April market volatility was notable. Red ink swept across the monthly results for most asset classes, highlighting the need for active risk management and strategies for capital preservation. Equity and bond markets were down world-wide with few exceptions. Strength in the US dollar remained significant and did little to temper outstanding commodity sector returns. The following analysis provides a visual record of returns across and within the major asset classes. The purpose is to facilitate investor performance benchmarking.

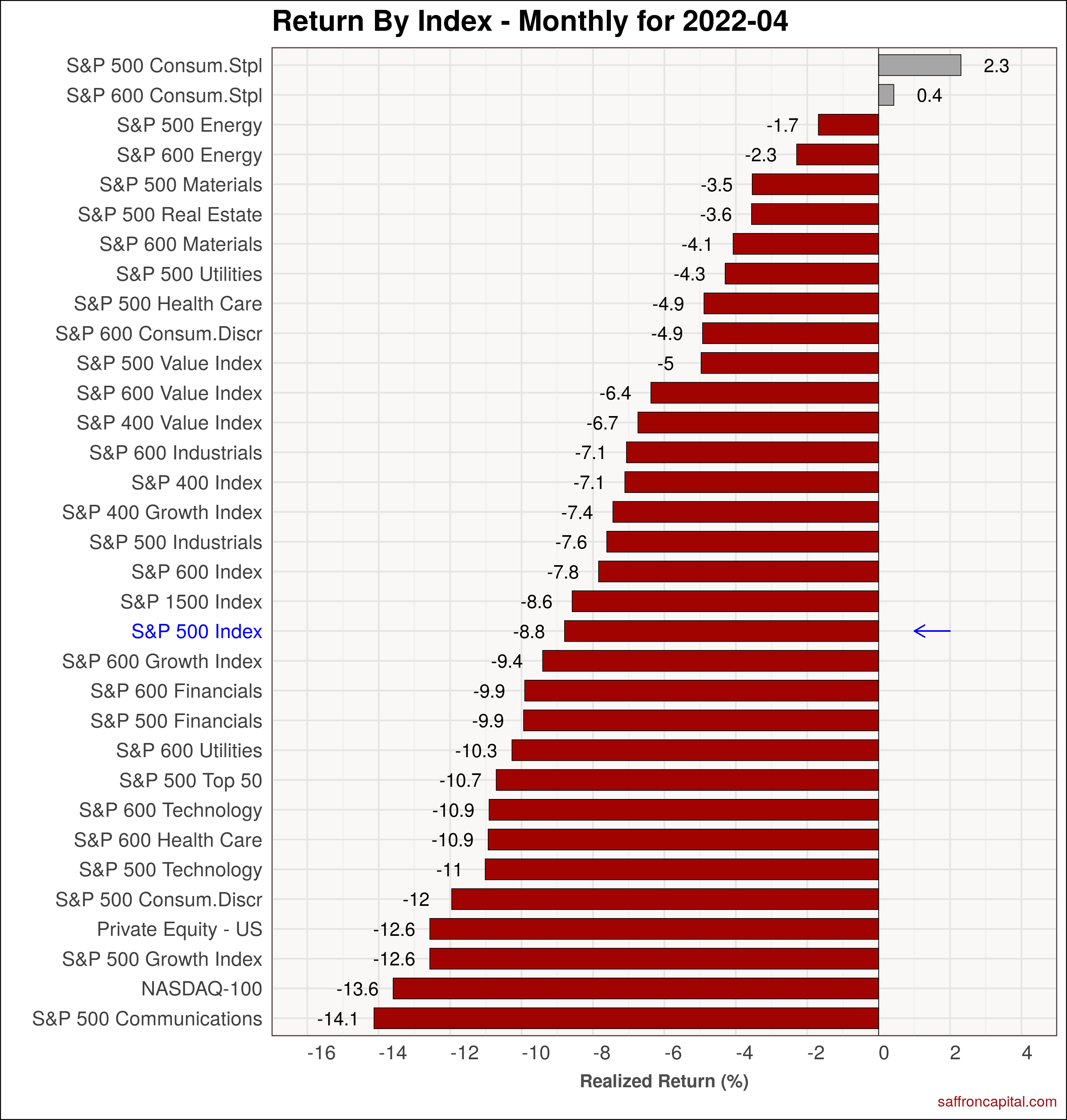

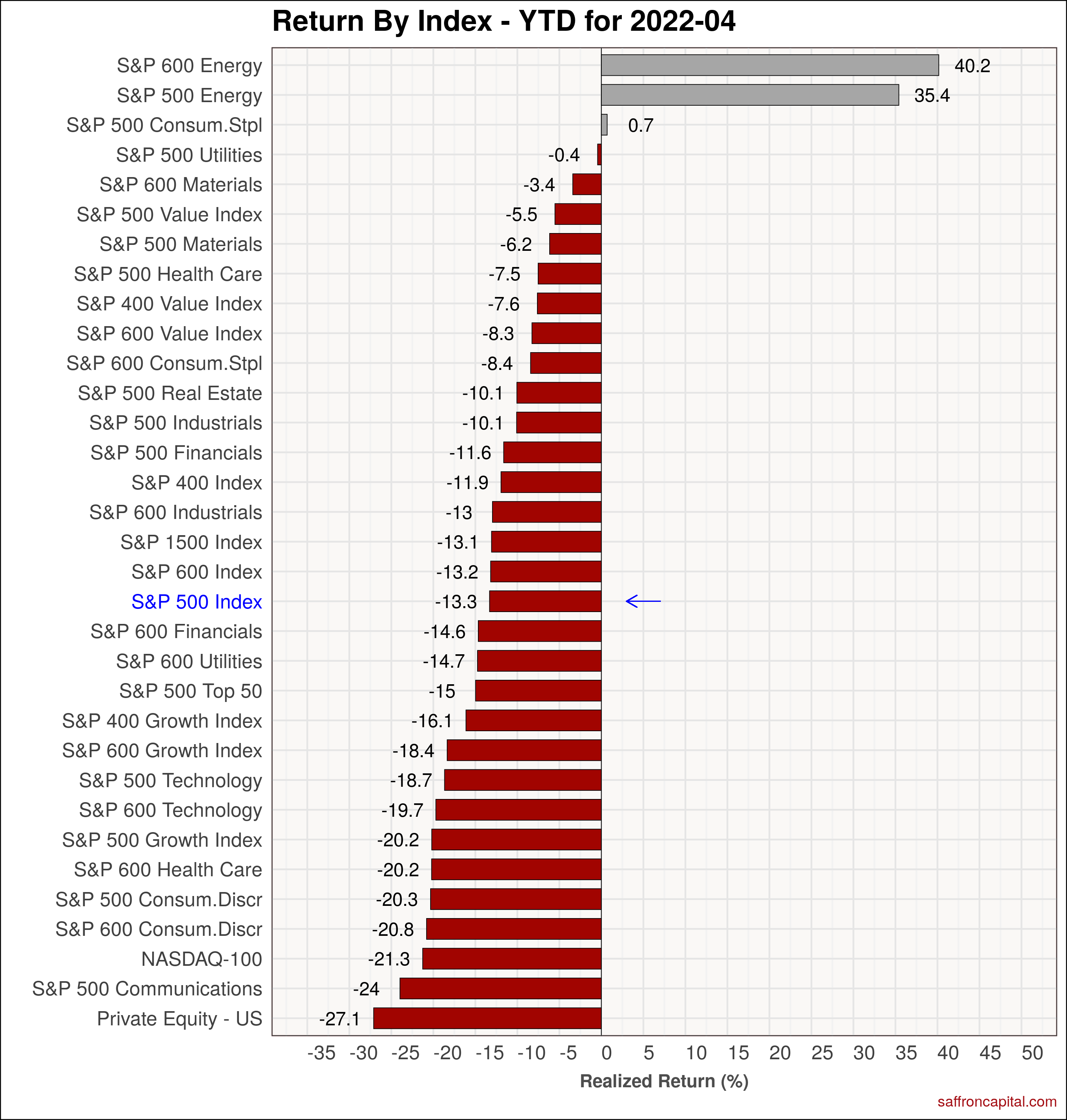

US Equities

For all of April, the Nasdaq shed 13.3% – marking its biggest monthly decline since October 2008. The S&P 500 fell 8.8% for its’ worst months since March 2020. Strength was limited to Consumer Staples, where the defensive sector posted solid gains for both large cap shares (+2.3%) and small cap shares (+0.4%). On a year-to-date (YTD) basis, large cap energy shares (+40.2%) and small cap energy (+35.4%) easily outperformed the S&P 500 index. The hardest hit sectors on a YTD basis include private equity (-27.1%), Communication Services (-24.0%) and the NASDAQ (-21.3%).

Click to enlarge

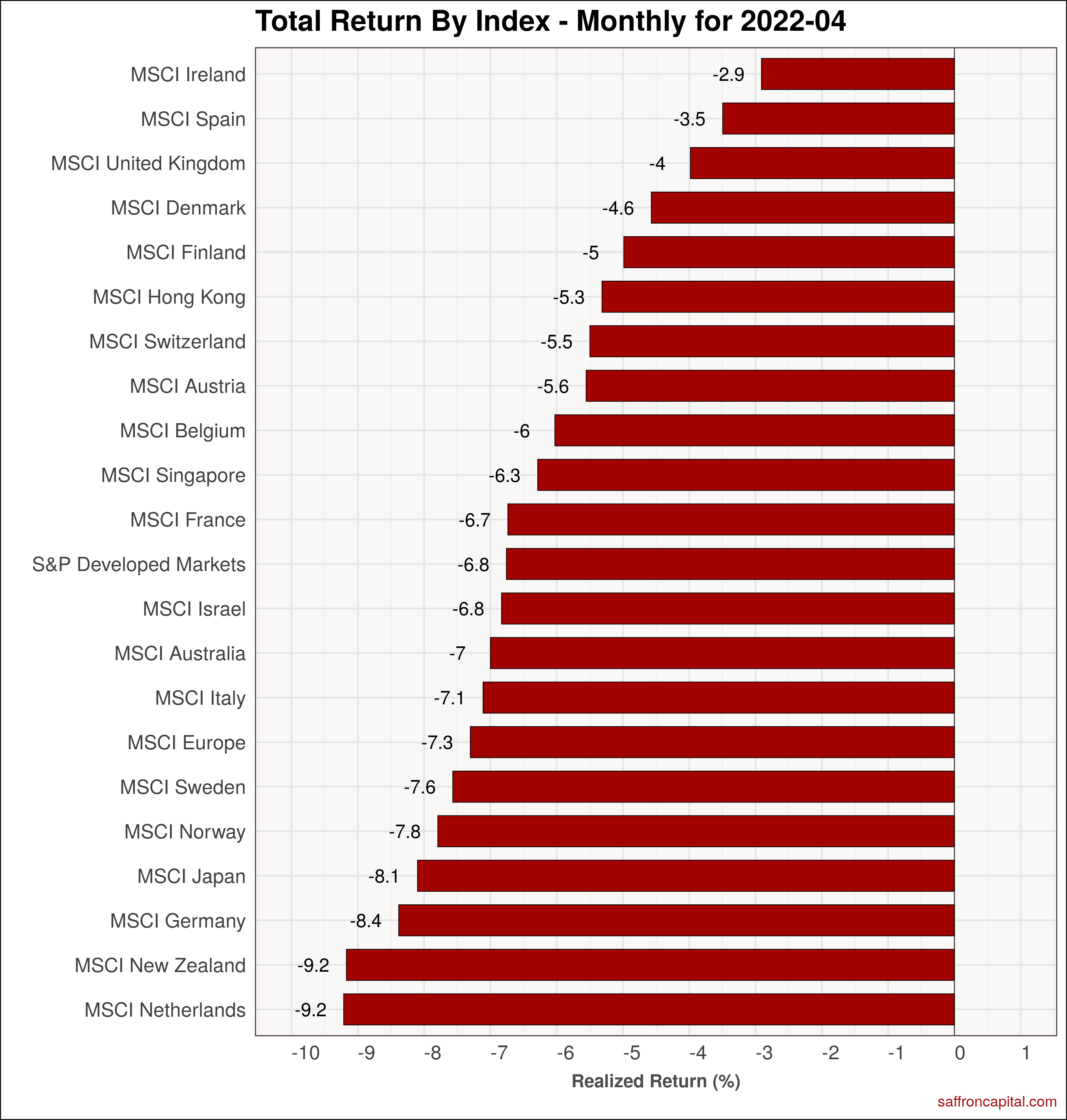

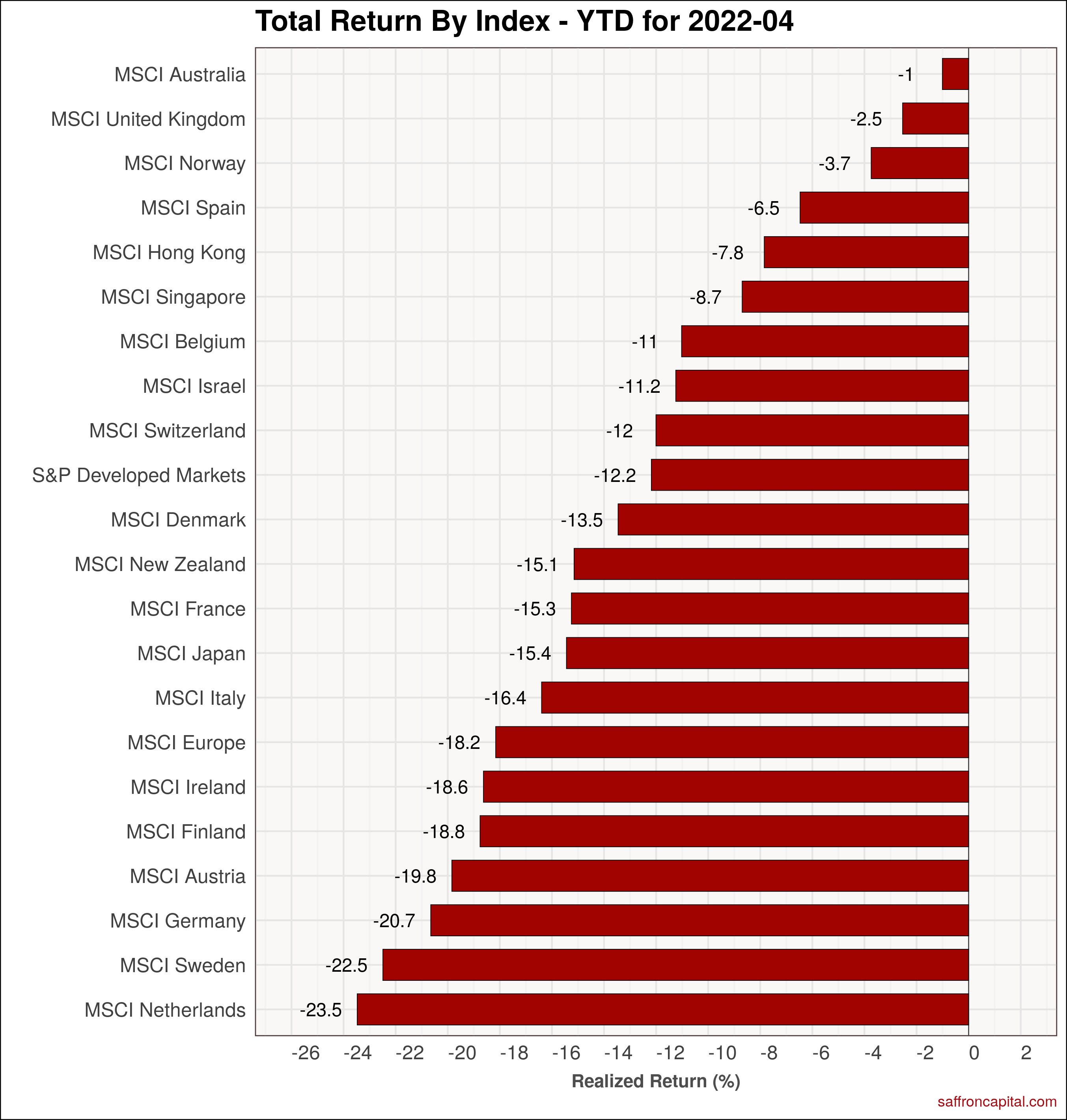

Developed Market Equities

Elsewhere, equity markets for all the developed economies had negative returns. Regardless, the S&P Developed Markets index (-6.8%) outperformed the S&P 500 index by 200 basis points (bps). Meanwhile, on a year-to-date basis, the Developed Market index (-12.2%) is also beating the S&P 500 index by 90 basis points. The best markets in the category include Australia (-1%), The United Kingdom (-2.5%), and Norway(-3.7%).

Click to enlarge

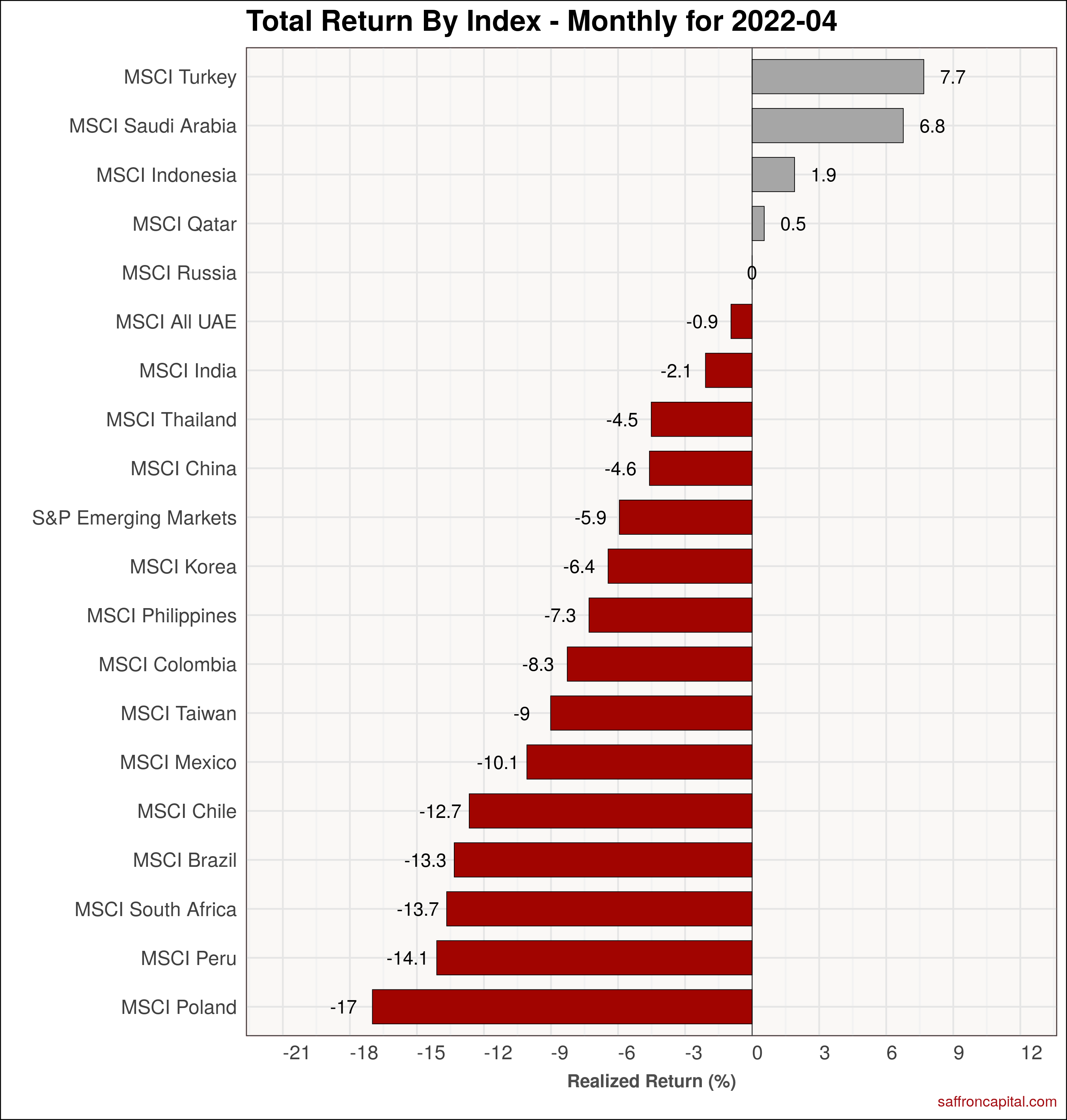

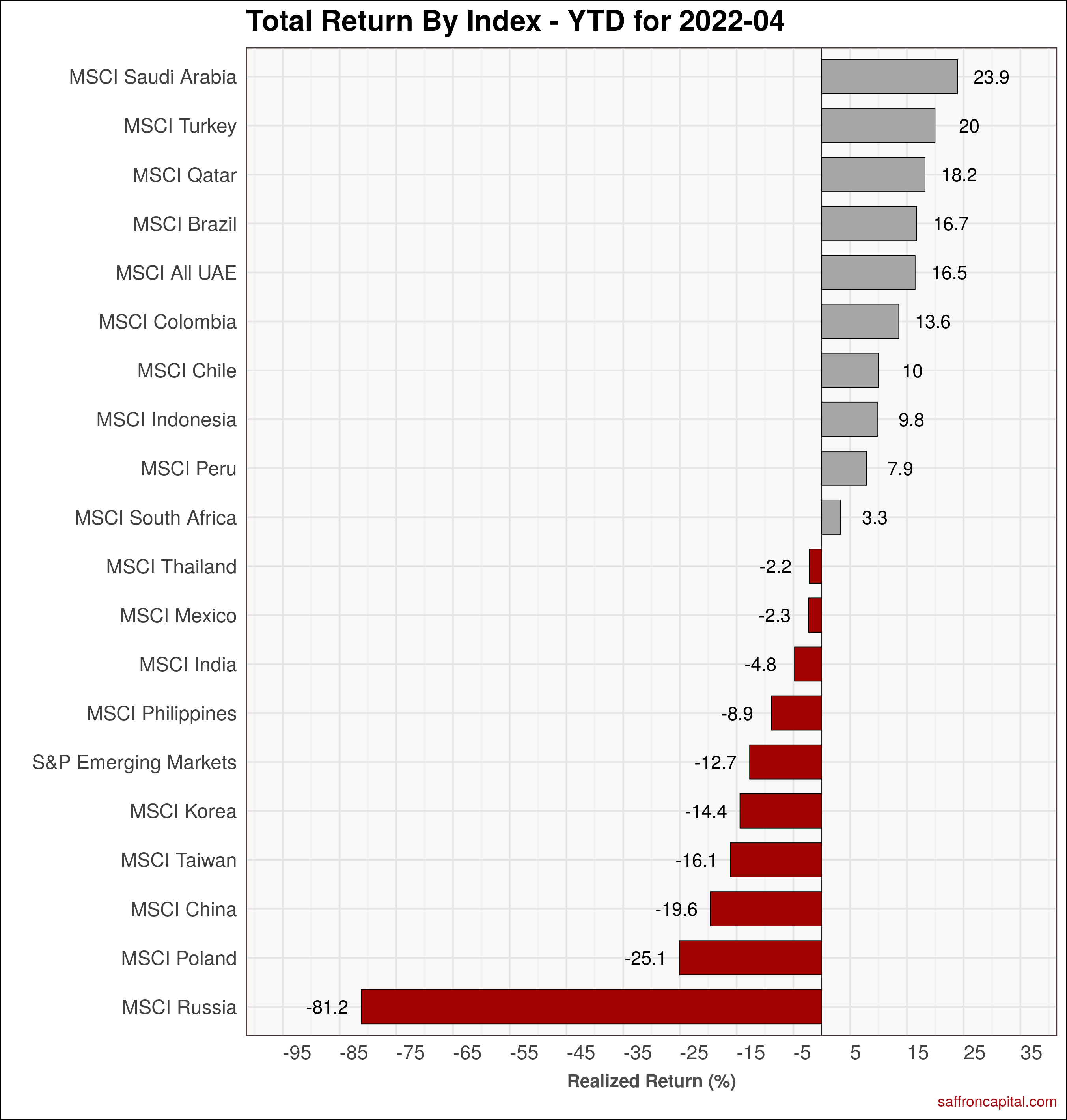

Emerging Market Equities

Emerging markets, notably resource rich economies, have easily outperformed the developed markets. The S&P Emerging Market index (-5.9%) outperformed the S&P 500 index by 290 bps and beat the S&P Developed Markets index by 90 bps. At the top of the performance list was Turkey (+7.7%), Saudi Arabia (6.8%), Indonesia (+1.9%) and Qatar (+0.5%). Year to date, the relative performance of the Emerging Market index (-12.7%) has been dragged down by Russia (-81.2%). However, a number of emerging markets are performing admirably, including Saudi Arabia (+23.9%), Turkey (+20.0%), and Qatar (+18.2%) among others.

Click to enlarge

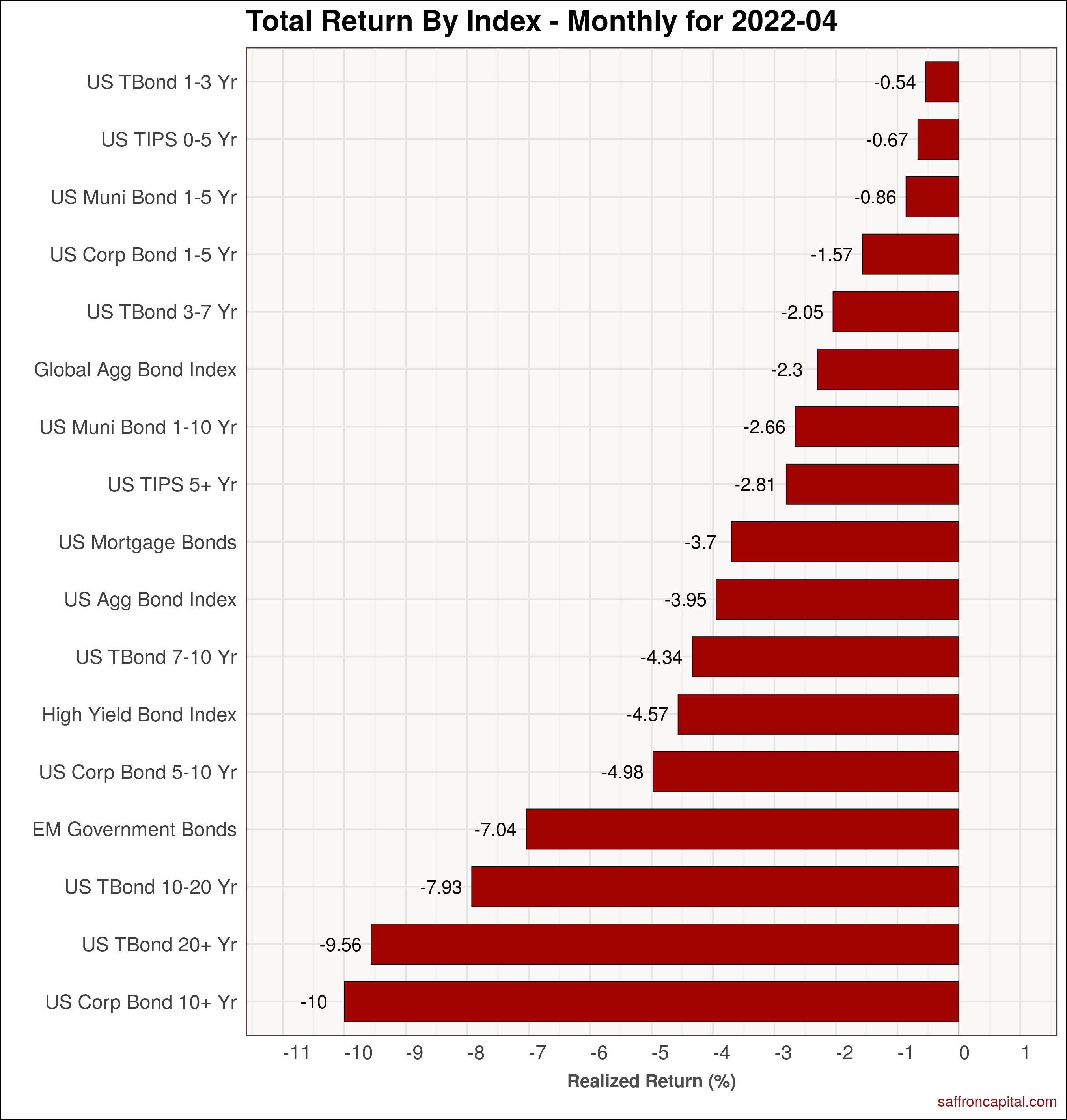

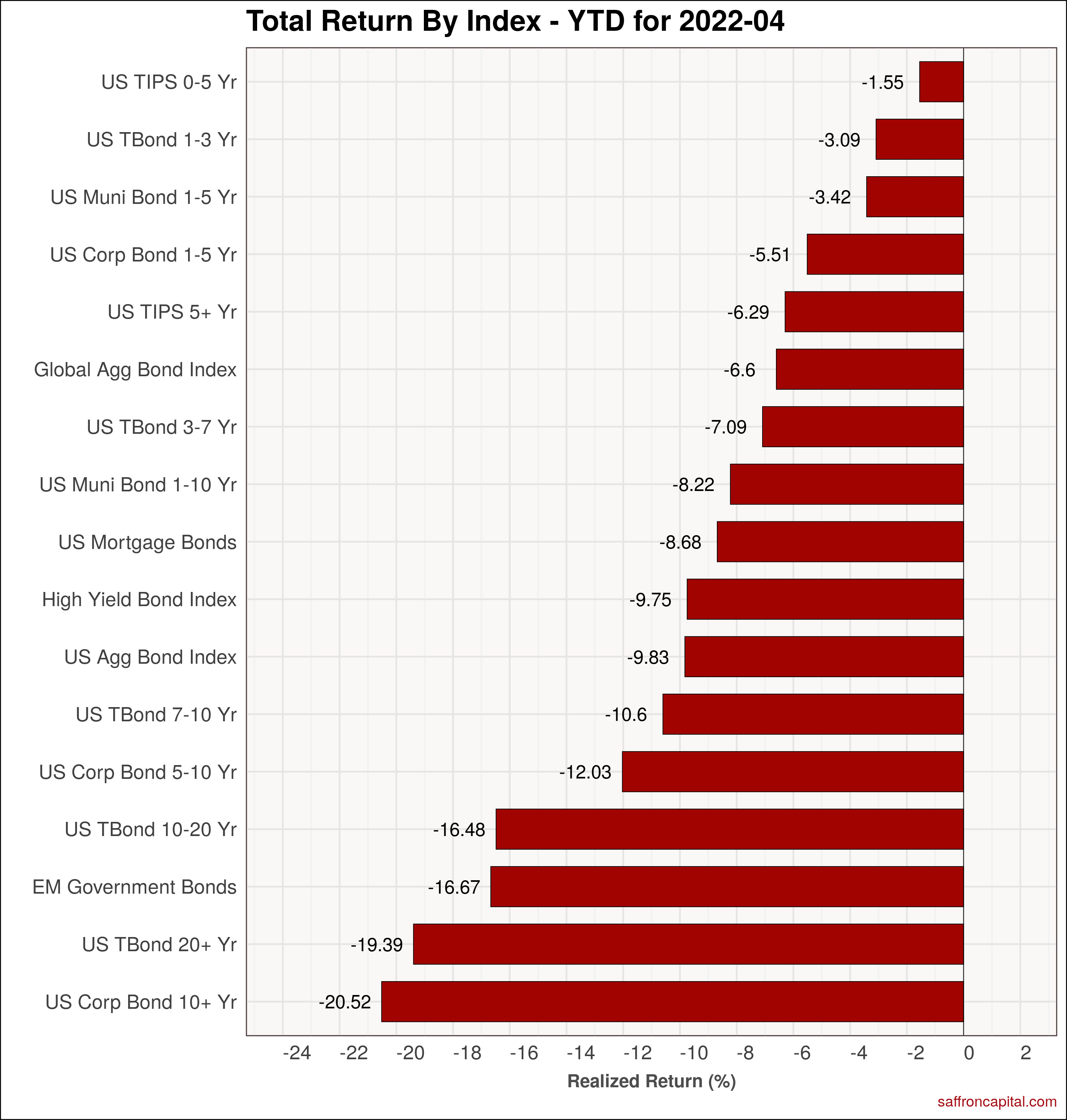

Government Bonds

April was the second month where returns were down for all government bond maturities. The US Aggregate Bond Index (-3.95%) lagged behind the Global Aggregate Bond Index (-2.3%), owing to delayed efforts to raise interest rates in many countries when compared to the US. Emerging market Bonds (-7.04%) were particularly hard hit in April. On a year-to-date basis the returns are even worse. US treasury bonds (-19.39%) and US Corporate Bonds (-20.52) have been crushed! The good news: both will offer heavily discounted prices and attractive buying opportunities once a trend reversal is confirmed.

Click to enlarge

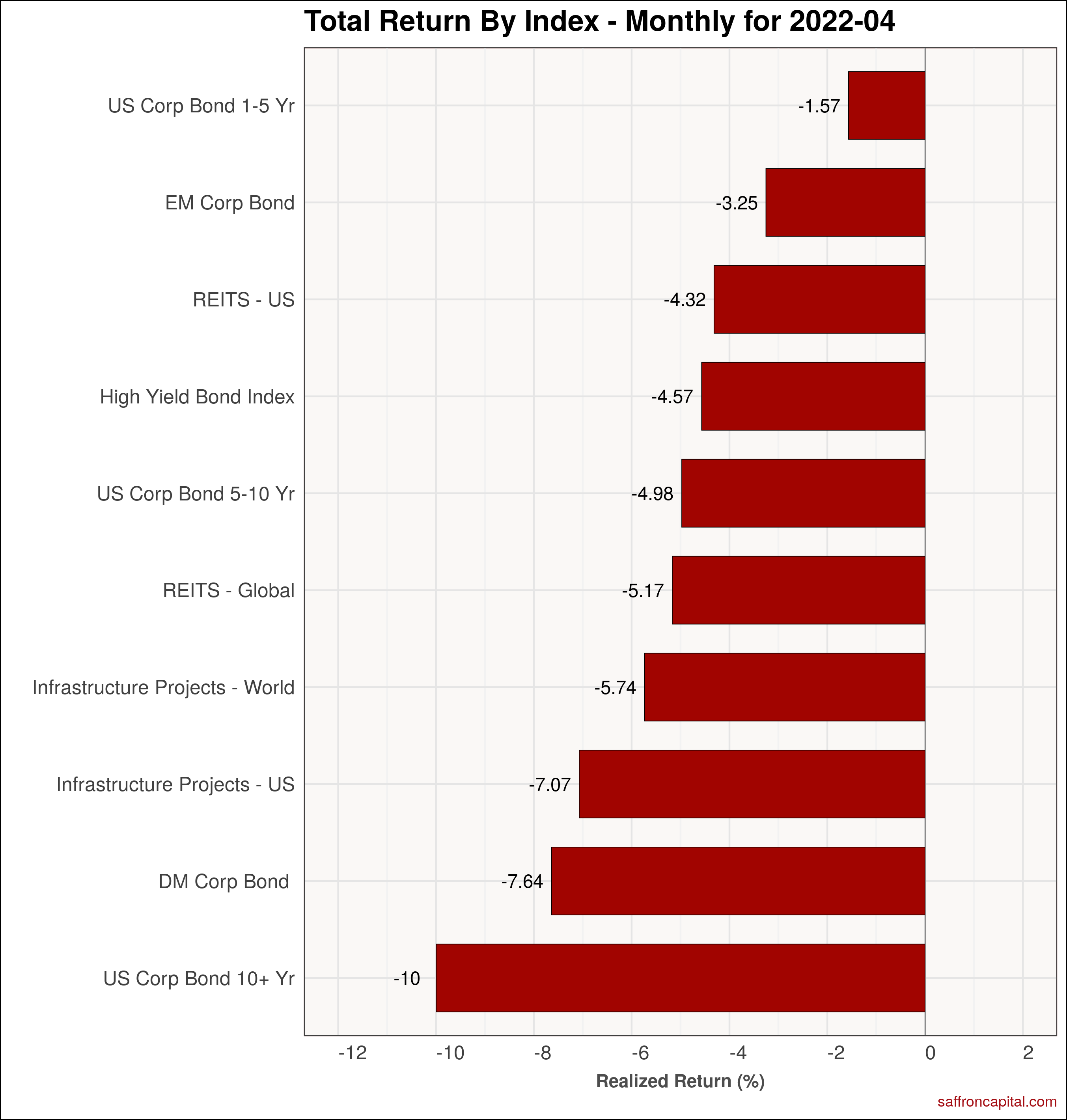

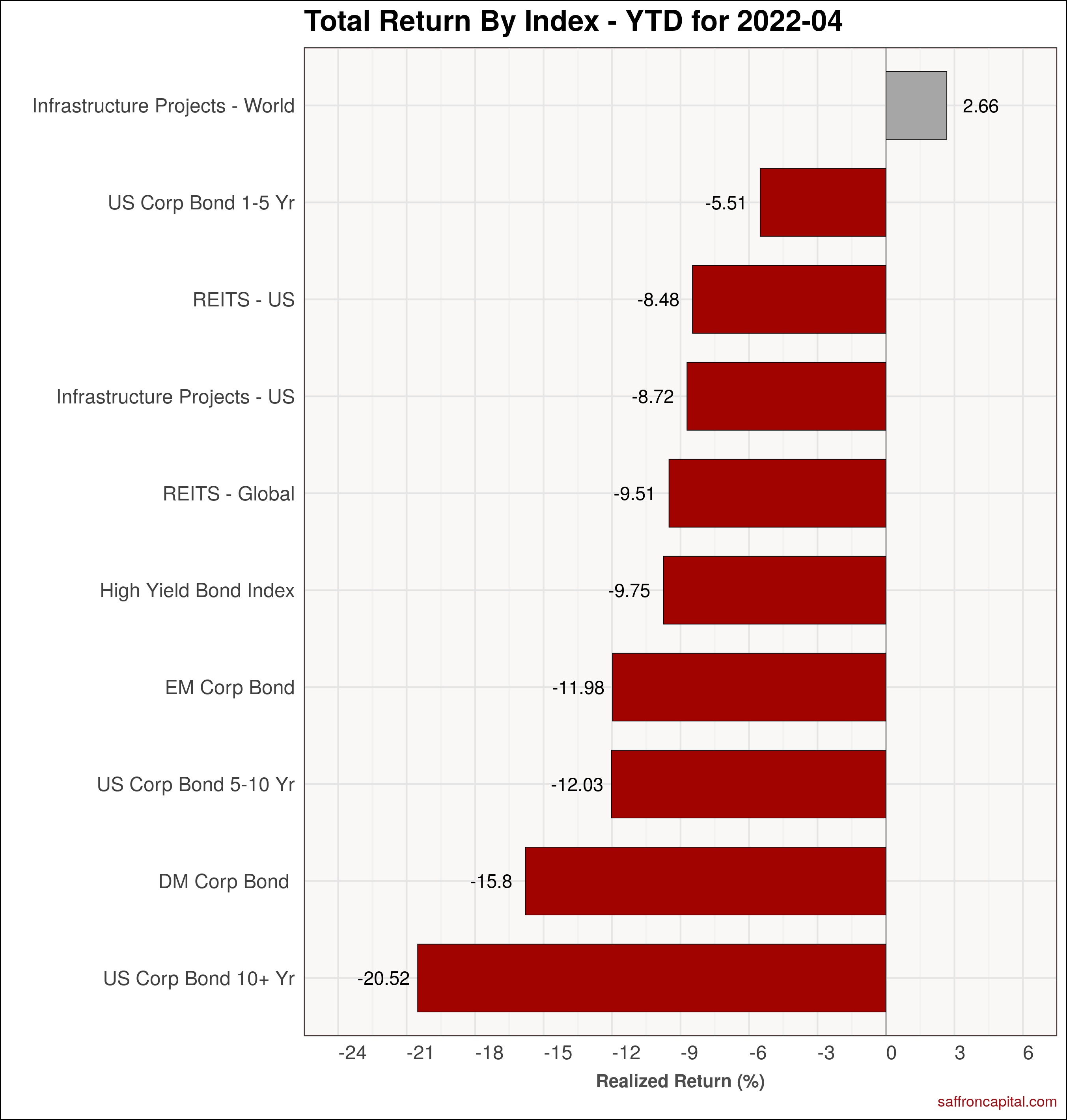

Corporate & Infrastructure Bonds

Corporate and infrastructure project bonds also suffered in April. The benchmark US Corp Bond 5 -10 Year index (-4.98%) outperformed the S&P 500 index and US treasuries of the same maturity. US and global infrastructure project bonds (-7.07% and -5.74%) have consistently outperformed US equities with prices rising until mid-April when prices dropped 15% from their peak. World infrastructure projects continue to have positive YTD returns and outperform the US project benchmark significantly.

Click to enlarge

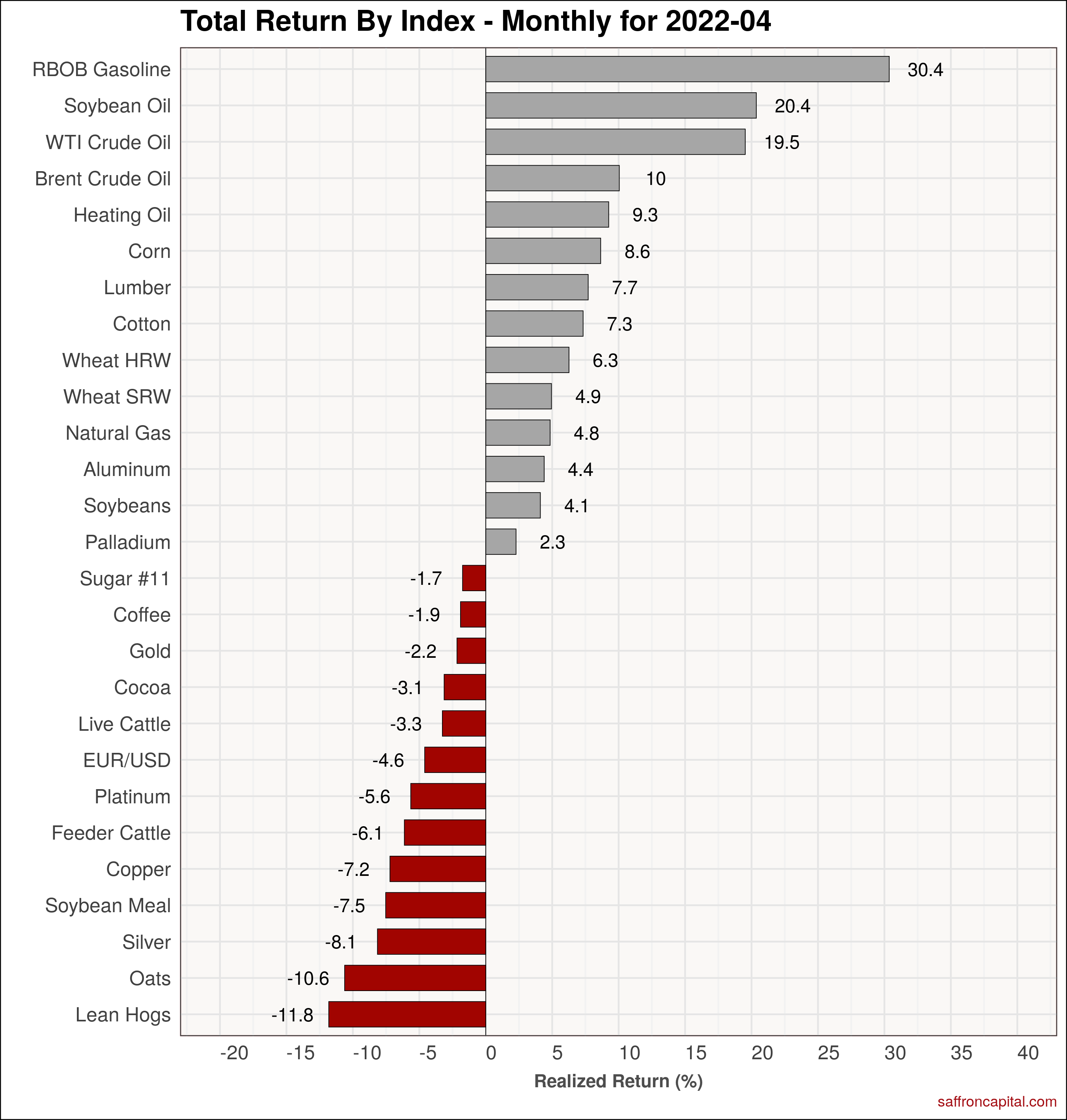

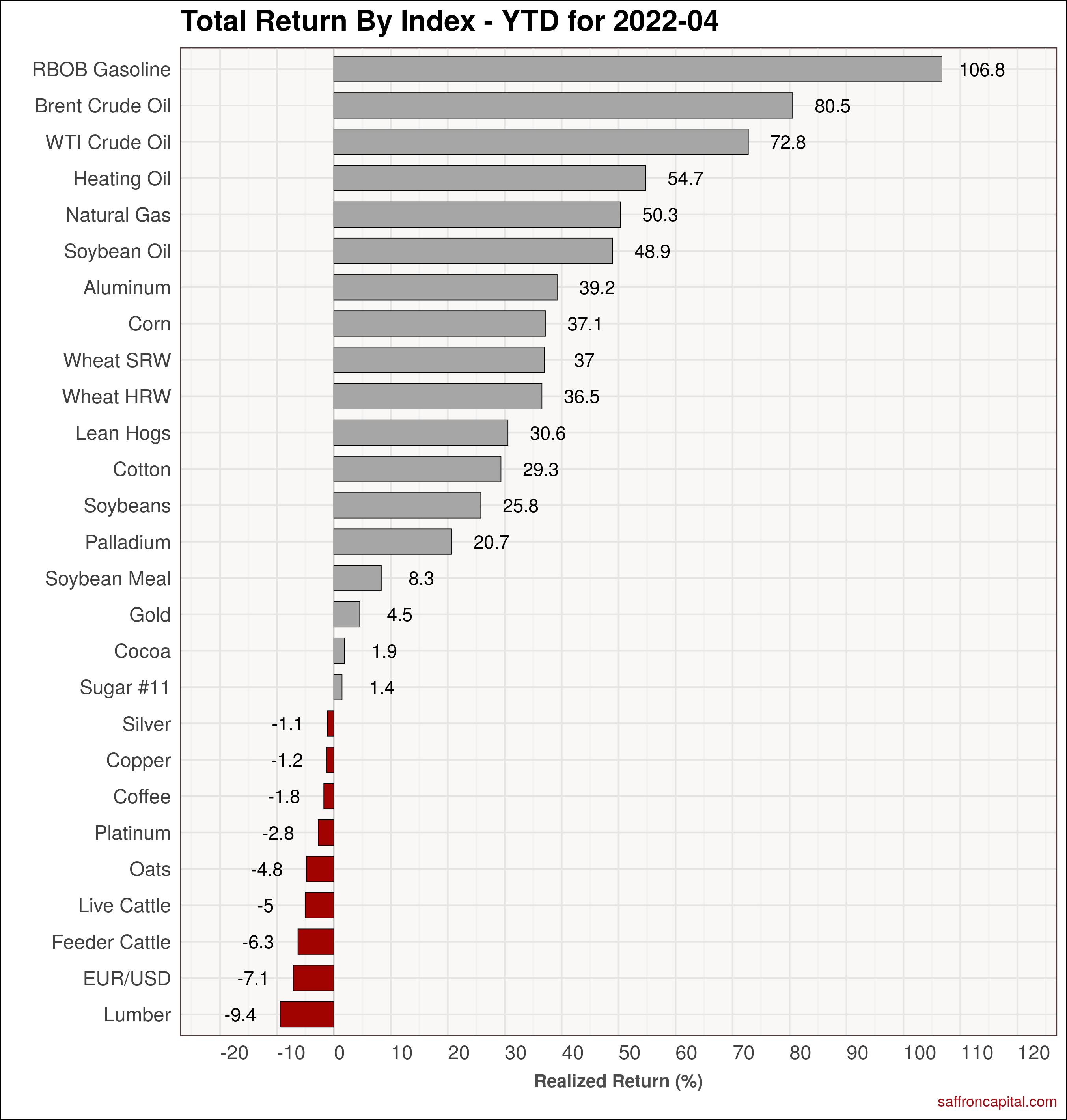

Commodities

Energy commodity prices have been strongly impacted by rising demand, supply disruptions and geopolitics. April was no exception and the year-to-date cumulative return is spectacular. Gasoline (+106.8%) WTI (+72.8%) and low sulfur diesel (+54.7%) have outpaced price changes in all other commodities. Grains and metals also seen material price inflation. However, precious metals were don in April and remain relatively weak on a year-to date basis.

Click to enlarge

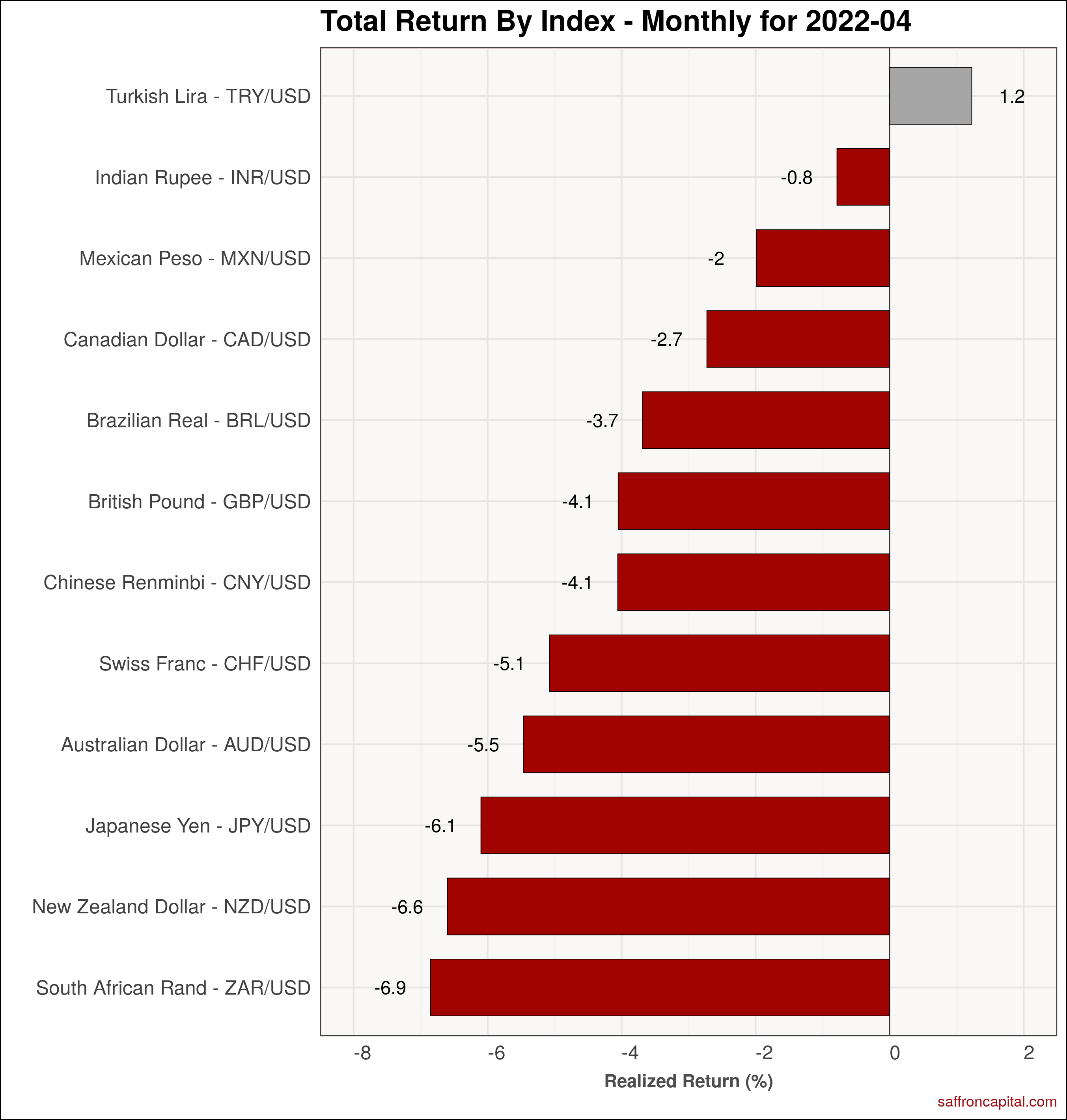

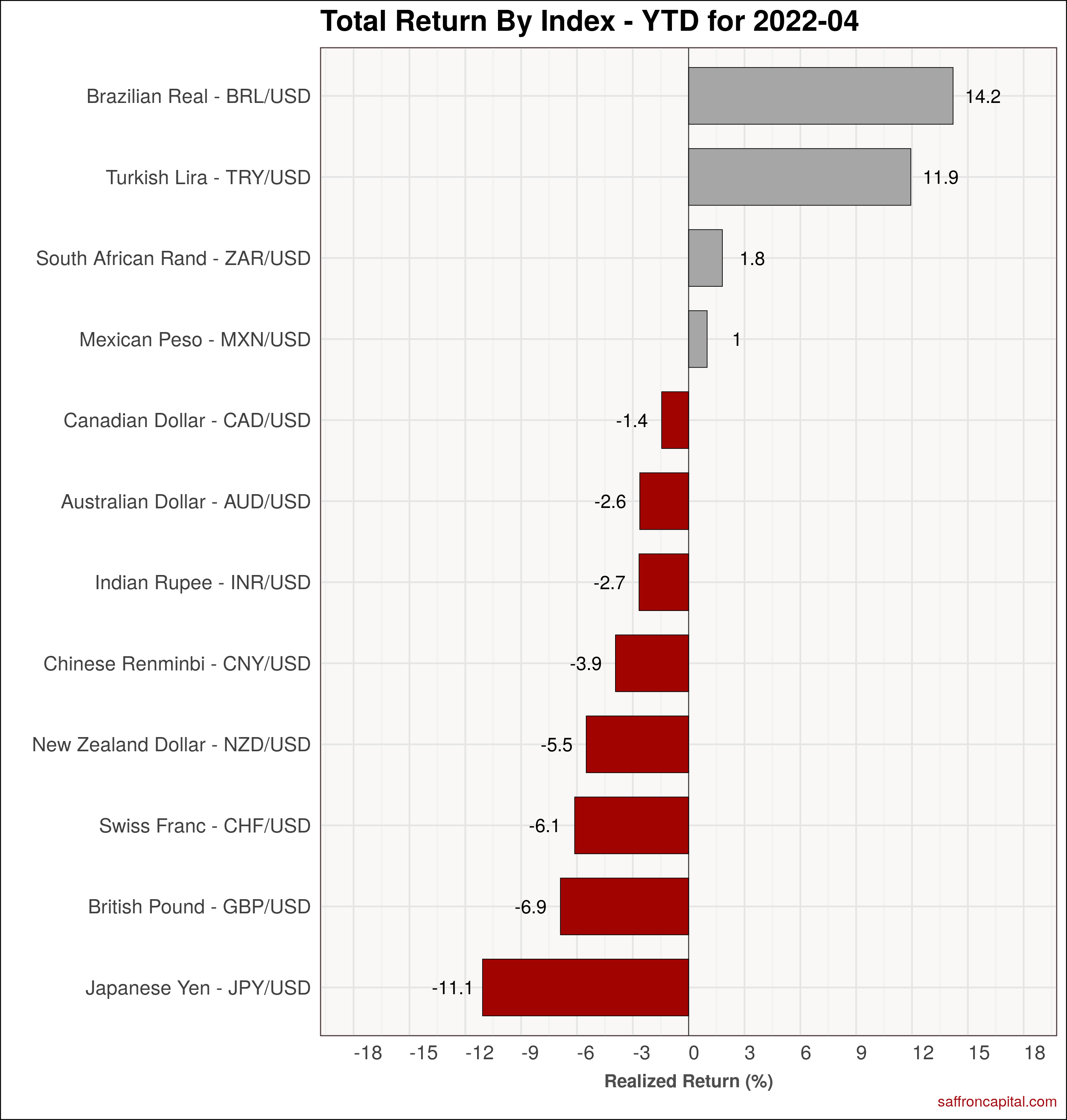

Currencies

The US Dollar continued to appreciate in April, negatively impacting all currencies, with the exception of the Turkish Lira (+1.2%). Since January, the Yen (-11.1%) has fallen the most, followed by the Pound (-6.9%) and the Swiss Franc (-4.1%).

Click to enlarge

Have questions about your portfolio? Looking for active risk management to secure your financial future? Contact us here.

{kind=link}

{kind=link}

{kind=link}