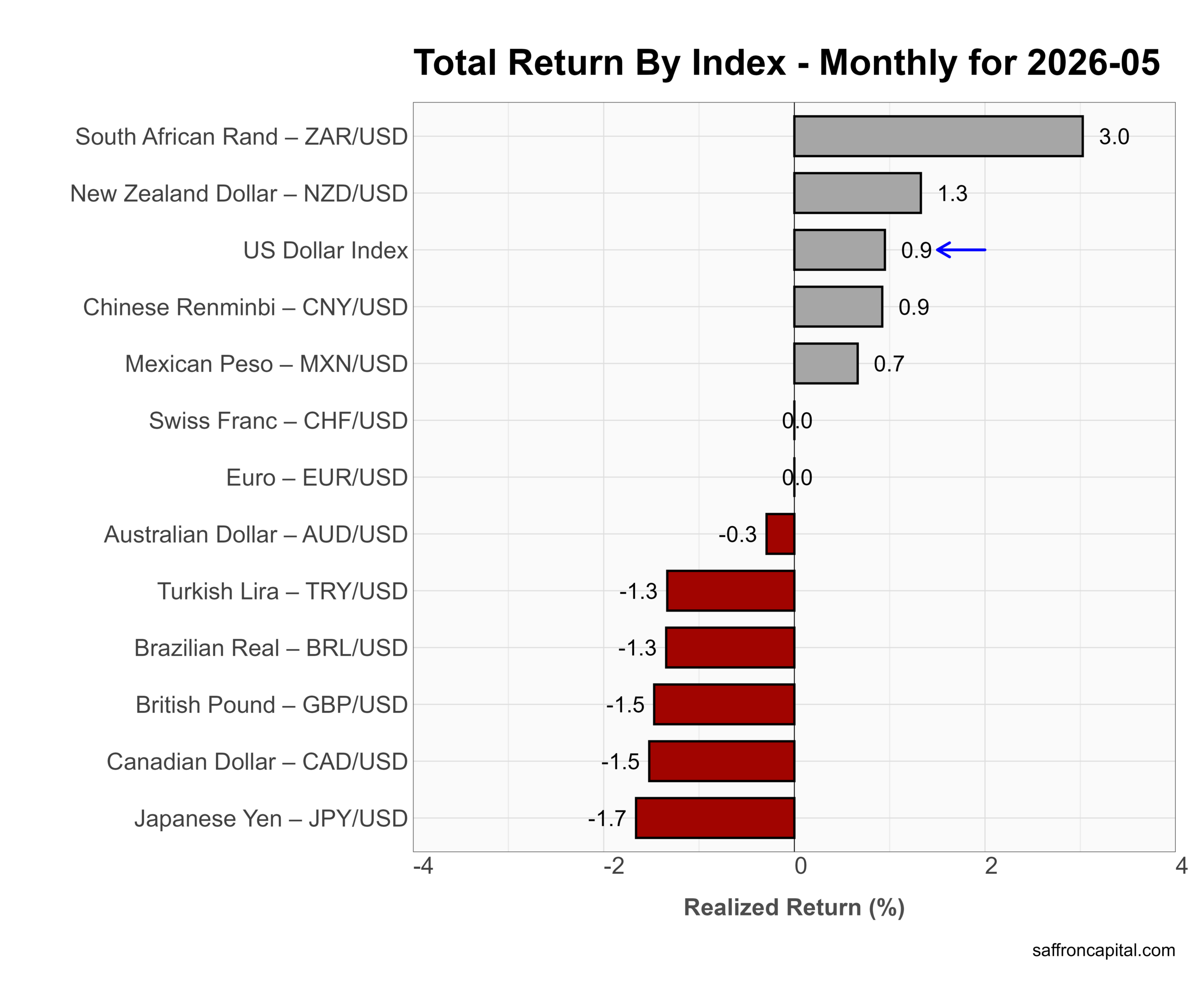

May produced a mixed currency market. The U.S. Dollar Index gained 0.9%, reversing part of the prior weakness. The South African rand led with a 3.0% gain, while the New Zealand dollar rose 1.3%. The renminbi and peso also advanced. In contrast, the yen fell 1.7%, while the pound, Canadian dollar, and Brazilian real lost more than 1%. The main takeaway is that dollar strength returned, but currency leadership remained fragmented rather than risk-off.

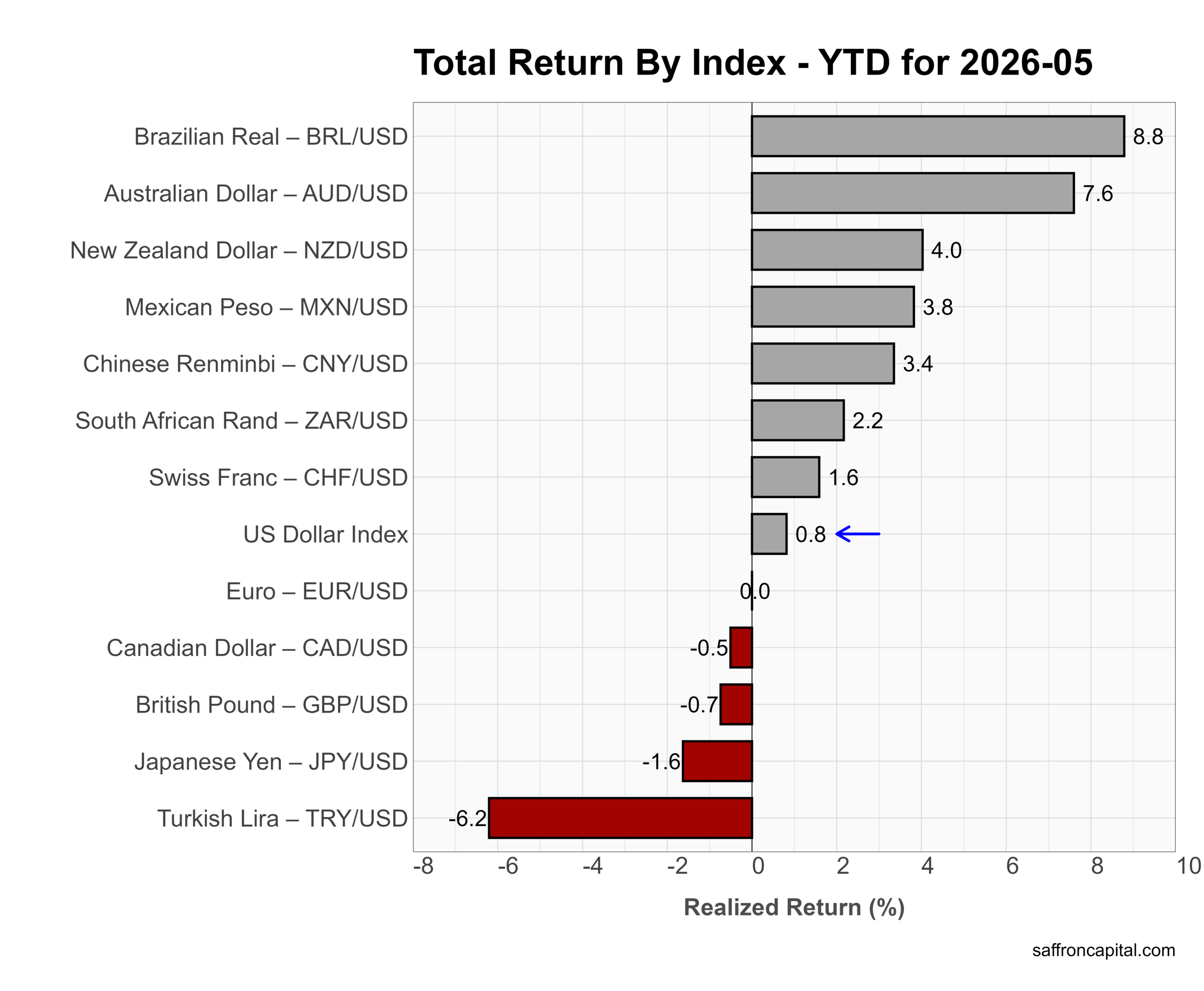

Year to date, commodity and export-oriented currencies still lead. The Brazilian real tops the rankings with an 8.8% gain, followed by the Australian dollar at 7.6%. The New Zealand dollar, peso, and renminbi also show solid advances. Meanwhile, the Dollar Index remains near unchanged at 0.8%, while the yen and pound continue to lag. The Turkish lira remains the weakest major currency at -6.2%. Overall, 2026 still favors commodity-linked currencies, although May suggests the dollar may be stabilizing after its earlier decline.

{kind=link}

{kind=link}

{kind=link}