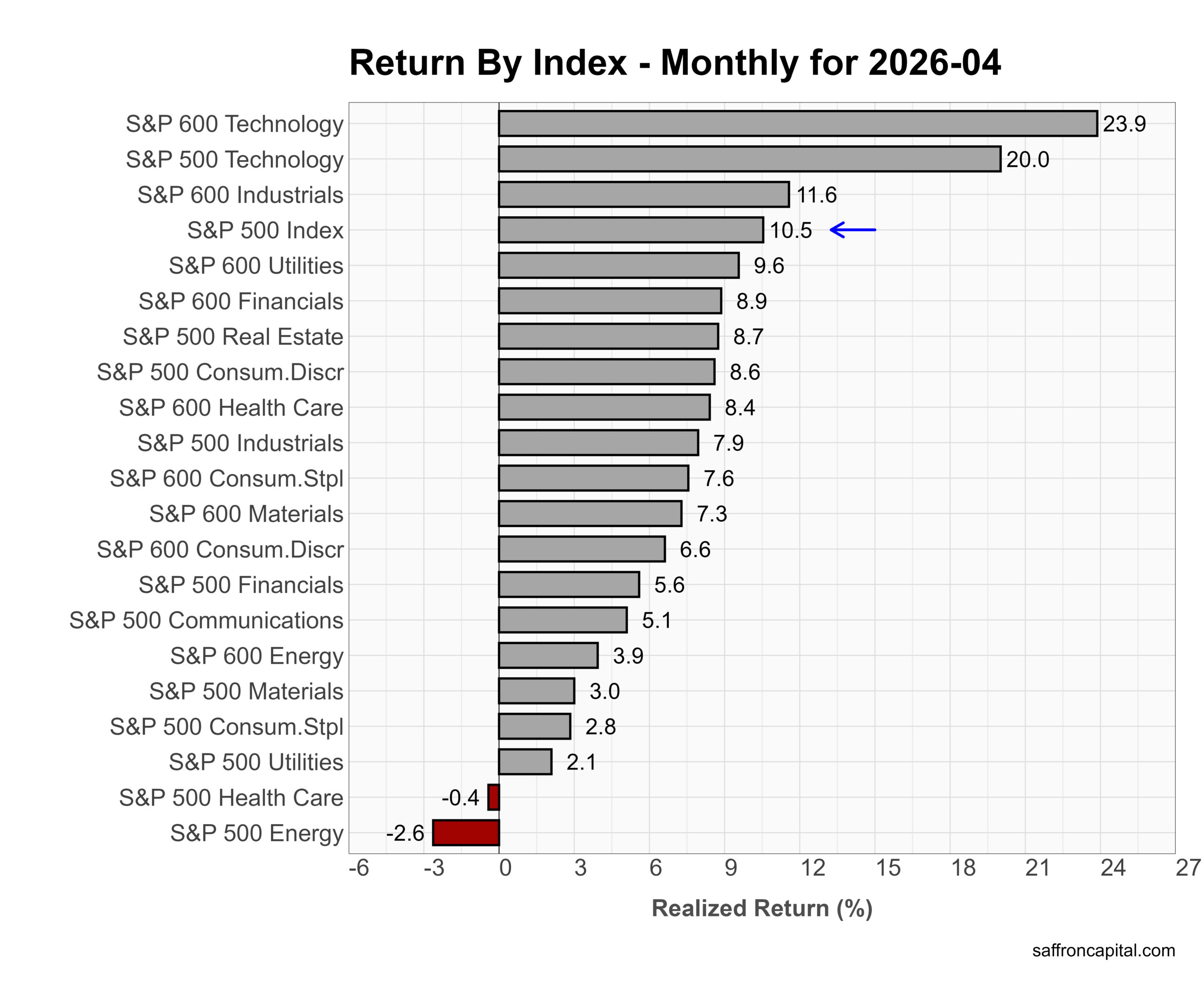

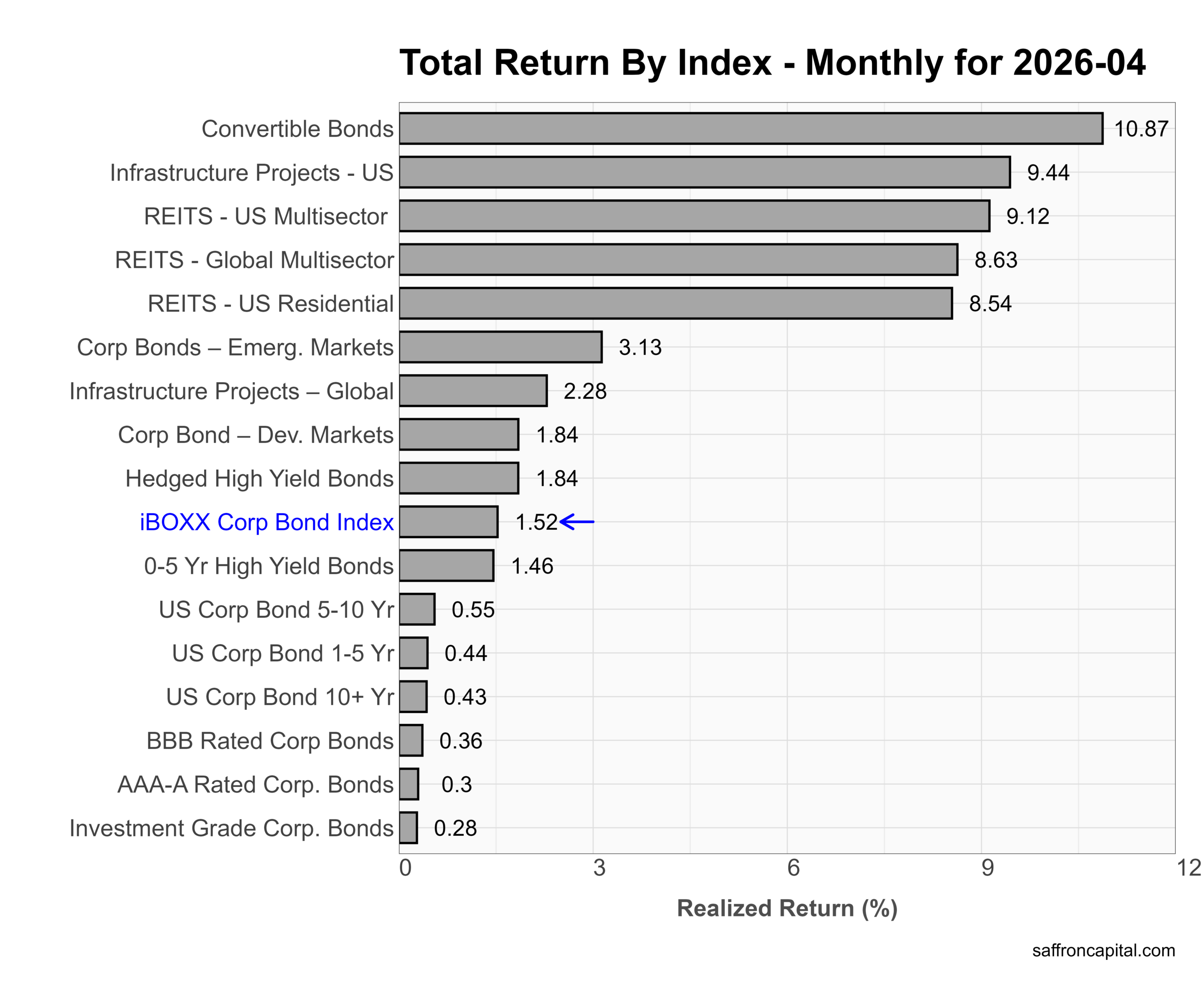

April favored equity-linked credit and real assets as spreads remained stable and risk appetite improved. Convertible bonds led with a +10.9% gain, while US infrastructure projects rose +9.4%. REITs also rallied sharply, with US Multisector REITs up +9.1% and Residential REITs gaining +8.5%. Core corporate bonds posted modest gains, with the iBOXX Corporate Bond Index up +1.5%, while investment-grade and long-duration corporates lagged below +0.5%. Overall, April rewarded spread exposure and equity-sensitive income assets more than traditional corporate duration.

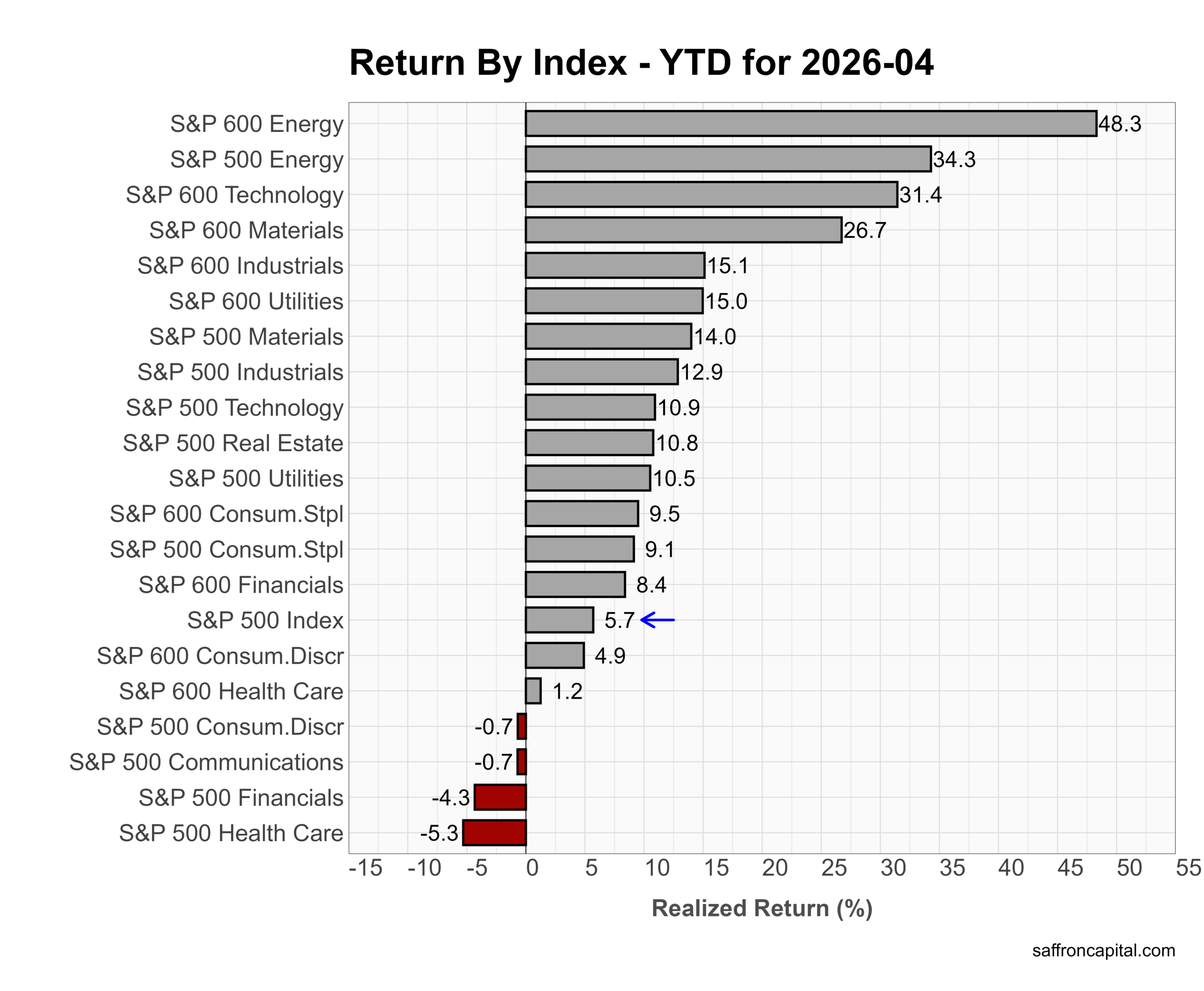

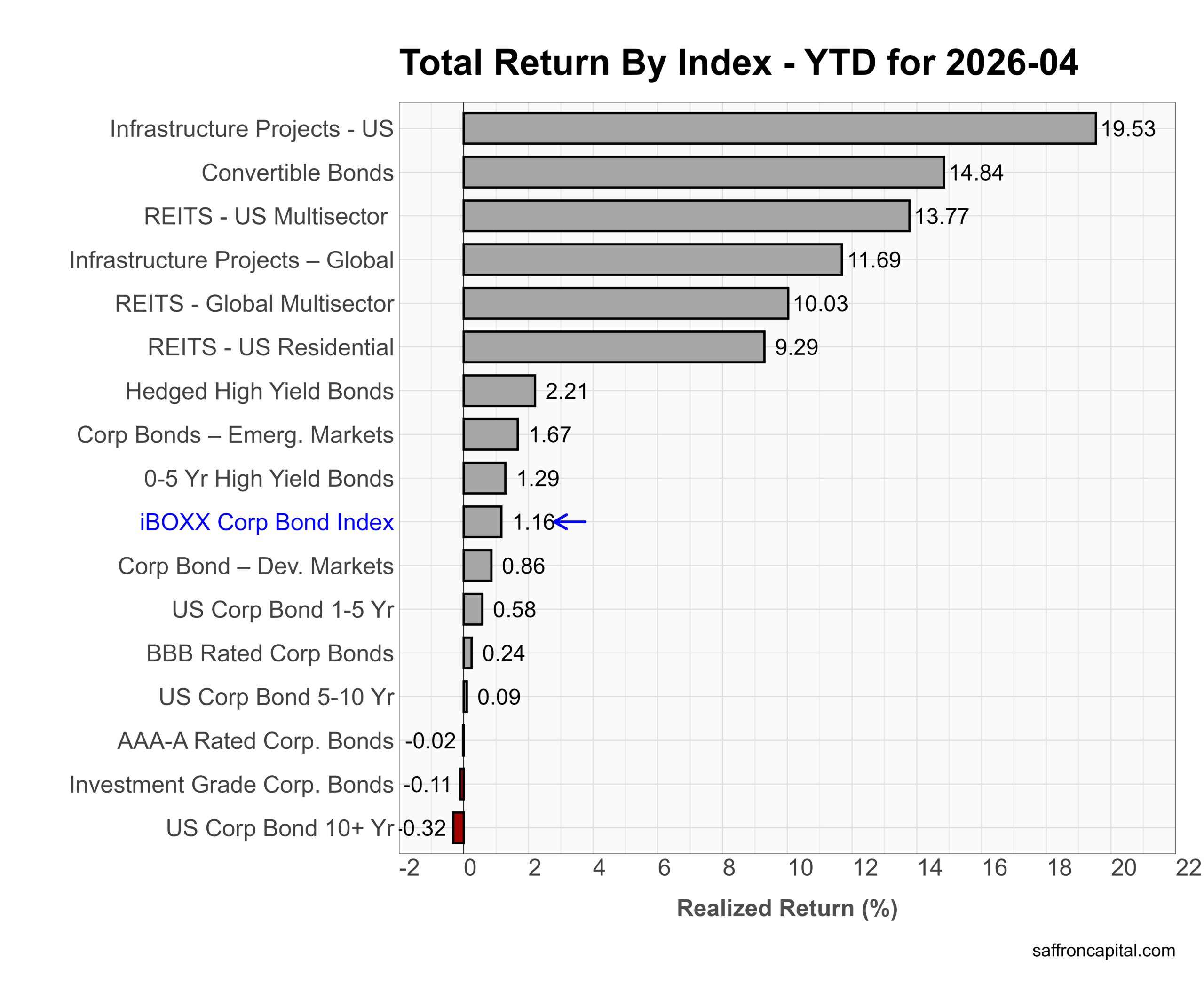

Year to date, leadership remains concentrated in infrastructure, REITs, and convertibles. US infrastructure leads at +19.5%, followed by convertible bonds at +14.8% and US Multisector REITs at +13.8%. Global infrastructure and REITs also remain strong. In contrast, traditional investment-grade corporates continue to lag, with the iBOXX Corporate Bond Index up just +1.2% and long-duration corporates still negative. Overall, 2026 continues to favor real assets and equity-linked income over pure duration exposure.

{kind=link}

{kind=link}

{kind=link}