Strong GDP growth in the third quarter is the backdrop for October 2023 market returns. Still, the U.S. equity markets fell last month, the third monthly loss in a row. Meanwhile, key drivers included mixed third quarter earnings results, surging long-dated yields, and geopolitical tensions, all of which hit all US equity indices. In October, the S&P 500 was down 2.2% and the NASDAQ-100 index was down 2.1%.

Fixed income markets were also down in October. However, the Aggregate Bond Index for US Treasuries (-1.57%) and the iBOXX Corporate Bond Index (-1.04%) both fared better than equities. In comparison, the S&P Commodities Index (-3.9%) masked a wide variety of returns, with Natural Gas (+22.1%) rising rapidly and Crude Oil (-10.8%) under pressure.

The following analysis provides a visual record of October 2023 returns across and within the major asset classes.

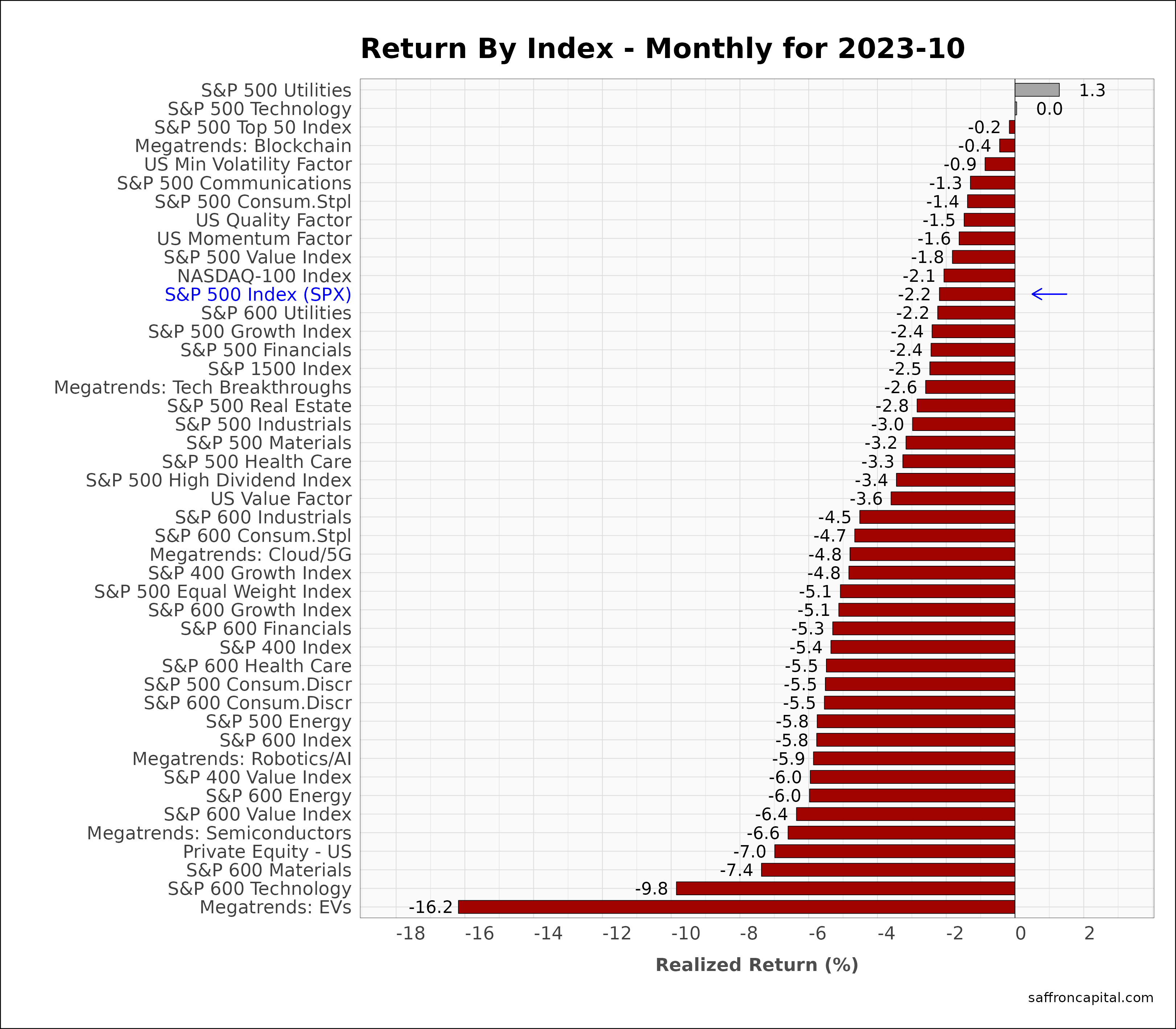

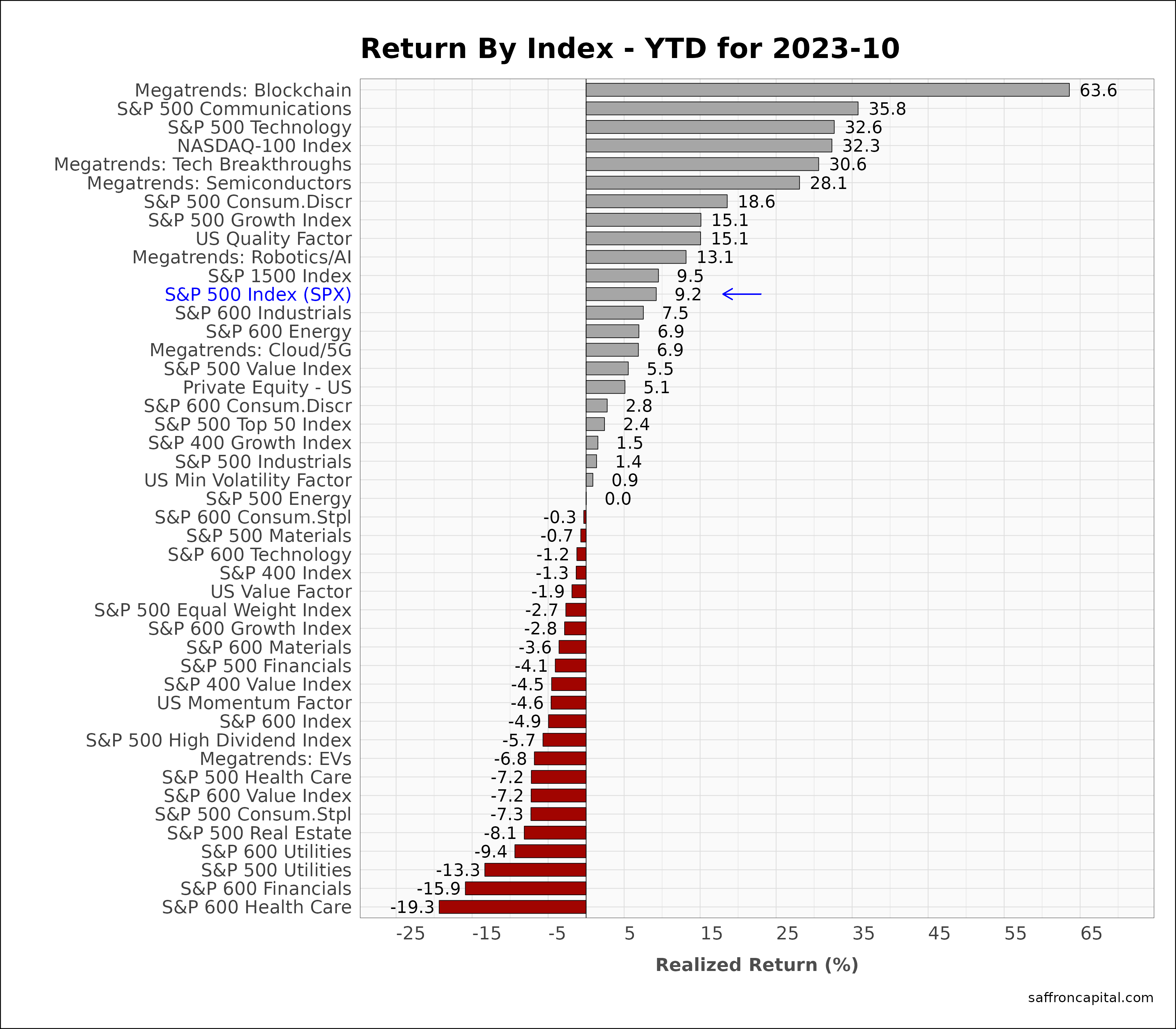

US Equities

Large-cap Utilities (+1.3%) and Technology (0.0%) shares where the only sectors to avoid red ink in October. As one would expect in a declining market, the best relative performance came from defensive strategies. For example, Minimum Volatility or low beta stocks (-0.9%) had solid relative performance. At the same time, the hardest hit were shares included megatrend Electric Vehicle (-16.2%), small cap Technology (-9.8%), and small cap Materials (-7.4%). Large cap Energy (-5.8%) tracked lower with crude oil prices.

Year-to-date (YTD) returns are also presented for the the first 10 months. The S&P 500 Index (+9.2%) continues to perform well, while the NASDAQ-100 Index (+32.3%) has significantly outperformed. In comparison, the S&P 400 Mid-Cap Index (-1.3%) and the S&P 600 Small Cap Index (-4.9%) have not fared as well, confirming that market breadth remains weak. A wide dispersion of results is also seen by sector, with Technology shares (+32.6%) at the top of the list and Utilities (-13.3%) at the bottom.

Click to enlarge

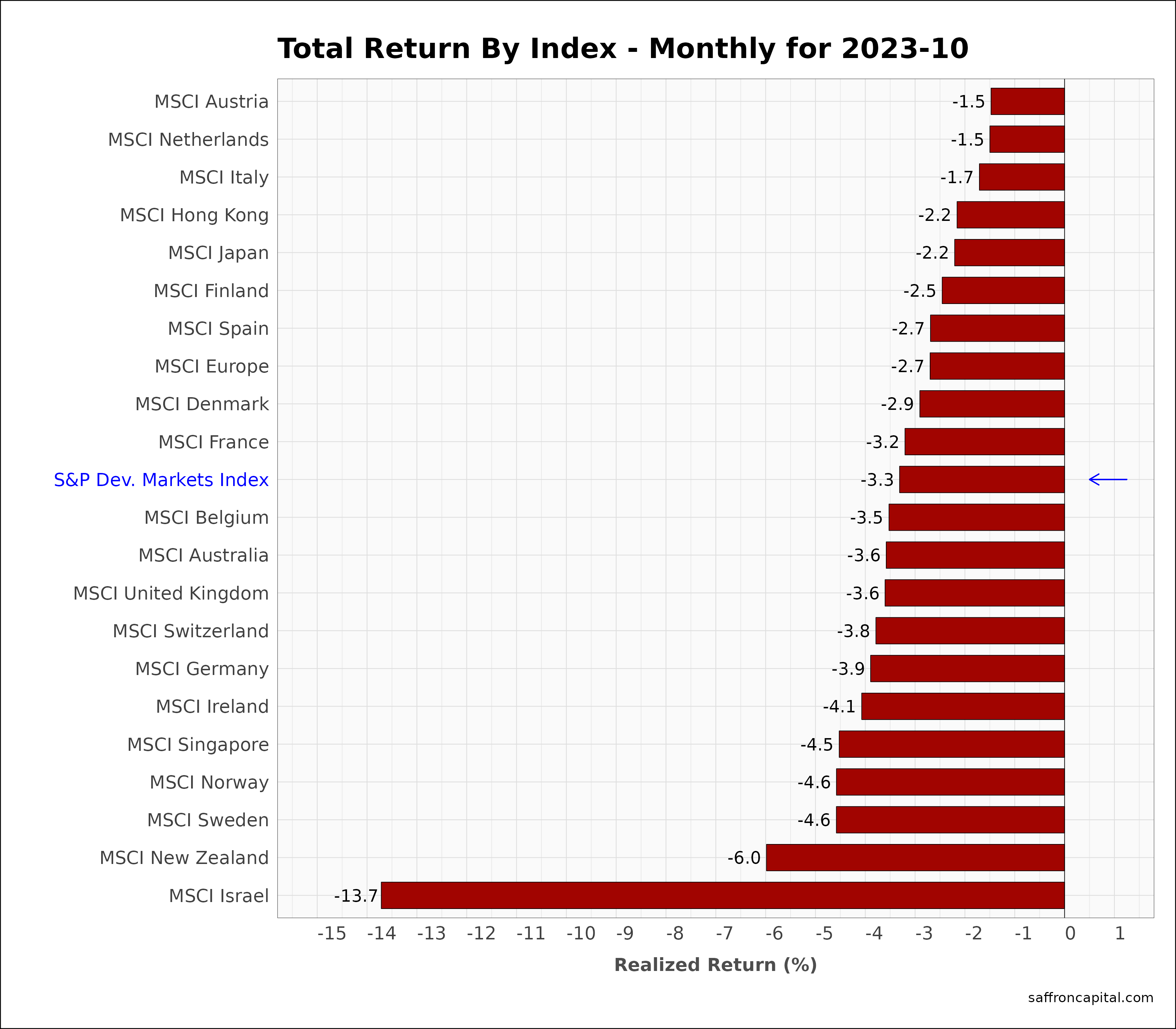

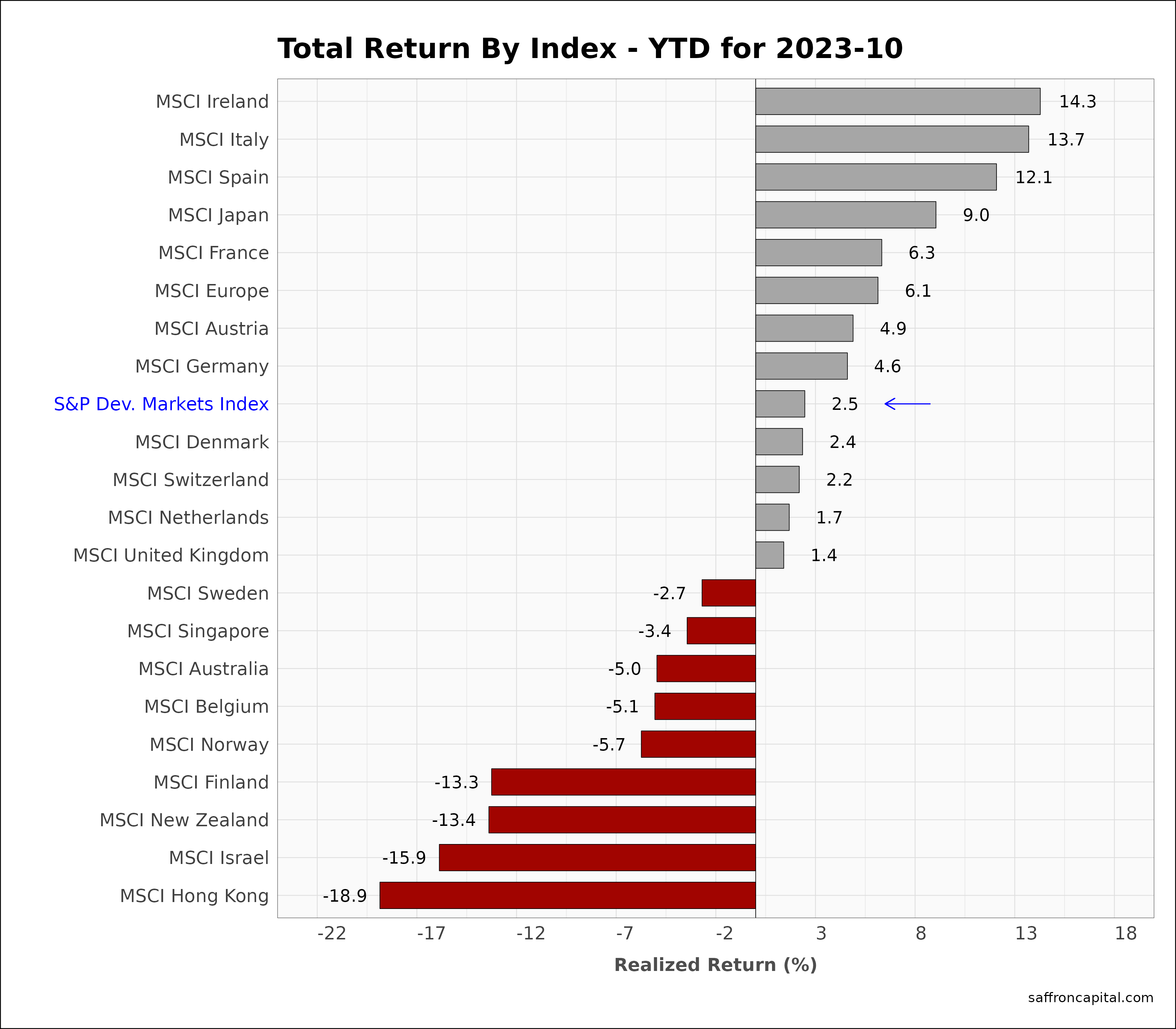

Developed Market Equities

International developed markets (-3.3%) in October were all broadly down. Austria (-1.5%), the Netherlands (-1.5%), and Italy (-1.7%) all outperformed the US S&P 500 Index. Japan (-2.2%) was flat to the US benchmark, while the United Kingdom (-3.6%) and Germany (-3.9%) both lagged the asset group. The worse performing market was Israel (-13.7%).

For the first 10 months, developed markets (+2.5%) remain positive. The best performers continue to lead the S&P 500 index year-to-date, notably Ireland (+14.3%), Italy (+13.7%), and Spain (+12.1%). Japan (+9.0%) is running flat to US large cap market, while Hong Kong (-18.9%) has widened its lag behind the group.

Click to enlarge

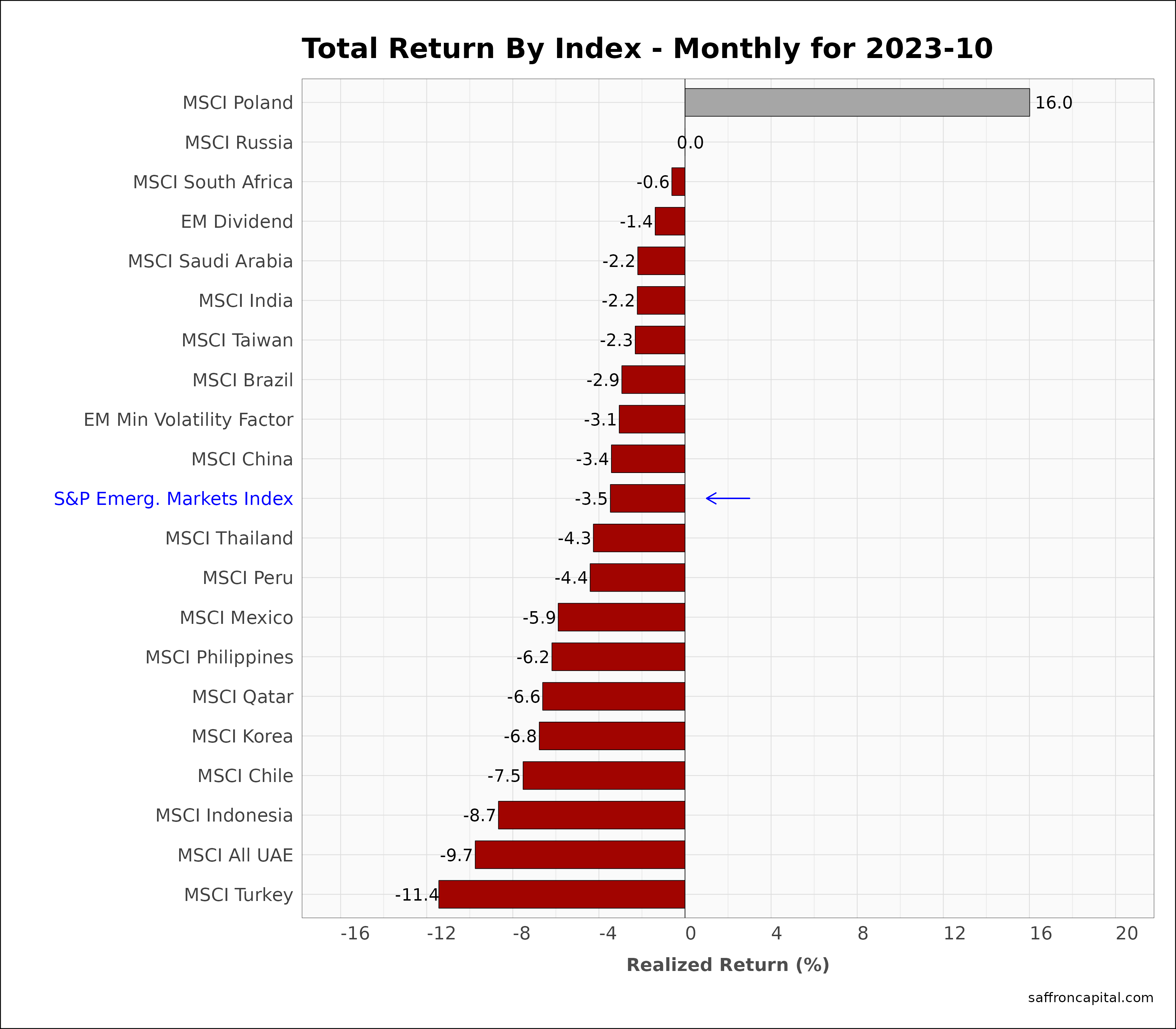

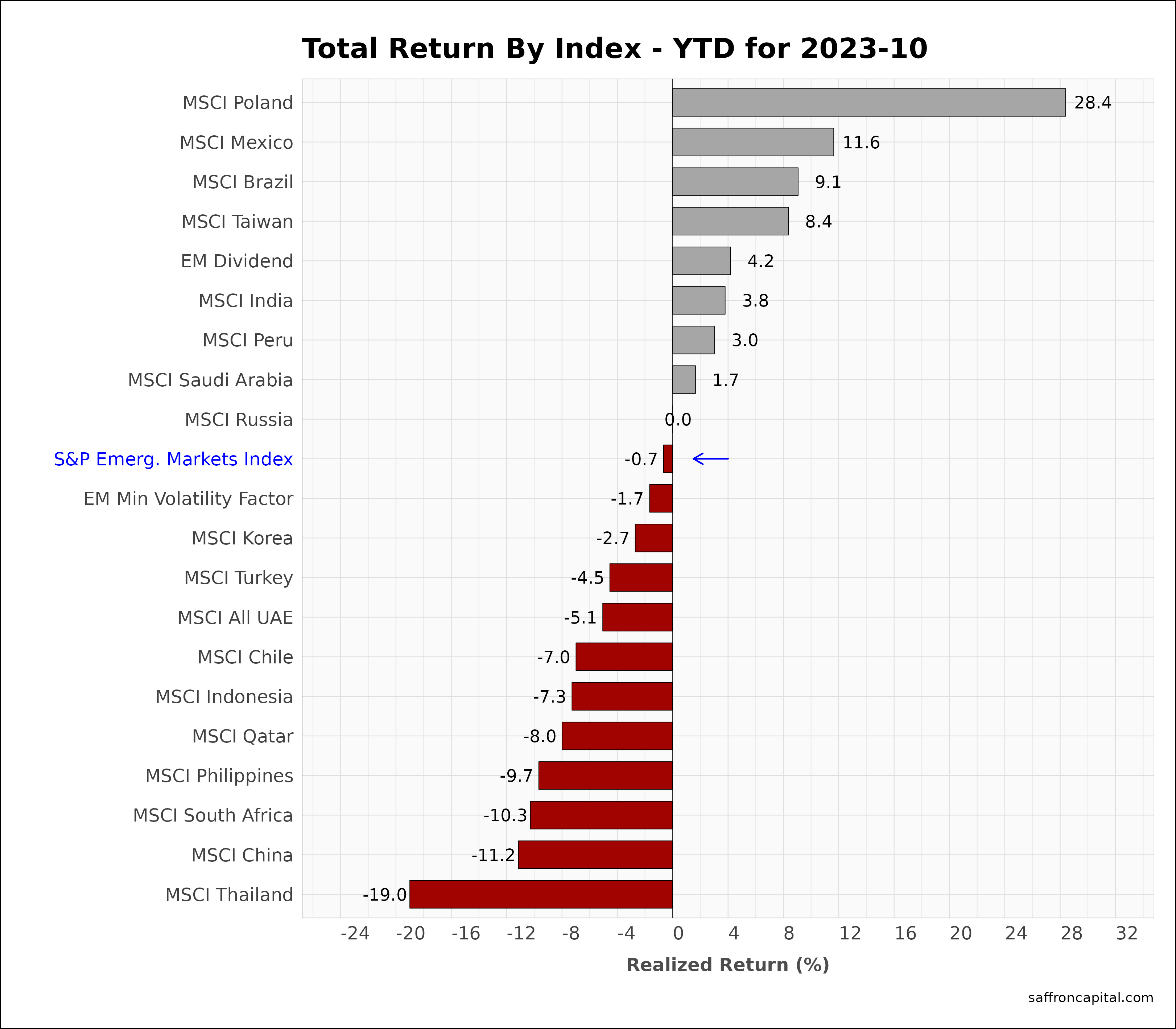

Emerging Market Equities

October 2023 returns for the S&P Emerging Markets Index (-3.8%) also fell victim to higher yields. However, the Polish stock market (+16.0%) is the world’s best performing equity group in October. Both India (-2.2%) and China (-3.4%) beat the group index in October, while Mexico (-5.9%) Korea (-6.8%), and Turkey (-11.4%) lagged the group. The top performers year-to-date are Poland (+28.4%), Mexico (+11.6%) and Brazil (+9.1%).

Click to enlarge

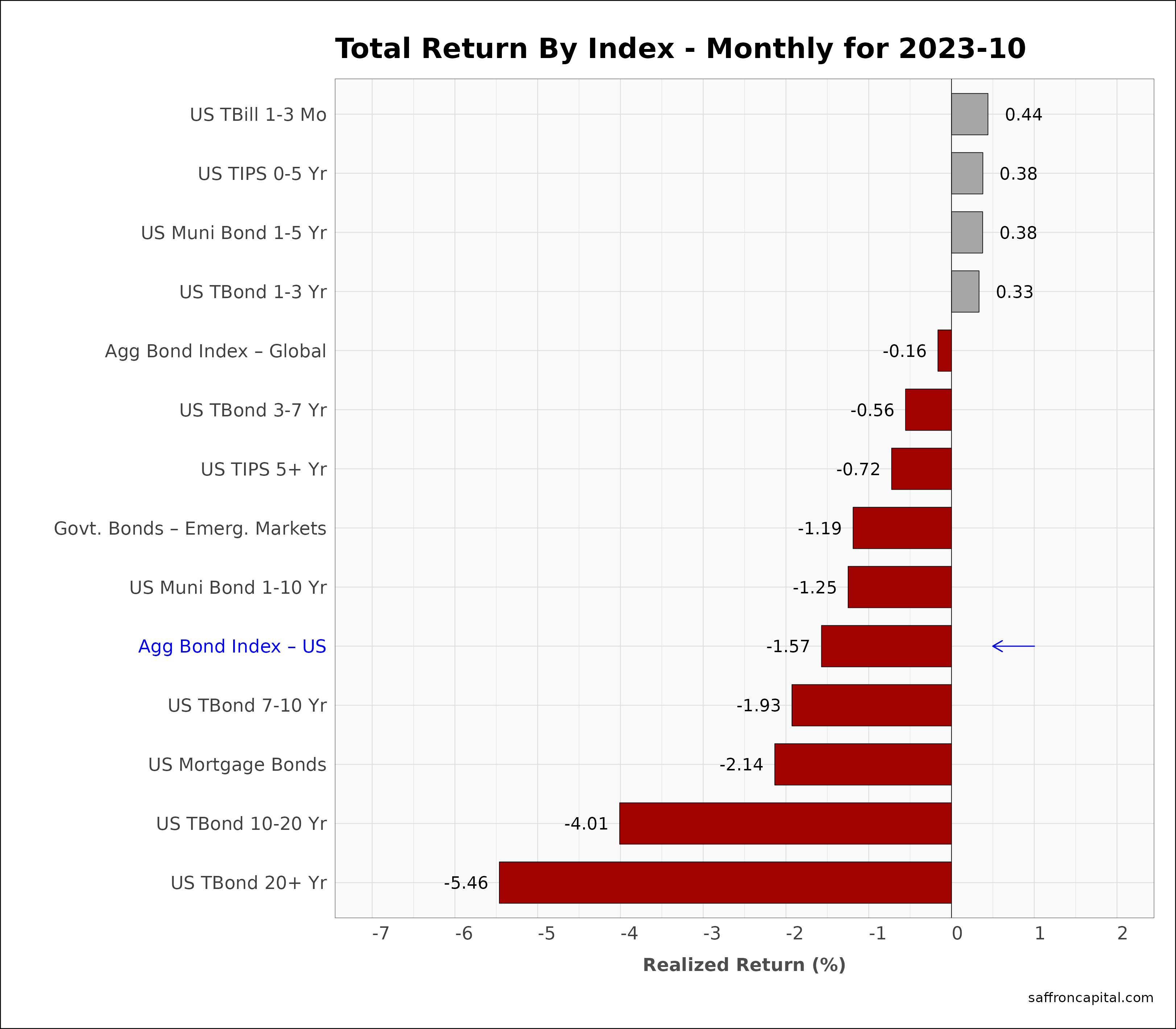

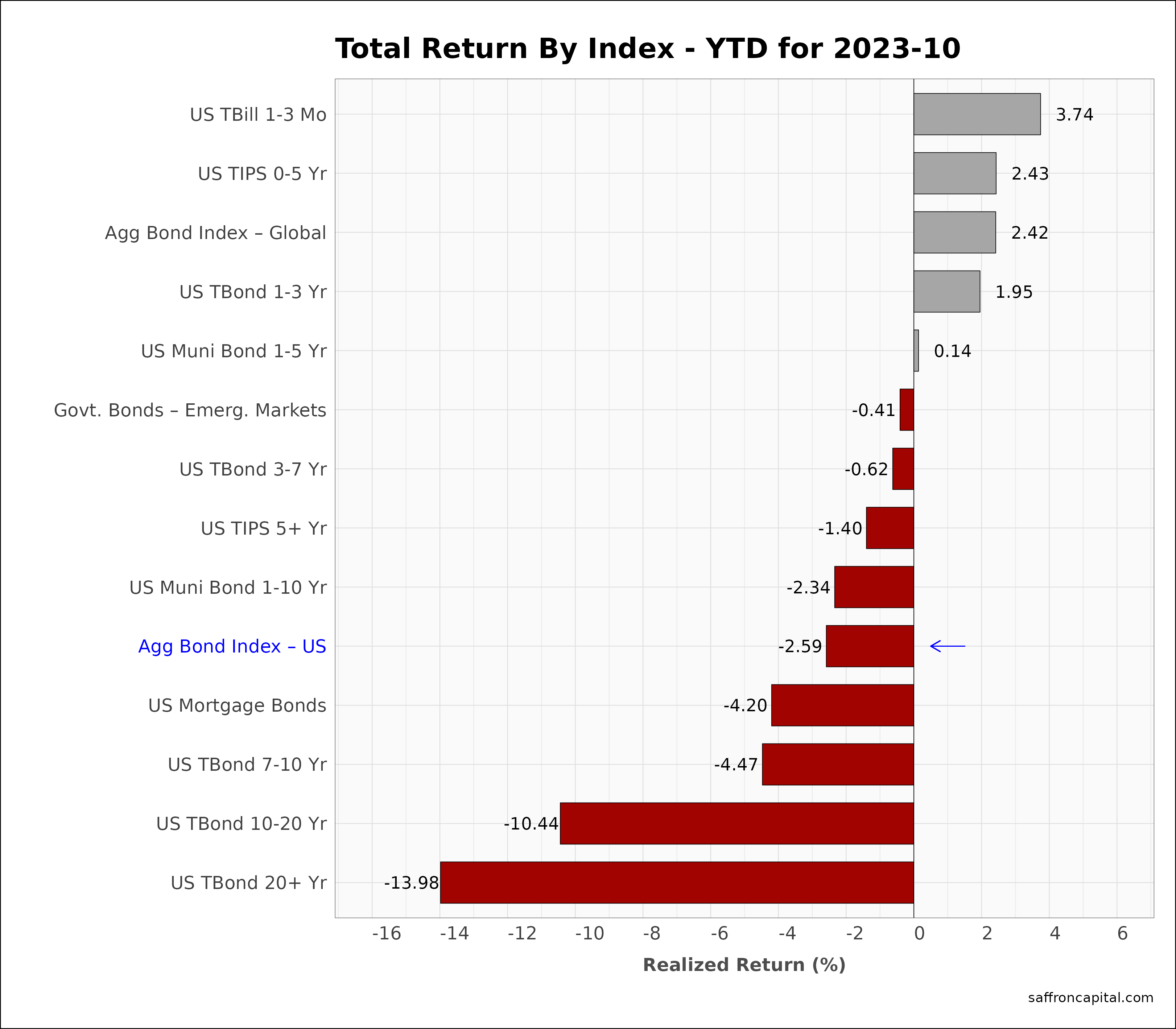

Government Bonds

Returns for the Aggregate US Government Bonds Index (-1.57%) showed that negative momentum was unabated in October. The front of the yield curve saw positive returns as seen by short-term T-Bills (+0.44%), US TIPS 0-5 years (+0.38%), Municipal bonds 1 to 5 years (+0.38), and T-Notes 1-3 years (+.33%). However, the back-end of yield curve proved volatile with the US T-bond for 20 years (-5.46%) down significantly. Since January, returns for the Aggregate US Bond index (-2.59%) are yet to match realized inflation in 2023. Short-term T-Bills (+3.74%) lead the group, while the the 20 year T-Bond (-13.98) has burnt cash like a furnace, proving how difficult 2023 has been for investors without active risk control.

Click to enlarge

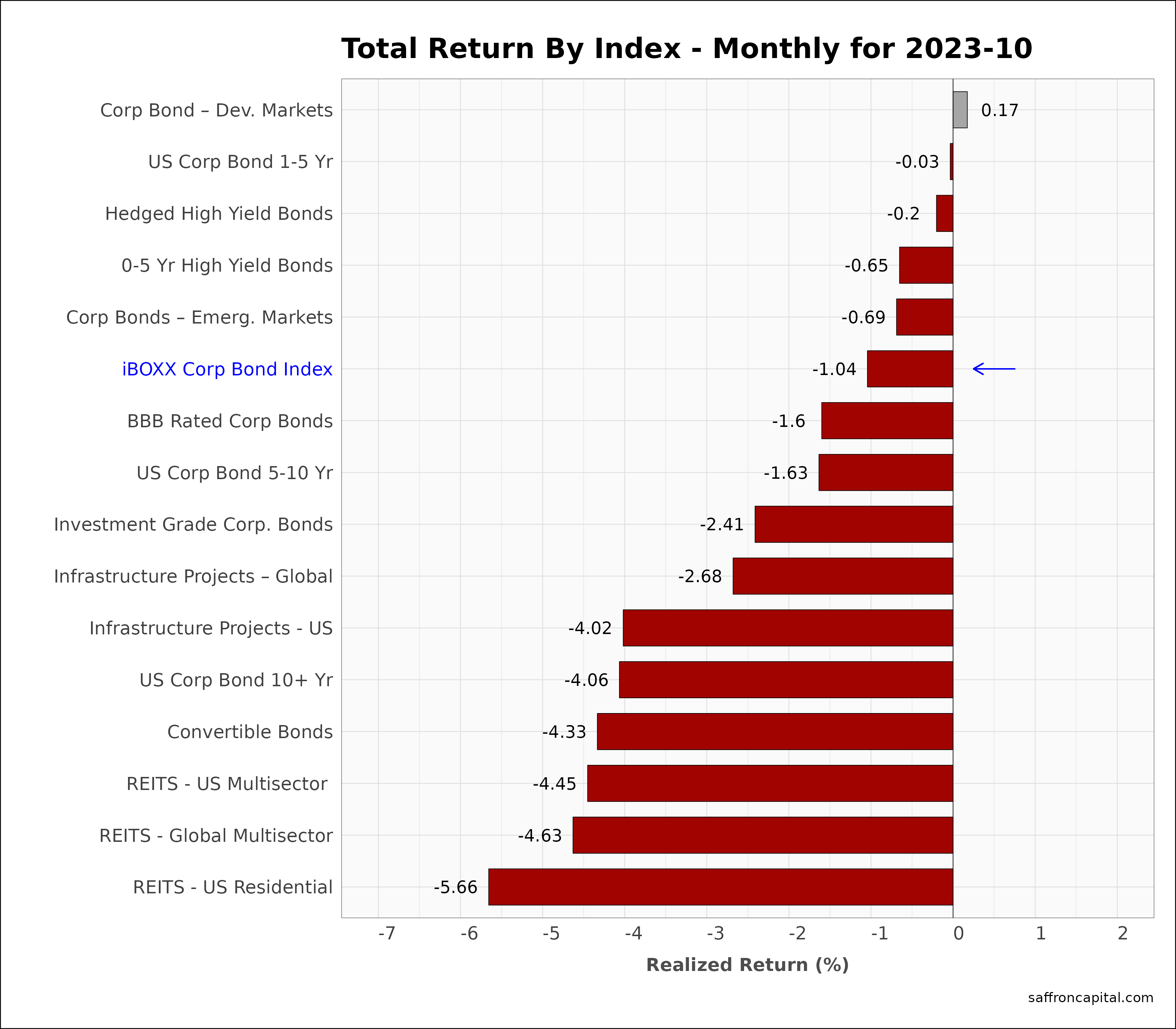

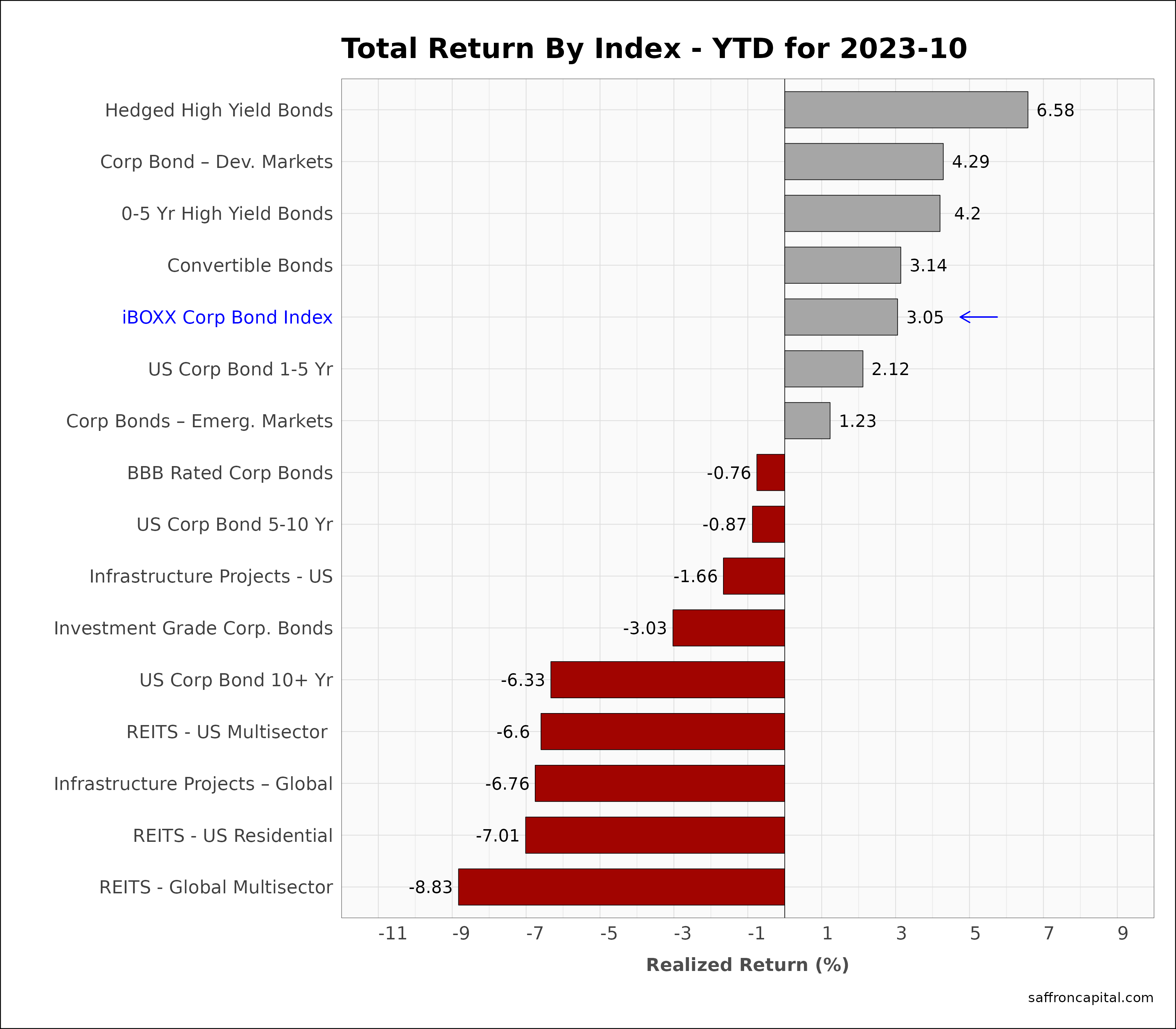

Corporate & Infrastructure Bonds

The iBoxx Corporate Bond Index (-1.04%) again outperformed Treasury bonds in August. Performance was lead by international corporate bonds (+0.17%), short-term Corporate bonds 1 to 5 years (-0.03%), and Hedged High Yield Bonds (-0.2%). Global Infrastructure Project Bonds (-2.68%) and US Infrastructure Bonds (-2.68%) continued their multi-month declines. Finally, Real Estate Investment Trusts (REITS) all trailed the group, regadless of type. Looking at year-to-date performance, the best returns were generated by Hedged High Yield Bonds (+6.58%), international corporate bonds (+4.29%) and short-term 0-5 Yr High Yield Bonds (+4.2%).

Click to enlarge

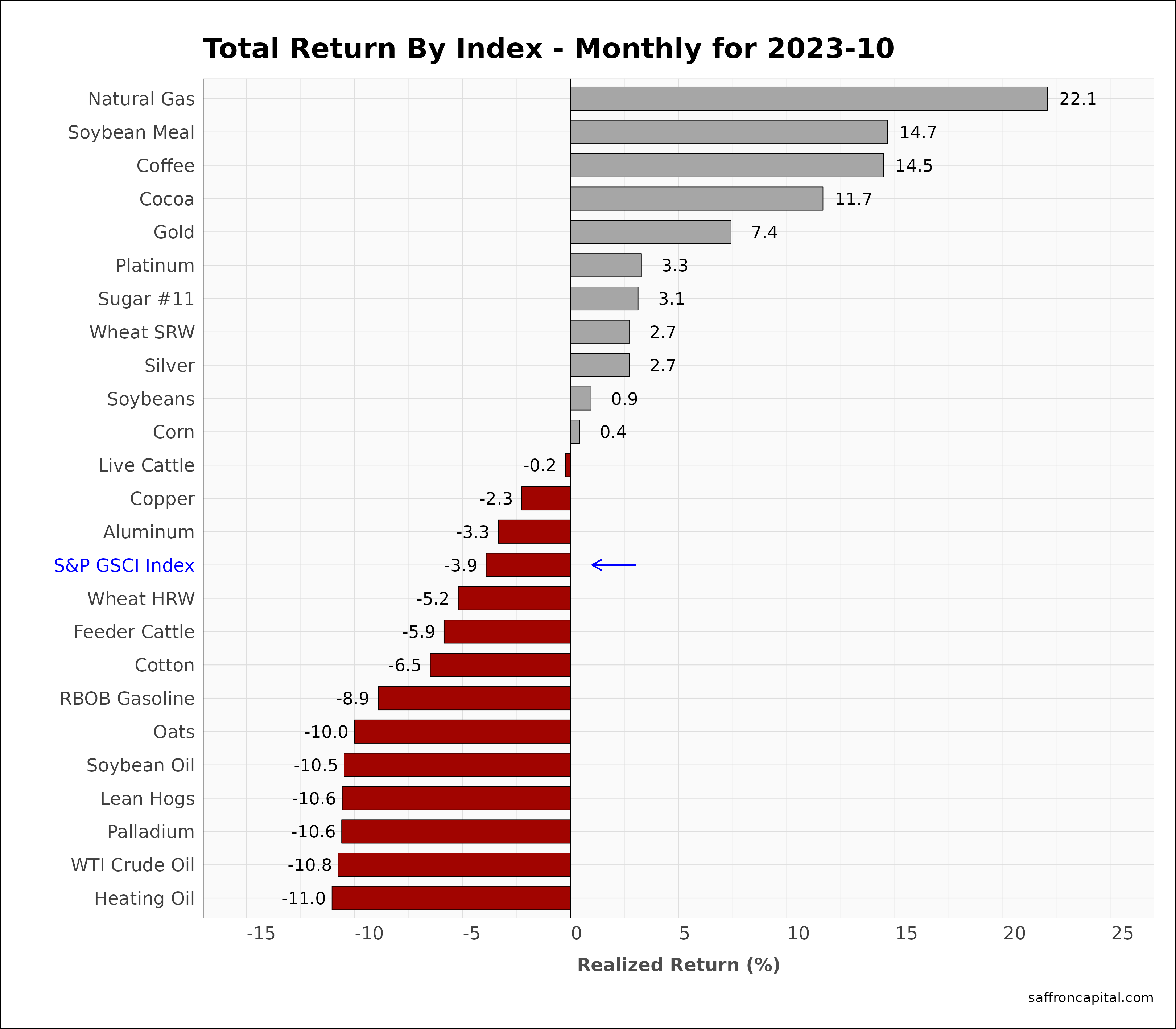

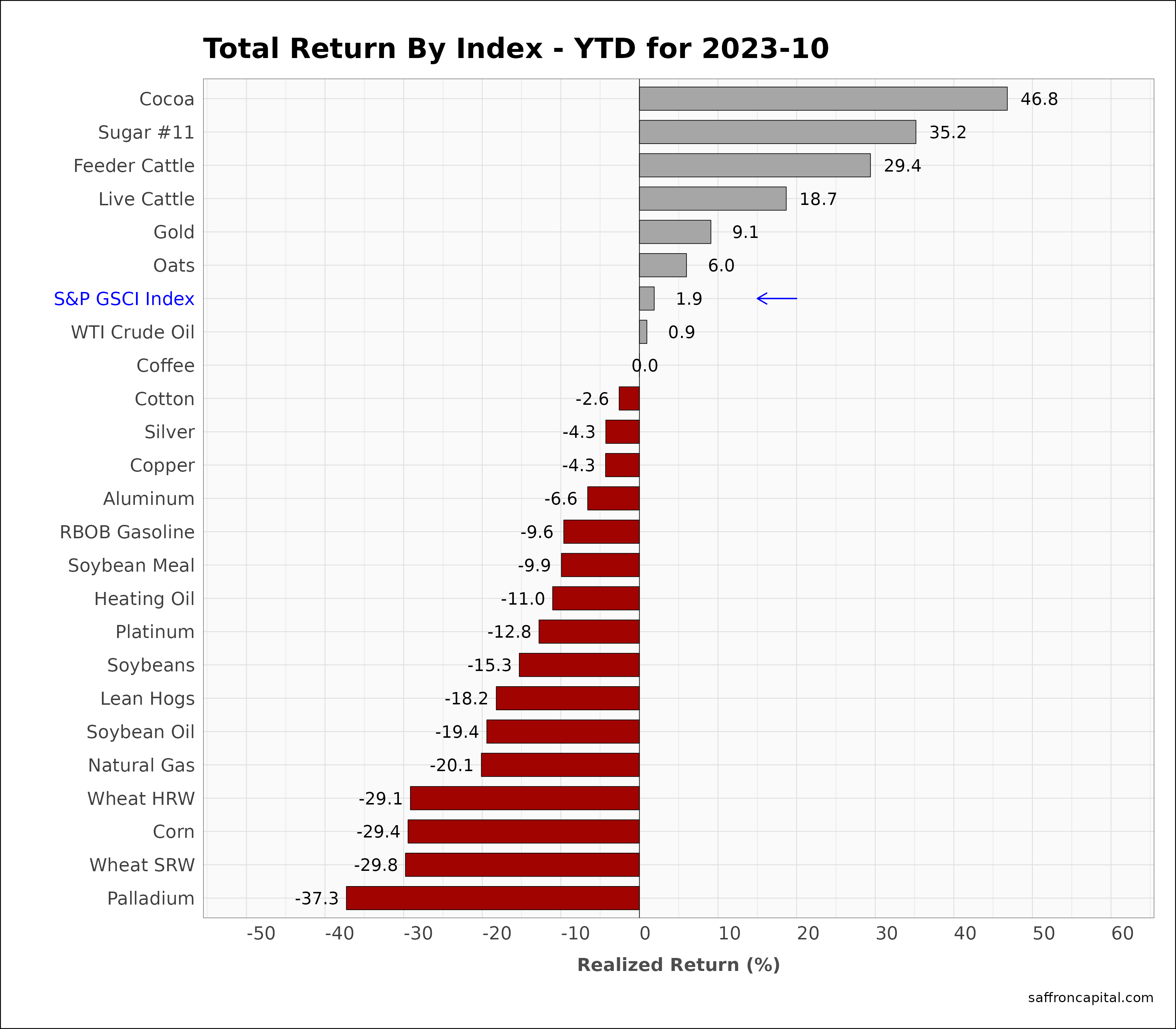

Commodities

October 2023 returns for the S&P GSCI index (-3.9%) confirmed a trend for falling raw material prices, but with highly variable results. For example, Natural gas (+22.1%), Soybean Meal (+14.7%) and Coffee (+14.5%) outpaced the group, while Heating Oil (-11.0%), Crude Oil (-10.8%), and Palladium (-10.6%) were all weak. Year-to-date results for the commodity index (+1.9%) has declined over 500 basis points in the past 2 months. Tropical commodities, including Cocoa (+46.8%) and Sugar (+35.2%) lead the group, along with US Feeder Cattle (29.4%). Grains are trailing the group following recent harvest results.

Click to enlarge

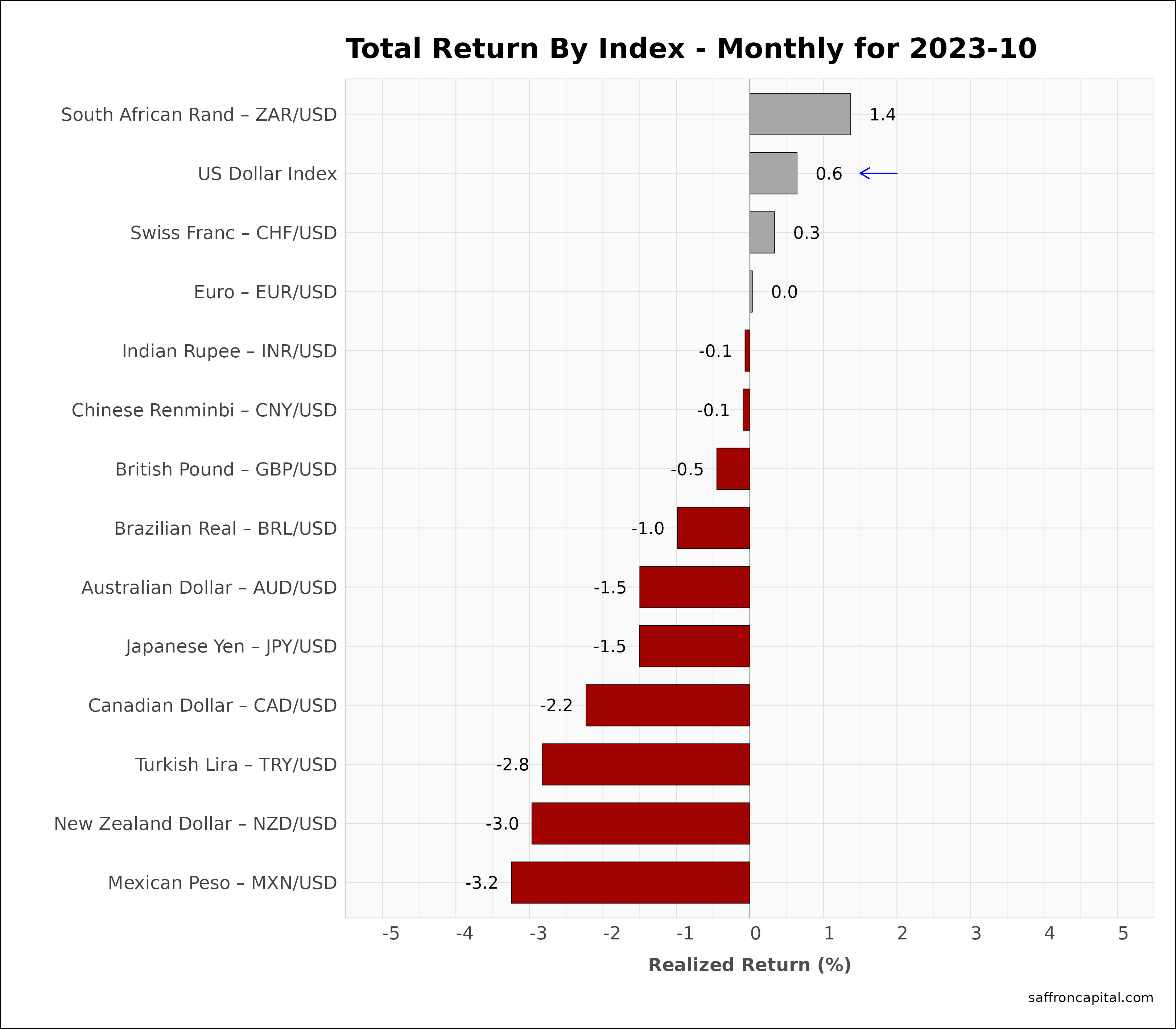

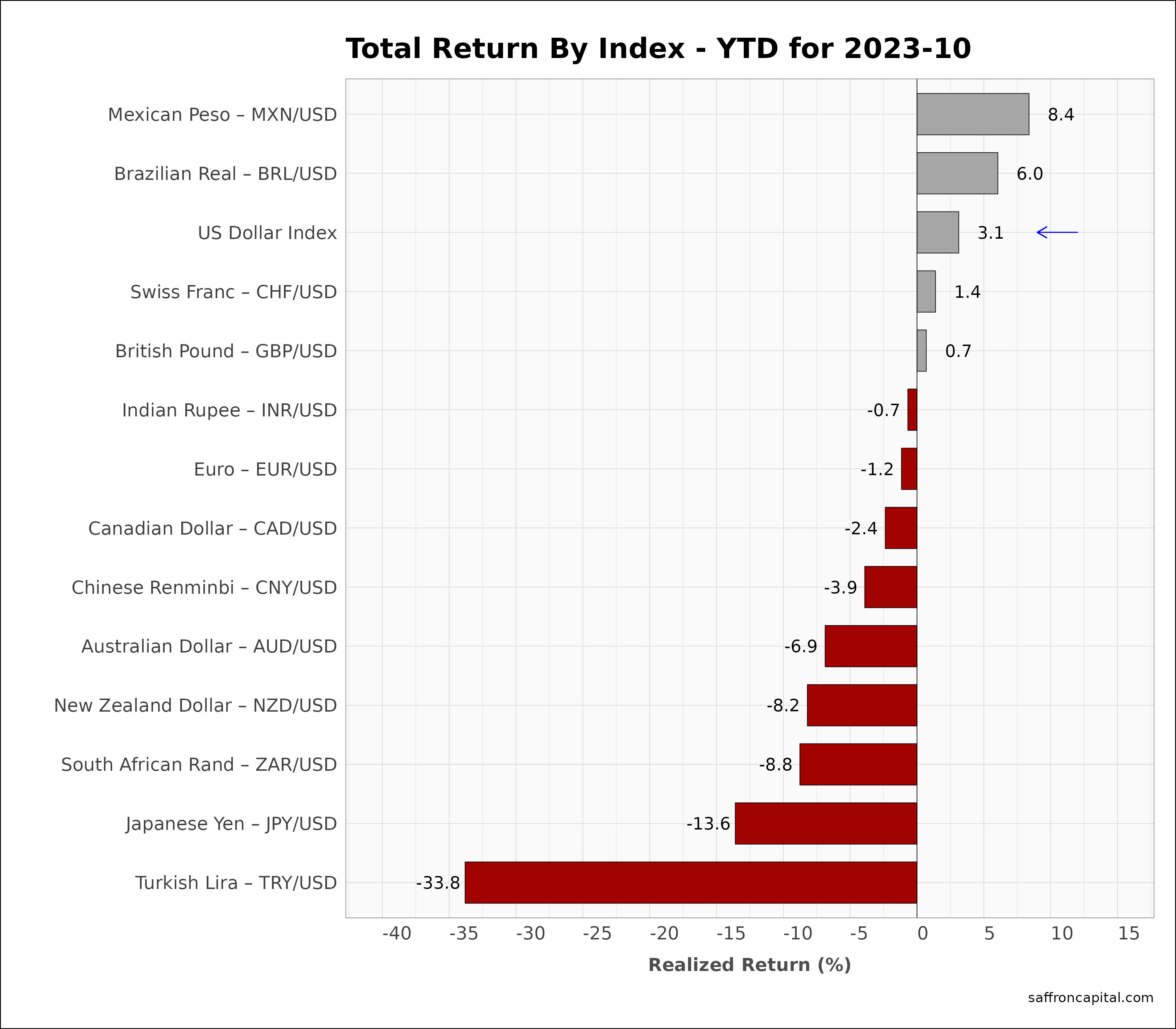

Currencies

Finally, the US Dollar (+0.6%) was near unchanged for the month, but continues to be in an uptrend year-to-date (+3.1%). Since January, the Mexican Peso (+8.4%) has been the strongest currency, while the weakest has been the Turkish Lira (-33.8%).

Click to enlarge

Have questions or concerns about the performance of your portfolio? Whatever your needs are, we are here to listen and to help. Schedule time with us here.

{kind=link}

{kind=link}