November 2022 equity market returns were strong in the US and were especially strong across international equity markets. The relief rally that began in October benefited from revised expectations and confirmation that Fed rate increases would moderate. For example, the S&P 500 gained +5.4%, while the S&P Developed markets Index gained +12.3% and the S&P Emerging Markets gained +14.7%. Meanwhile, bond market returns were also strong with the US. Aggregate Bond Index up 3.8%. The short-end of the yield curve was up significantly, while the back-end saw only limited gains. At the same time, the High Yield Index for corporate issues was up 3.4%, which lagged gains seen in REITs, and project infrastructure bonds. Finally, the US Dollar trended down during November, supporting positive returns across many commodities.

The following analysis provides a visual record of October returns across and within the major asset classes.

US Equities

November 2022 returns for the S&P 500 index (+5.4%) continued the uptrend seen in October. Equities benefited from strong returns in large cap Materials (+11.7%), Industrails (+7.8%), Utilities (+7.0%) and Financials (+6.9%). Private Equity (+10.4%) also saw significant gains, reversing the negative trend since the start of the year. This was the first month all year that large cap Energy (+1.3%) lagged the S&P 500 Index. The only sectors with negative returns were small cap Energy (-0.1%) and Utilities (-0.4%). On a year-to-date (YTD) basis, the benchmark S&P 500 index (-14.4%) remains weak. Losses are most evident in the Communications (-33.2%), private equity (-33.1%), Consumer Discretionary (-28.1%) and NASDAQ (-25.9%) shares. The top performers since January are large cap energy (+69.5%), small cap Energy (+57.7%), and high dividend stocks (+9.9%).

Click to enlarge

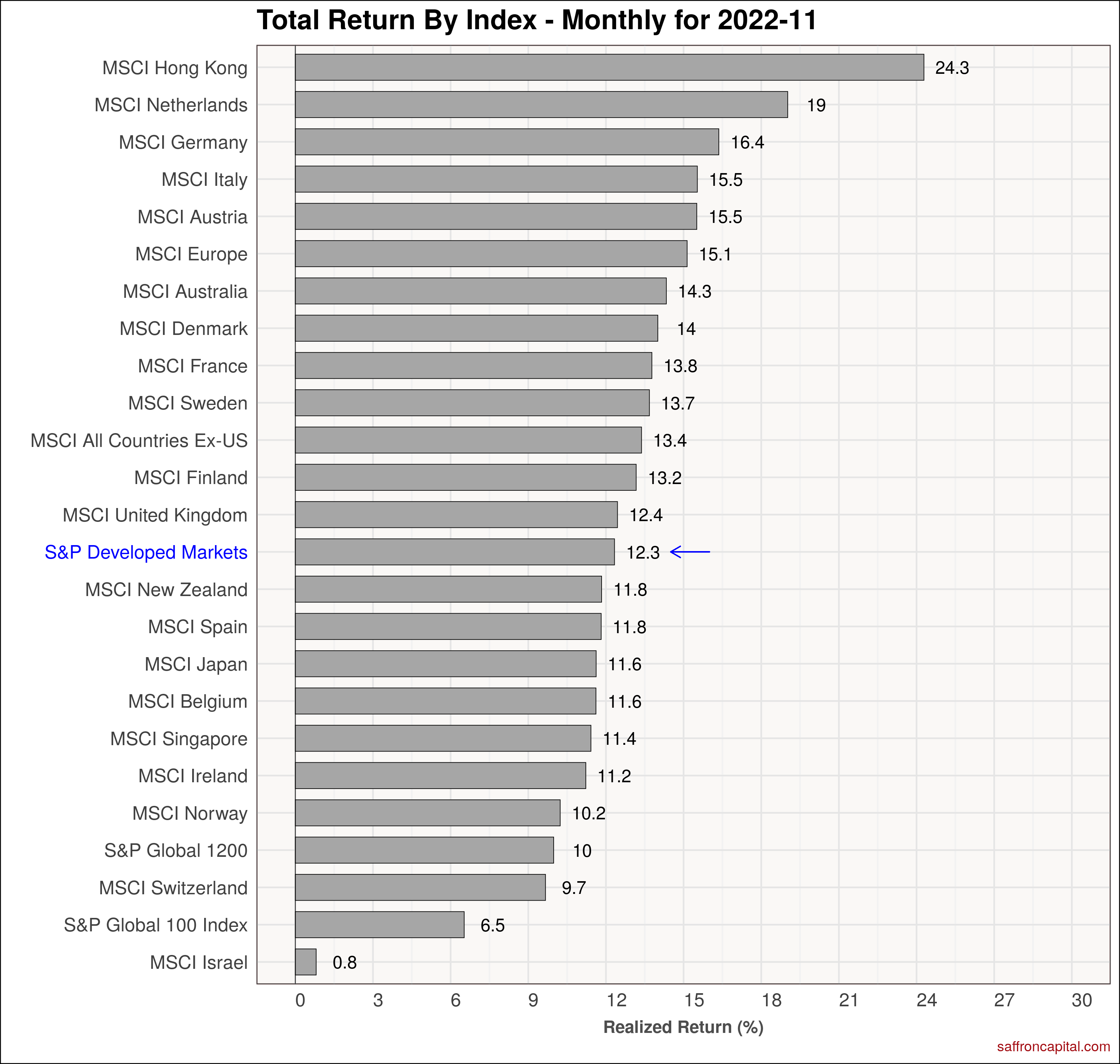

Developed Market Equities

Elsewhere, developed market equities were among the best performers of the month. Specifically, the S&P Developed Markets index (+12.3%) outperformed the S&P 500 index by 600 bps. Markets in Hong Kong (+24.3%), the Netherlands (+19.0%) and Germany (+16.4%) topped the leaders list. In contrast. Isreal (+0.8%) lagged most international marekts, while the other weak sector elements, like Switzerland (+6.5%) still outperformed US equities. Year to date, the S&P Developed Markets index (-13.2%) now leads the US equities by 120 basis points. Like US equities, every developed market is in the red since January.

Click to enlarge

Emerging Market Equities

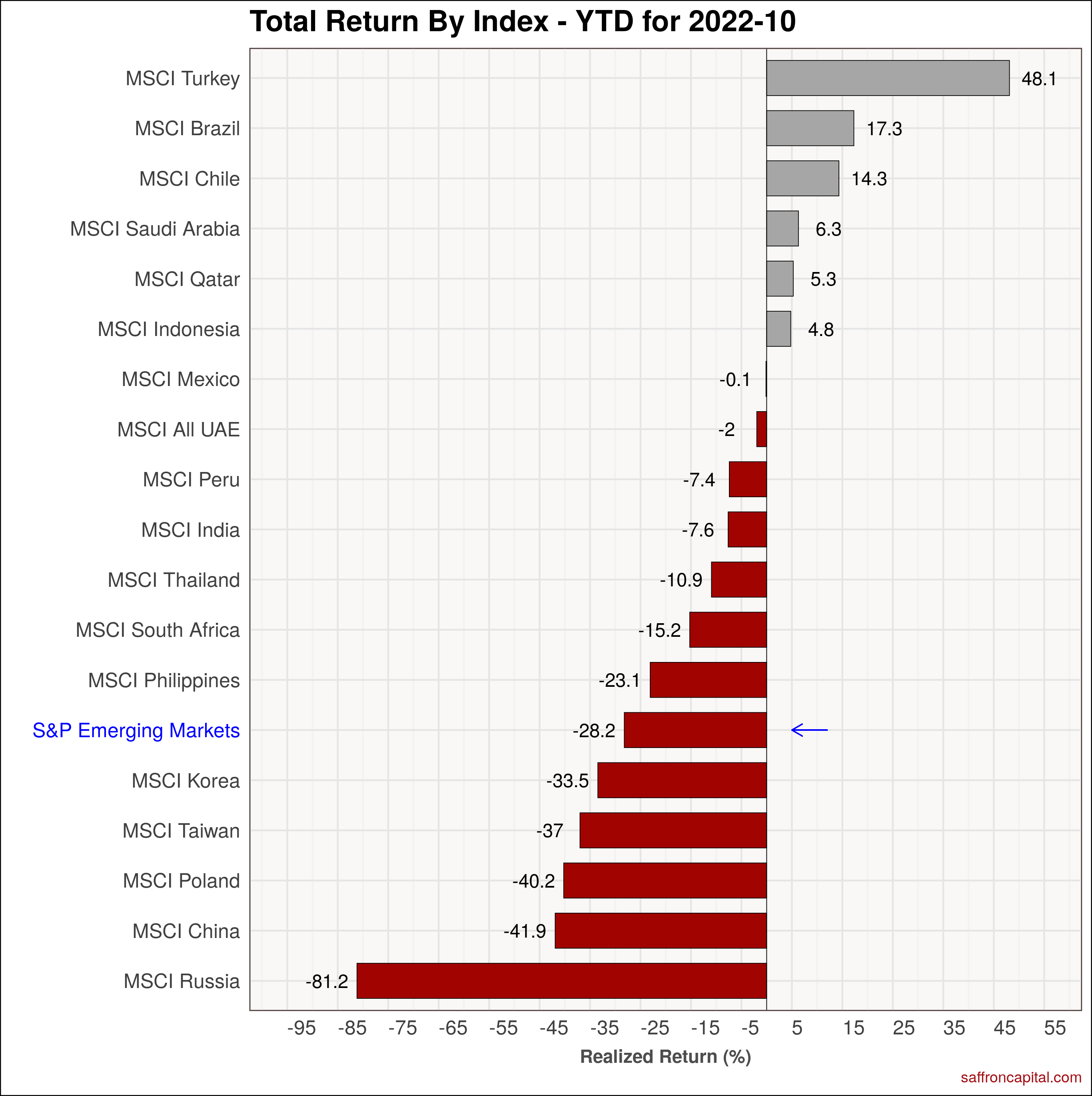

November 2022 return for the the S&P Emerging Markets Index (+14.7%) topped all major asset groups. The strongest stock markets were in China (+32.1%), Turkey (+26.1%) and Taiwan (+22.0%). Meanwhile, India (+3.8%) continued to beat the emerging market index and trailed U.S. equities in October. China (-14.8%). Taiwan (-2.6%) and Qatar (-1.2%), fell the hardest. On a year to date basis, the S&P Emerging Market index (-28.2%) remains solidly down and is now lagging developed markets significantly given weakness in Asia.

Click to enlarge

Government Bonds

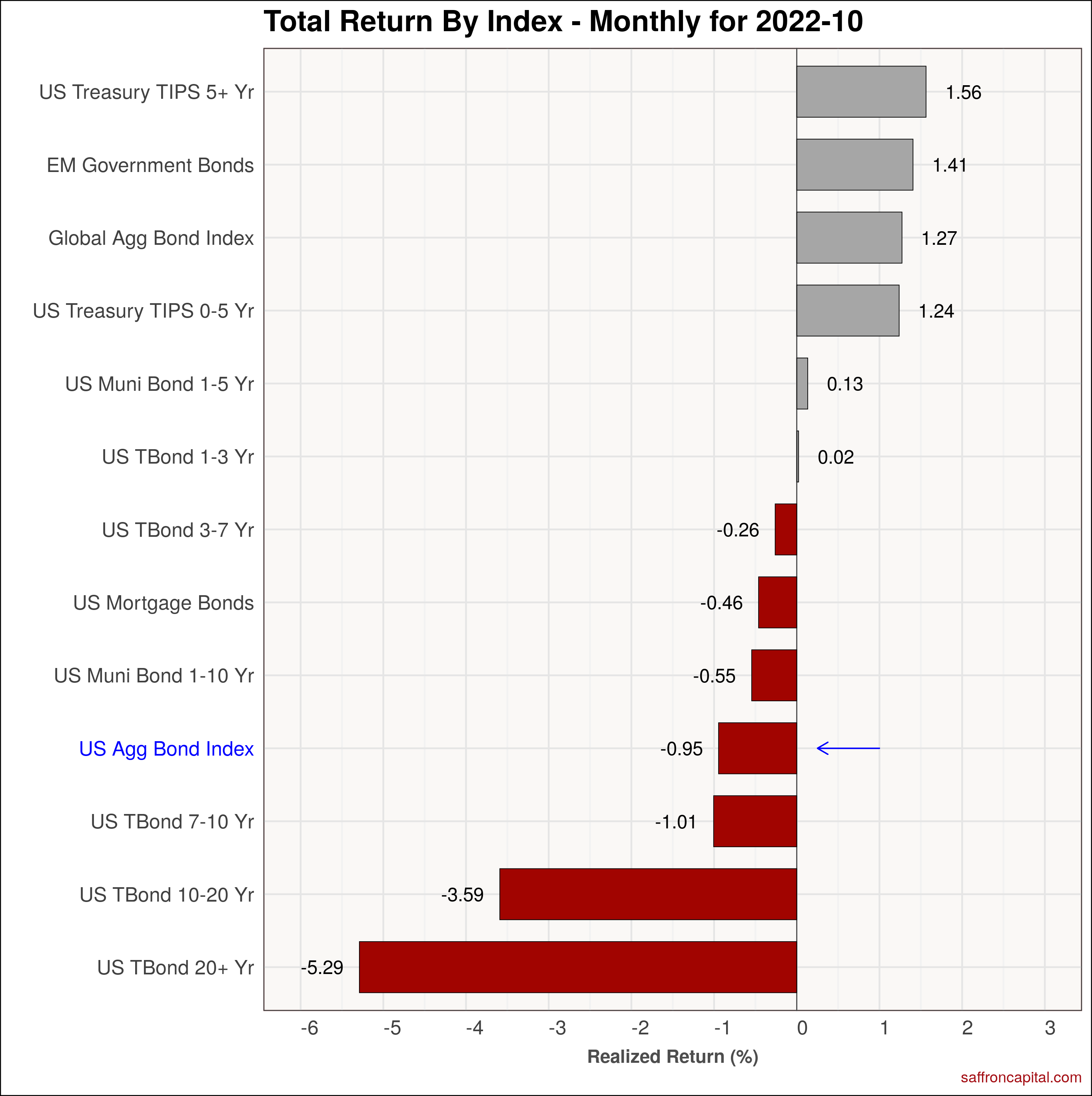

October returns for government bond markets had modest declines as seen in the U.S. Aggregate Bond Index (-0.95%). At the same time, sovereign bonds for emerging (+1.41%) and developed (+1.27%) economies had modest gains. US Treasuries expiring in 1-3 years were flat, while the belly of the curve expiring 7 years forward (-0.95%) had modest losses. Long dated Treasuries (-5.29%) were clobbered. On a year-to-date basis, the US aggregate Bond index (-1519%) is subject to ongoing pressure and is being pulled down by long duration 20 year plus treasuries (-33.62%) and Treasuries maturing 10 to 20 years (-28.21%).

Click to enlarge

Corporate & Infrastructure Bonds

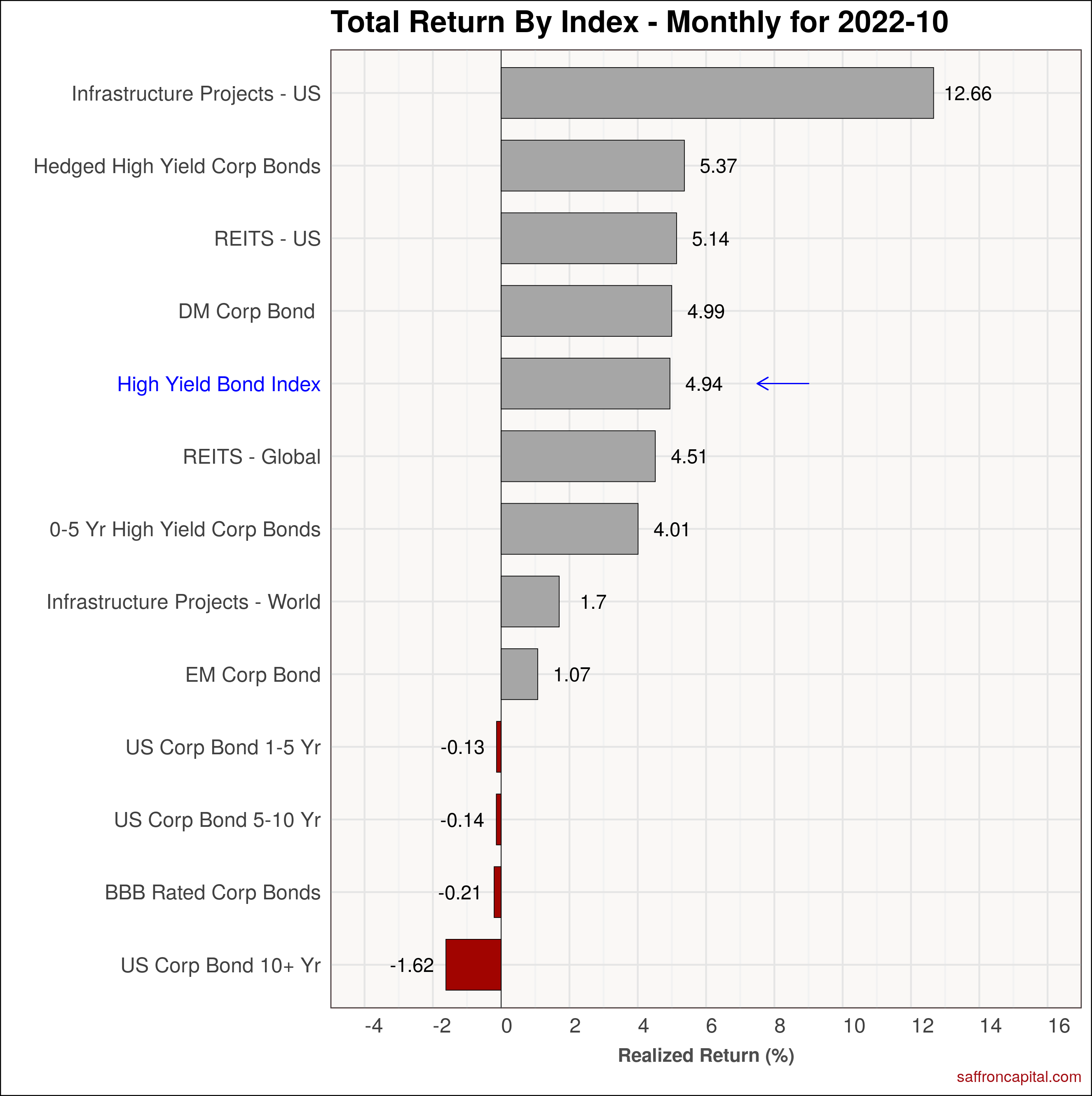

US infrastructure bonds (+12.66%) had another strong month after being subject to heavy selling early in the month. Similarly, High Yield Corp Bonds (+5.37%) also had solid gains. Finally, US REITS (5.14%) benfited from end of the month buying given the prospect for a slower pace of interest rates increases going in the future. Long-dated corporate bonds (-1.62%) was the weakest portfolio. On a year-to-date basis, the benchmark high yield index (-11.86%) is weak, but still proving to be more durable than US equities.

Click to enlarge

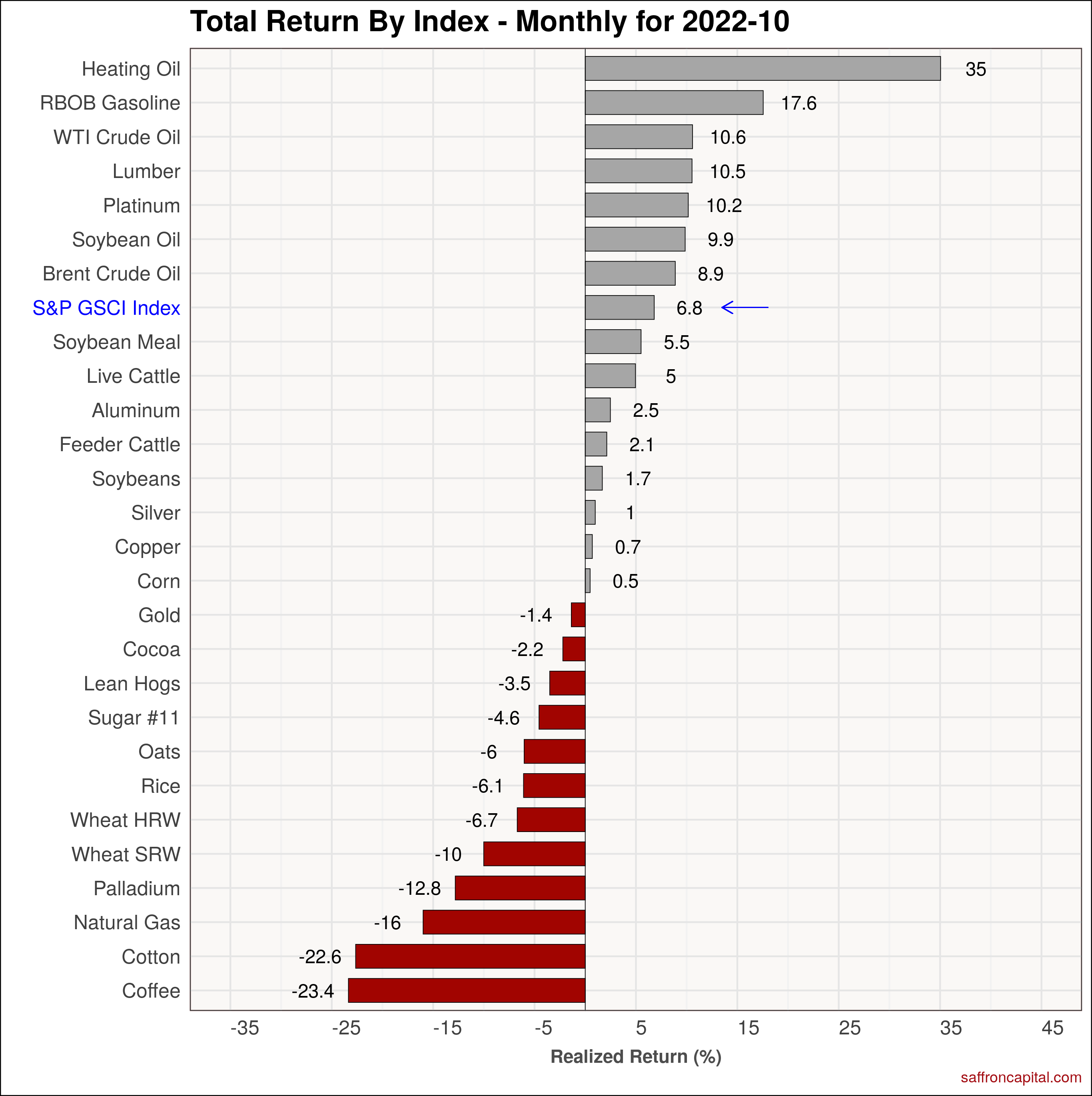

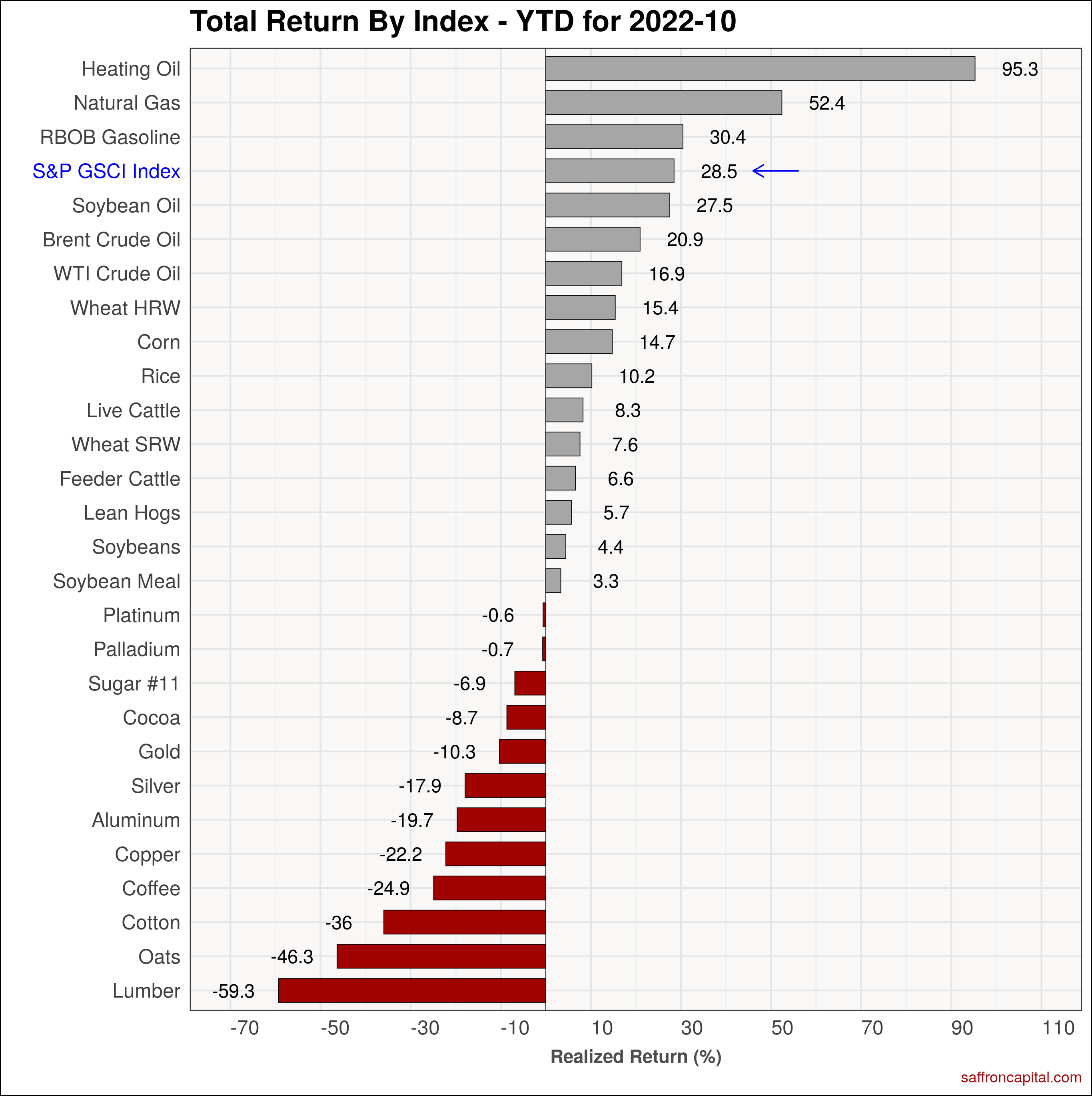

Commodities

October returns for commodities were positive for the most part. The S&P GSCI index (+6.8%) benefited from string gains in heating oil (+35.0%), Gasoline (+17.6%) and WTI crude oil (+10.6%). Moreover, the high dollar has raised demand concerns for a number of commodities, including coffee (-23.4%), cotton (-22.6%), and natural gas (-16.0%). Since January, The strongest performing commodities include heating oil (+95.3%), natural gas(+52.4%), and gasoline (+30.4%).

Click to enlarge

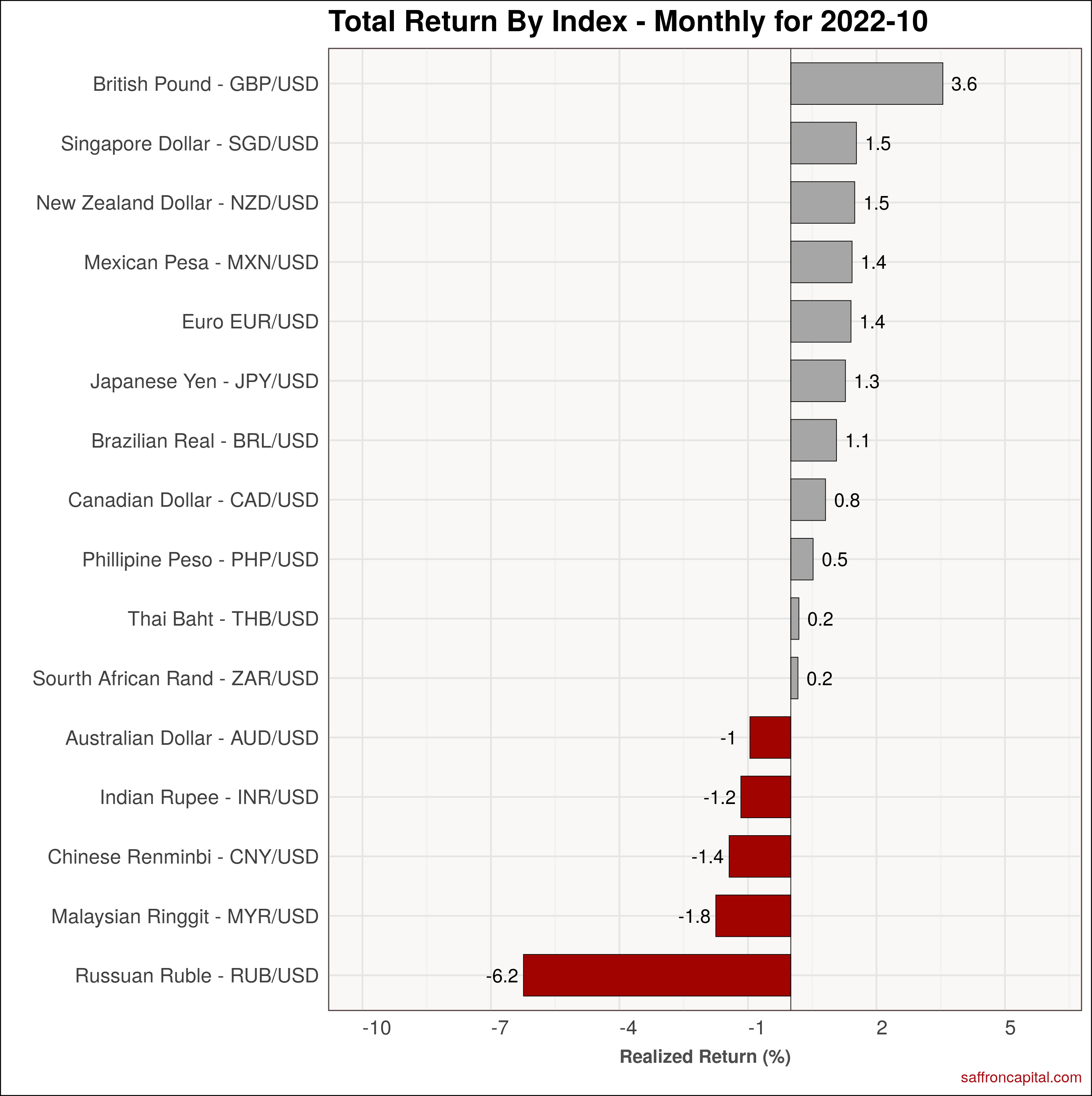

Currencies

The US Dollar (+0.57%%) rose slightly in October, after strong losses initially in October. Gains were lead by the British Pound (+3.6%) and the Singapore Dollar (+1.5%). The Russian Ruble (-6.2% was the hardest hit currency, followed by the Malasian Ringit *-1.8%) and the Chinese Renminbi (-1.4%). Since January, the strongest currencies have been the Japanese Yen (+27.1%) and the Russia Ruble (+21.6%).

Click to enlarge

Have questions about the performance of your portfolio? Schedule a meeting with us here.

{kind=link}

{kind=link}

{kind=link}