April returns tell a tale of two markets. Early in the month, a severe market drawdown was triggered by tariff turmoil. Notably, the second half of the month had a relief rally given reduced geopolitical tension and improving corporate earnings. The S&P500 index (-0.8%) ended the month down, marking three consectuive months of losses. In contrast, international Developed Markets (+4.0%) and Gold (+5.8%) remained strong in April.

The following analysis reviews April returns by asset group, sector, and the key factors that drive returns. The aim of the visual summary is to help investors to identify new opportunities and to benchmark returns for your portfolio.

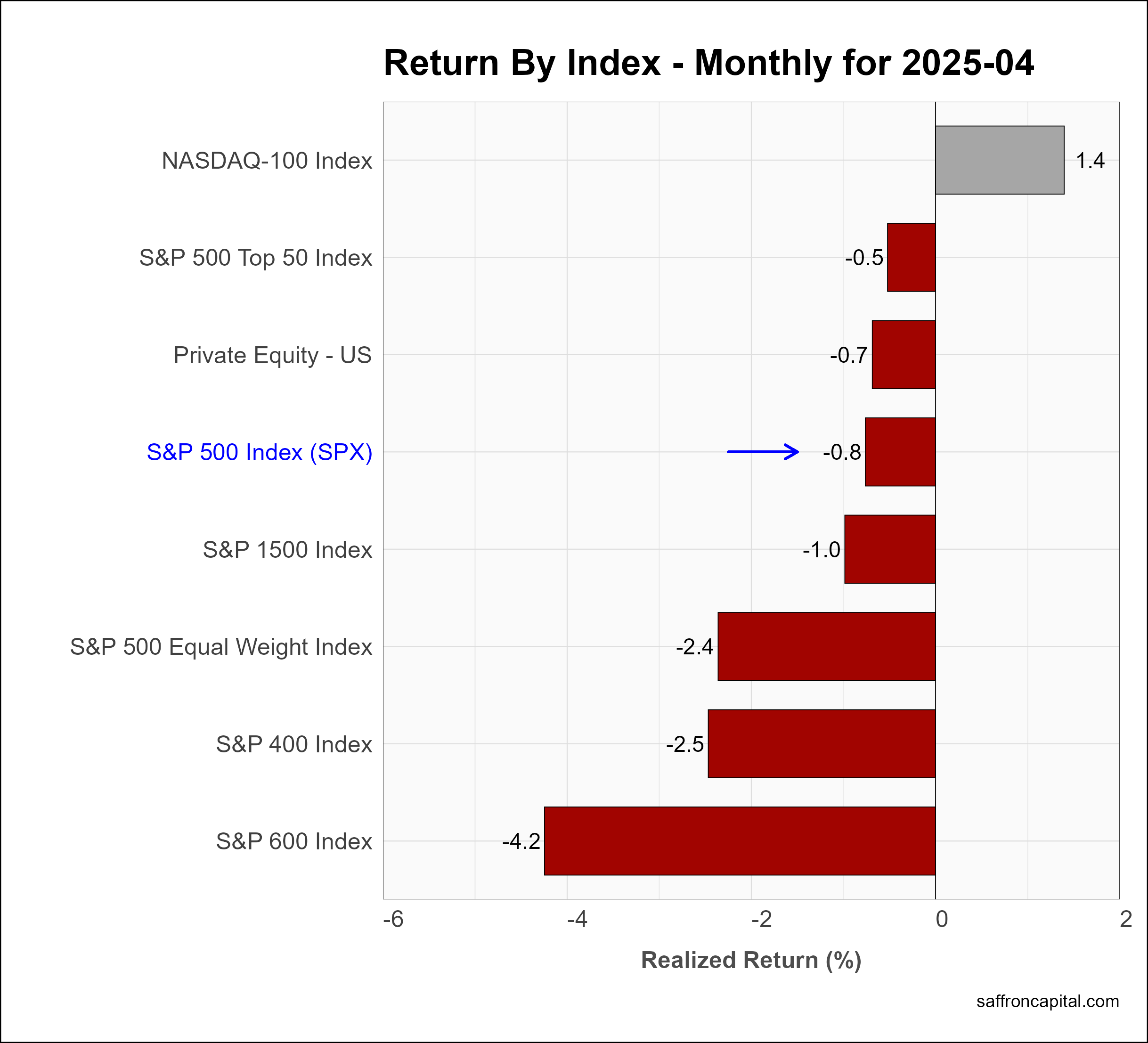

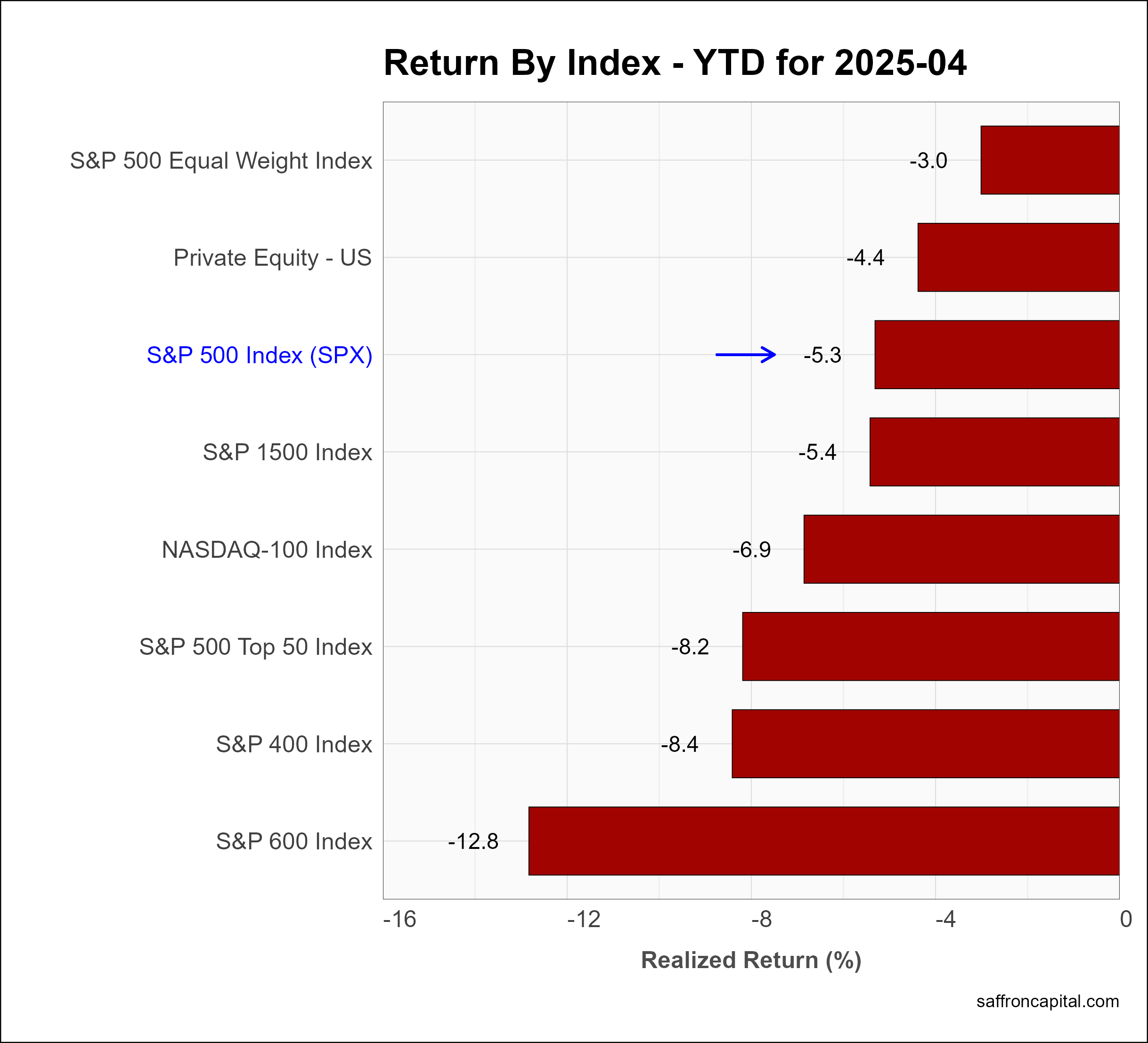

Core US Indices

Core indices posted mixed results in April. Gains in the technology-heavy NASDAQ index (+1.4%) were the exception as all the major indices ended the month in the red. The top 50 index (-0.5%) easily outperformed the S&P 500 Equal Weight index (-2.4%) as fund flows gravitated to large caps. Meanwhile, small cap stocks (-4.2%) proved to be the most vulnerbale to tariff induced weakness given their more domestic focus. Year-date, the S&P 500 index (-5.3%) is outperforming the NASDAQ( -6.9%), mid-cap shares (-8.4%) and small caps (-12.8%).

Click to enlarge

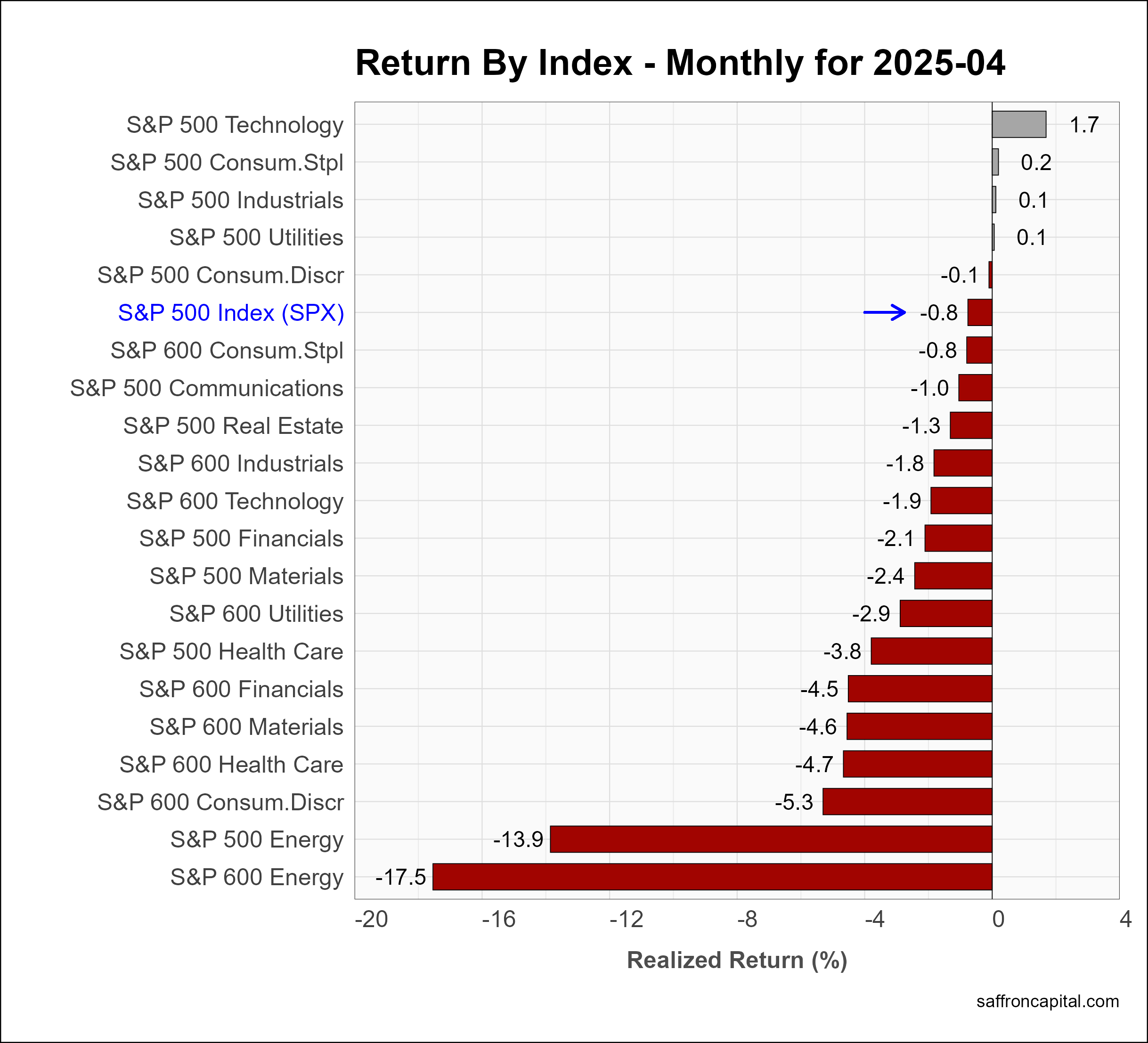

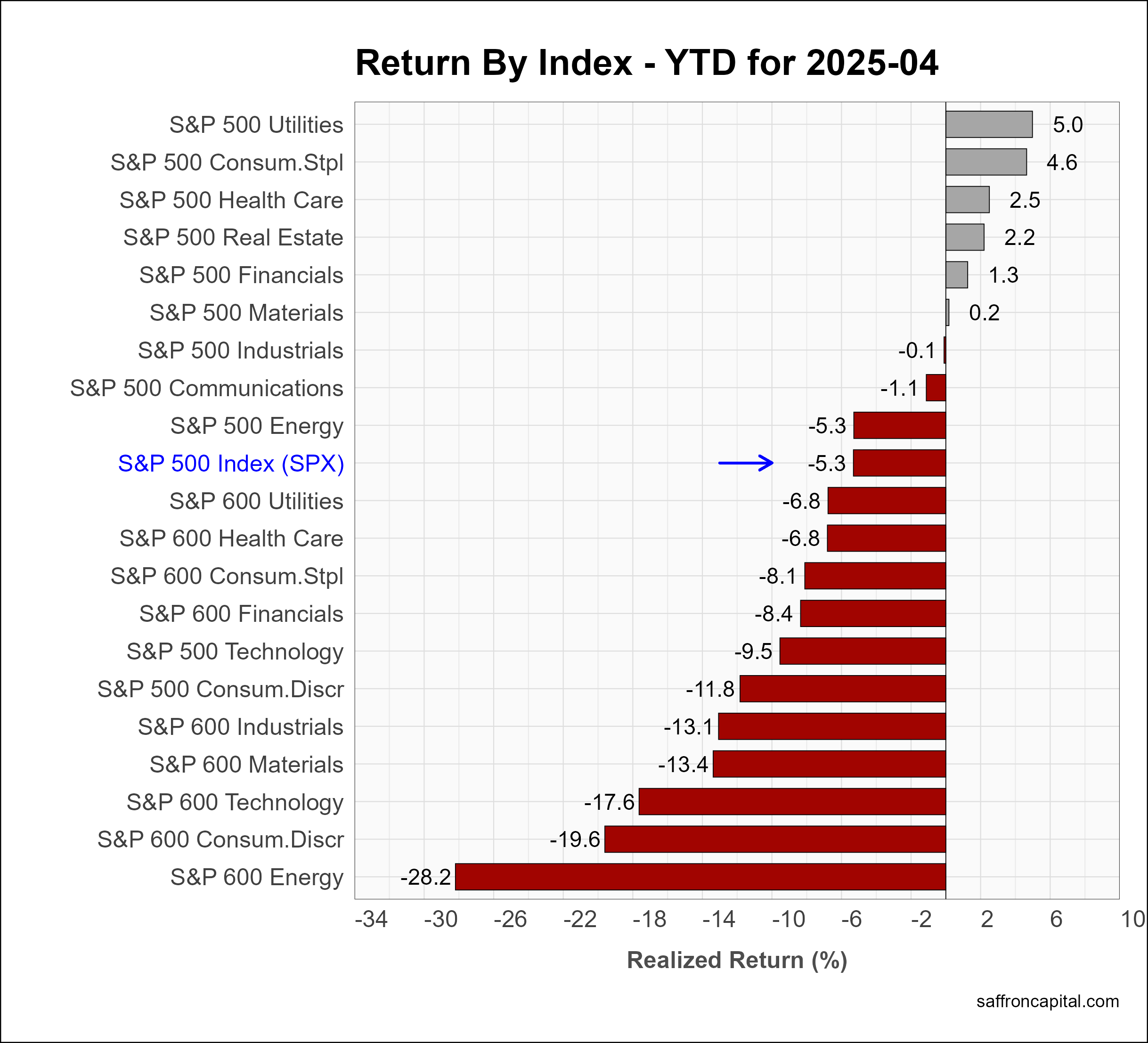

US Sector Indices

April returns by sector were mixed, but a rotation was evident compared to Q1, with Information Technology (+1.7%) in the lead and Energy (-17.5%) presenting the worse of the sector losses. Consumer Staples (+0.2%) stayed positive in APril, as did Industrials (+0.1%) and Utilities (+0.1%). Defensive sectors also lead the year-to-date results with Utilities (+5.0%), Staples (+4.6%), and Health Care (+2.5%) in the lead. Energy (-28.2%) is performing badly as is Information Technology (-9.5%).

Click to enlarge

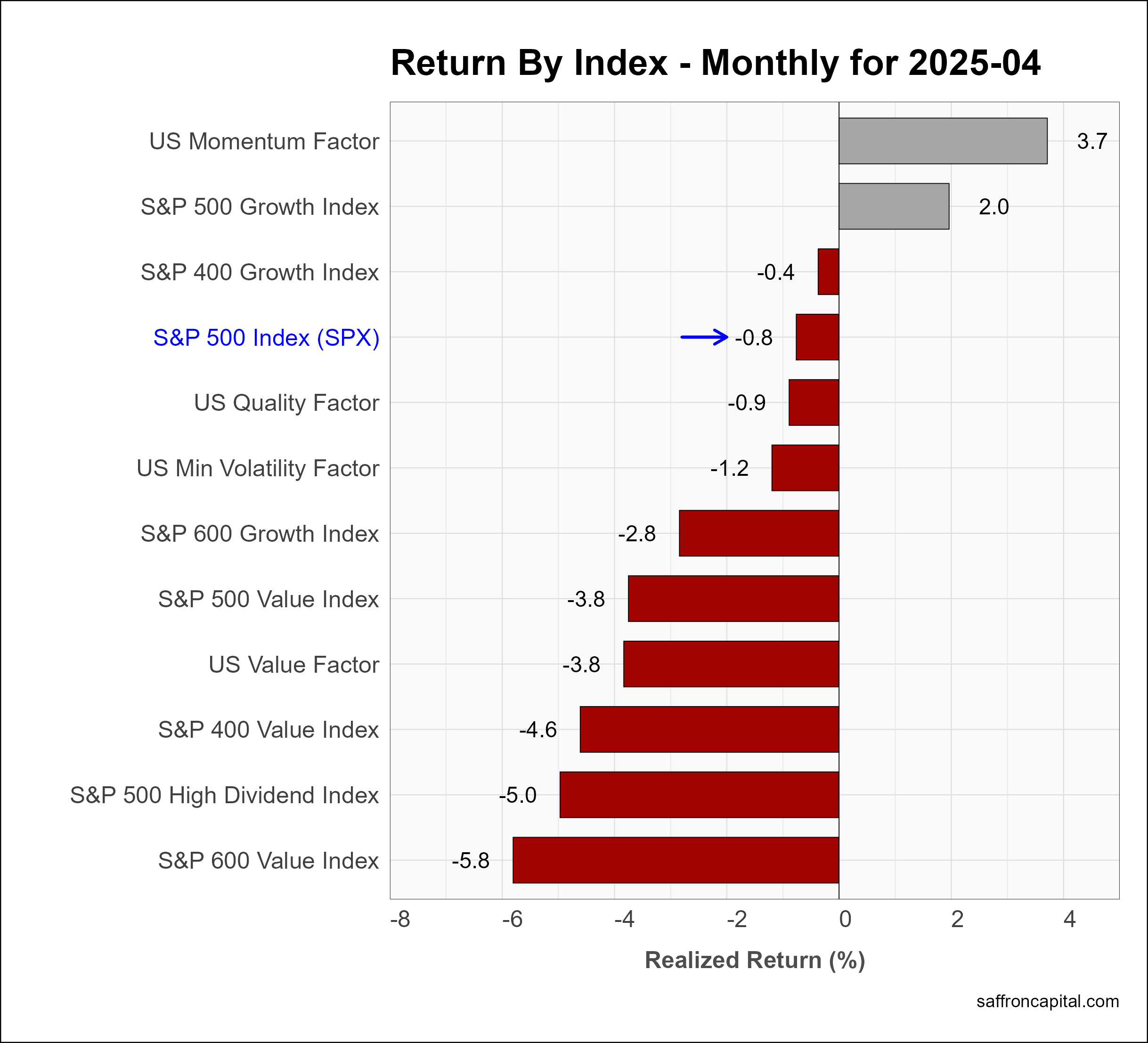

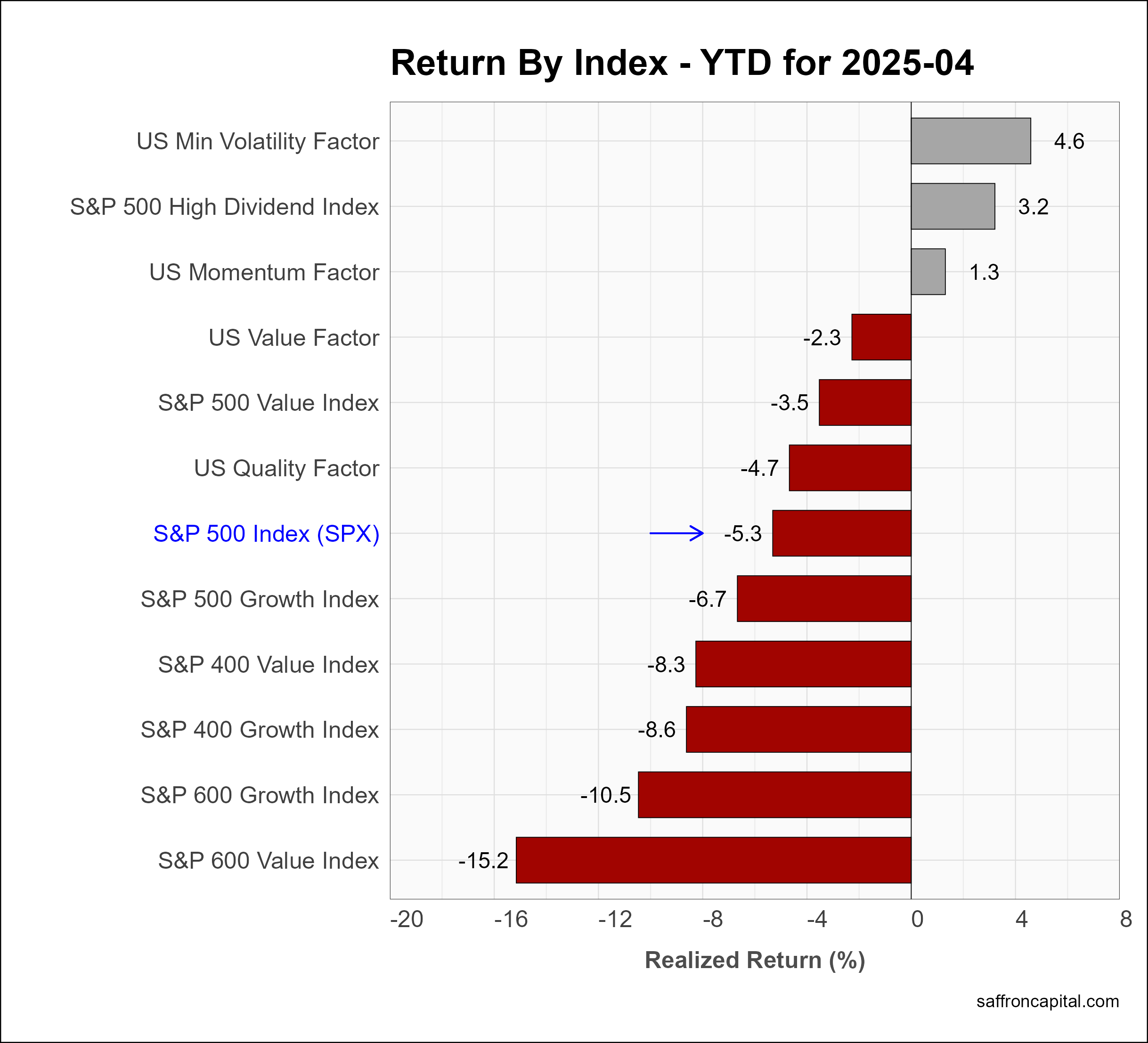

US Factor Indices

Factor portfolios are constructed to emphasize the core drivers behind returns, which include company size, relative value, profitability, growth, and momentum. Multi-factor portfolios combine two or more factors. In contrast to Q1, April returns marked a shift away from defensive factor indices, with Momentum (+3.7%) and Growth (+2.00%) both outperforming the core US indices. The high Dividend index (-5.0%) saw the heaviest selling as did small cap value (-5.8%). Since January, defensive factors continue to lead with US Minimum Volatility (+4.8%) being the strongest of the portfolios.

Click to enlarge

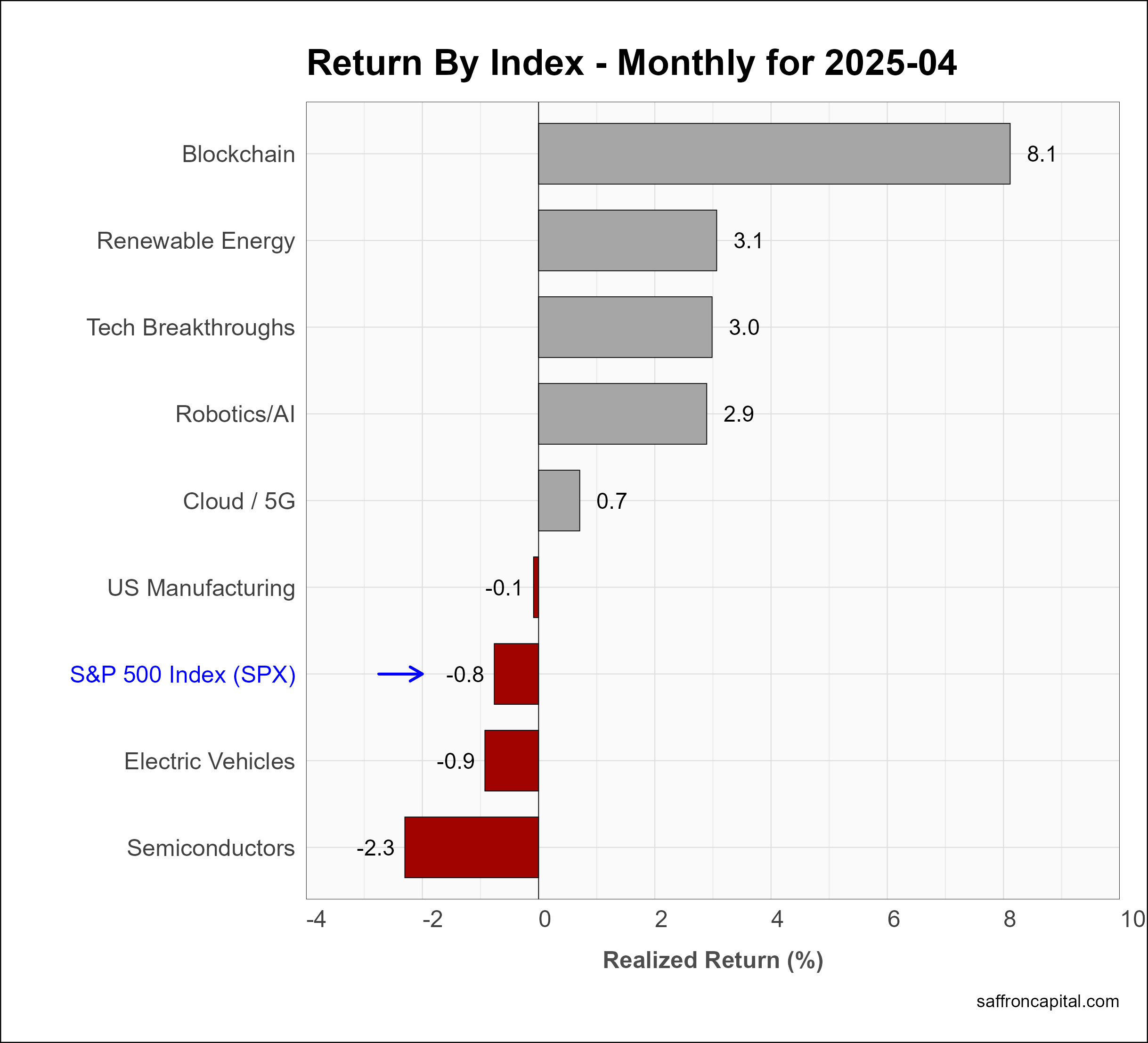

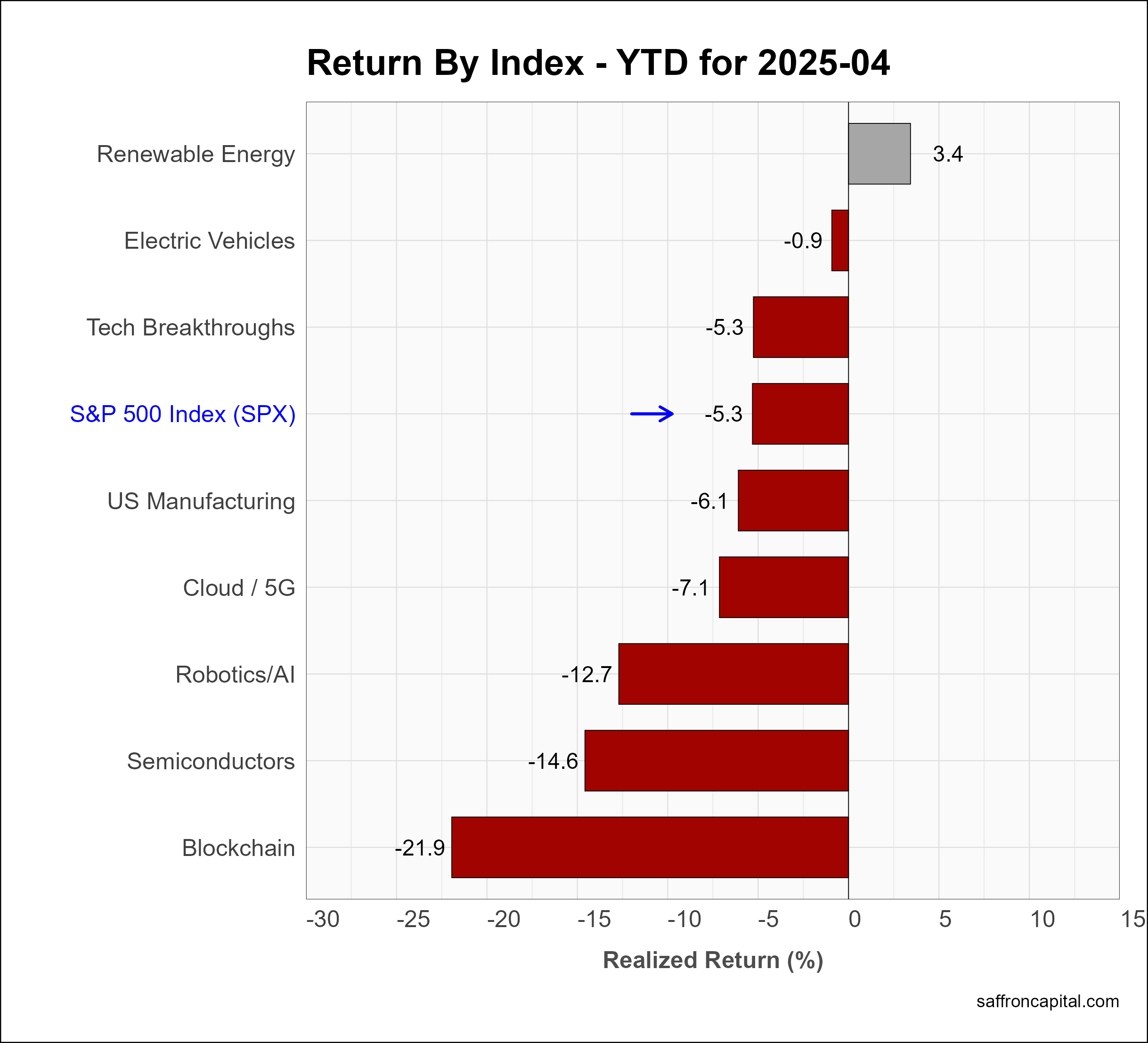

US Thematic Portfolios

US thematic portfolios are megatrend growth portfolios that seek to capture the primary growth trends of the U.S. economy. April returns were led by Blockchain shares (+8.1%), Renewable Energy (+3.1%), Tech Breakthroughs (+3.0), and Robotics/AI (+2.9%). Electric Vehicles (-0.9%) and Semiconductors (-2.3%) were down for the month. Year-to-date, Renewable Energy (+3.4%) has emerged as top portfolio. It is interesting to note that US manufacturing (-6.1%) is yet to benefit from the initiatives of the new administration. Finally, blockchain shares (-21.9%)

Click to enlarge

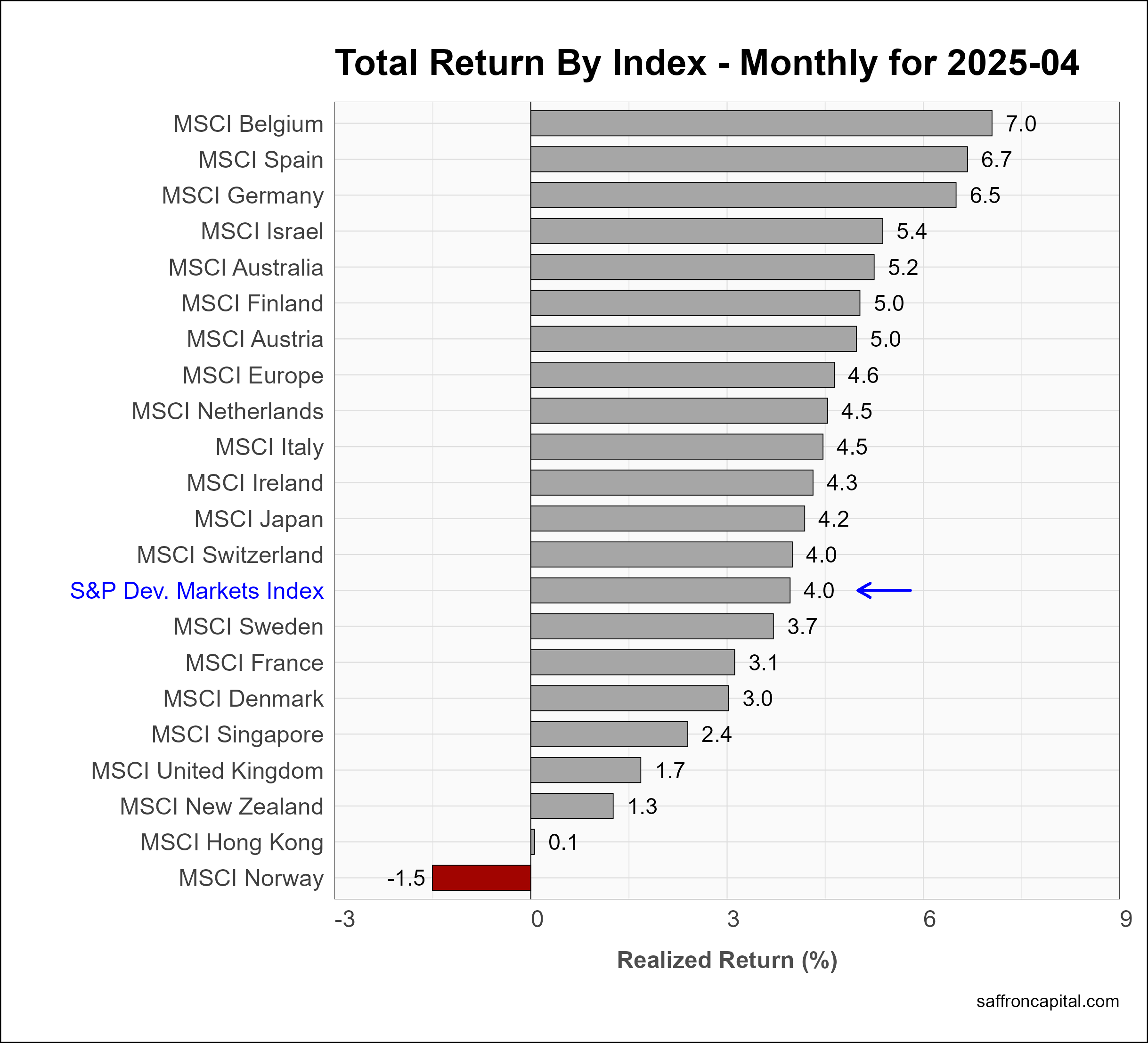

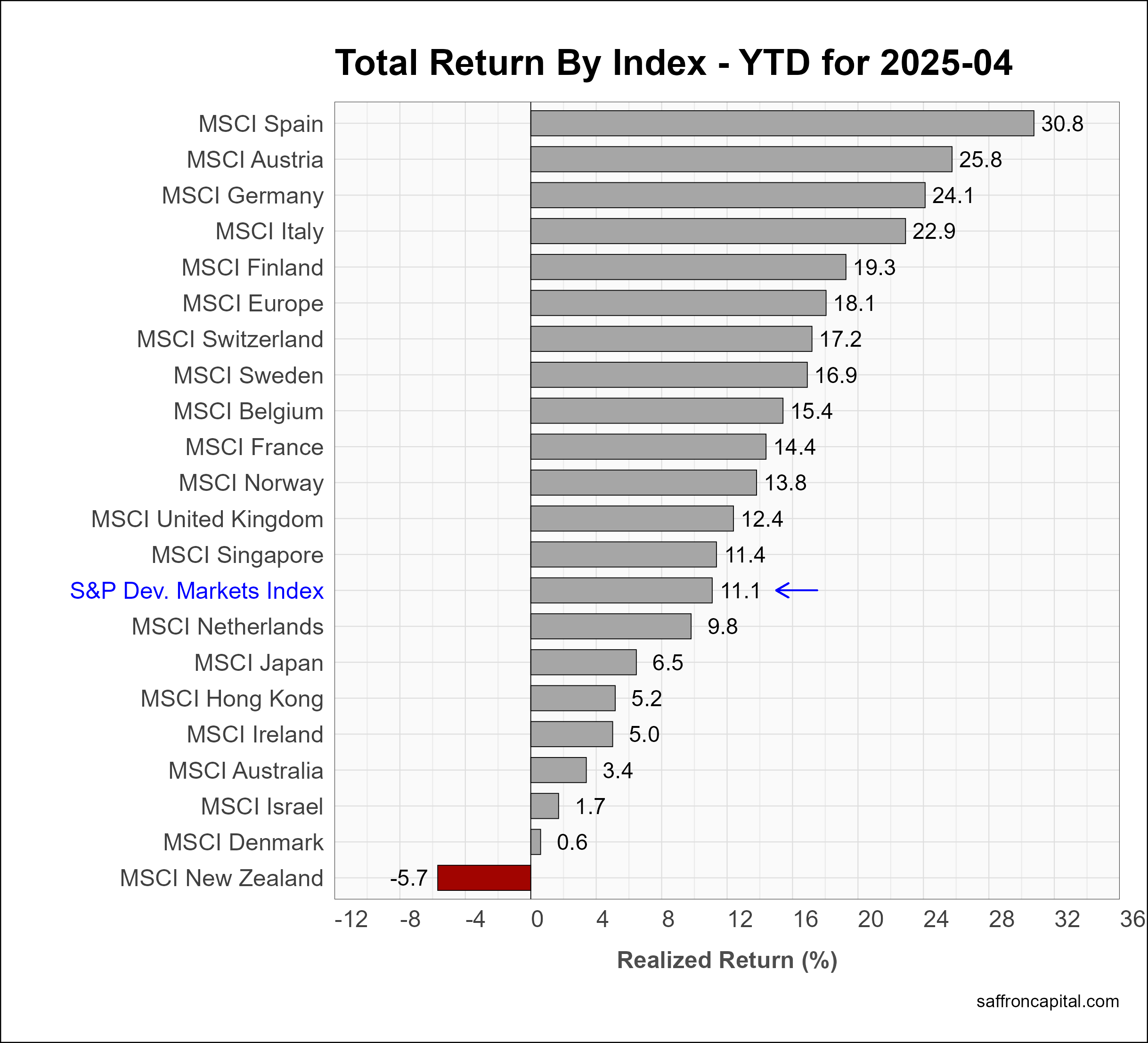

Developed Market Equities

International Developed Markets index (+4.0%) led equity returns in April. The MSCI Europe index (+4.6%) again outperformed the US, with Belgium (+7.0%), Spain (+6.7%), and Germany (+6.5%) topping the list. Typically, when international shares outperform the US in the first quarter, they tend to outperform over the entire year. Since December, the Developed markets index (+11.1%) is significantly ahead of the US, led by Spain (+30.8%), Austria (+25.8%), and Germany (+24.1%).

Click to enlarge

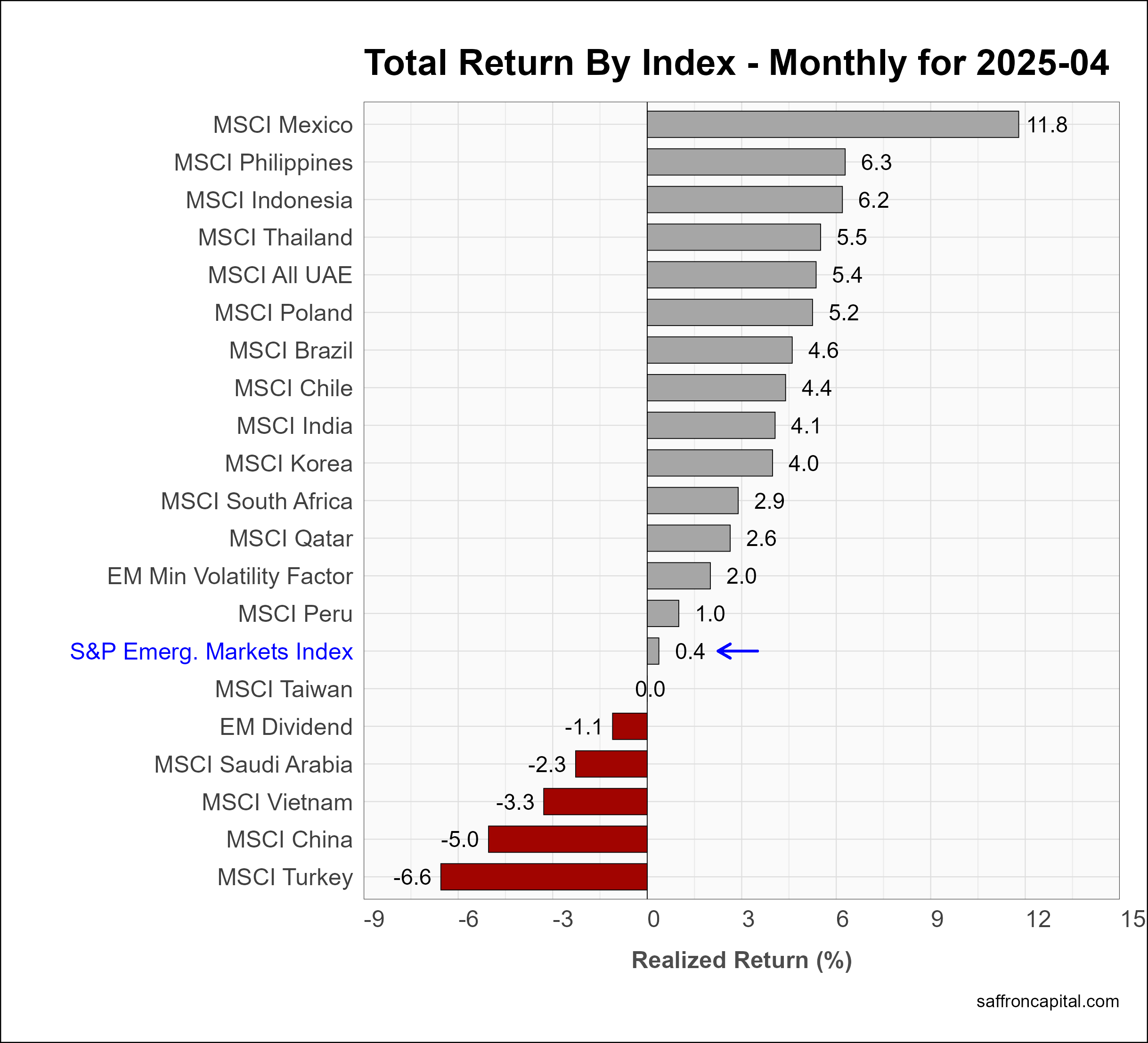

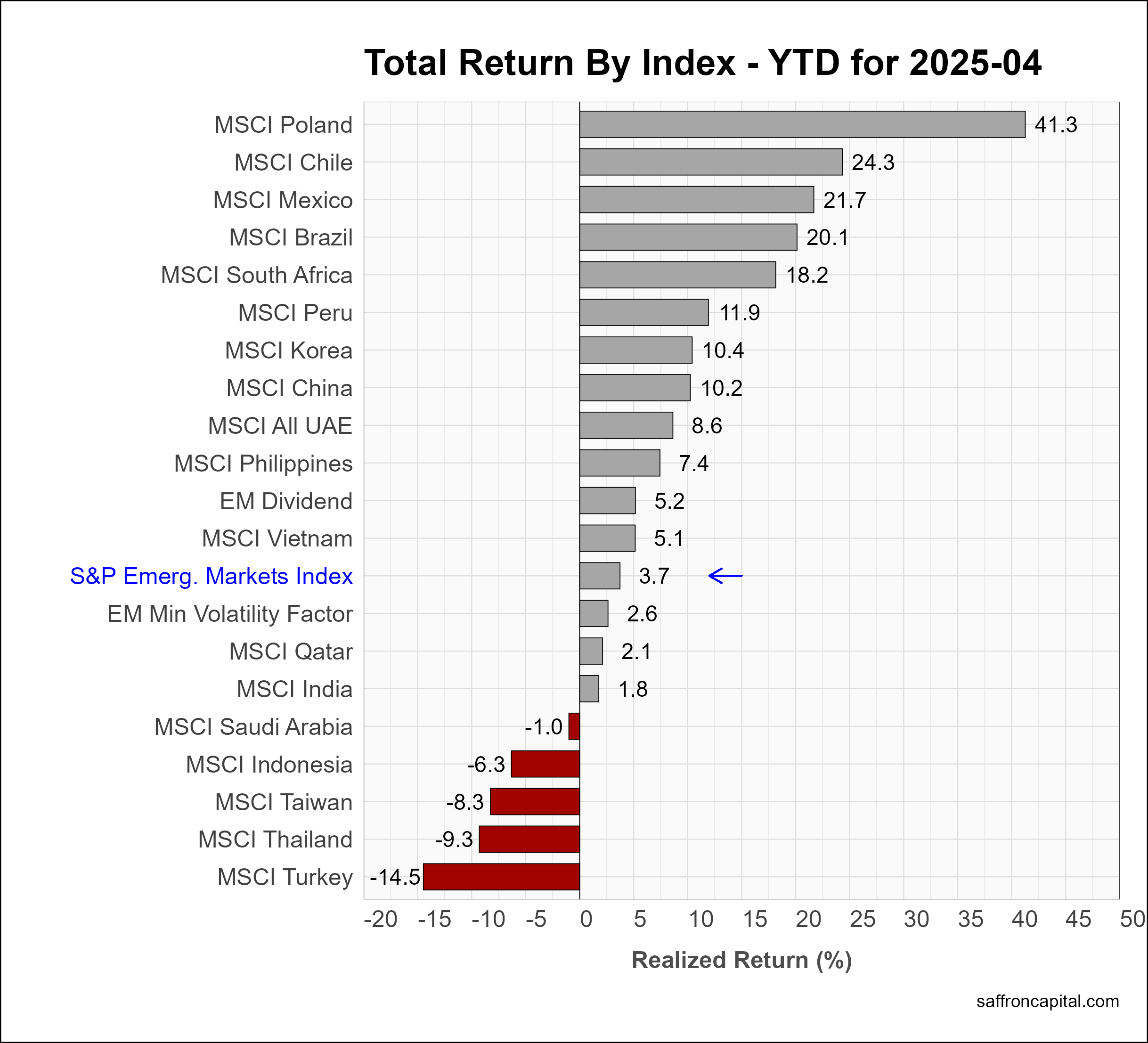

Emerging Market Equities

The S&P Emerging Markets Index (+0.4%) was essentially flat but did well versus U.S. benchmarks. Mexico (+11.8%), the Phillippines (+6.3%), and Indonesia (+6.2%) had the best returns in April. China (-5.7%) comes in close to the bottom of the pack, while India (+4.1%) and Korea (+4.0%) are beat the group indix. Year-to-date, Poland (+41.3%) continues to lead the group.

Click to enlarge

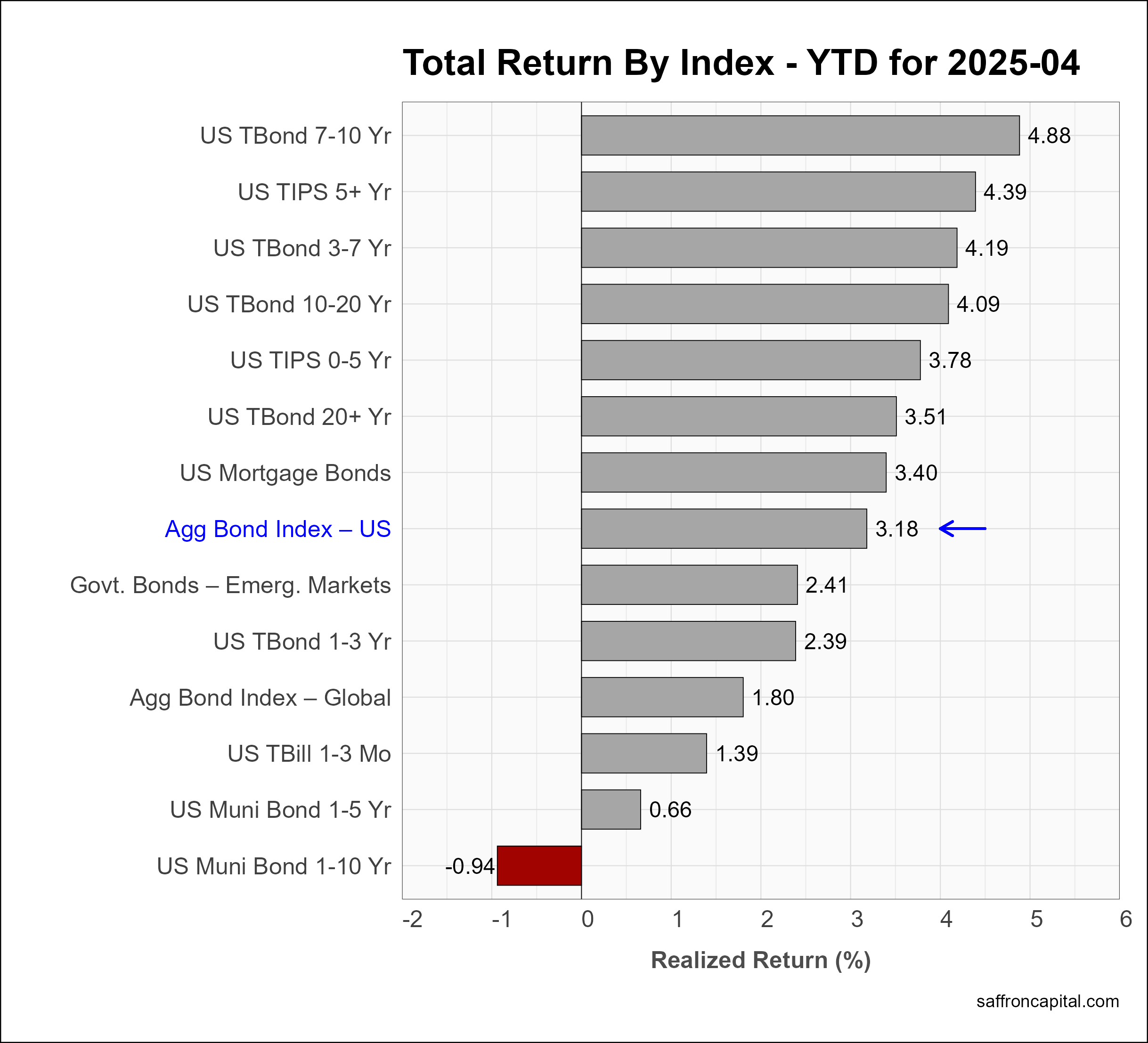

Government Bonds

During April, the yield-to-maturity on the 10-year Treasury Note spiked dramatically from 3.9% to 4.6%, before settling at 4.1%. As a result, the US Aggregate Bond Index (+0.43%) had modest gains. At the same time, long duration bonds (-1.36%) suffered from the yield spike. However, the Global Aggregate Bond Index (+1.665) did much better. Year-to-date, the Aggregate Bond Index (3.16%) continues to outperform equities.

Click to enlarge

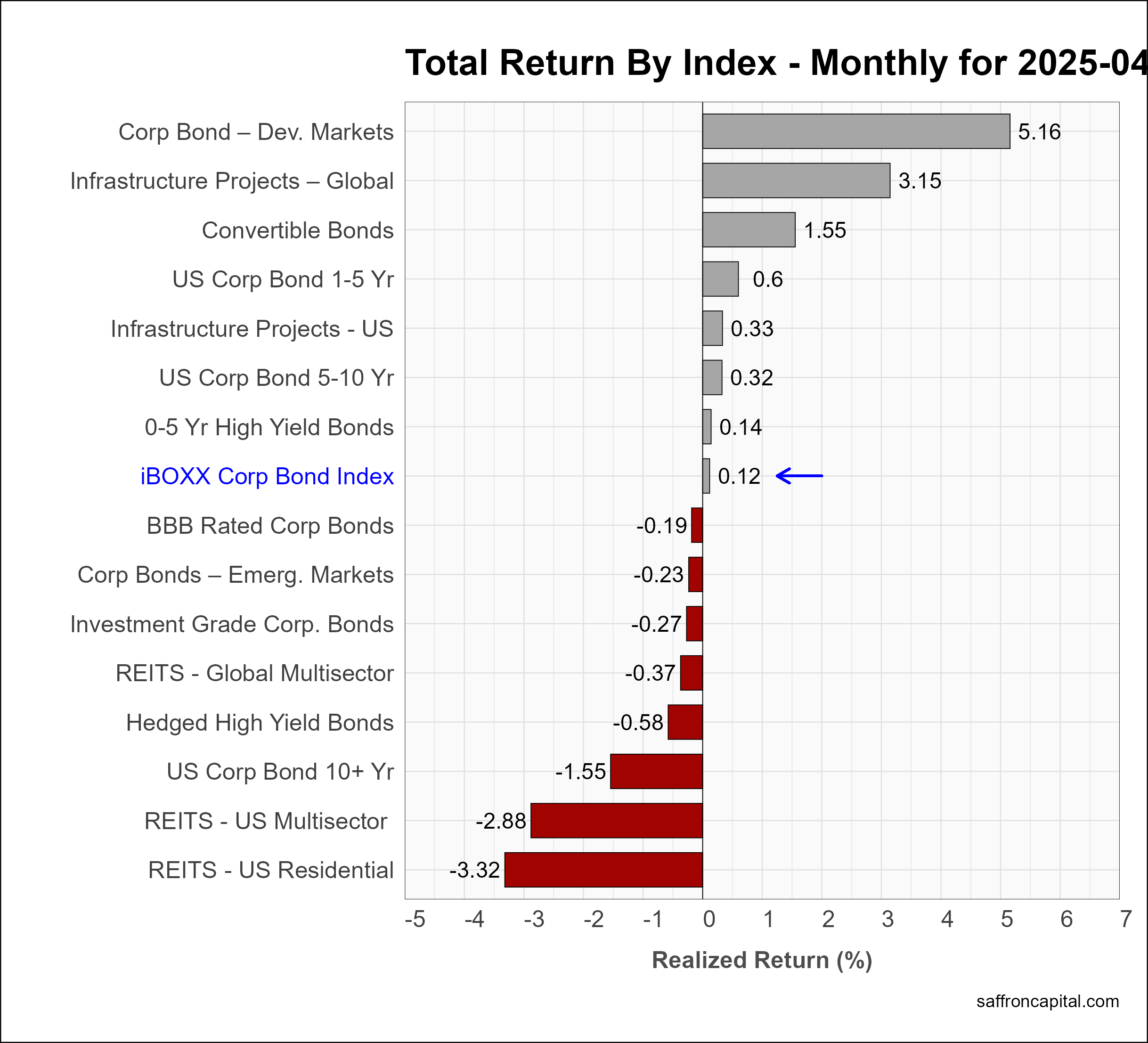

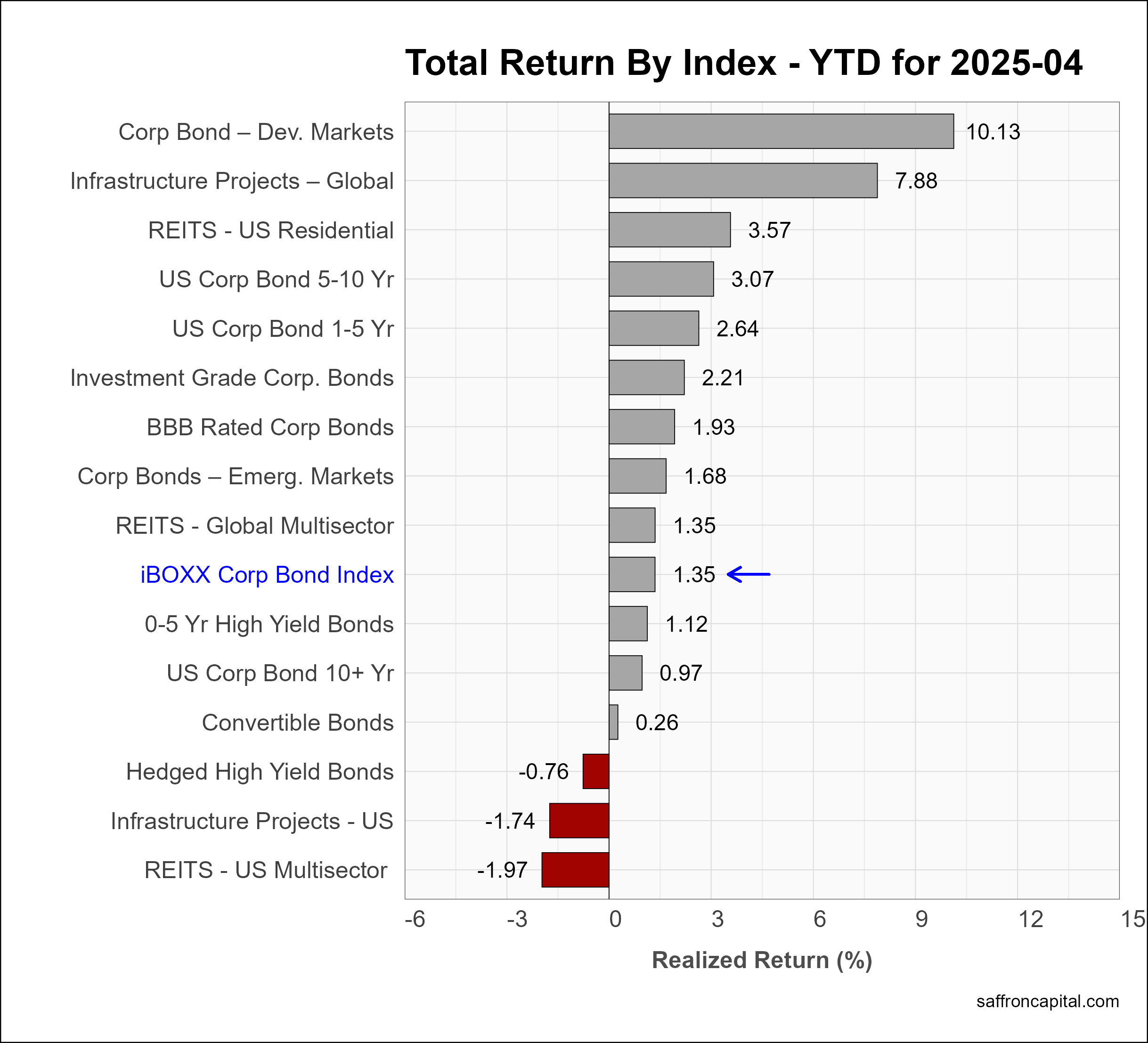

Corporate & Infrastructure Bonds

The iBoxx Corporate Bond Index (+0.12%) was essentially unchanged in April, and again lagged behind the government bond benchmark. Developed market corporate bonds (+5.16%) has solid gains, as did Global infrastructure project bonds (+3.15%). US REITS (-2.9% to -3.3%) trailed the sector. Year-to-date, the iBOXX Corporate Bond Index (+1.35%) remains below the high for the year but continues to outperform US equities. Developed market corporate bonds have generated a total return of +10.13% since the start of the year.

Click to enlarge

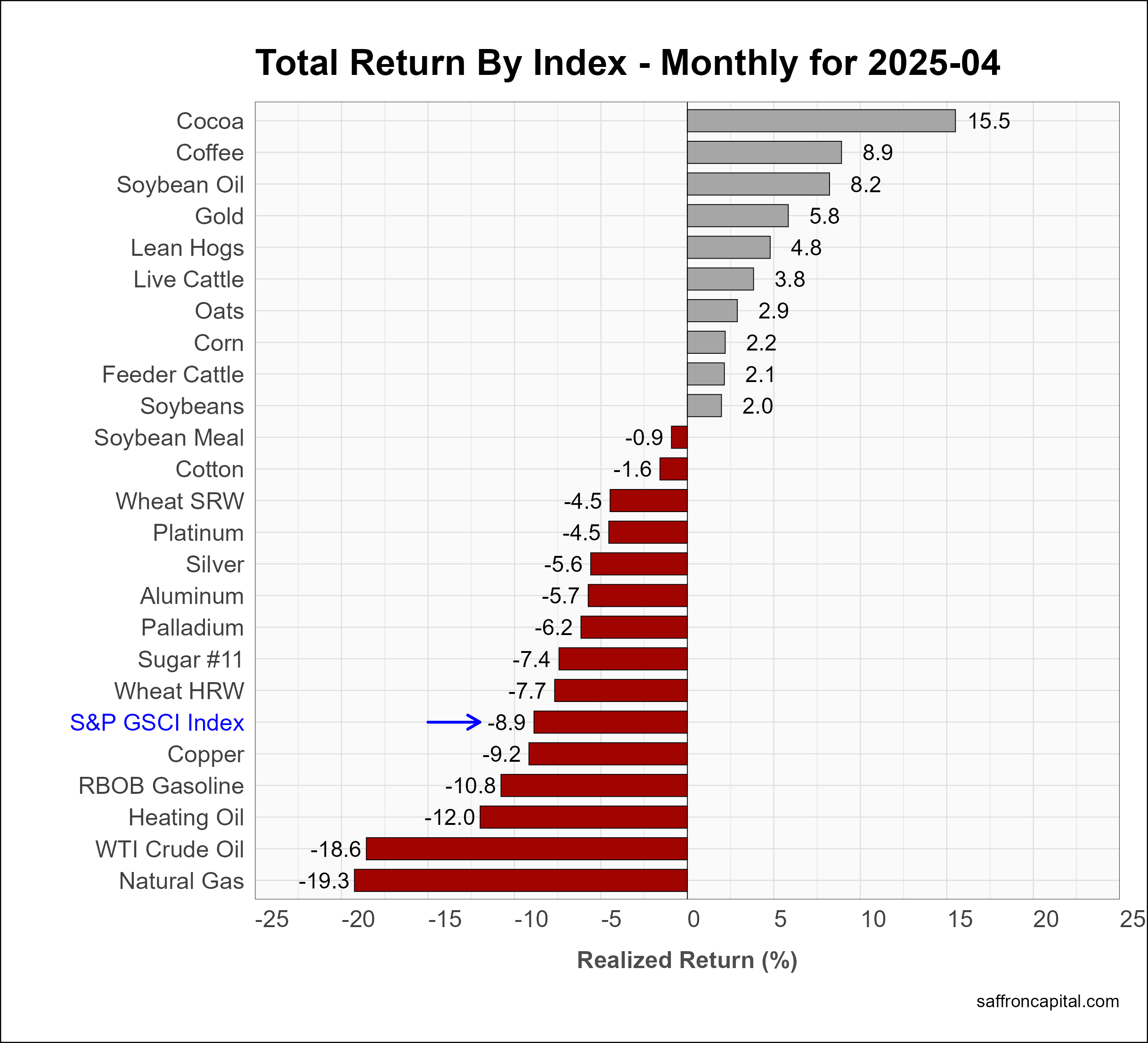

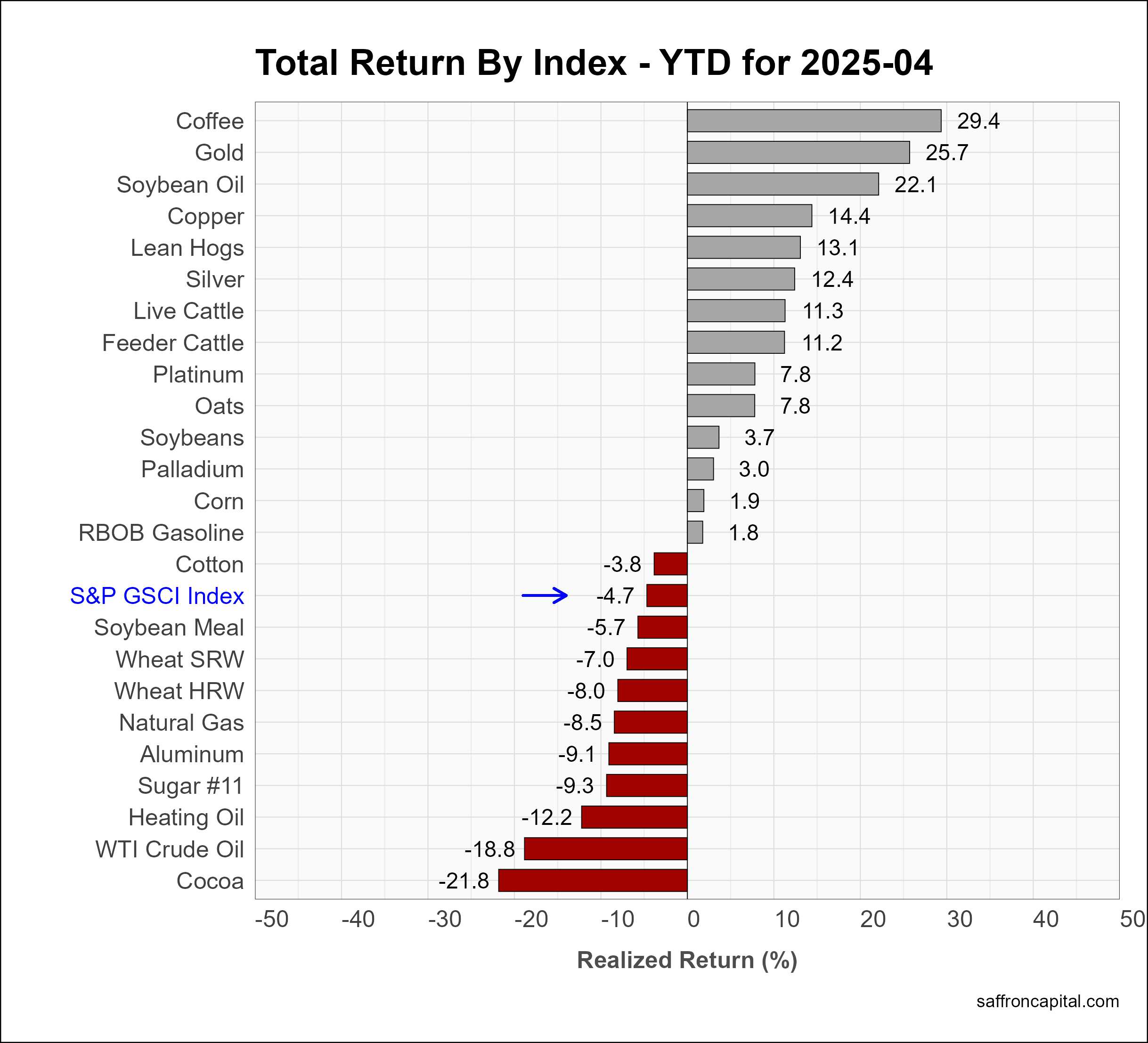

Commodities

Commodities, as measured by S&P GS Commodity Index (-8.9%) had their worse month of the year in April with energy products (-10.8% to -19.3%) experiencing the largest losses. Cocoa (+15.5%) continues to suffer from limited p[roduction, while Gold (+5.8%) turned in solid performance relative to stocks and bonds. Year-to-date, the commodity index (-4.7%) remains under pressure with Coffee (+29.4%), Gold (+25.7%), and Soybean Oil (+22.1%) leading the way.

Click to enlarge

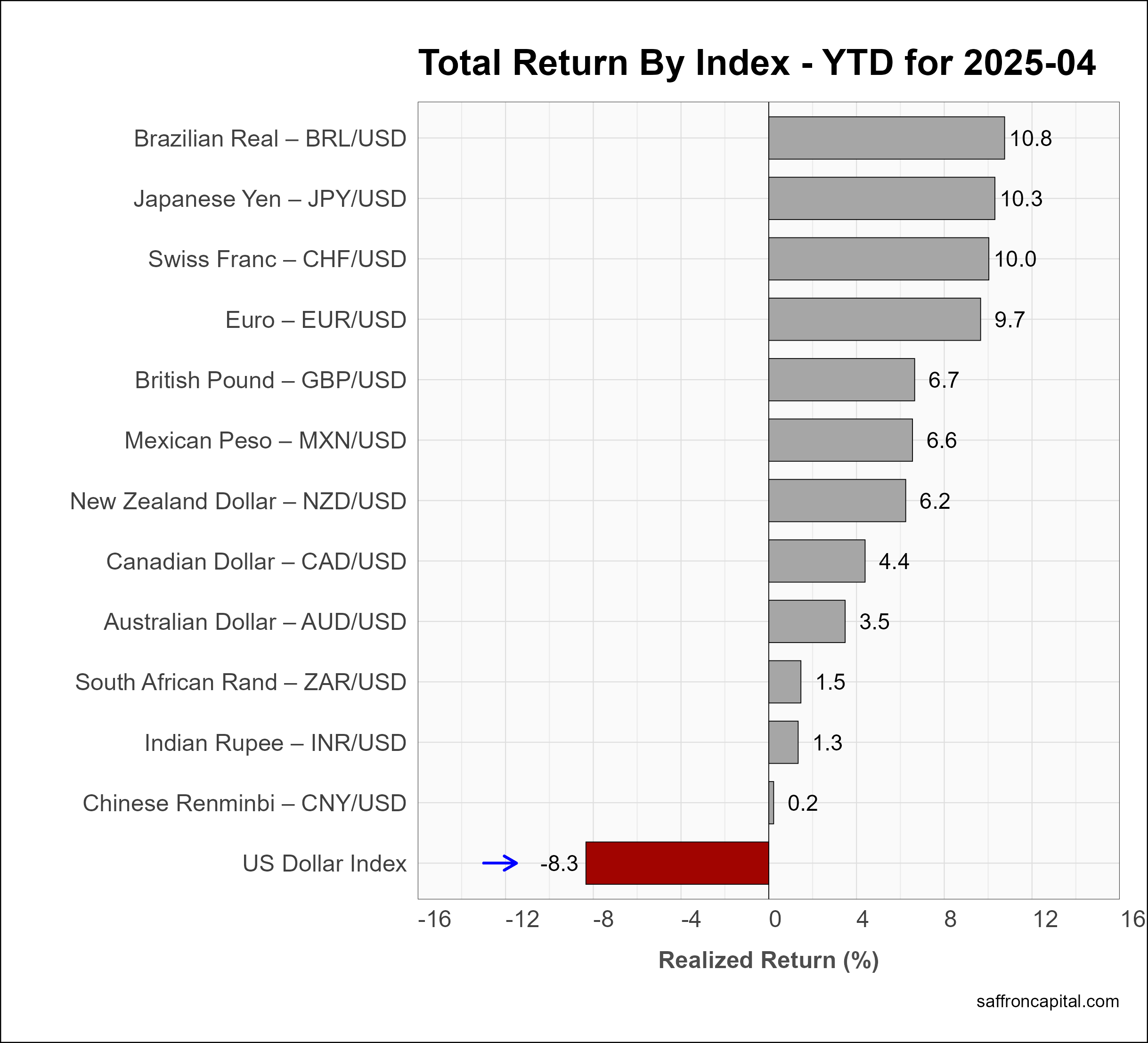

Currencies

The U.S. Dollar index (-4.4%) fell in April with the Swiss Franc (+7.1%) benefiting from safe haven investing. The Yesn (+5.2%) and the Euro (+5.0%) were also strong, while Chinese Renminbi (-0.2) was down slightly. The US Dollar is now down -8.3% since the start of the year.

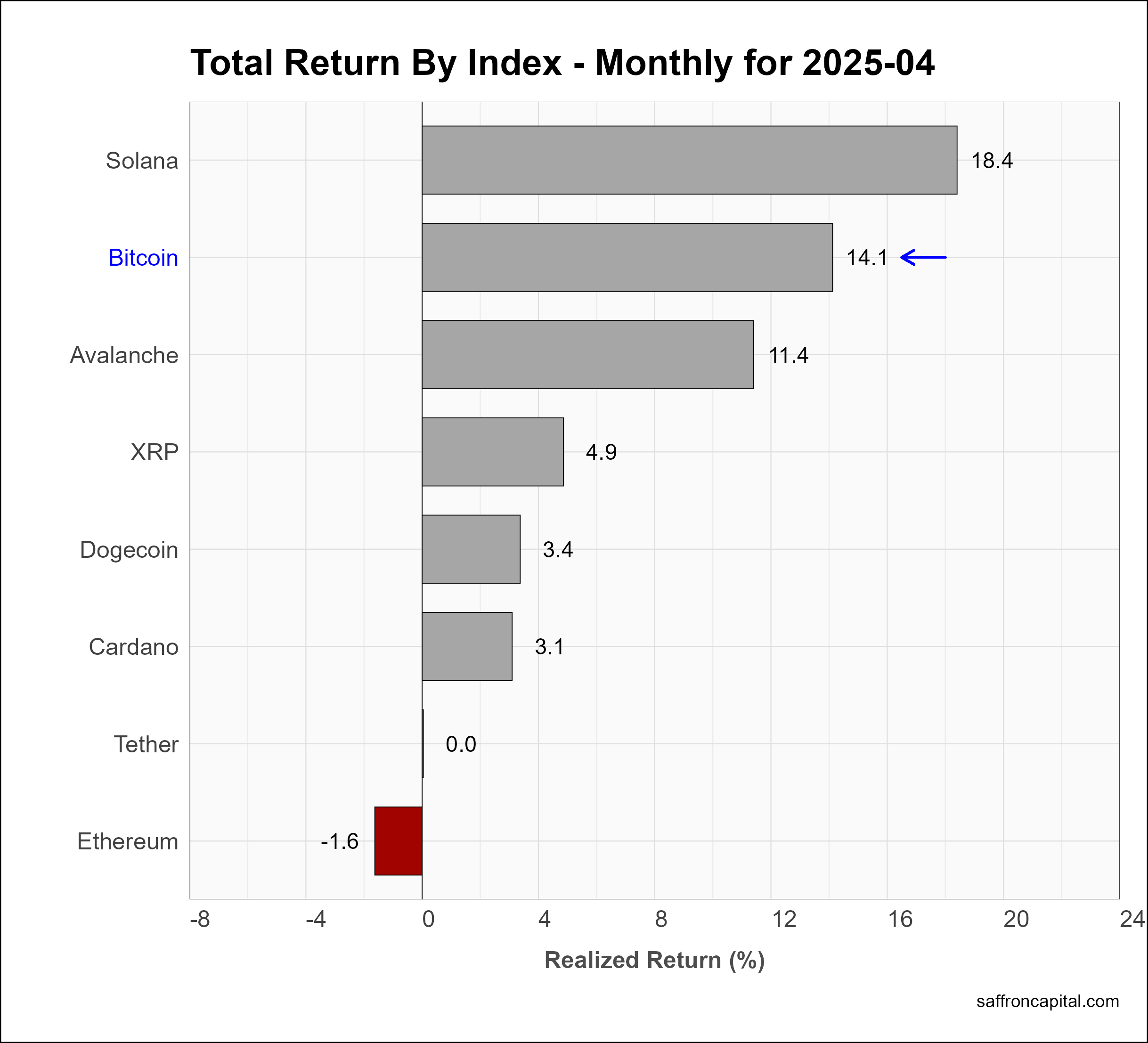

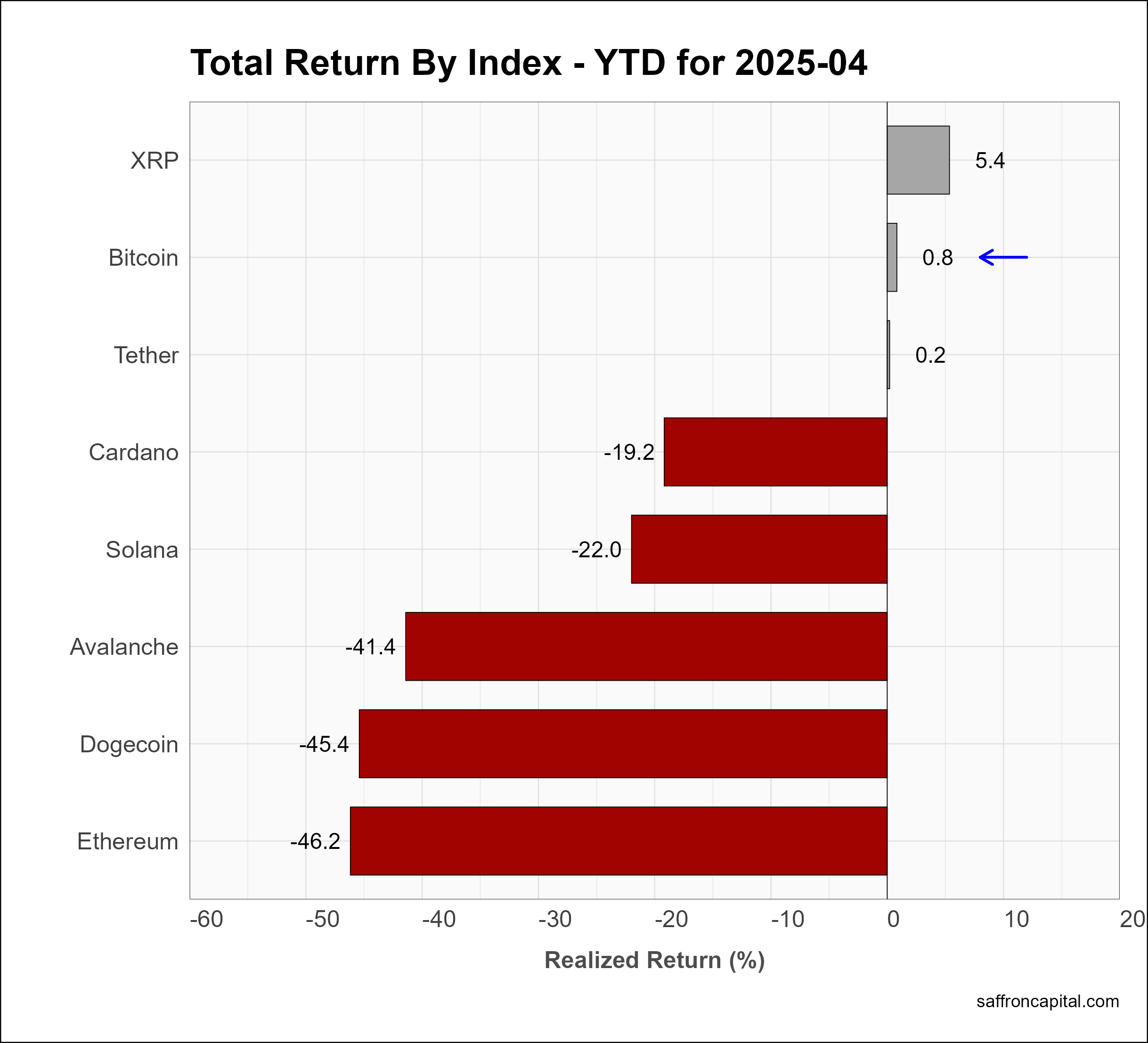

Cryptocurrencies

Cryptocurrencies had positive gains in April with benchmark Bitcoin (+14.1%) up significantly. Since January, Bitcoin (+0.8%) is up only modestly, while many alt coins remain down significantly.

Click to enlarge

Have questions or concerns about the performance of your portfolio? Could you benefit from a capital preservation strategy or a custom portfolio formulation that better aligns to your risk appetite? Whatever your needs, we are here to listen and to help. Contact us to schedule a meeting.

Saffron Capital LLC is a registered investment advisor that is employee-owned and Minnesota-based.

{kind=link}

{kind=link}

{kind=link}