June 2023 returns came in strong with the S&P 500 index up +6.5% for the month and the NASDAQ 100 index +6.3%. In a sign of strong market internals, the small cap S&P 600 Index broke away from the larger market and was up +9.2% in June. Meanwhile, US fixed income indexes were mixed as seen by the US Aggregate Bond Index (-0.37%) and the iBoxx Corporate bond index (+1.78%). Bonds for US Infrastructure Projects (+9.1%) were a top performer within the fixed income space and outperformed most equities. Commodity prices (+4.4%) were also strong in June, supported in part by declines in the US Dollar (-0.3%).

The following analysis provides a visual record of June 2023 returns across and within the major asset classes.

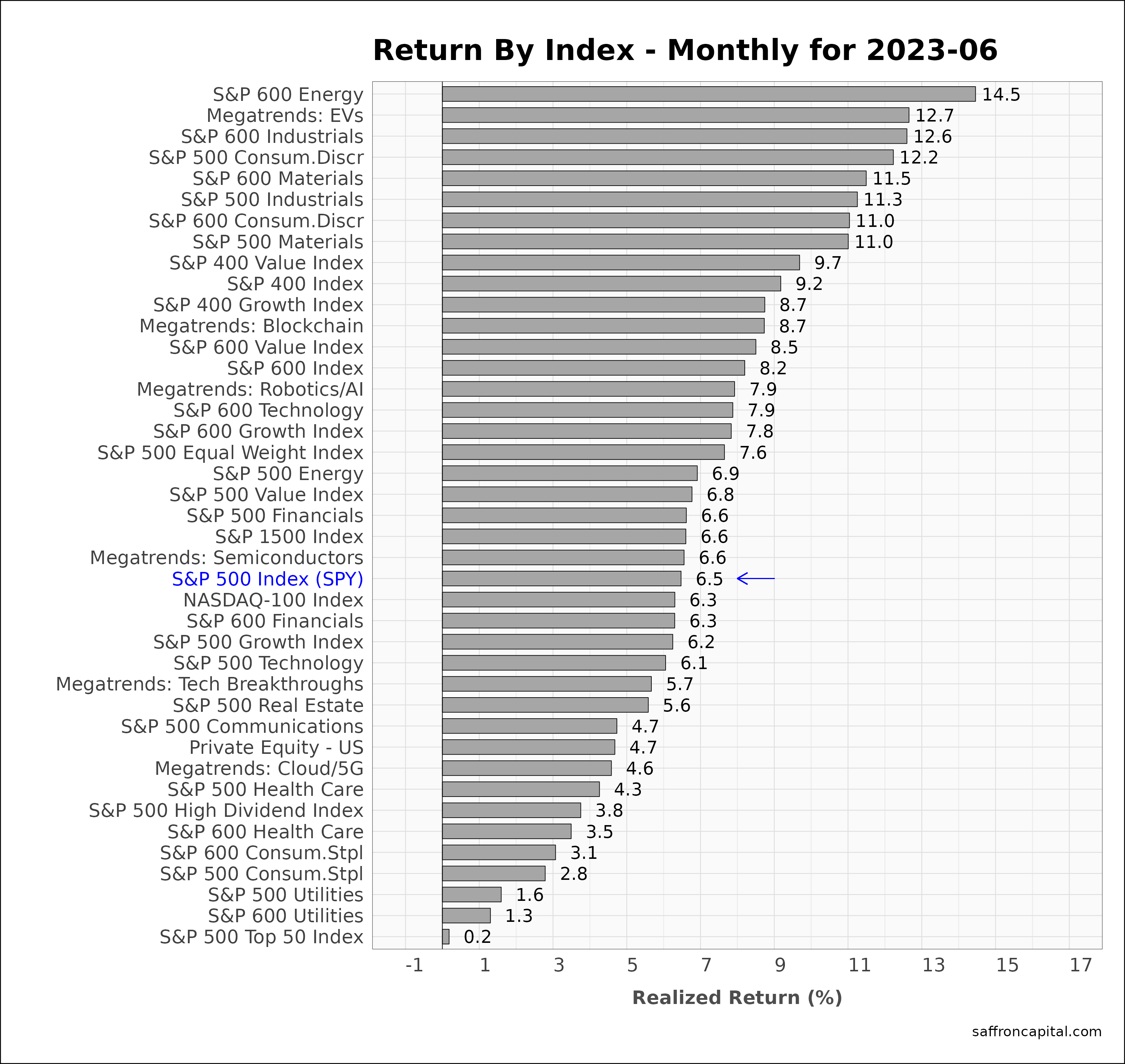

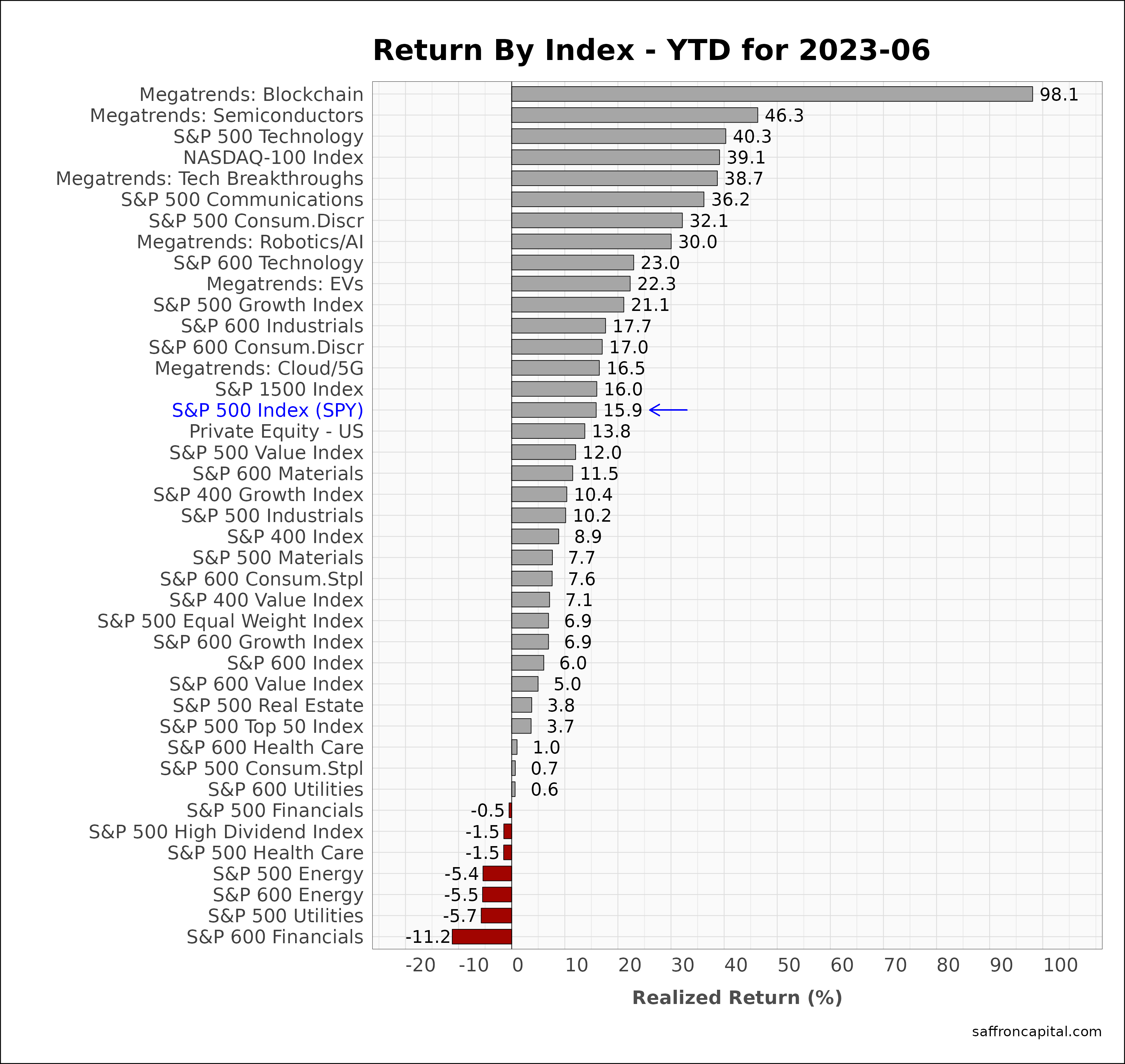

US Equities

The S&P 500 index ends the second quarter up 15.9% year-to-date (YTD). Astoundingly, the mega-cap 7 (AAPL, MSFT, NVDA, META, TSLA, GOOG, and GOOGL) now explain 77% of the rise in S&P 500 index since January. In comparison, the S&P 500 Equal Weight Index is up +6.9% YTD and is a better proxy of the market’s broader performance. Top performing sectors since January include Blockchain technologies (+98.1%), Semiconductors (+46.3%), and large cap Technology (+40.3%). Laggards since January include small cap Financials (-11.9%), large cap Utilities (-5.7%), and small cap energy (-5.5%).

Click to enlarge

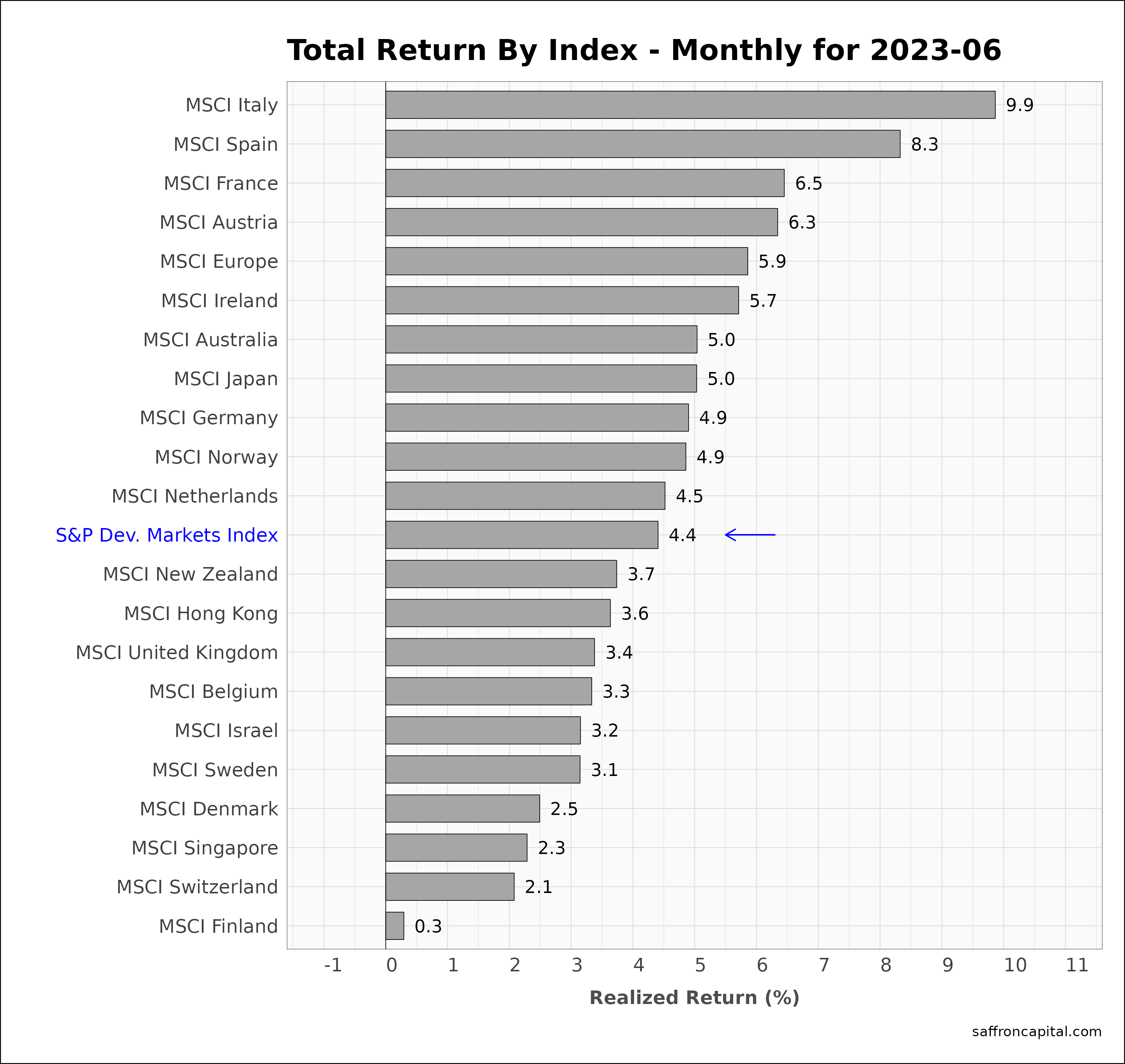

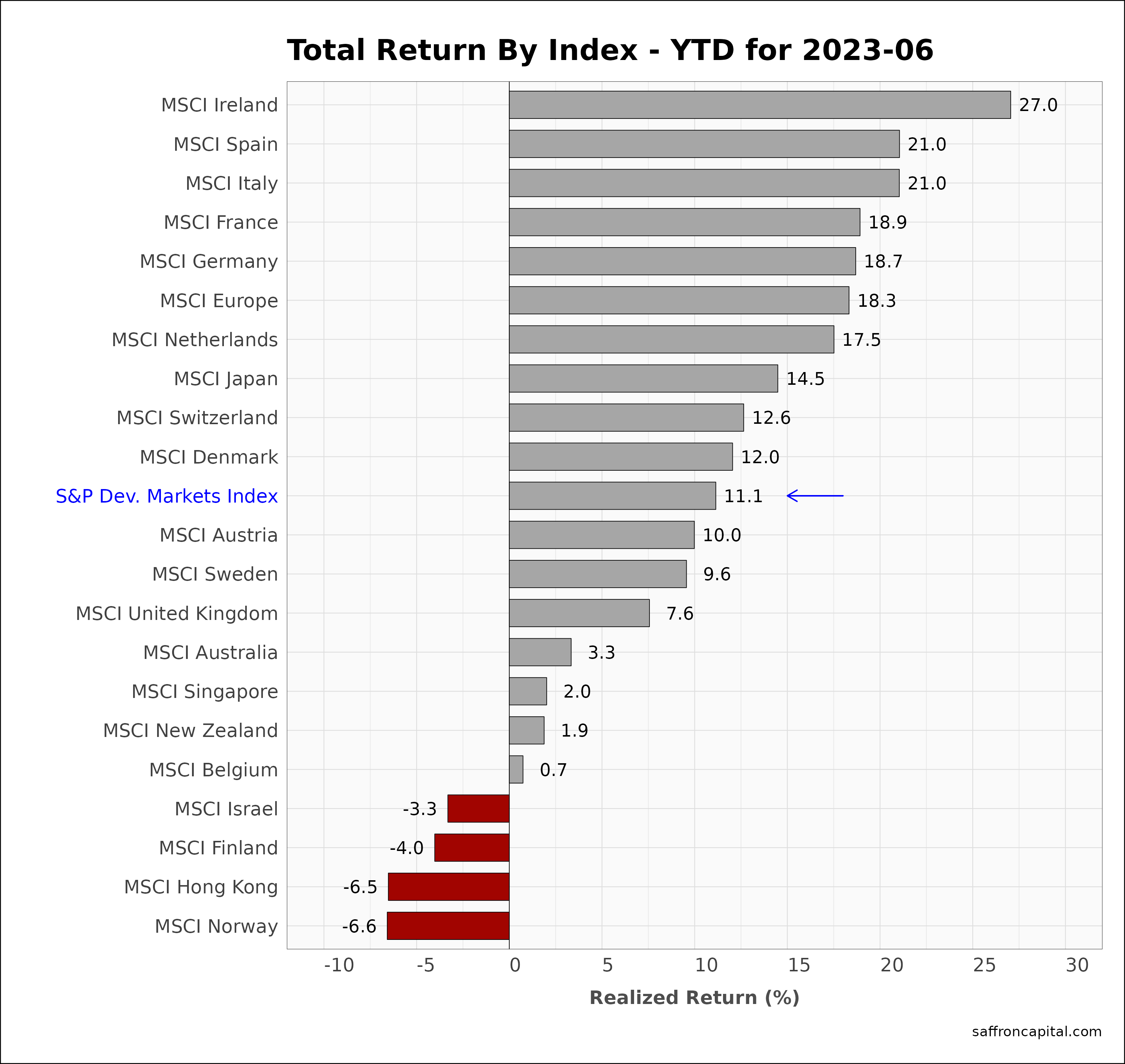

Developed Market Equities

international developed markets (+4.4%) lagged US equities in June. However, European shares (+5.9%) were stronger with Italy (+9.9%) and Spain (+8.3%) leading the developed markets. Since January, European shares (+18.3%) continue to beat US equities and the broader Developed market Index (+11.1%). 2023 performance of note includes Ireland (+27.0%), Spain (+21.0%), France (+18.9%) Germany (+18.7%), and the Netherlands (+17.5%).

Click to enlarge

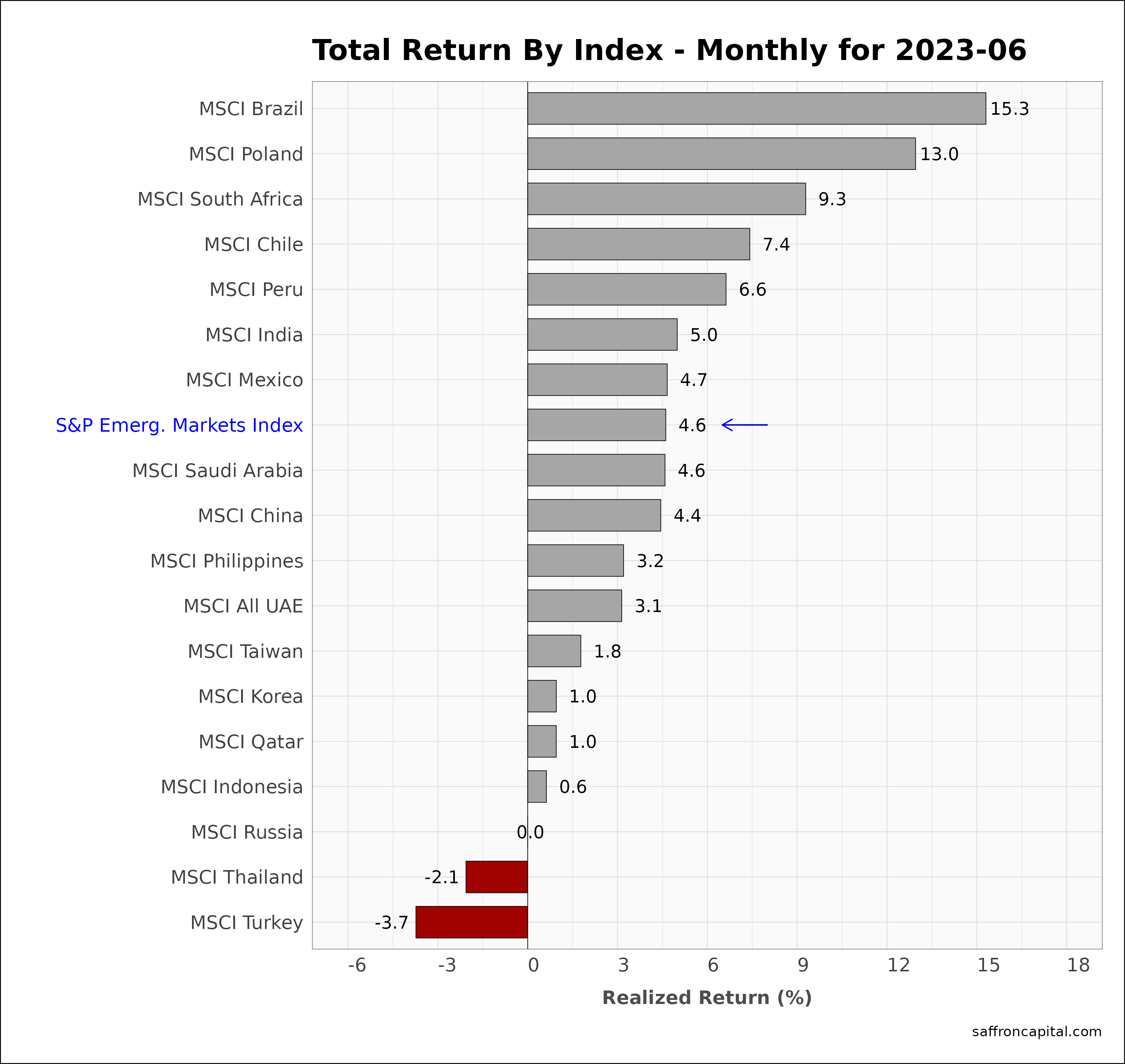

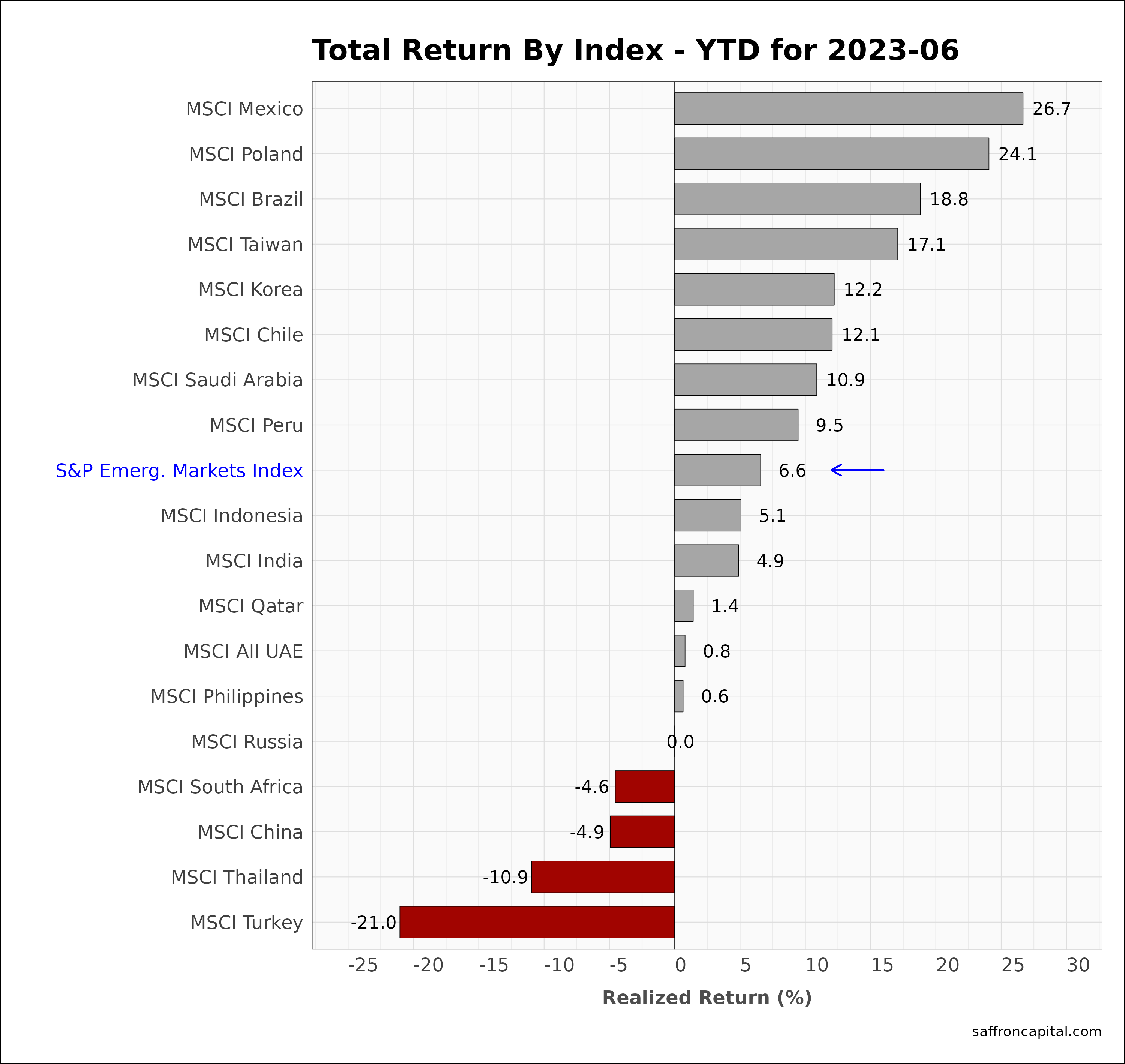

Emerging Market Equities

June 2023 returns for the S&P Emerging Markets Index (4.6%) trailed the US and the developed markets. Strong monthly returns were realized in Brazil (+15.3%), Poland (+13.0%) and South Africa (+9.3%). The weakest performer was Turkey (-3.7%). China (+4.4%) trailed the group average, while Indian shares (5.0%) outperformed the average. Year-to-date performance for emerging markets (+6.6%) is now dominated by Mexico (+26.7%), Poland (+24.1%), and Brazil (+18.8%).

Click to enlarge

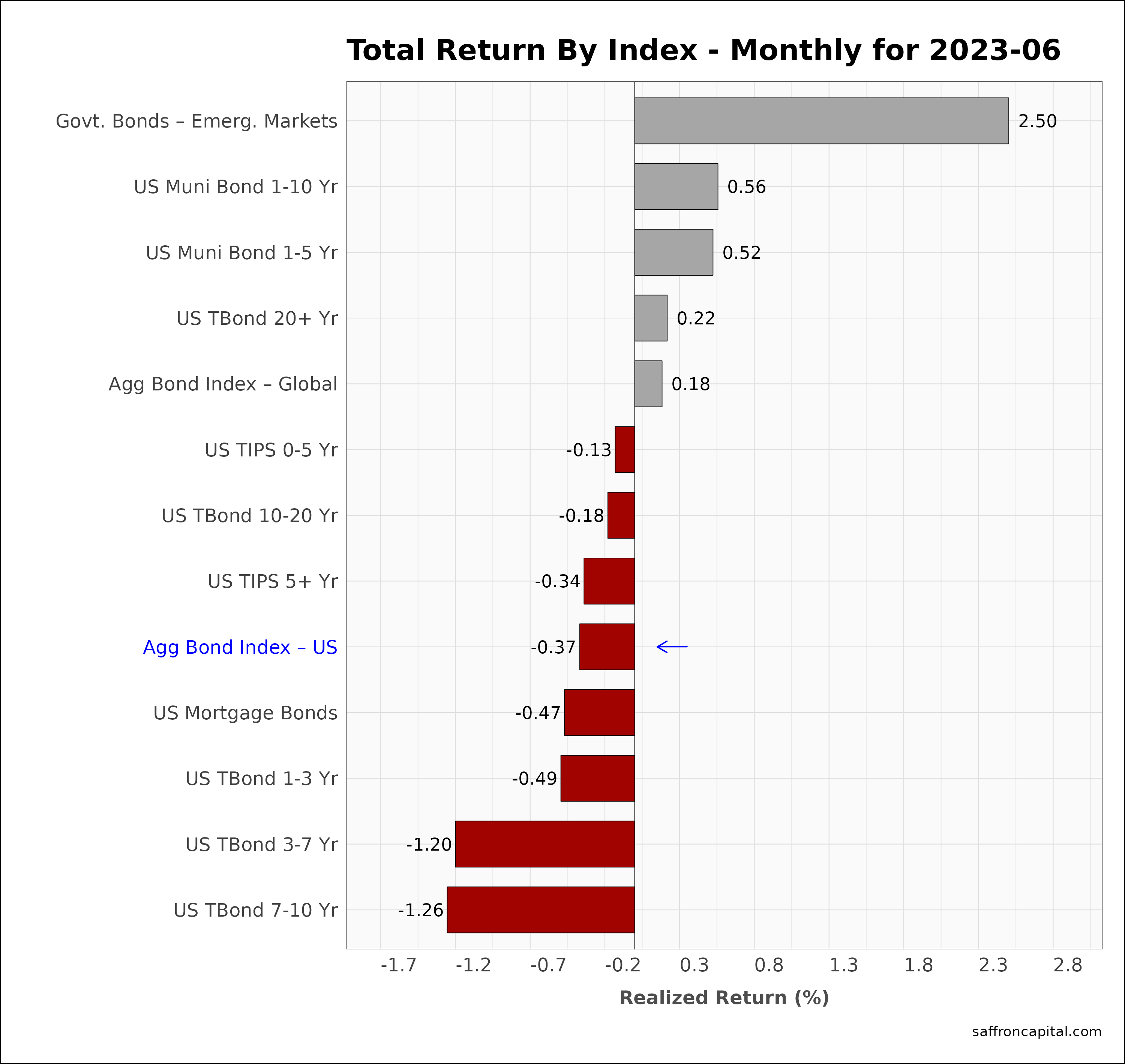

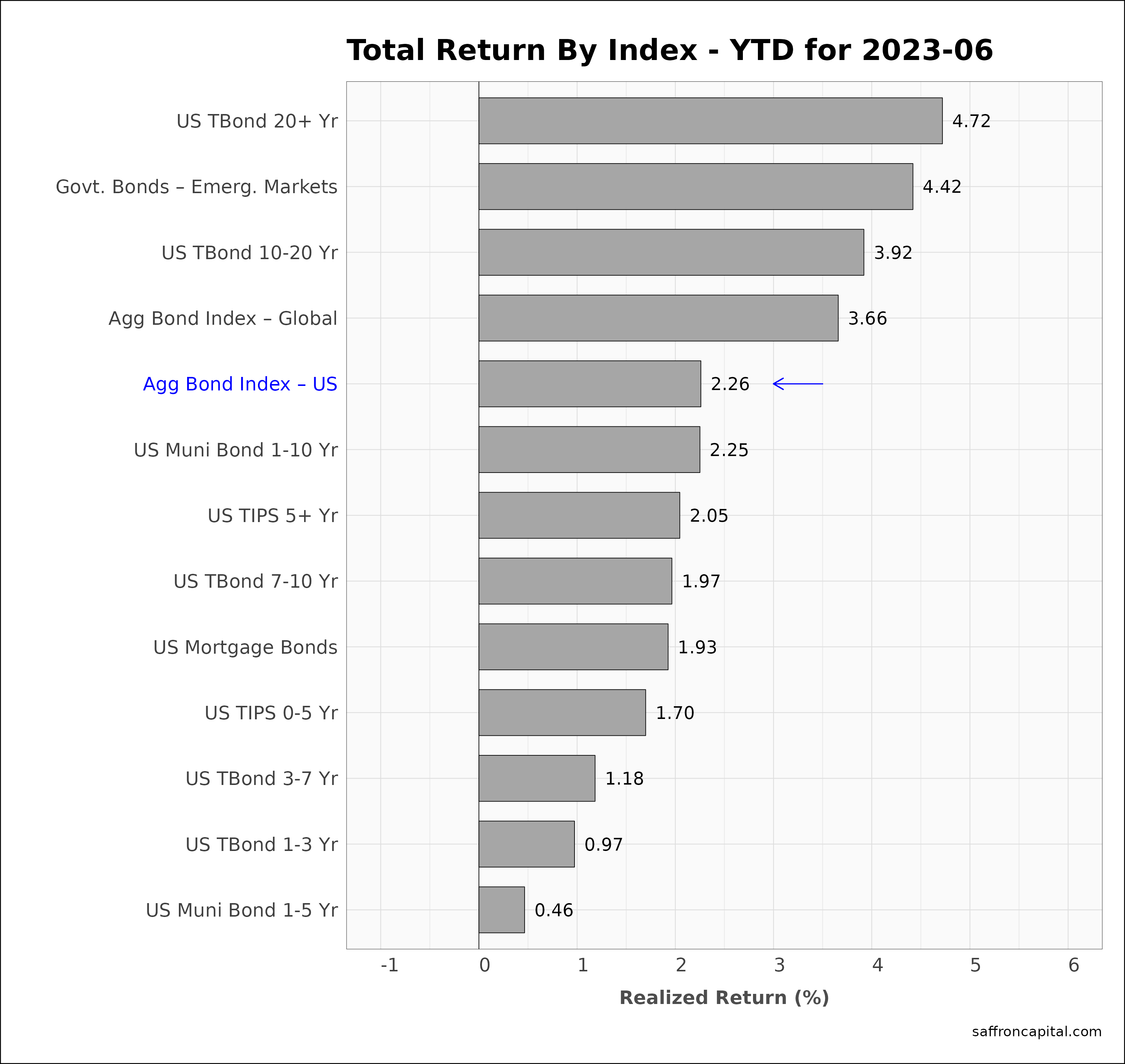

Government Bonds

June returns for the Aggregate US Government Bonds Index (-0.37%) reflected rising rates and losses across all matrities with the exception of the 20 year + maturities. Meawnhile, emerging market government bonds (+2.5%) had strong gains in June given yield declines in countries with more accommodating bank policies. Meanwhile, returns since January for the Aggregate US Bond index (+2.26%) and long-dated US treasury bonds (+4.72%) are yet to match realized inflation in 2023.

Click to enlarge

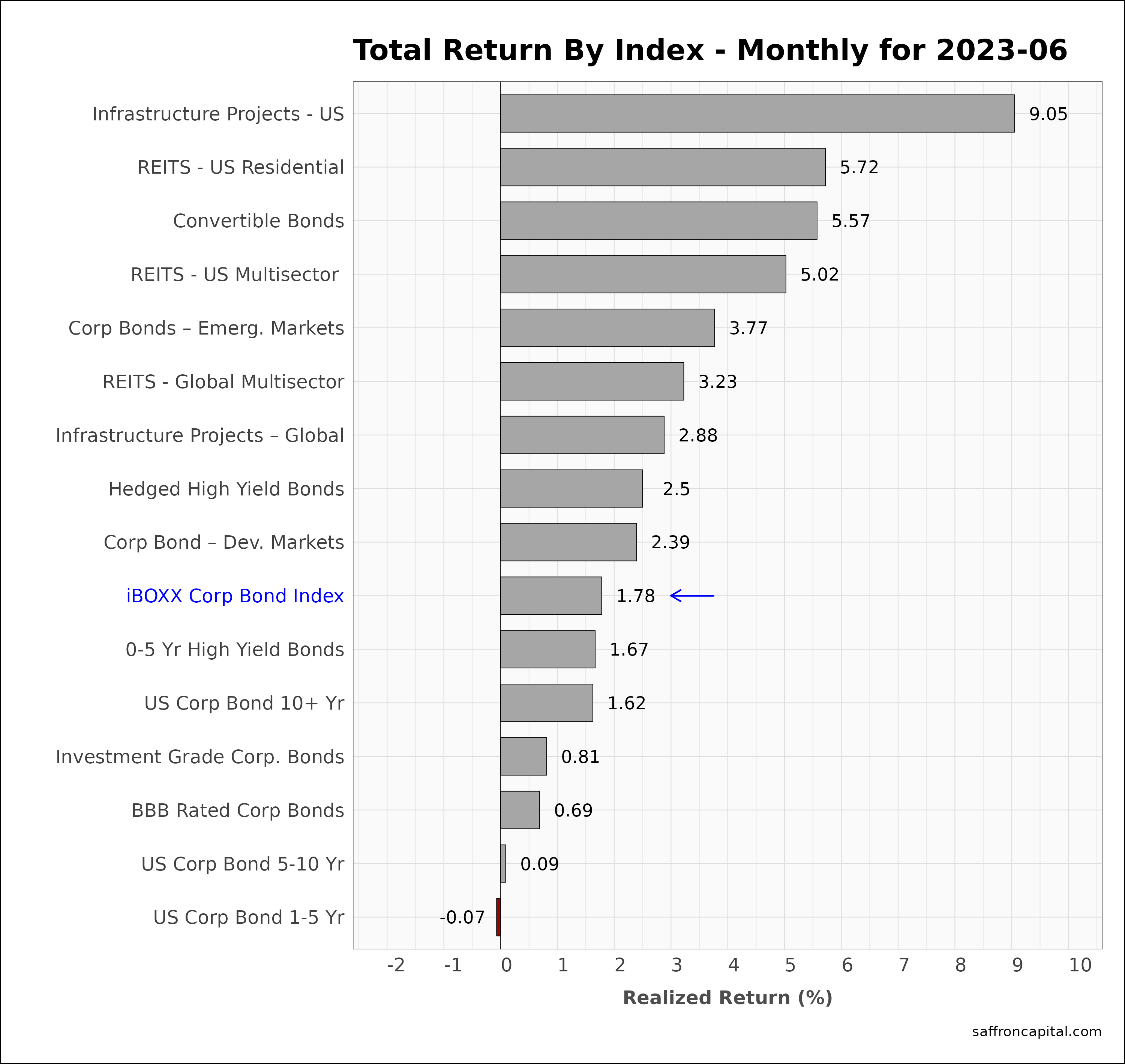

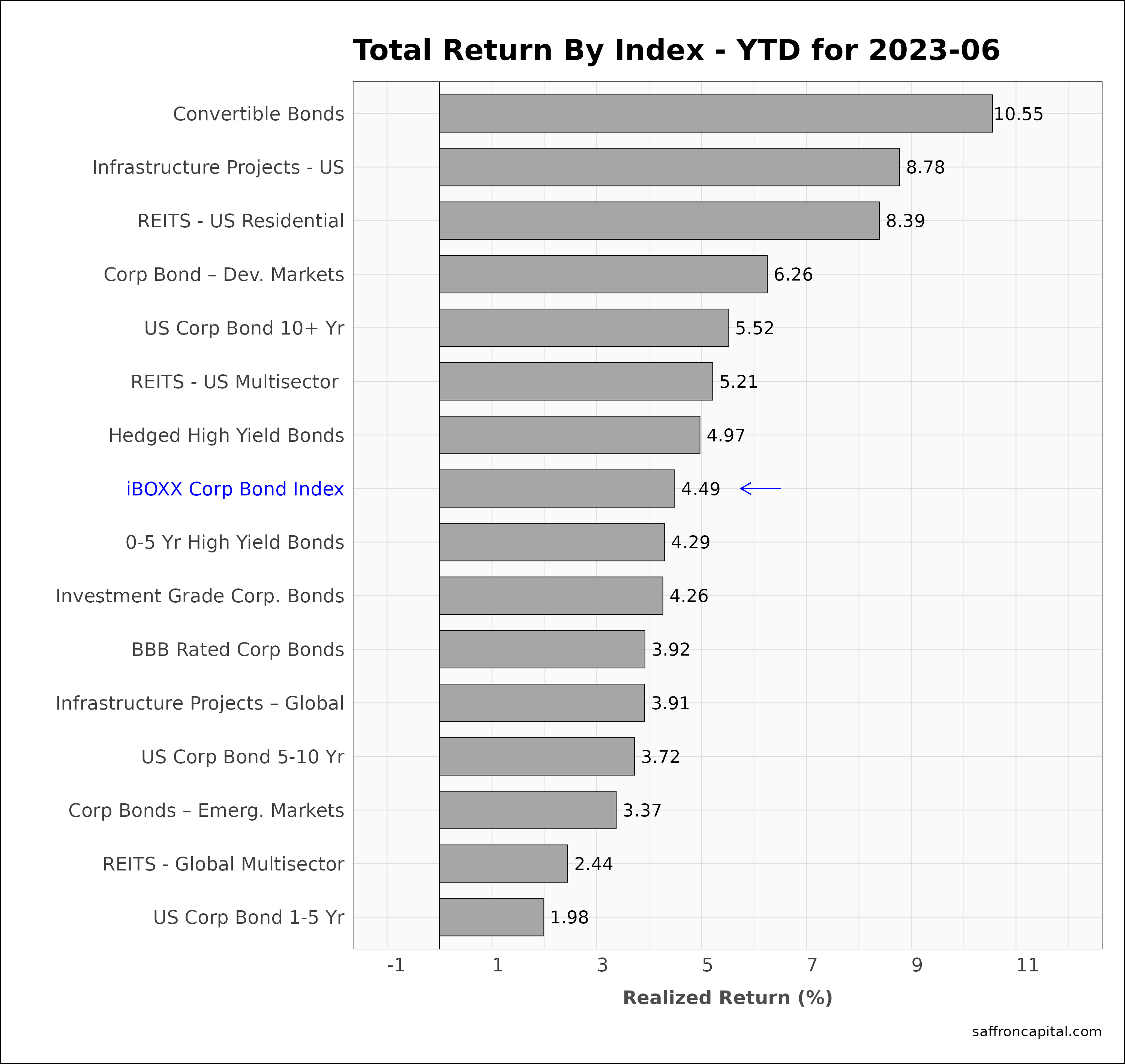

Corporate & Infrastructure Bonds

The iBoxx Corporate Bond Index (+1.78%) lagged Treasury bonds in June. However, strong performance within the sector is evident for US Infrastructure bonds (+9.05%), Residential REITS (+5.72%), and Convertible Bonds (5.57%). In contrast, more defensive plays within the sector, like investment grade and low duration corporate bonds, all performed badly. Year-to-date performance through the second quarter is topped by Convertible Bonds (+10.55%), US Infrastructure Bonds (+8.78%) and US Residential REITS (+8.39%).

Click to enlarge

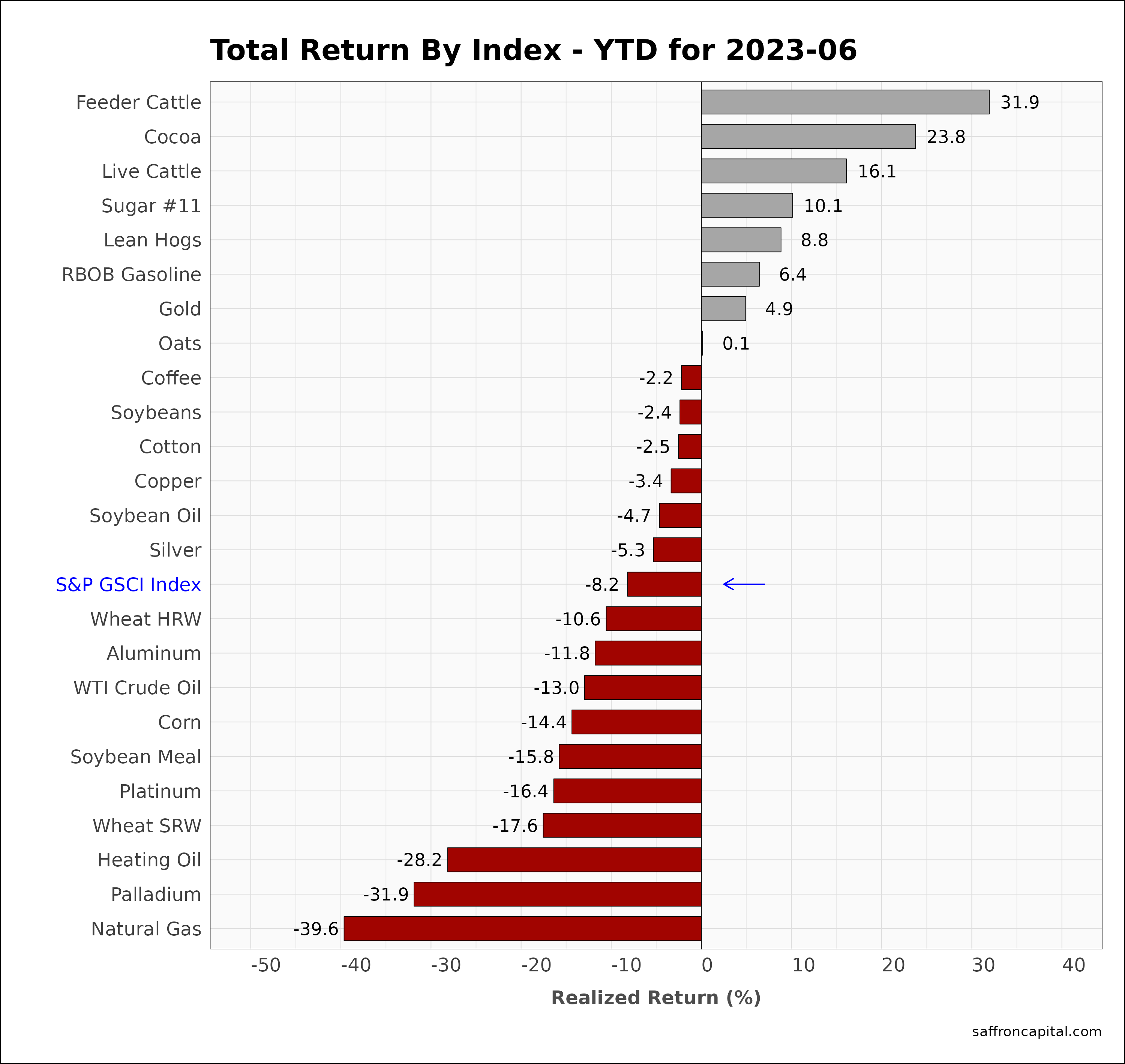

Commodities

June 2023 returns for the S&P GSCI index (+4.4%) masked the wide range of results across commodities. For example, Soybean Oil (+31.7%), Natural Gas (+19.2%) and Lean Hogs (15.6%) continued to inflate at high rates. Transportation fuel demand continues to support Heating Oil (+6.9%) and Gasoline (+2.3%) prices. Finally, precious metals have been under pressure, testing uptrend support where new buying has been evident.

Click to enlarge

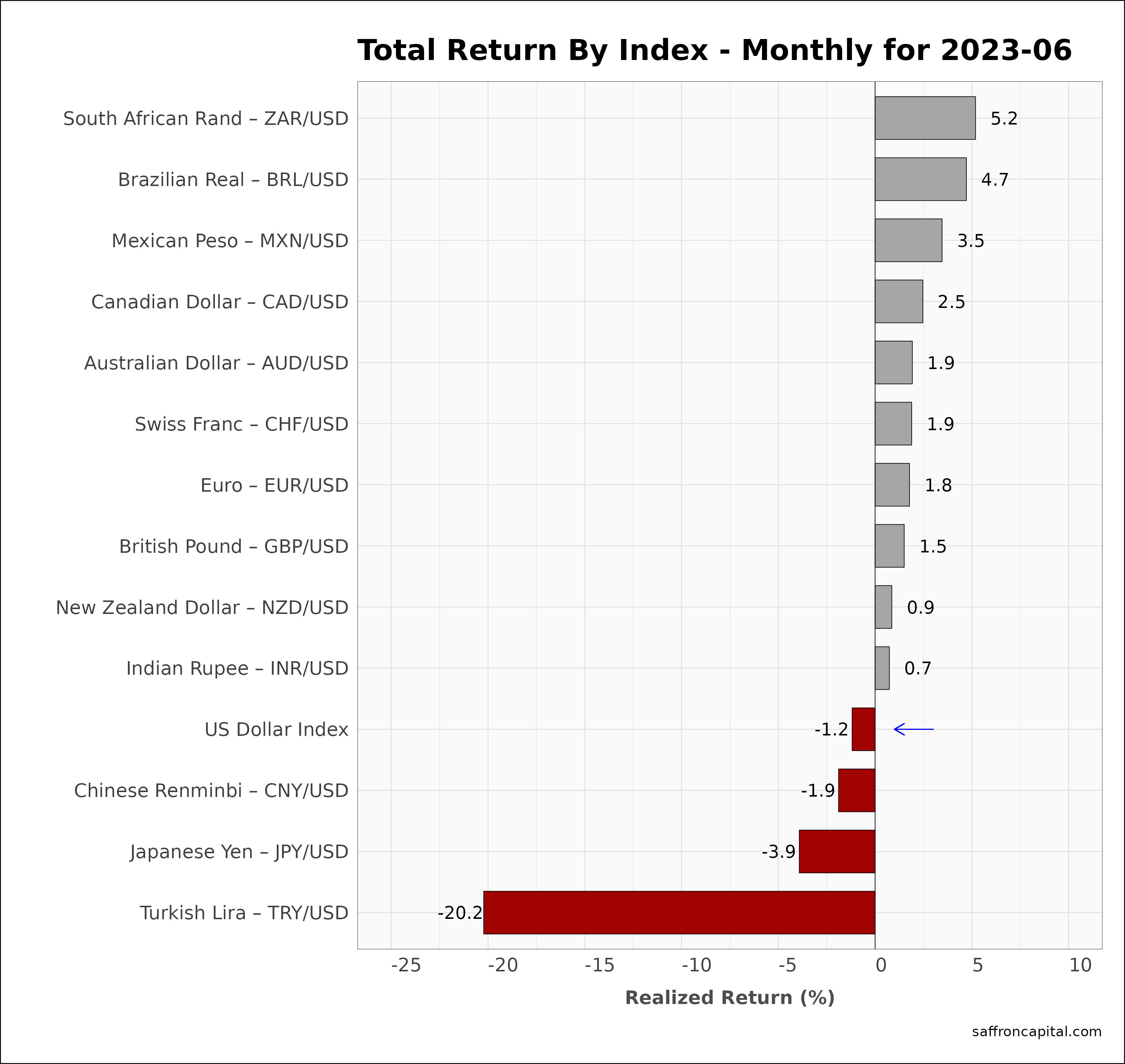

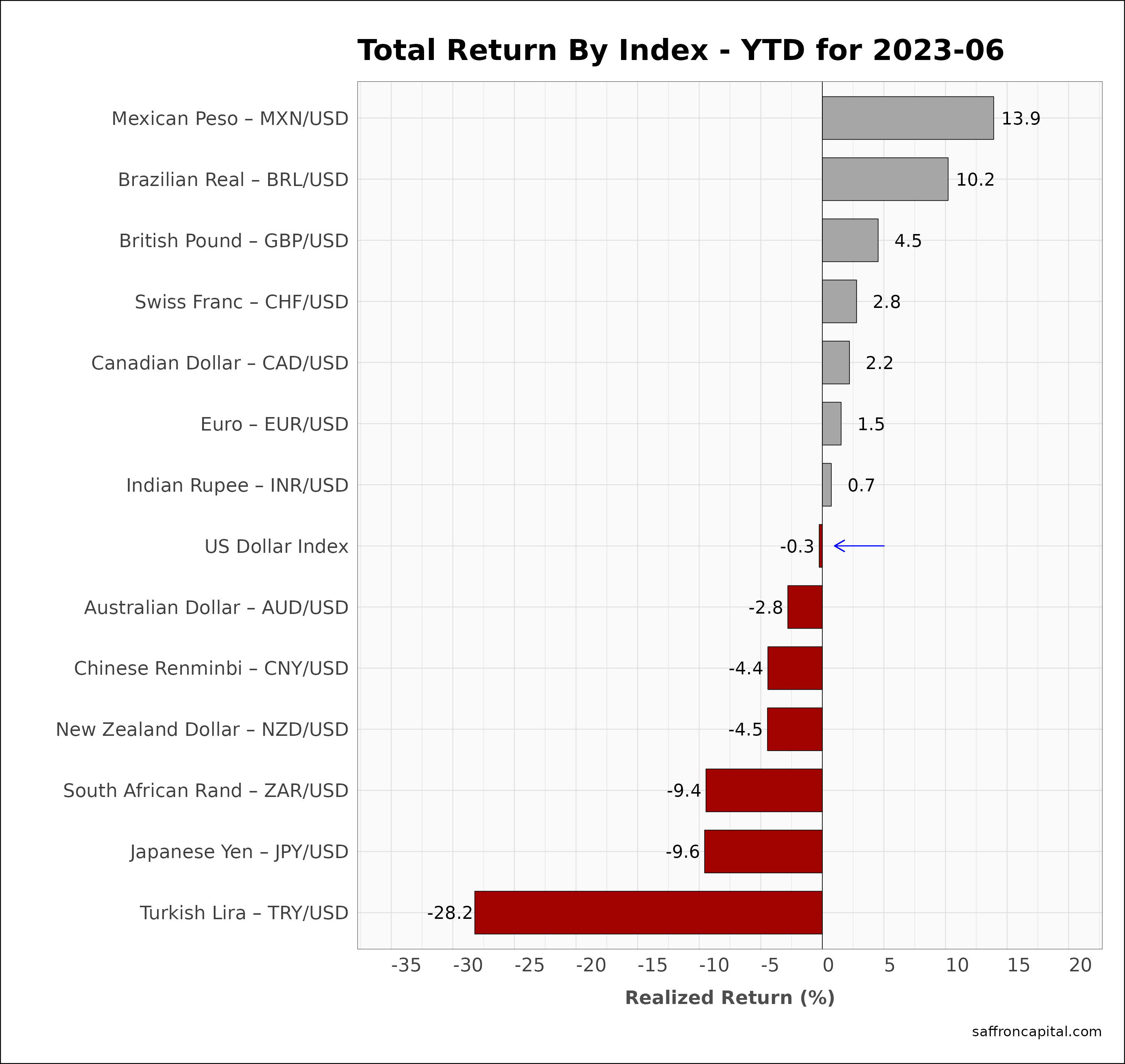

Currencies

The US Dollar (-1.2%) reversed course in June, allowing many currencies to increase with the exception of the Chinese Renminbi (-1.9%), the Yen (-3.9%) and the Turkish Lira (-20.2%). Since January, the dollar ends the second quarter very close to where it started the year, which is impressive considering the significant changes in short-term interest rates.

Click to enlarge

Have questions or concerns about the performance of your portfolio? Looking for improved performance at a lower cost? Whatever your needs are, we are here to listen and to help. You can schedule time with us here.

{kind=link}

{kind=link}

{kind=link}