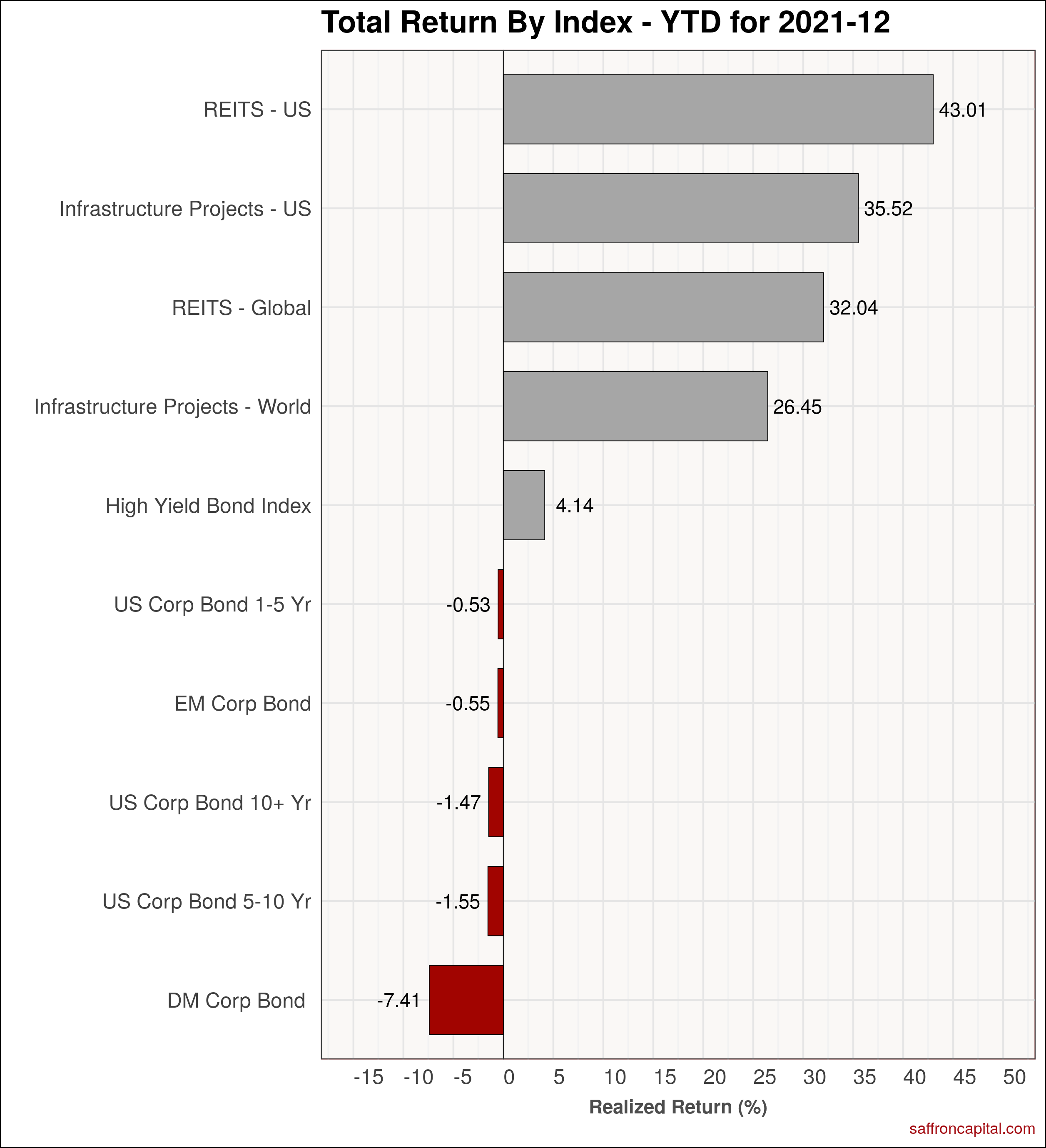

Corporate & Infrastructure Bonds

Returns on REITS (9.01% to 10.45%) and infrastructure project bonds (+6.88 to 7.27%) topped US stocks in December. Meanwhile, high yield corporate bonds (+2.64%) had negative price returns offset by high coupon yields. YTD gains for REITS (+32.04-43.01%) and infrastructure bonds (26.45-35.5%) also outperformed US large cap stocks.

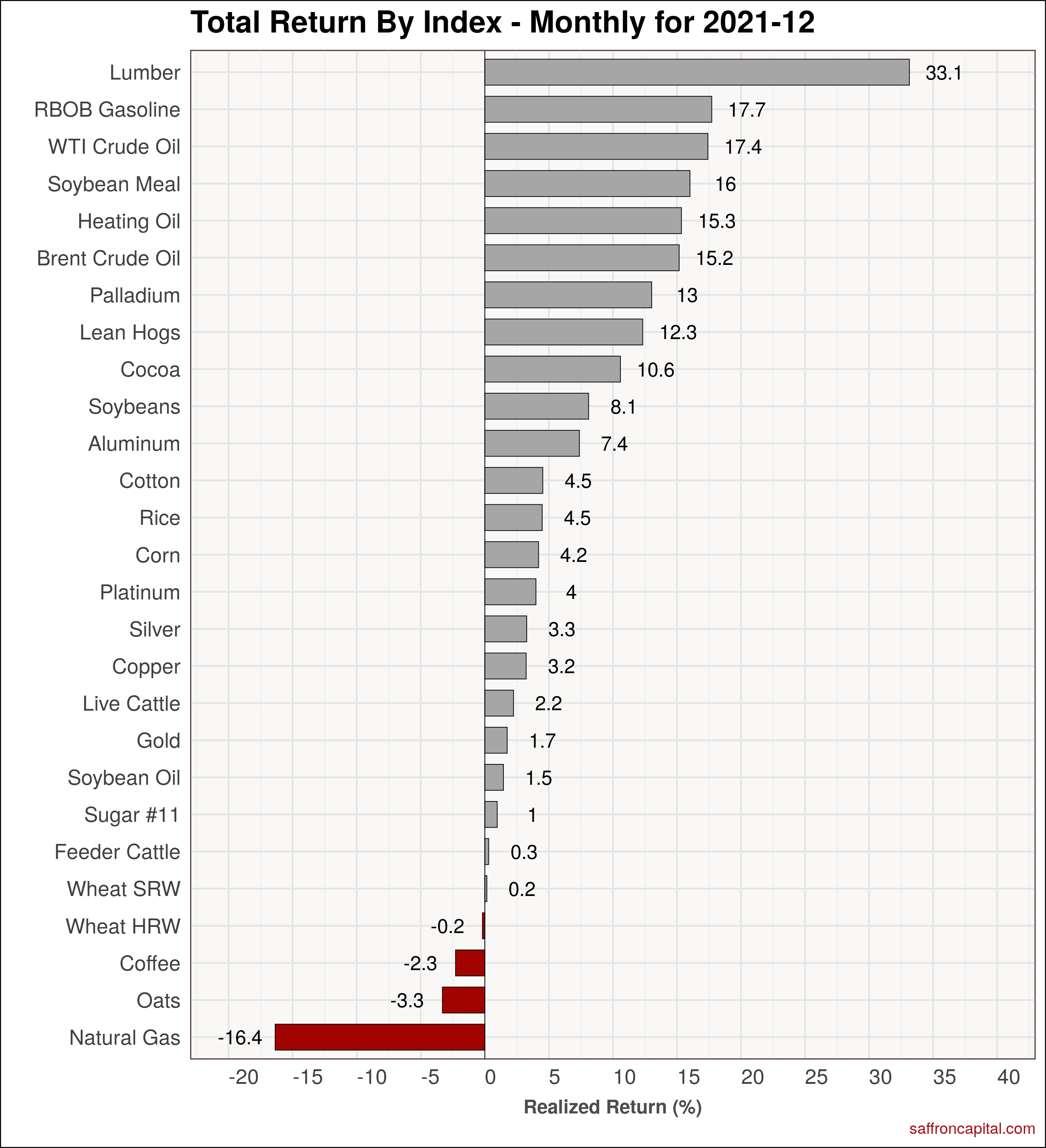

Commodities

Typical of 2021, December commodity returns continued to benefit from low interest rates and inflationary pressures. Lumber (33.1%), gasoline (+17.7%) and WTI crude oil (+17.4%) lead monthly return performance. On a YTD basis, gains were led by oats (+90.3%), coffee (+78.4%) and gasoline (63.1%). Precious metals are notable for negative annual returns (-5.9% to -27.1%).

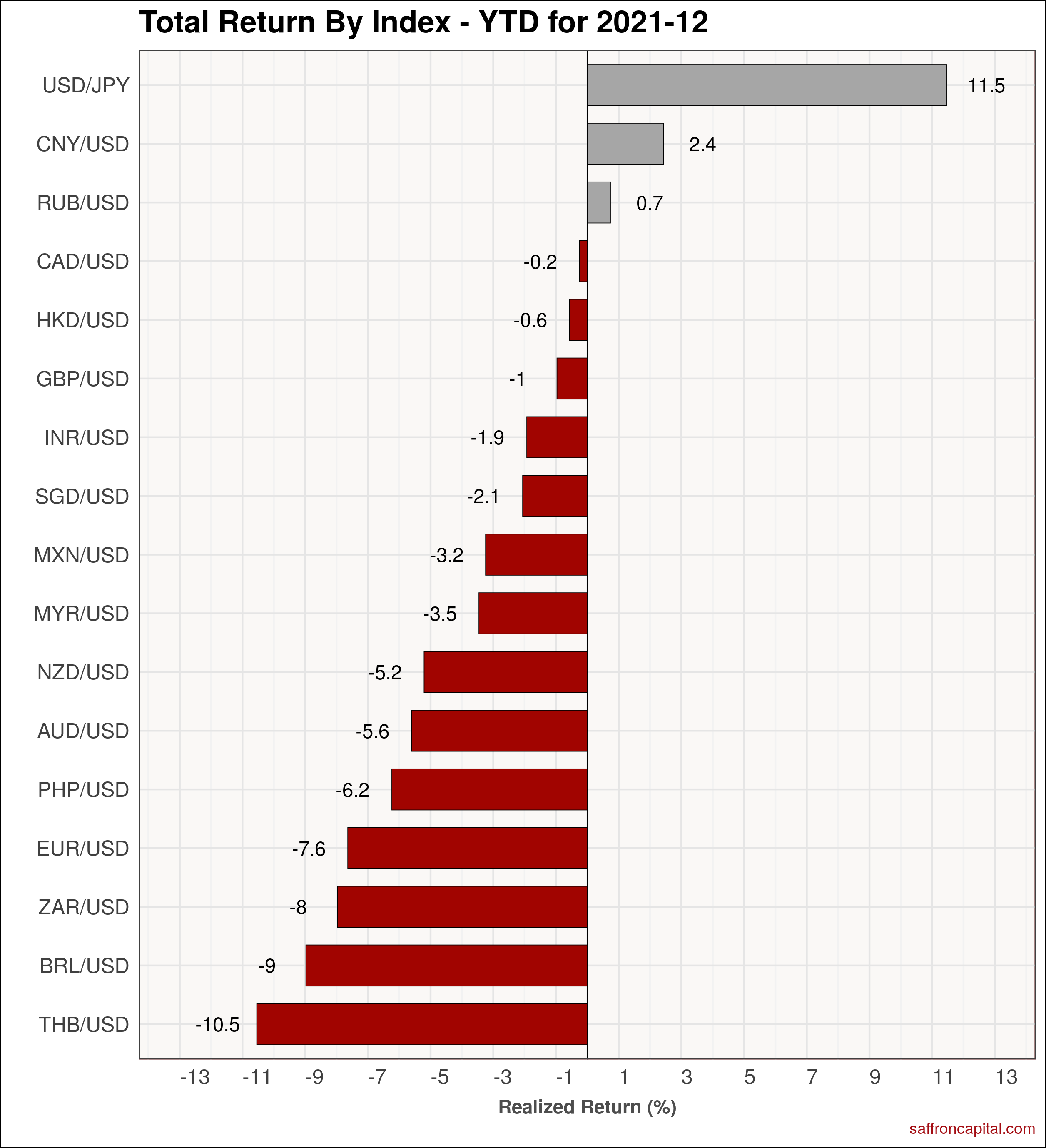

Currencies

The strongest gains for the month were seen in the Mexican Peso (+5.46%), the Aussie dollar (+1.58%) and Pound Sterling (+1.38%). The YTD leaders were the Yen (11.5%), the Chinese Renminbi (+2.4%) and the Russian Ruble (+0.7%).

{kind=link}

{kind=link}

{kind=link}