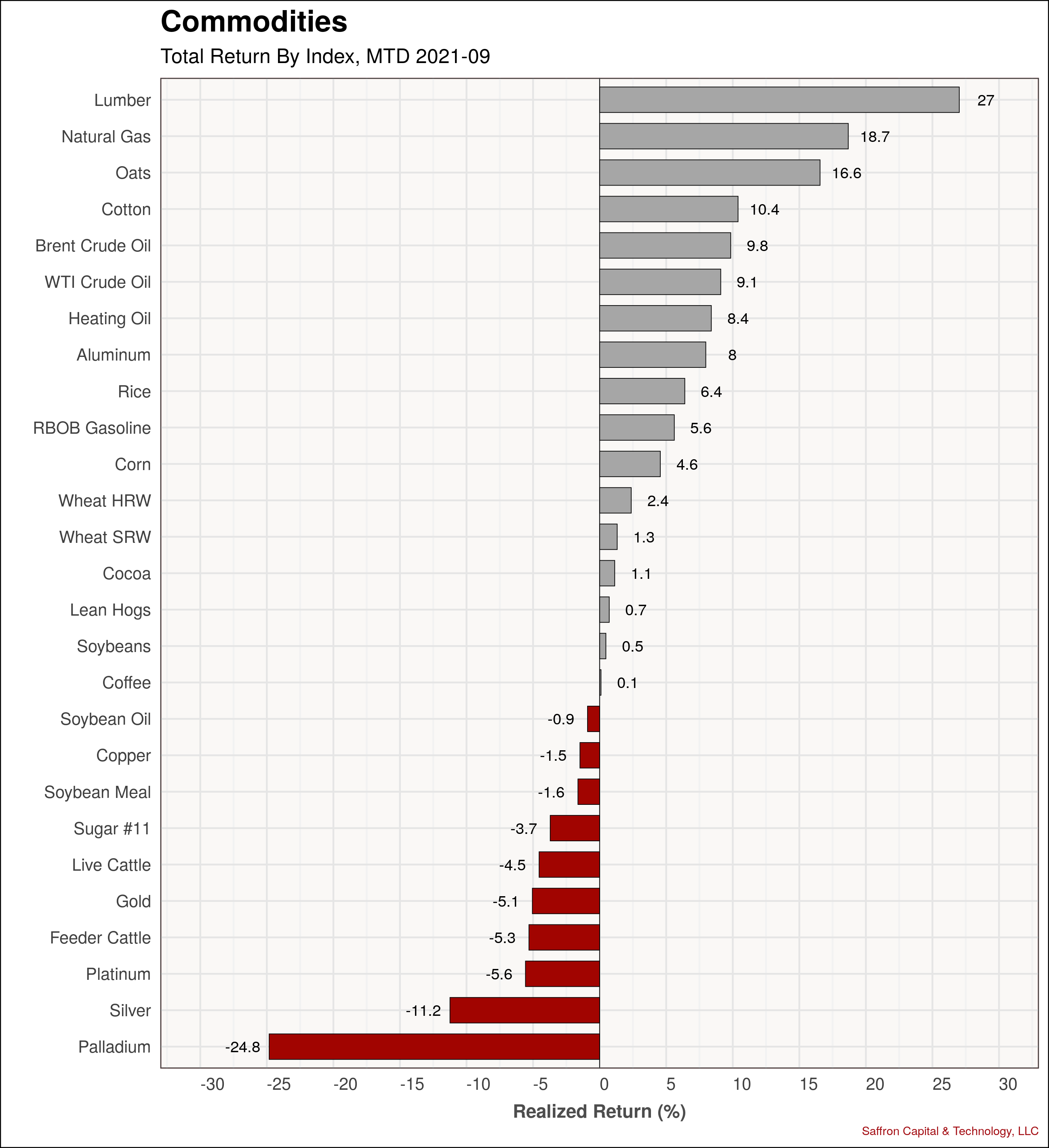

September returns across global financial markets suffered their broadest retreat in a year. First, the hardest hit asset classes were domestic and international equities. Second, government and corporate bonds also declined more than 5%. Commodity prices were mixed. For example, lumber, natural gas, cotton and oil all inflated significantly, while grains and metals declined. Finally, the US Dollar also fell against the Japanese Yen, the Russian Ruble and the Chinese Renminbi in September.

A detailed visual comparison of returns within and across the major asset classes is provided below:

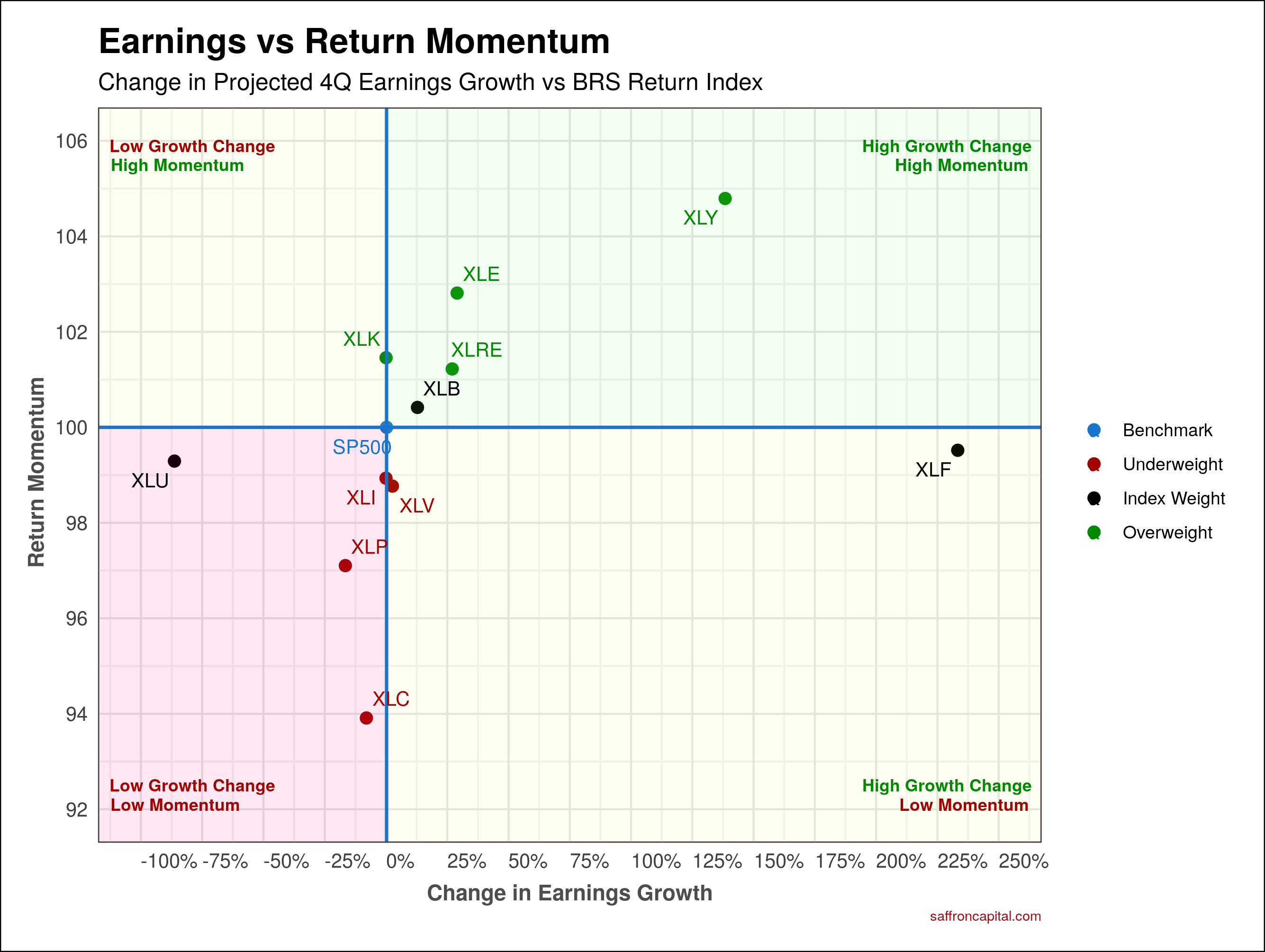

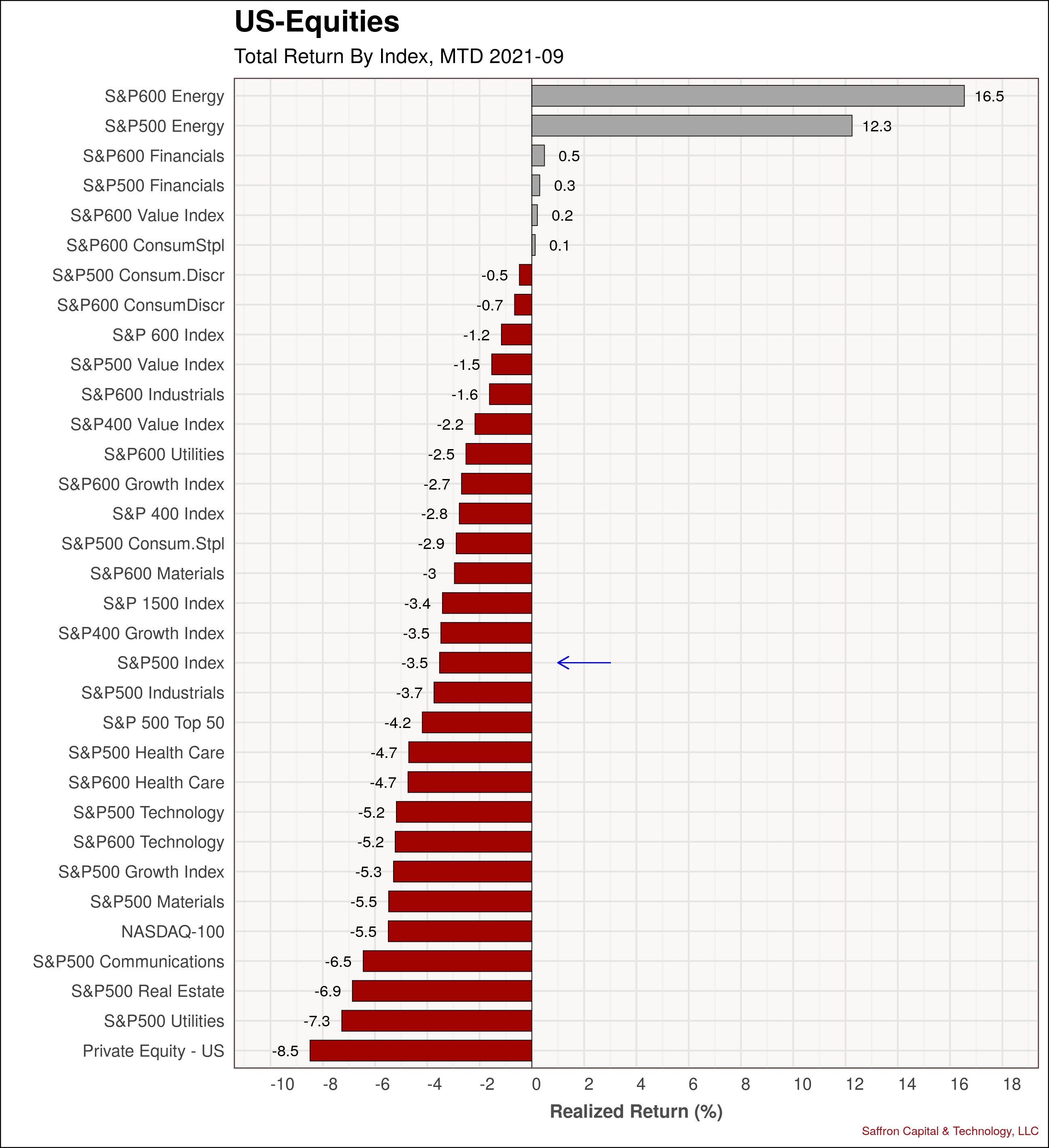

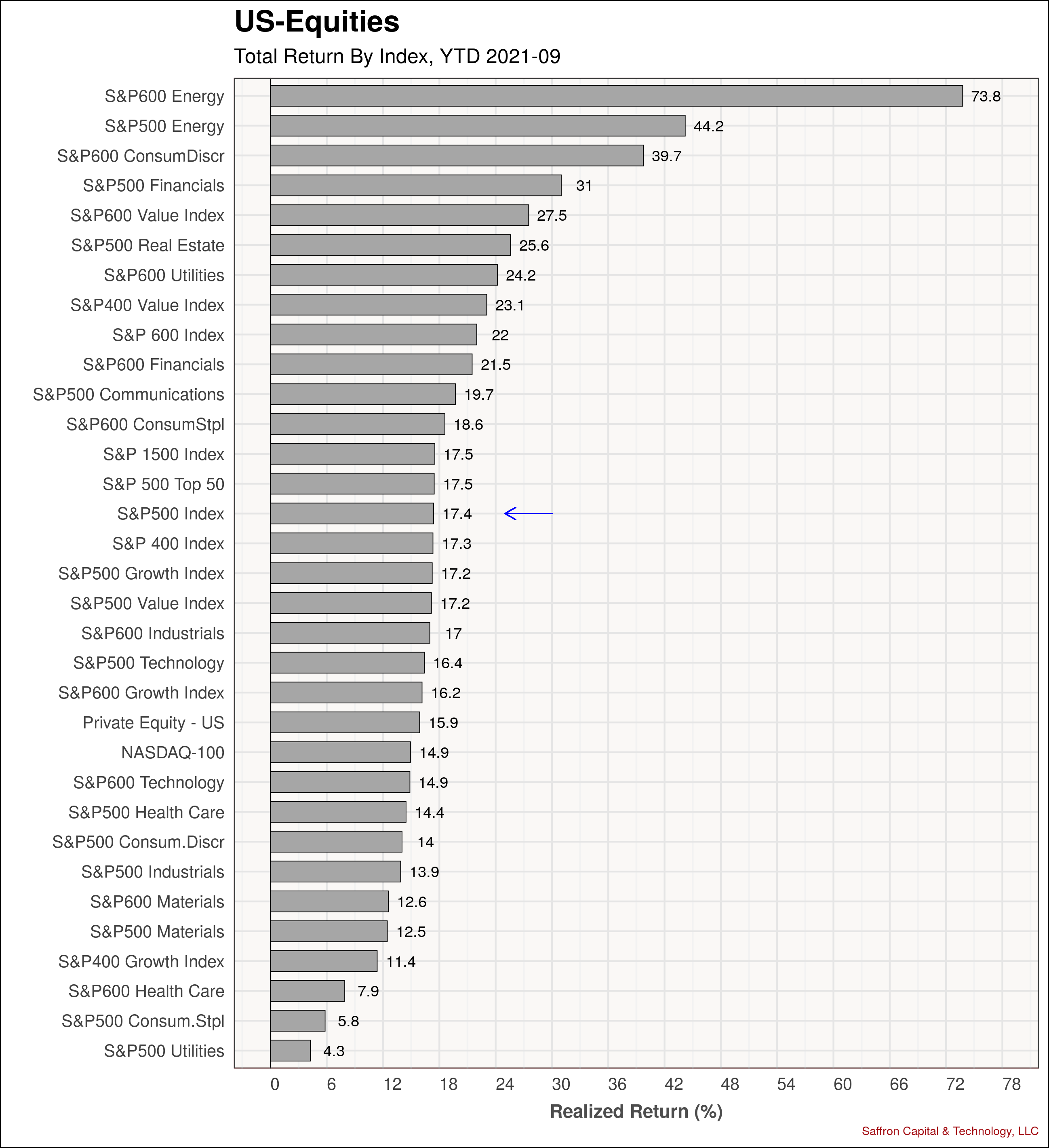

US-Equities

The S&P500 index was down 3.5% in September, while year-to-date (YTD) returns are now 17.4%. Notably, small- and mid-cap stocks in the energy and financial sectors provided the highest returns during the month. However, all other sectors where in decline. For example, private equity prices, large cap utilities and real estate sectors fell the most.

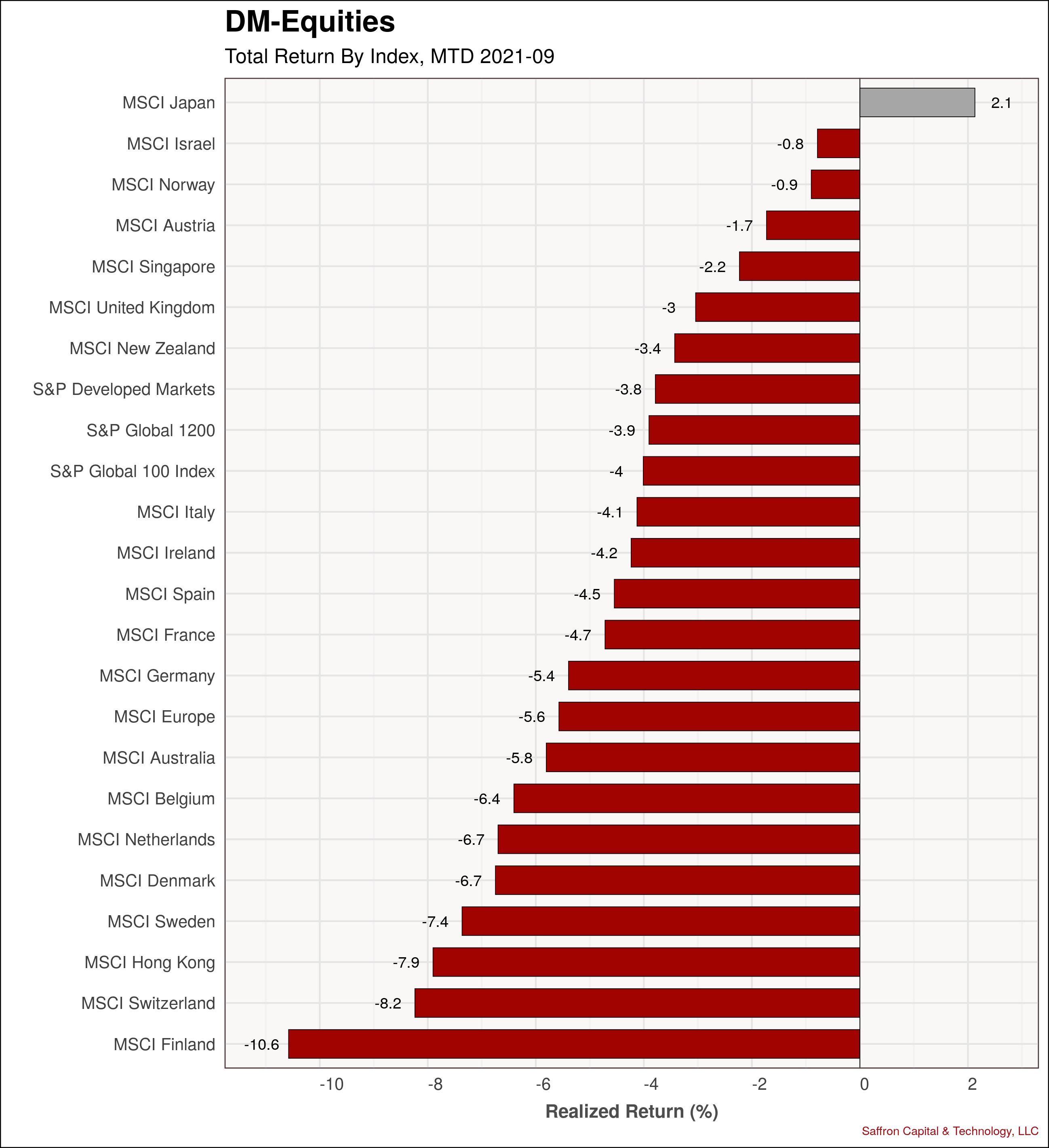

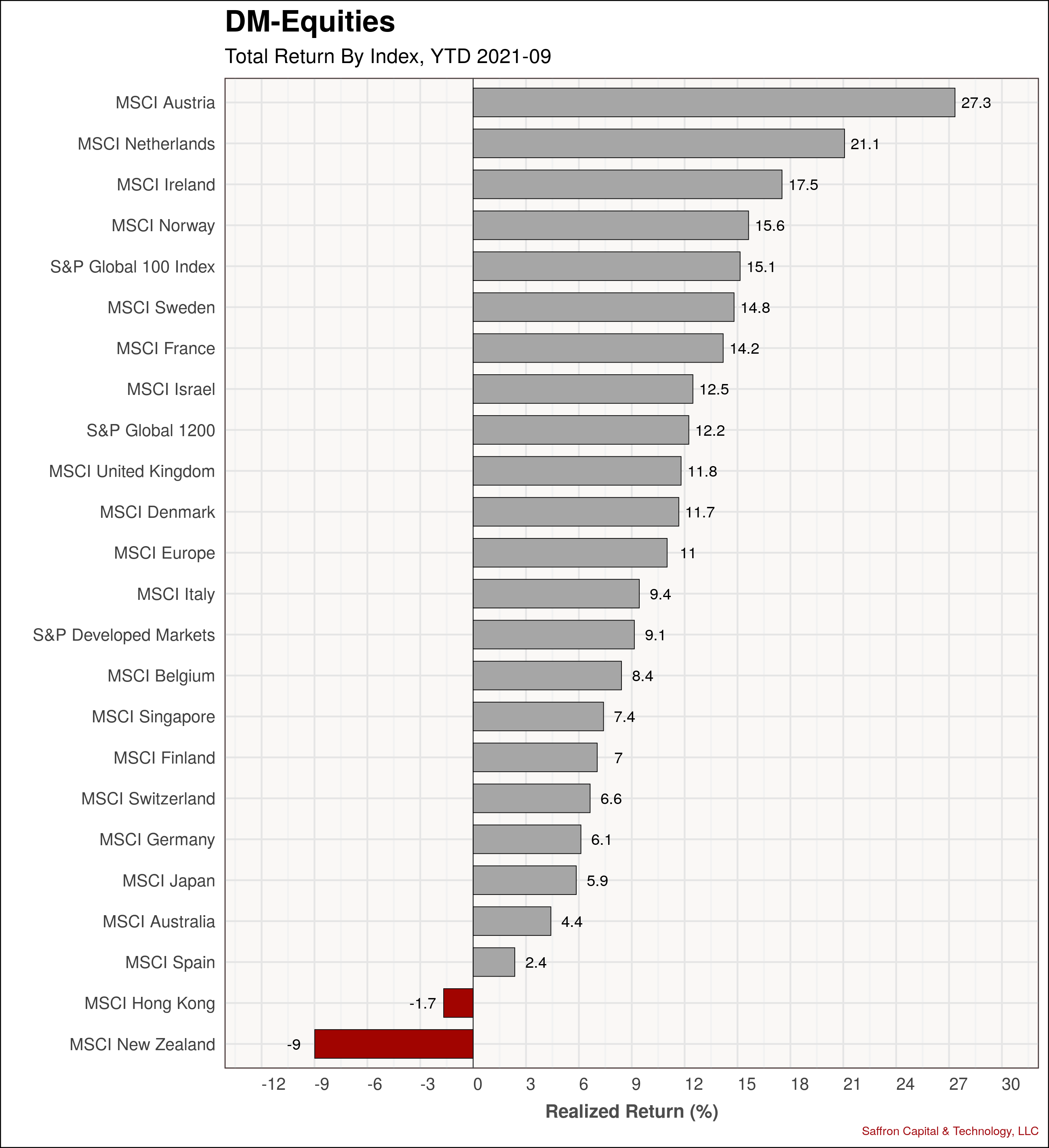

Developed Market Equities

Global equities ended a 7 month winning streak. Specifically, all major developed markets were down with the exception of Japan. Meanwhile, looking at YTD performance, only Austria, the Netherlands and Ireland outperform the U.S. S&P 500. Otherwise, all major markets remain positive with the exception of Hong Kong and New Zealand.

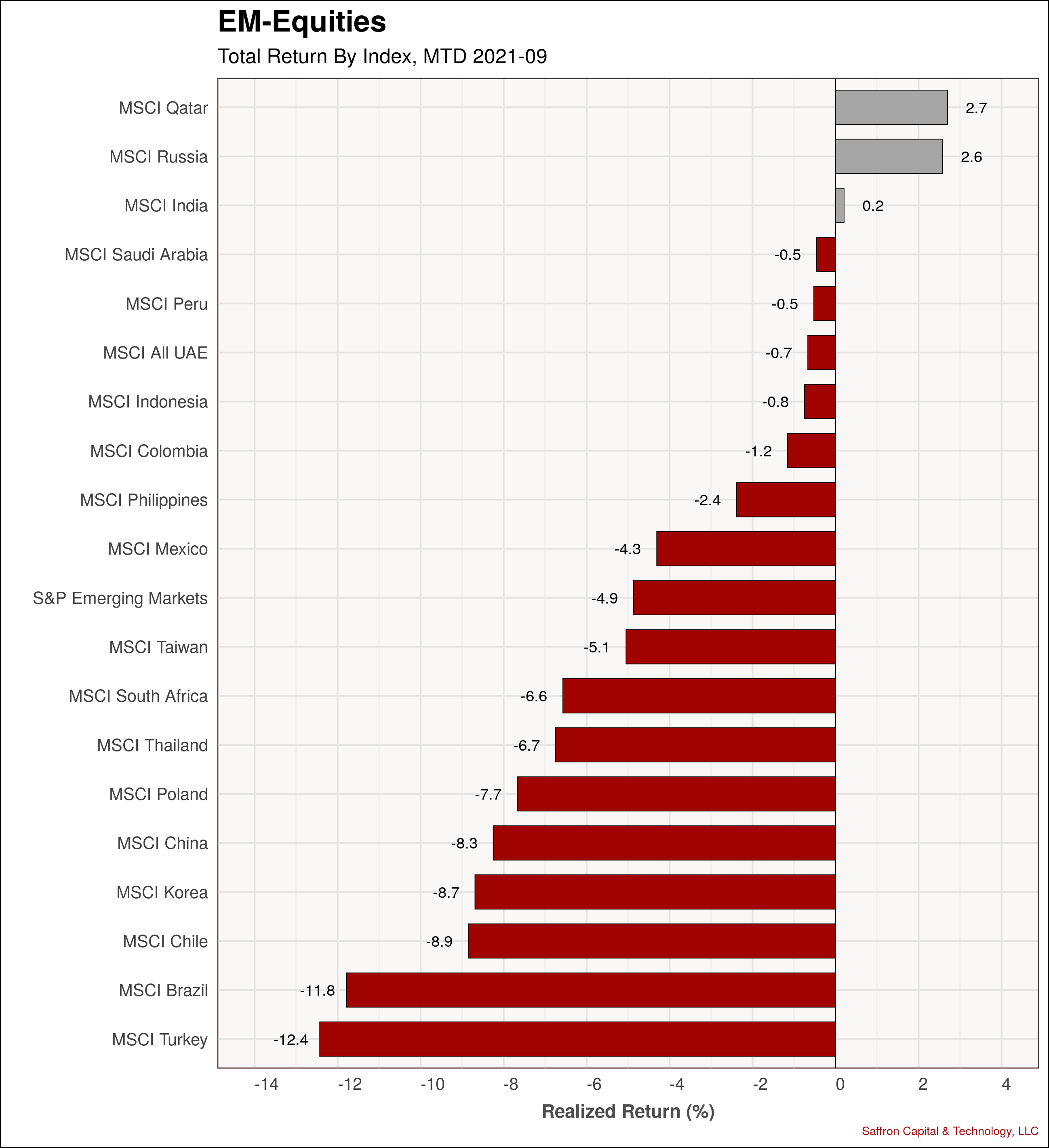

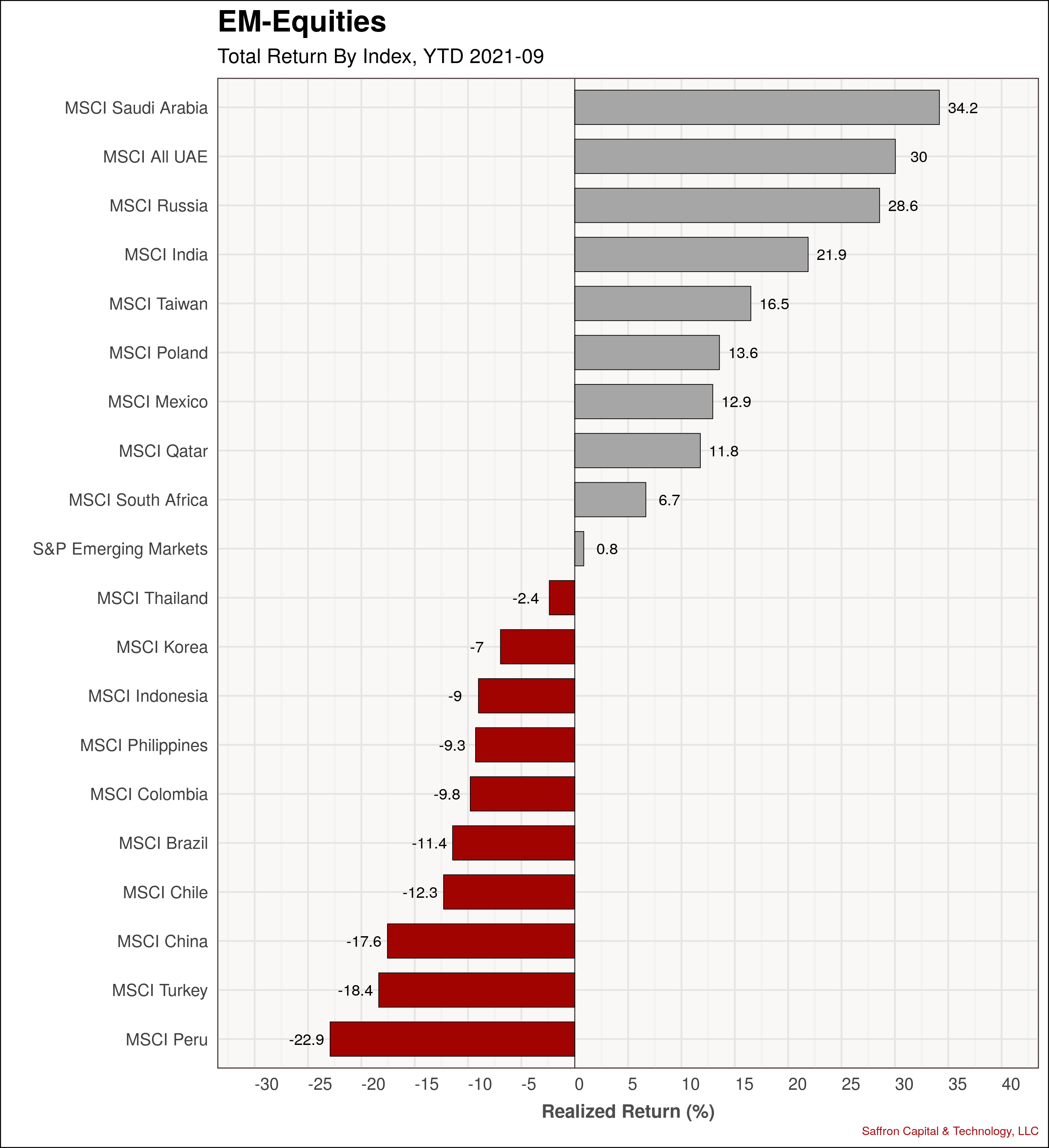

Emerging Market Equities

The two large natural gas producers, Qatar and Russia, topped emerging market equity performance with positive gains. Meawnhile, stock markets in India also rose in September. Next, looking at YTD performance, markets belonging to oil producers and India all outperformed the U.S. stock market.

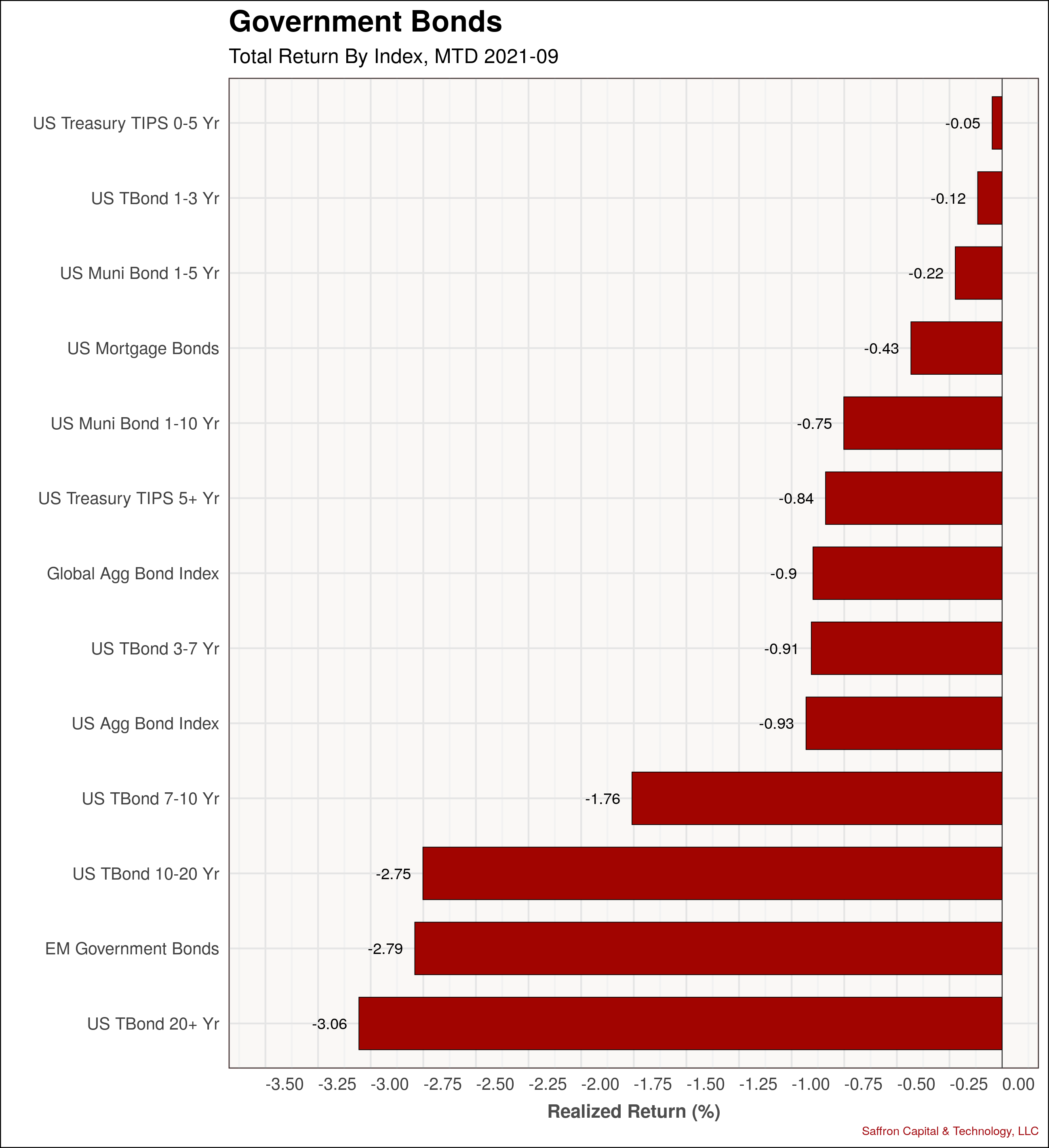

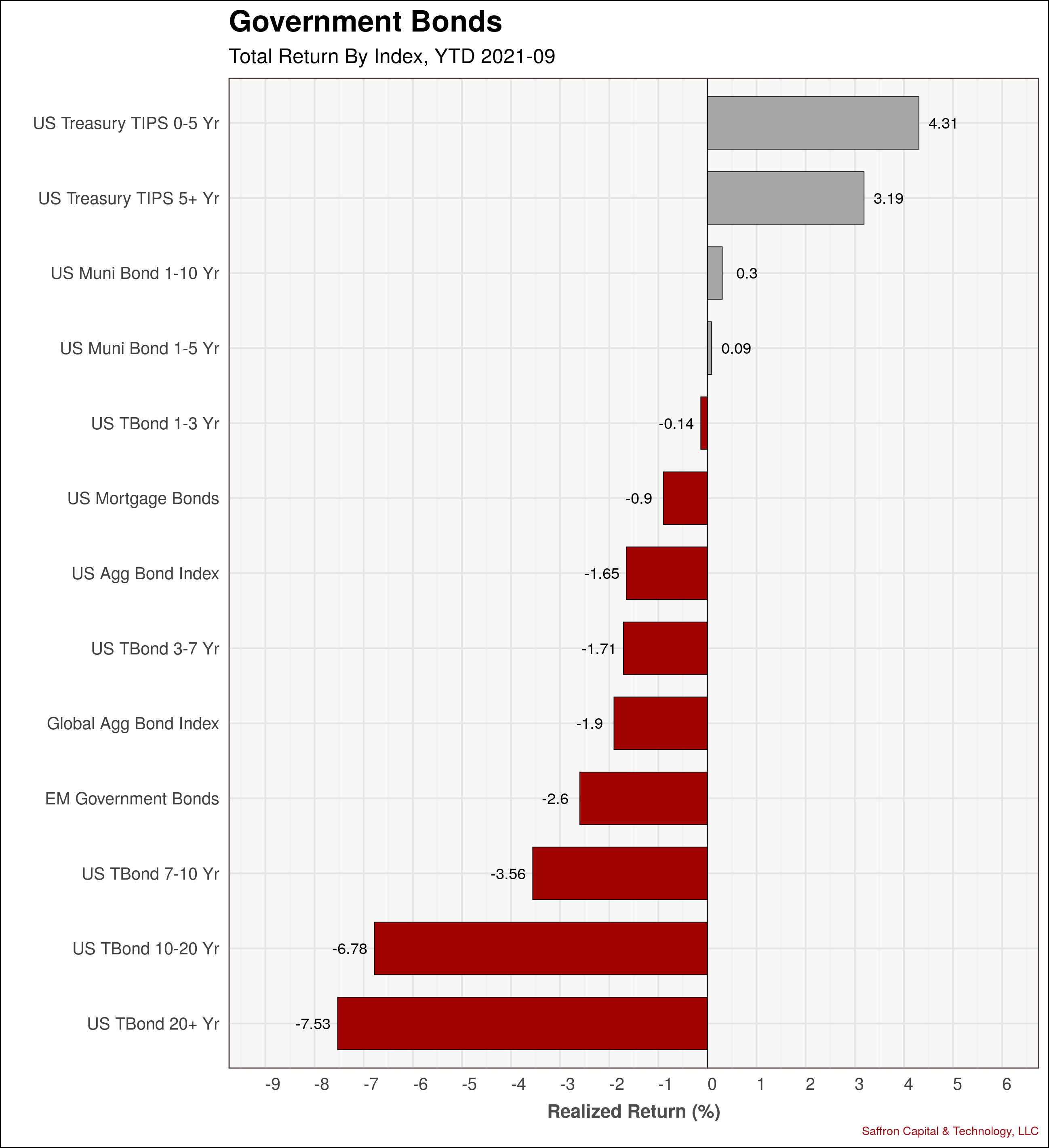

Government Bonds

Government bonds were down across the board following rapid yield spikes at the end of September. For instance, the 30-year bond fell 6 full points, the largest weekly drop of the year. Additionally, other long duration bonds, including inflation protected bonds, also fell. Notably, inflation protected bonds continue to lead YTD performance returns.

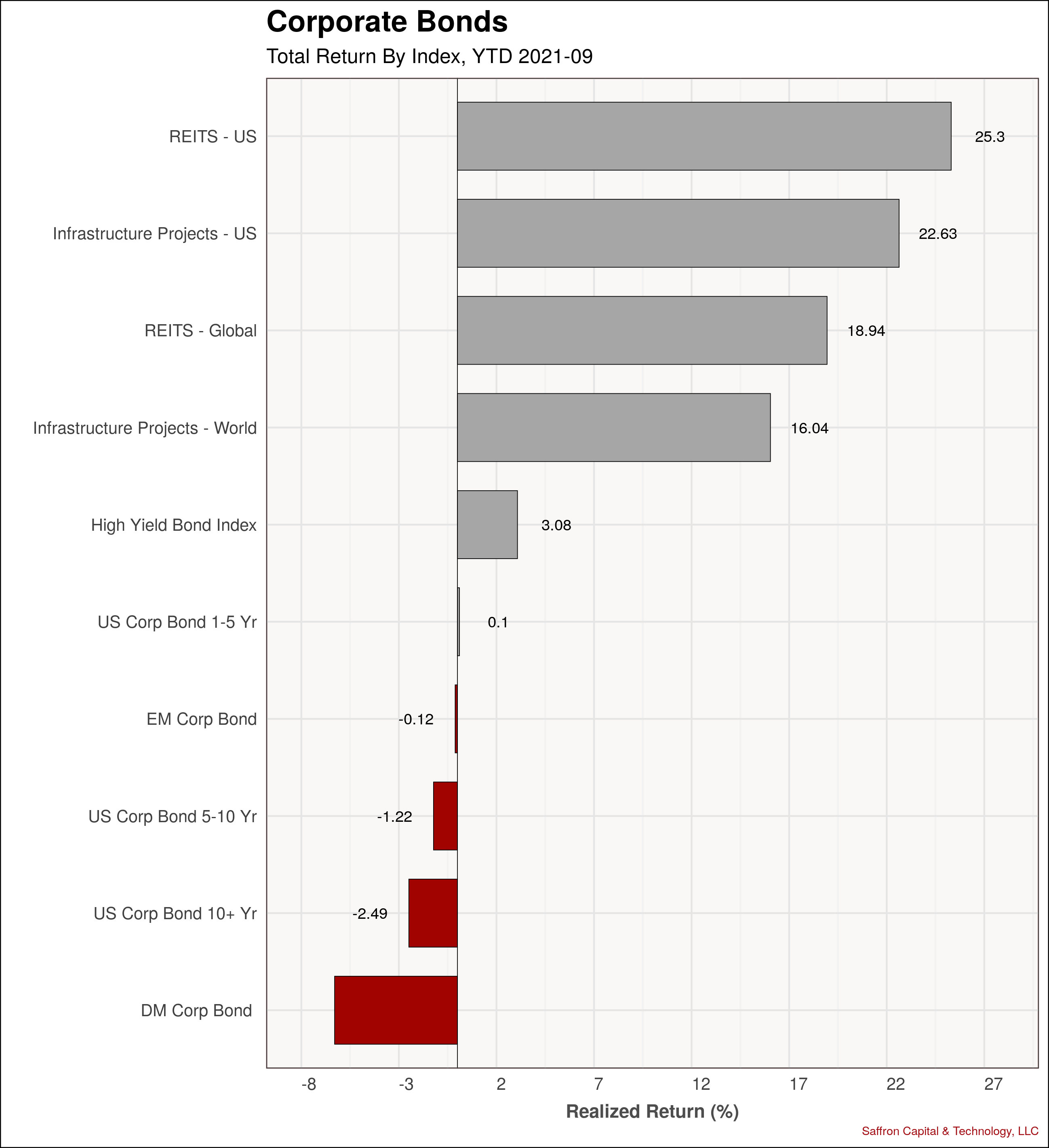

Corporate & Infrastructure Bonds

In contrast, short duration and high yield corporate bonds both avoided significant yield hikes in September, though prices were marginally down. Meanwhile, longer duration US and global REITS both had losses in excess of 5% during September. At the same time, infrastructure bonds were also hit with negative returns of 4.35%. However, investors in REITS and infrastructure bonds continue to enjoy YTD returns higher than those of the S&P 500 index.

Commodities

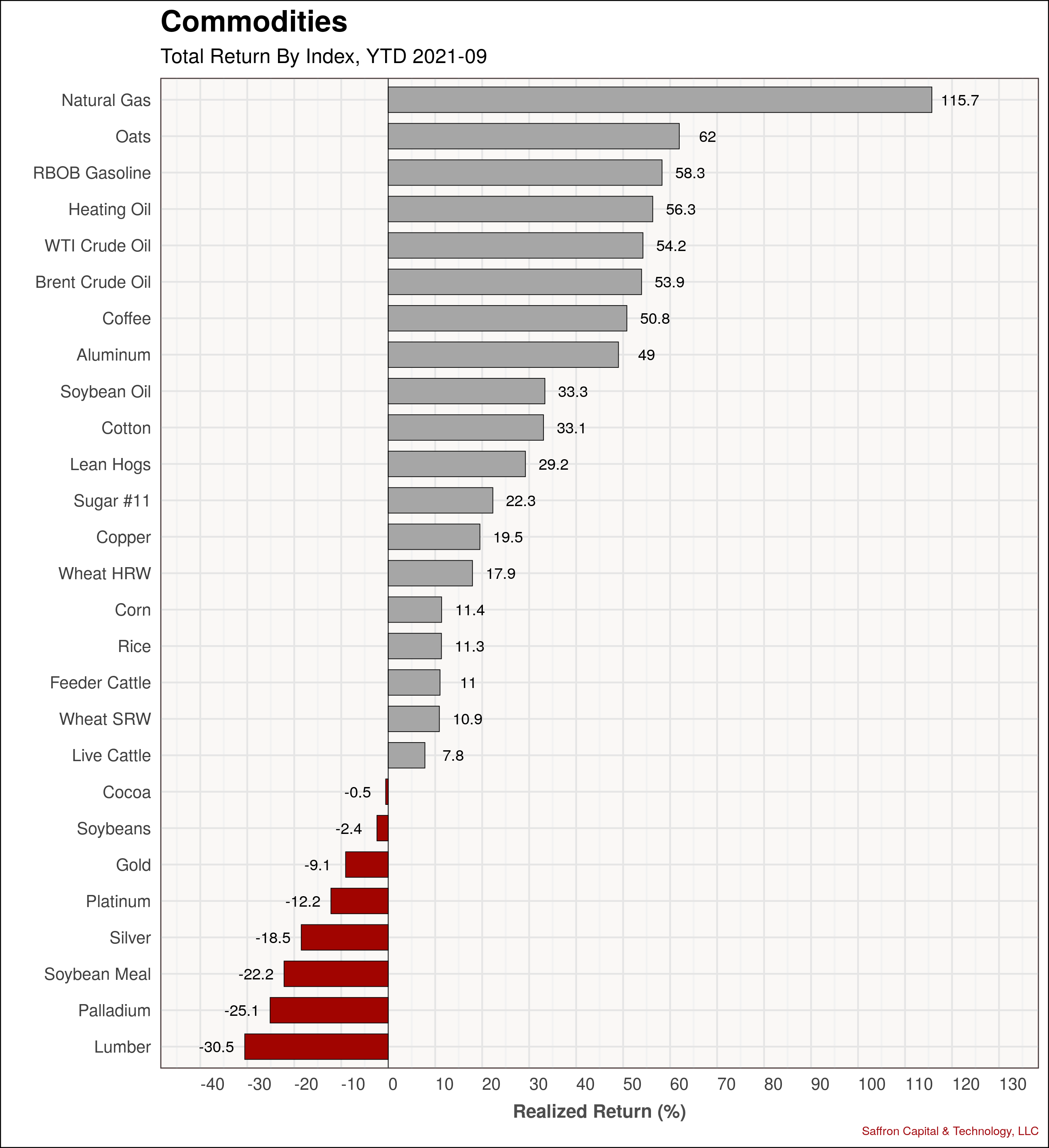

Above all, commodities continued to dominate asset returns in September, lead by lumber, natural gas, oats and oil. Alternatively, metals, meats and grains saw price declines. Similarly, energy markets and coffee continued to lead YTD performance with returns in excess of 50%.

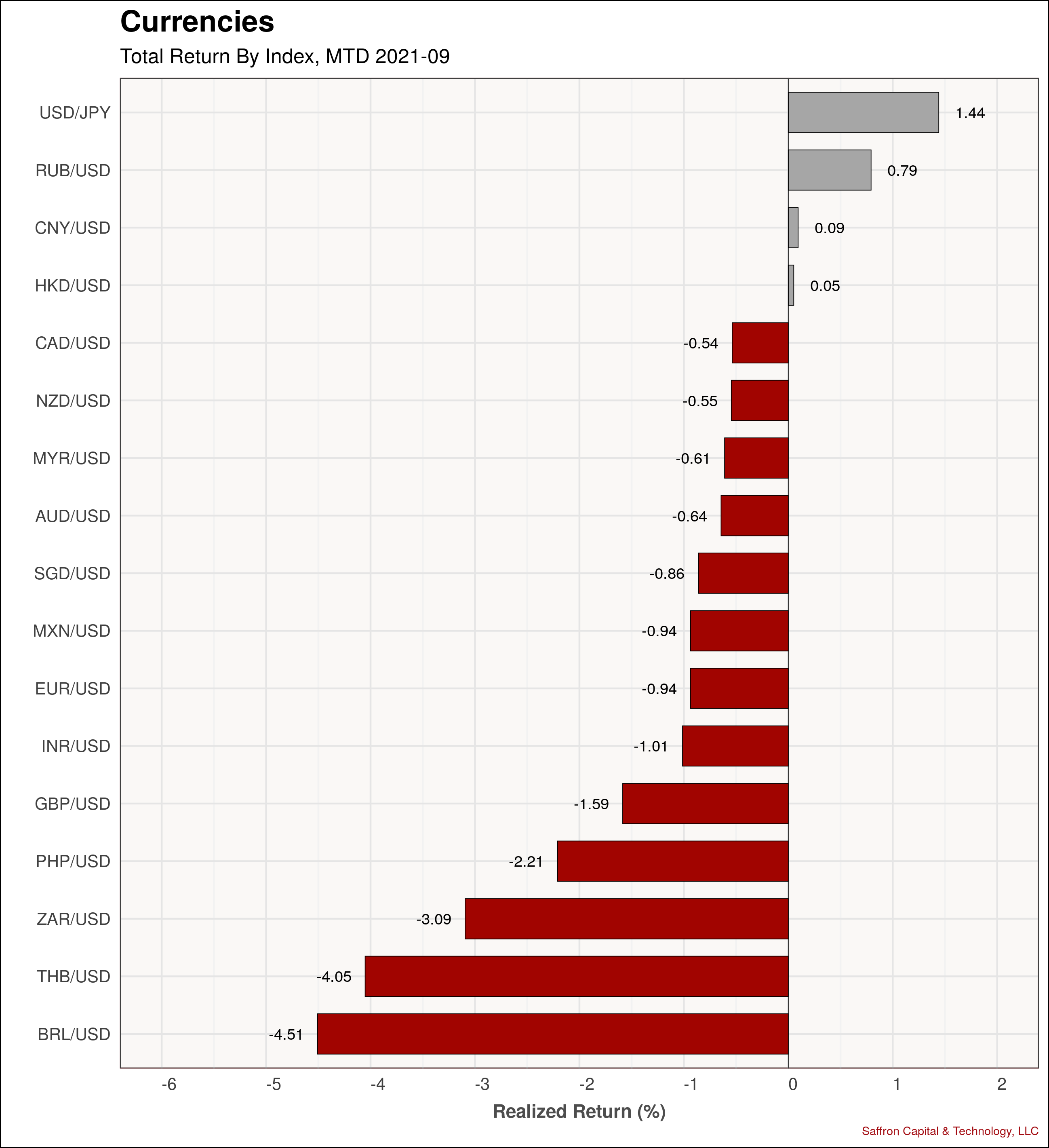

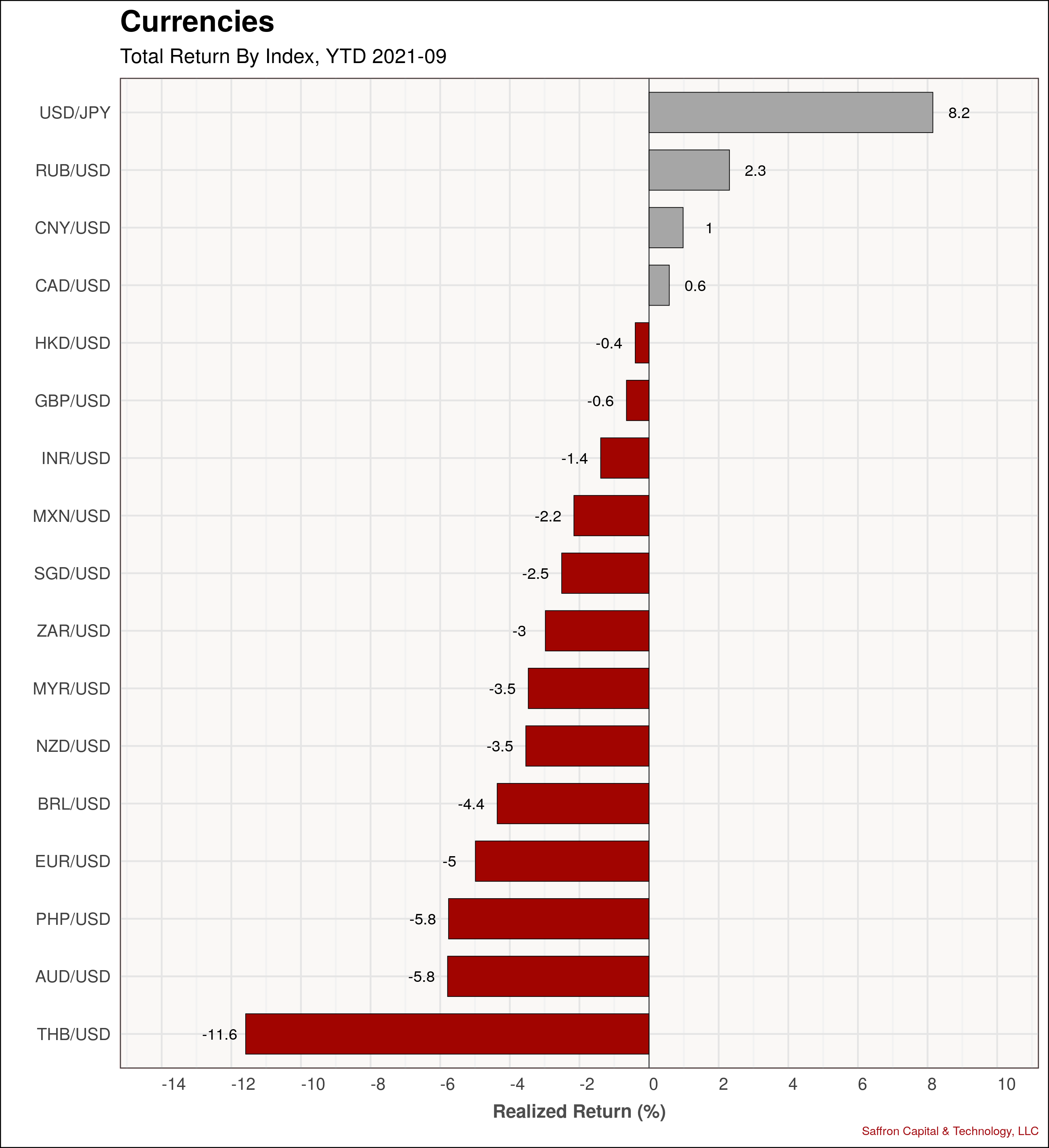

Currencies

Finally, the Japanese Yen, the Russion Rubble and the Chinese Renminbi lead September returns against the dollar. In addition, these same currencies top the chart for YTD returns.

That’s it for September asset returns. If you have any comments or questions, you can contact me here.

{kind=link}

{kind=link}