December 2022 returns were negative across all asset classes. The S&P 500 Index ended the year down -19.4%, yielding the 6th largest drawdown since 1930. Meanwhile, the 30-year T-Bond fared much worse, losing -31.2%. The large-cap energy sector (+64.3%) has been the noticeable standout since the beginning of the year. Other safe havens included select emerging markets and commodities. Finally, 2022 also rewarded investors that pursued tactical asset allocations for risk management and capital preservation. For more insight, the following analysis provides a visual record of year-end results across and within the major asset classes.

US Equities

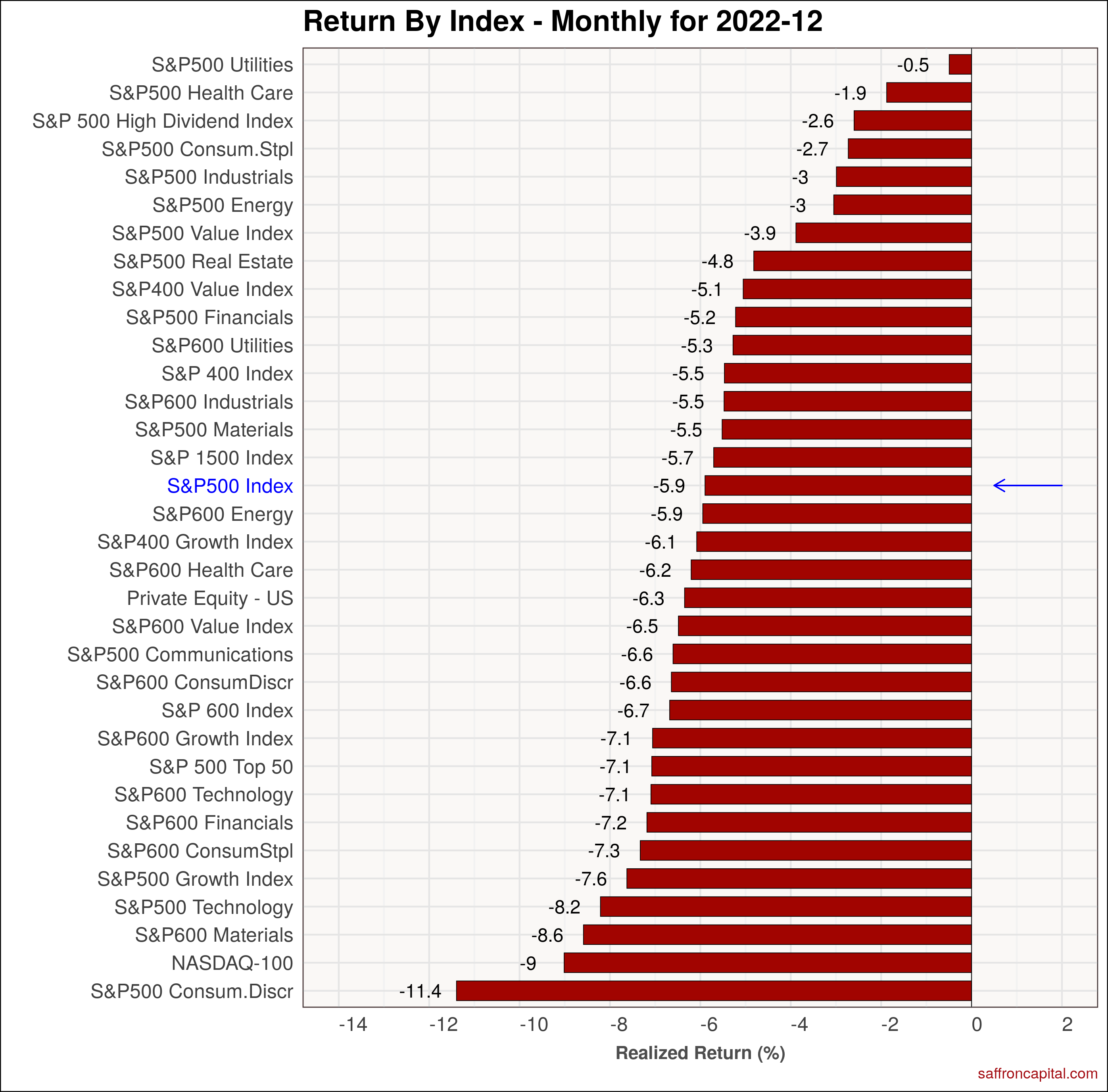

Red ink dominated December 2022 returns as confirmed by the S&P 500 index (-5.9%) and the NASDAQ-100 index (-9.0%). Top performing sectors in December in the large-cap index included Utilities (-0.5%), Health Care (-1.9%), Consumer Staples (-2.7%), and Energy (-3.0%). The S&P 500 High Dividend Index (-2.6%) also proved to be a relative safe haven. Finally, Growth shares (-7.8%) again lagged Value (-3.9%) stocks. On a year-to-date (YTD) basis, the benchmark S&P 500 index (-19.4%) significantly outperformed the NASDAQ-100 Index (-32.6%). Top large-cap sectors include Energy (+64.3%), High Dividend (+7.0%) stocks, and Consumer Staples (-0.8%). 2022 returns for Value shares (-5.4%) significantly beat Growth stocks (-29.5%).

Click to enlarge

Developed Market Equities

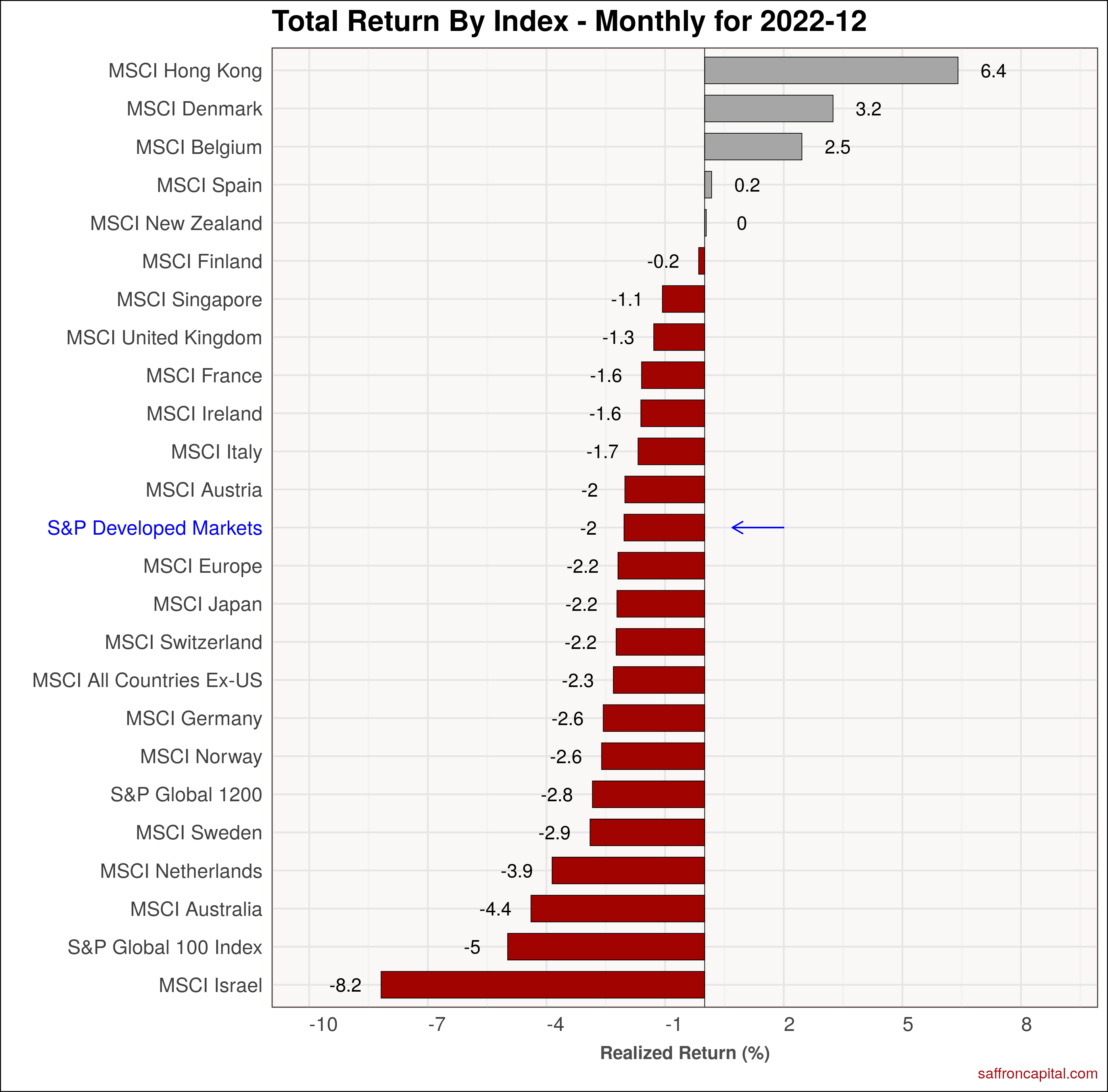

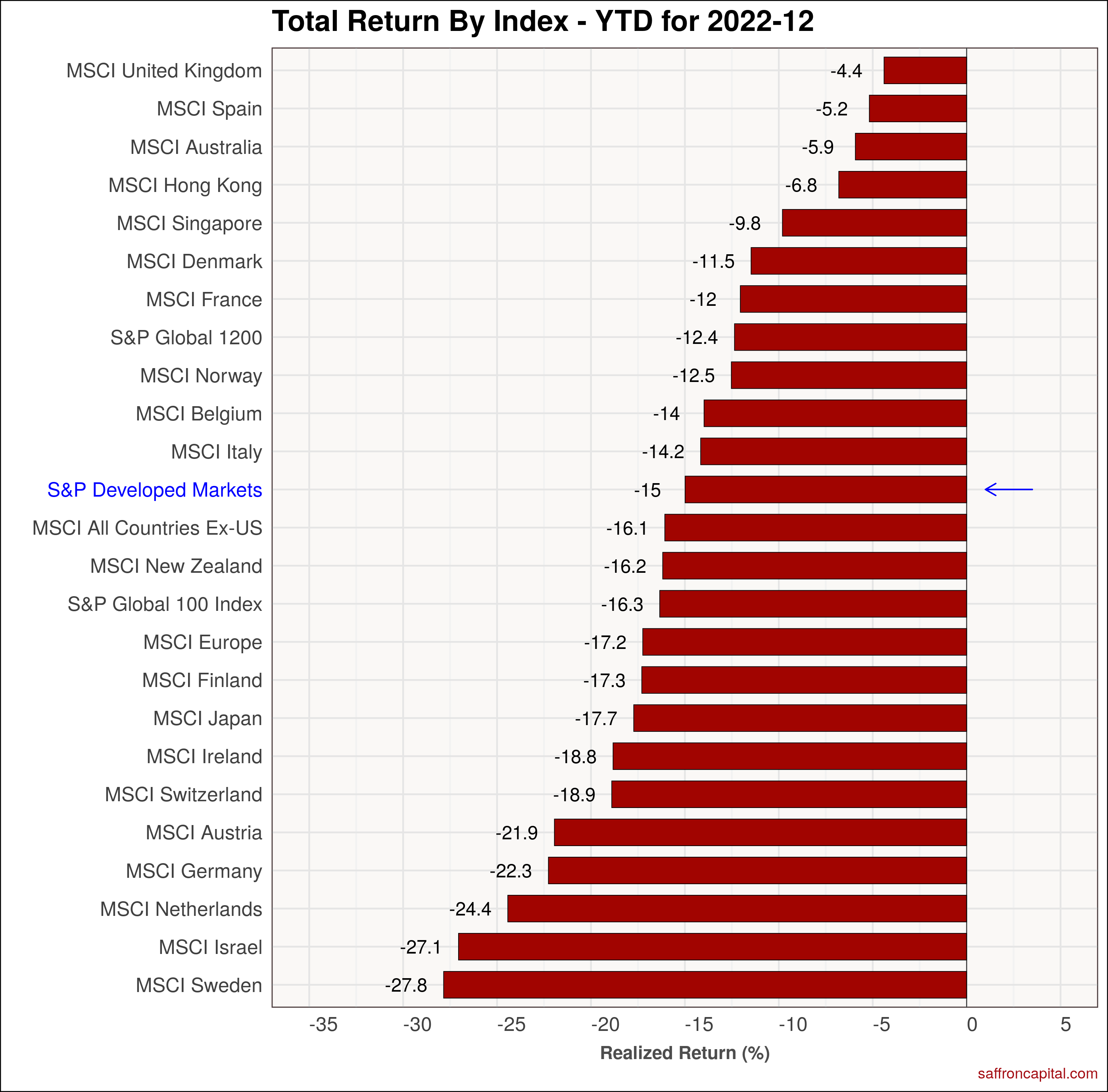

Elsewhere, the broad index for Developed Market equities (-2.0%) outperformed the S&P 500 Index for a second month in a row. Hong Kong (+6.4%) again topped the charts, followed by Denmark (+3.2%) and Belgium (+2.5%). In contrast. Israel (-8.2%) , Australia (-4.4%) and the Netherlands (-3.9%) lagged all other developed countries. Year to date, the S&P Developed Markets index (-15.0%) beat US equities by 440 basis points. The toper performing Developed Markets were the United Kingdom (-4.4%), Spain (-5.2%) and Australia (-5.9%). The MSCI Europe Index (-17.2%) also outperformed the S&P 500.

Click to enlarge

Emerging Market Equities

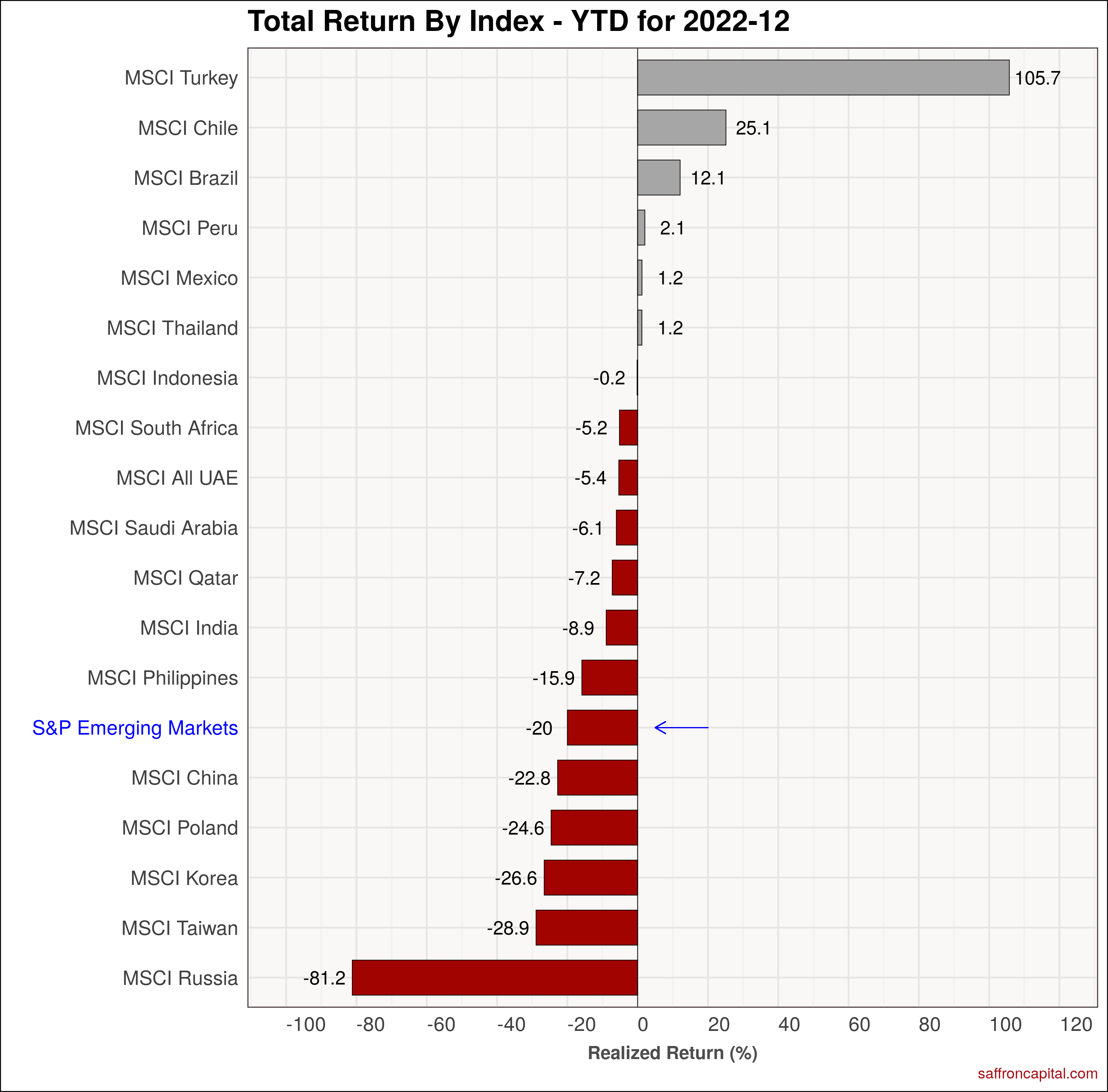

December 2022 return for the the S&P Emerging Markets Index (-2.5%) also beat US market indices. topped all major asset groups. The strongest stock markets were in Turkey (+8.4%), Poland (+4.4%) and Thailand (+3.1%). Meanwhile, results were mixed for China (+2.6%), Brazil (-4.5%) and India (-5.7%). Qatar (-9.7%) had the weakest performance of the Emerging Countries. On a year to date basis, the S&P Emerging Market index (-20.0%) lagging Developed Markets significantly given weakness in Asia.

Click to enlarge

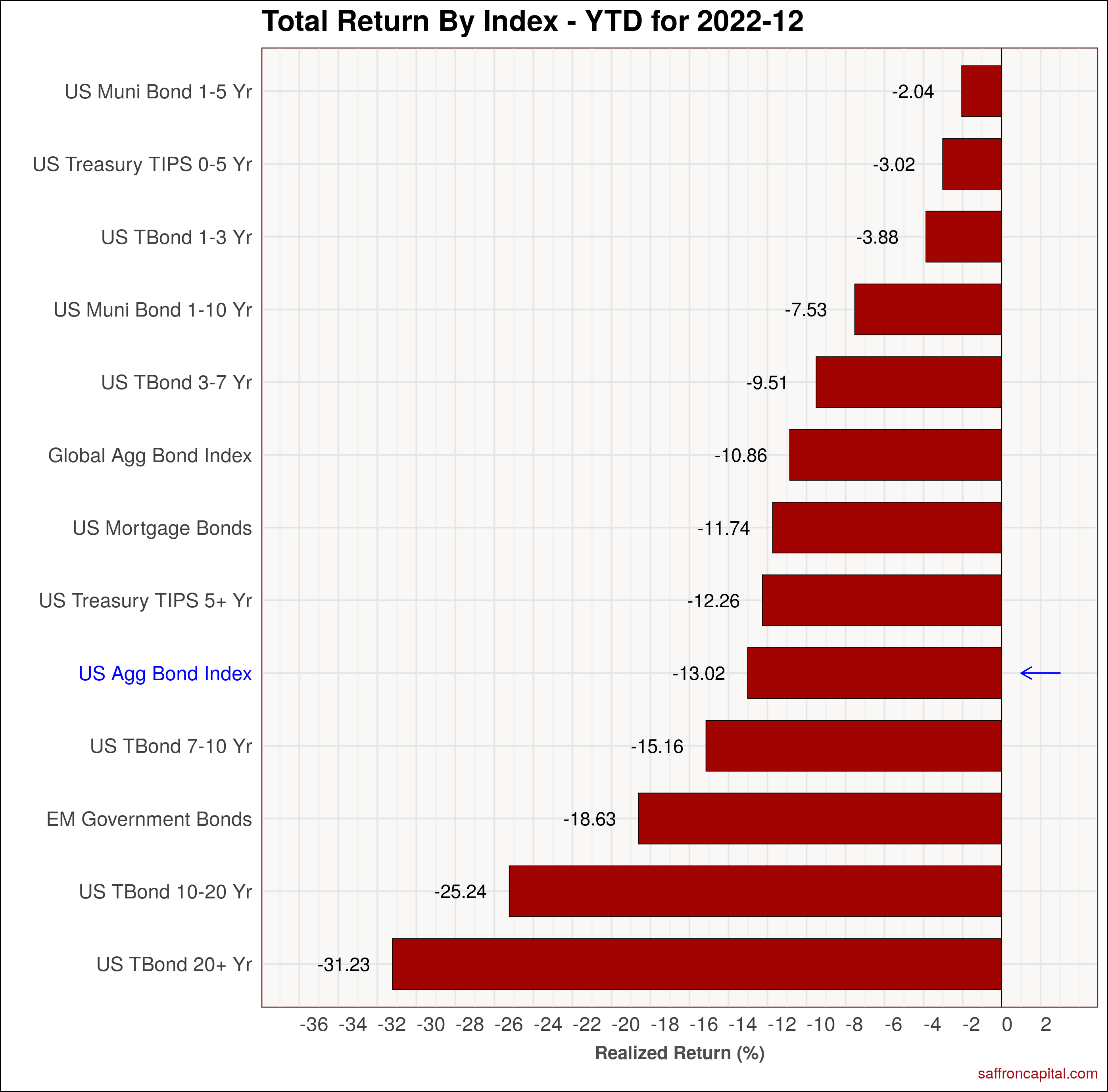

Government Bonds

October returns for government bond markets had modest declines as seen in the U.S. Aggregate Bond Index (-0.95%). At the same time, sovereign bonds for emerging (+1.41%) and developed (+1.27%) economies had modest gains. US Treasuries expiring in 1-3 years were flat, while the belly of the curve expiring 7 years forward (-0.95%) had modest losses. Long dated Treasuries (-5.29%) were clobbered. On a year-to-date basis, the US aggregate Bond index (-1519%) is subject to ongoing pressure and is being pulled down by long duration 20 year plus treasuries (-33.62%) and Treasuries maturing 10 to 20 years (-28.21%).

Click to enlarge

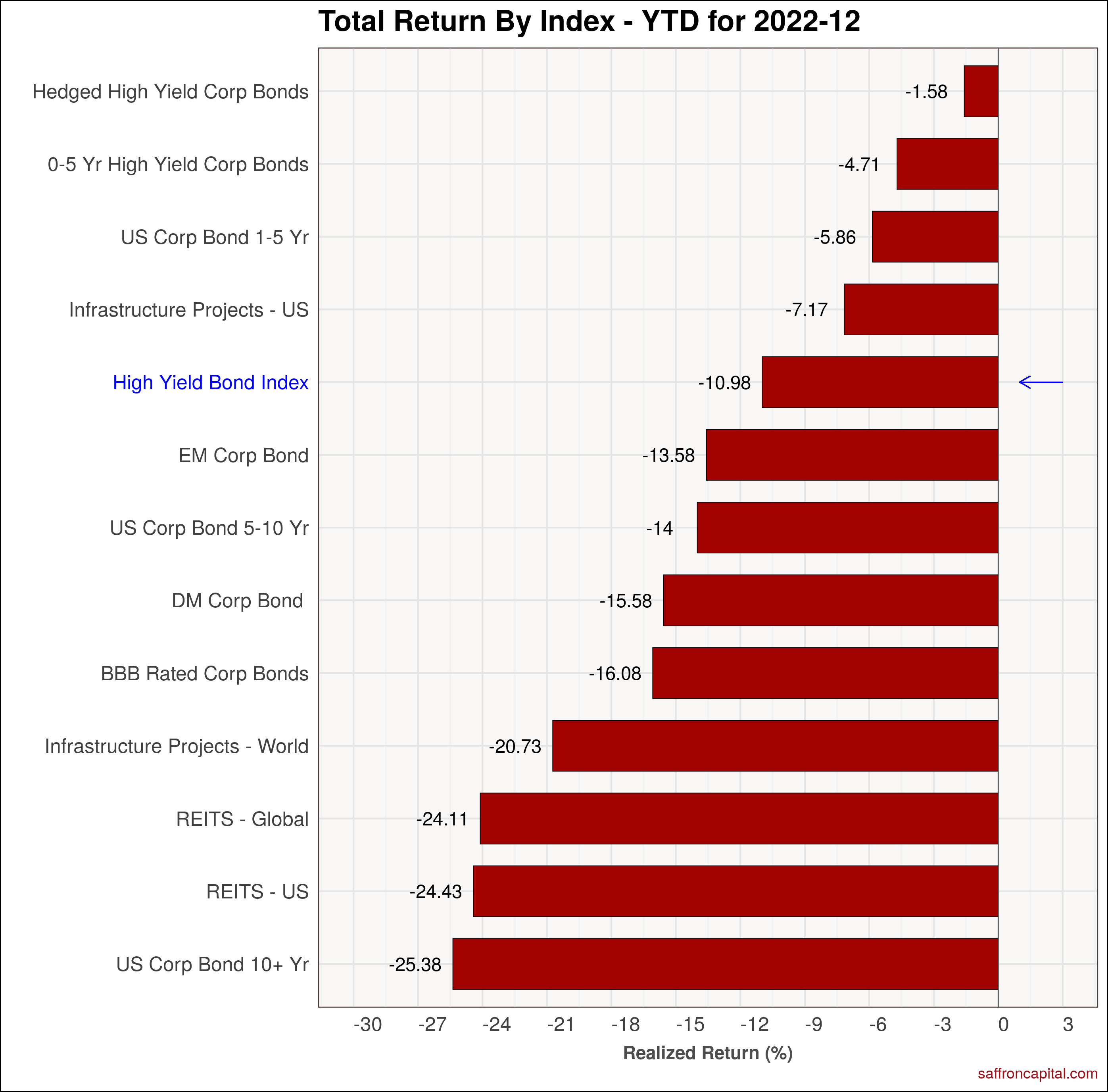

Corporate & Infrastructure Bonds

Developed Market corporate bonds (+1.36%) turned in relative strong returns when compared to the High Yield Bond Index (-1.76%). US Infrastructure project securities (-4.69%) lagged the index, but fared well when compared to international project securities (-17.4%). REITS, in both the US (-5.1%) and abroad (-3.7%) also had negative returns in December. On a year-to-date basis, the benchmark high yield index (-10.6%) was solidly down, but fared much better than corporate equities.

Click to enlarge

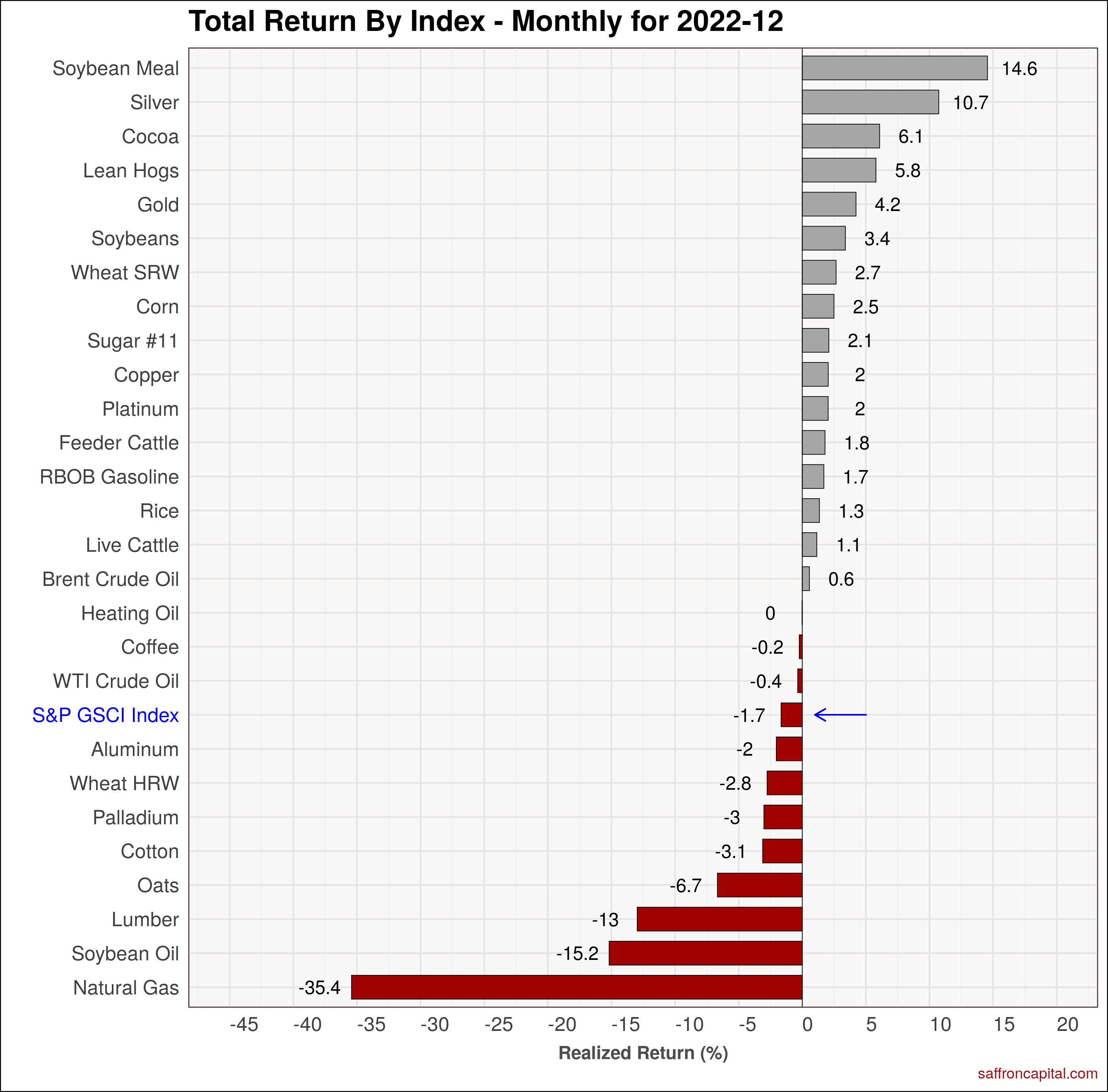

Commodities

December 2022 returns for commodities were mixed and were down on average. The S&P GSCI index (-1.7%) benefited from strong gains in Soybean Meal (+14.8%), Silver (+10.7%), and Cocoa (+6.1%). The weakest commodities in December included Natural Gas (-35.4%), Soybean Oil (-15.2%) and Lumber (-13.0%). Since January of last year, the strongest performing commodities include Heating Oil (+44.3%), Rice (+24.1%), and Natural Gas (+23.4%).

Click to enlarge

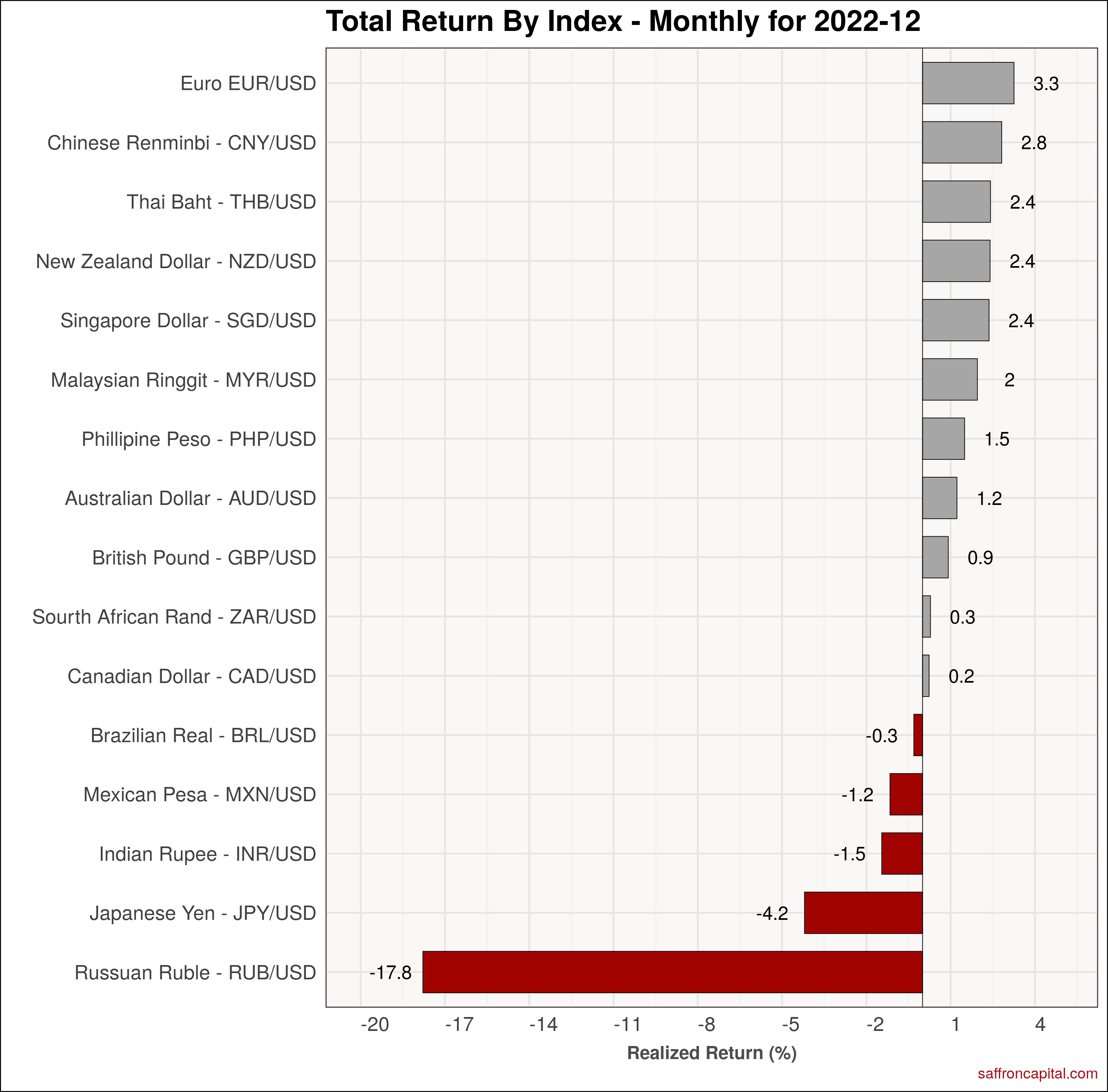

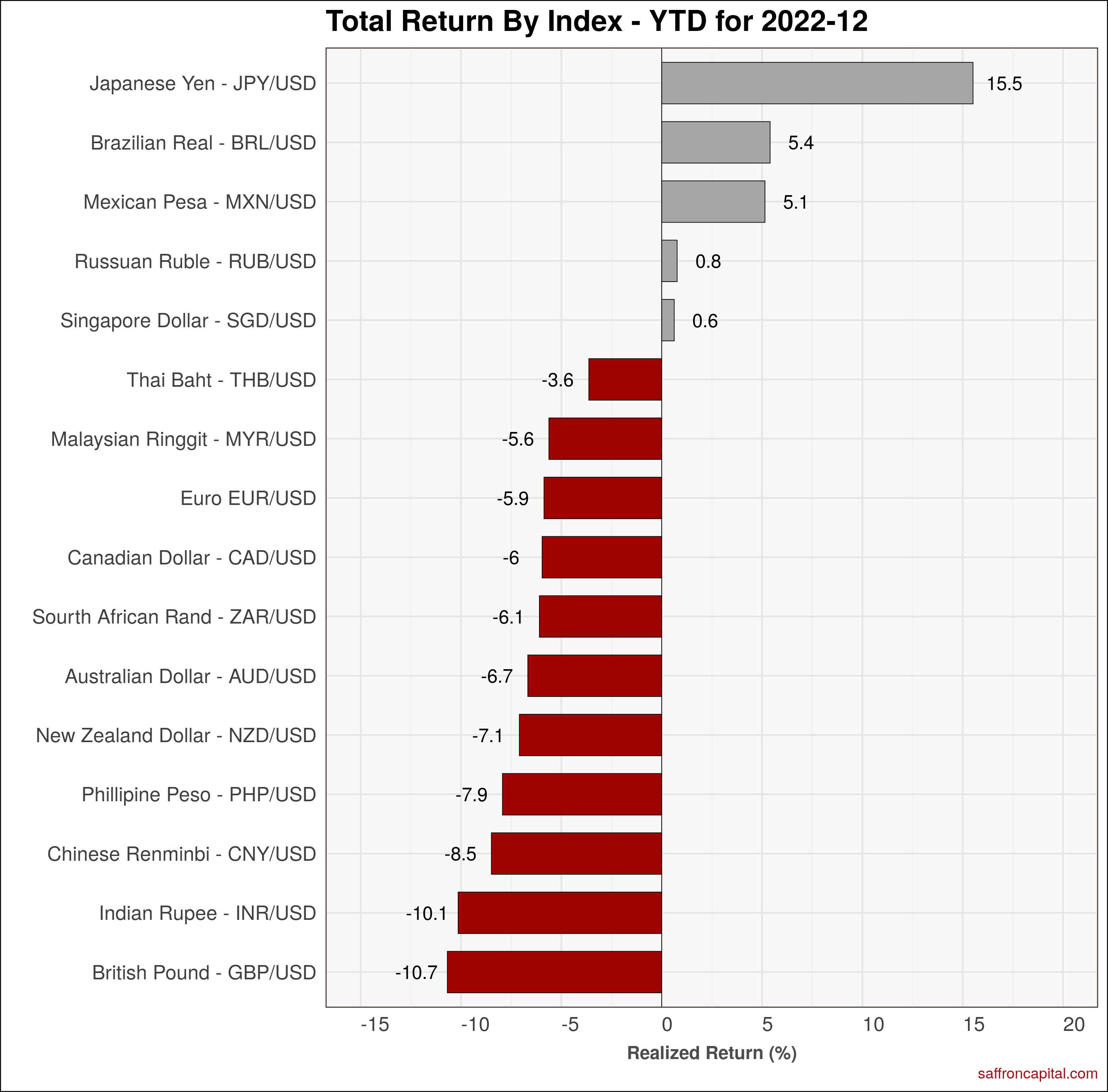

Currencies

The US Dollar was weak in December. Gains were lead by the Euro (+3.3%) and the Chinese Renmibi (+2.8%). The Russian Ruble (-17.8%) was the hardest hit currency, followed by the Japanese Yen (-4.2%). Since January 2022, the strongest currencies have been the Japanese Yen (+15.5%) and the Brazilian Real (+5.4%). The two weakest currencies in 2022 were the British Pound (-10.7%) and th eIndian Rupee (-10.1%).

Click to enlarge

Have questions about the performance of your portfolio? Schedule a meeting with us here.

{kind=link}

{kind=link}

{kind=link}