January 2023 returns will be remembered by investors. The S&P 500 Index was up +6.2% ,while the NASDAQ 100 index was up +10.6%. Meanwhile, international markets clearly outperformed the US. 16 of 22 developed markets had stock market returns higher the S&P 500 index, while 11 of 19 emerging markets beat the US index. In fixed income markets, US real estate (+10.7%) and infrastructure project bonds (+9.25%) topped the charts with strong gains. US Treasuries also continued to rebound, with the 30 year bond (+7.64%) putting in the strongest performance. Among commodities, Lumber (+38.2%) price increases were exceptionally strong, boding well for continued US growth and stock market gains. Finally, the US Dollar (-1.1%) declined in January.

The following analysis provides a visual record of January 2023 returns across and within the major asset classes.

US Equities

The top performing large-cap industrial sectors in January were Consumer Discretionary (+15.1%), Communications Services (+14.8%), Real Estate (+9.9%) and Technology (+9.3%). Private Equity (+13.3%) also had strong returns, rebounding from the bottom of the 2022 performance scorecard. Finally, the S&P 500 Values index (+7.0%) again lead Growth (+5.6%) shares.

Click to enlarge

Developed Market Equities

Elsewhere, the broad index for Developed Market equities (+8.9%) outperformed the S&P 500 Index for a third month in a row. Stock indexes in Ireland (+14.1), Germany (+13.4%), and the Netherlands (+13.35) lead the way. All countries in the MSCI European index (+12.3%) were noticeably strong. In total, 16 of 22 developed markets outperformed the the S&P 500 index in January, rewarding investors with international commitments and diversification.

Click to enlarge

Emerging Market Equities

January 2023 returns for the S&P Emerging Markets Index (+8.9%) also beat US market indices. The strongest stock markets were in Mexico (+16.6%), China (+12.8%), Korea (+12.4%), and Taiwan (+11.6%). Meanwhile, results were mixed India (-1.8%) and UAE (-2.2%). Turkey (-8.4%), a favorite in 2022, was the weakest of the emerging markets in January.

Click to enlarge

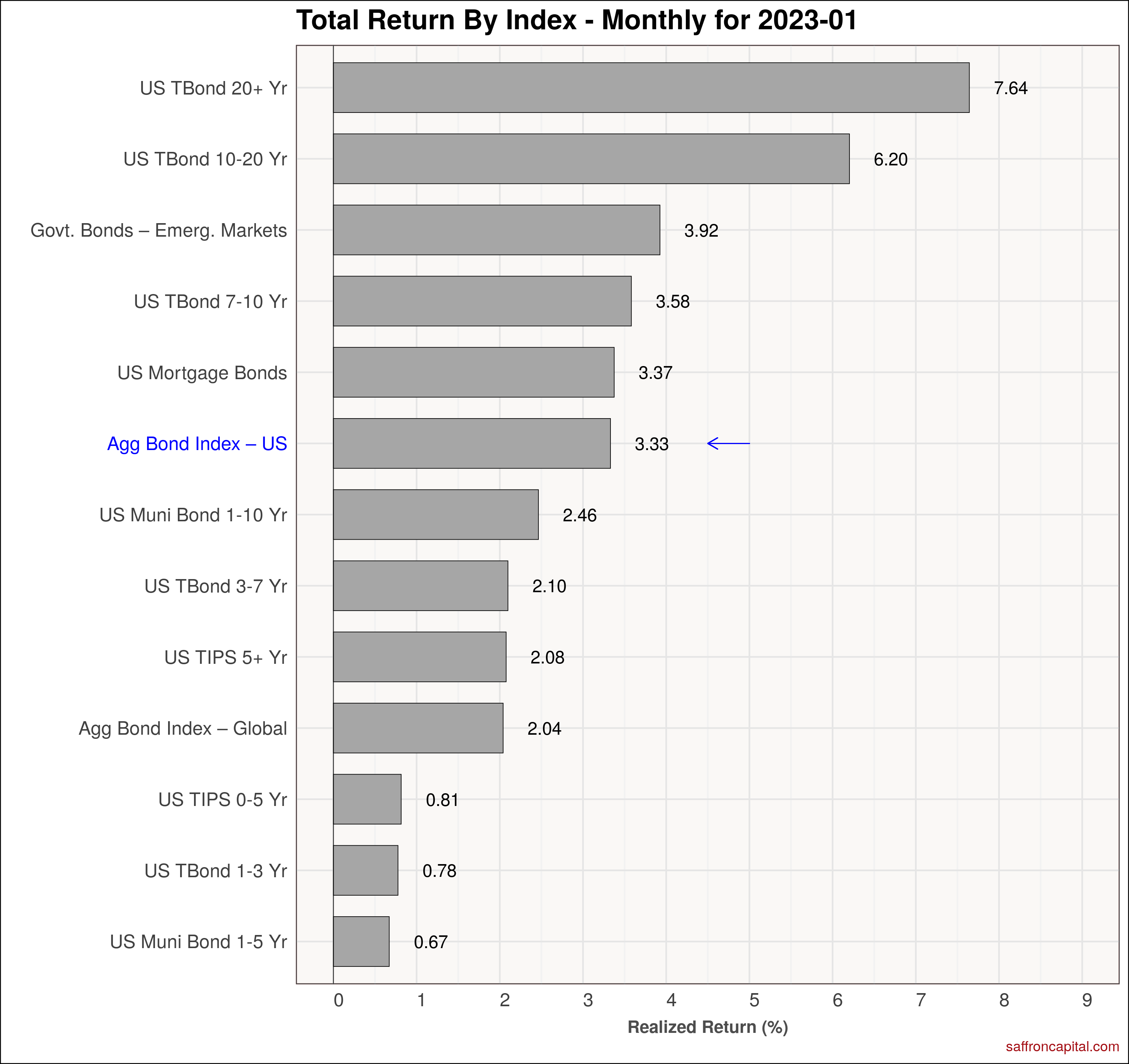

Government Bonds

January returns for government bond markets reversed the steep declines of 2022 and the U.S. Aggregate Bond Index (3.33%) had solid gains. At the same time, sovereign bonds for emerging (+3.92%) and developed (+2.04%) economies also had decent gains. US Treasuries expiring in 20+ years (+7.64%) had stellar gains while inflation protected TIPS (+2.08) with 5 years of more to expire are lagging the aggregate index,

Click to enlarge

Corporate & Infrastructure Bonds

The iBoxx Corporate Bond Index (+3.67%) also had solid fixed income gains. International infrastructure project securities (+14.04%) greatly outperformed the corporate bond index, US equities, and even US infrastructure bonds (+9.25%). Real estate investment Trusts (REITS), both US (+10.7%) and international (+9.47%), also did well in January.

Click to enlarge

Commodities

January 2023 returns for commodities were broadly mixed. The S&P GSCI index (-0.1%) masked the wide range of results. For example, Lumber (+38.2%), Copper (+10.5%) and Aluminum (+7.7%) benfirted from strong US growth and post-covid reopening in Asia. The weakest commodities in January included Natural Gas (-40.2%), Lean Hogs (-14.3%) and Palladium (-9.4%). Gasoline (+1.6%) continued to increase on refining capacity issues, even though crude oil (-2.9%) was relatively weak.

Click to enlarge

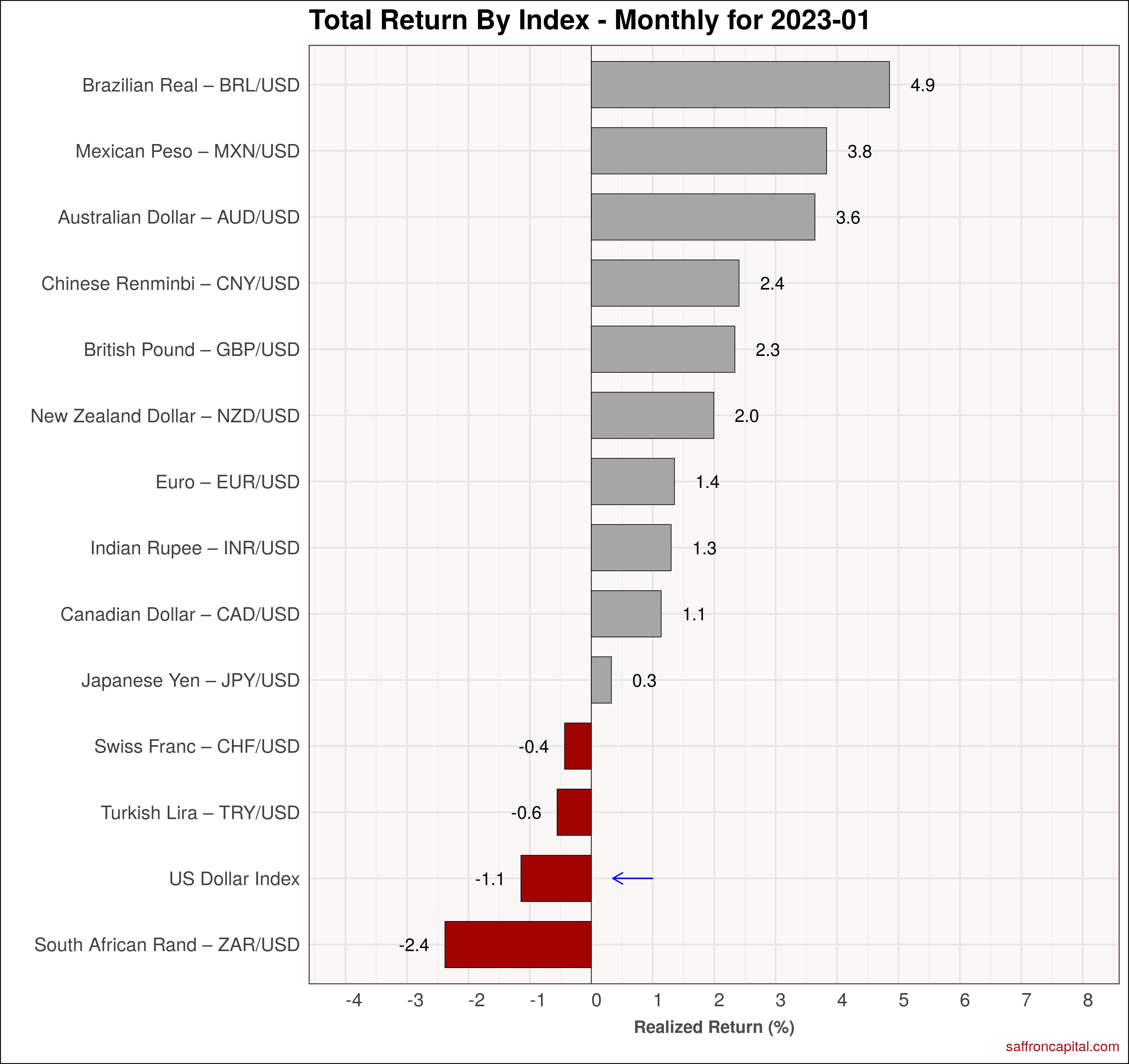

Currencies

The US Dollar weakness (-1.1%) continued from December. Currency gains were lead by the Brazilian Real (+4.9%) and the Mexican Peso (+3.8%). The South African Rand (-2.4%) was the weakest of the reported currencies, followed by the Turkish Lira (-0.6%).

Click to enlarge

Have questions or concerns about the performance of your portfolio? Schedule a meeting with us here.

{kind=link}

{kind=link}

{kind=link}