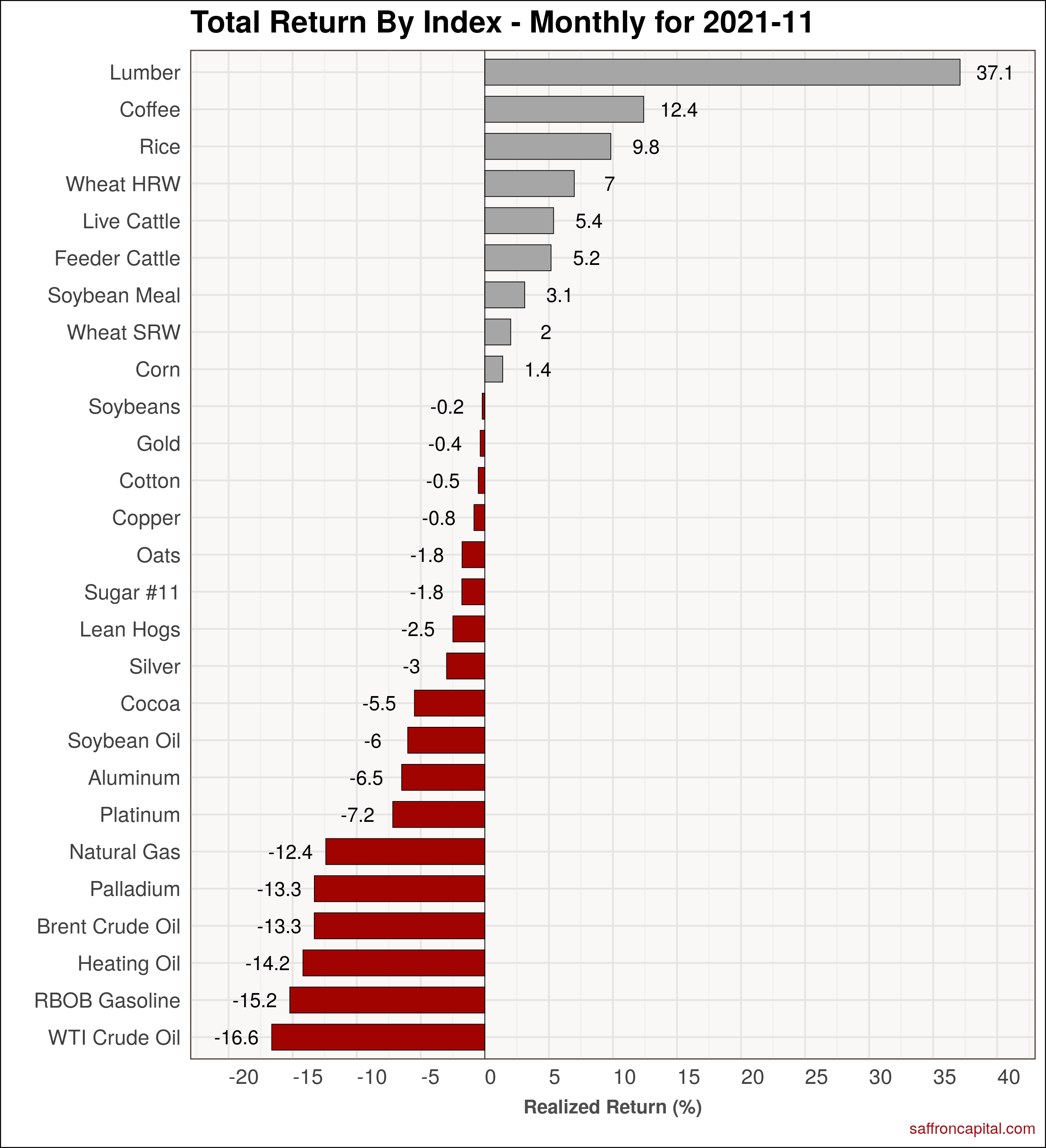

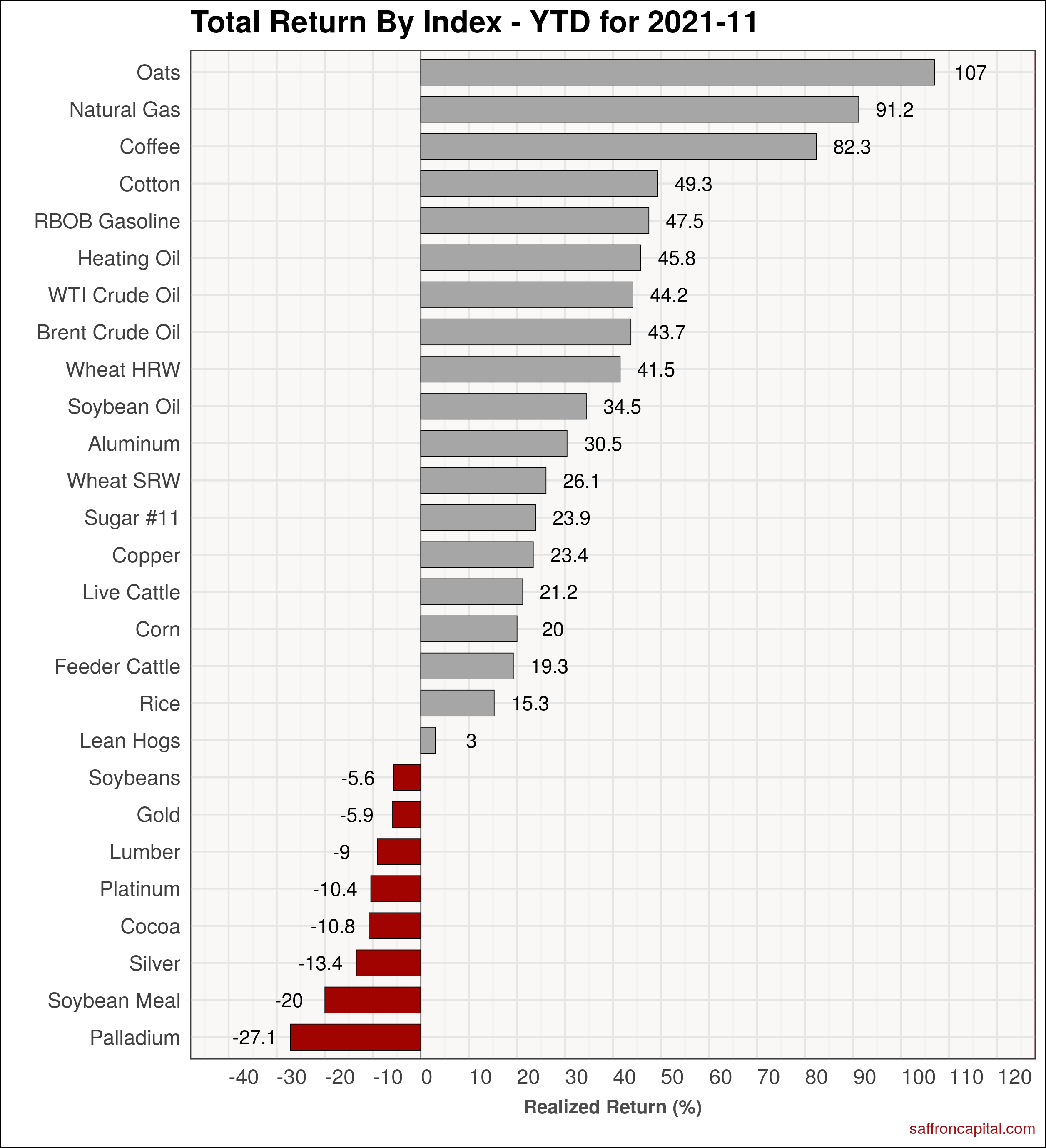

Red ink swept across the monthly results for most asset classes in November, highlighting the need for active risk management and strategies for capital preservation. Technology stocks performed well, as did U.S. investment grade bonds and inflation-indexed bonds. Finally, commodities continued to lead all asset groups with lumber, coffee and rice posting impressive gains.

The following analysis provides a detailed visual record of returns across and within the major asset classes, facilitating investor portfolio comparisons and performance benchmarking.

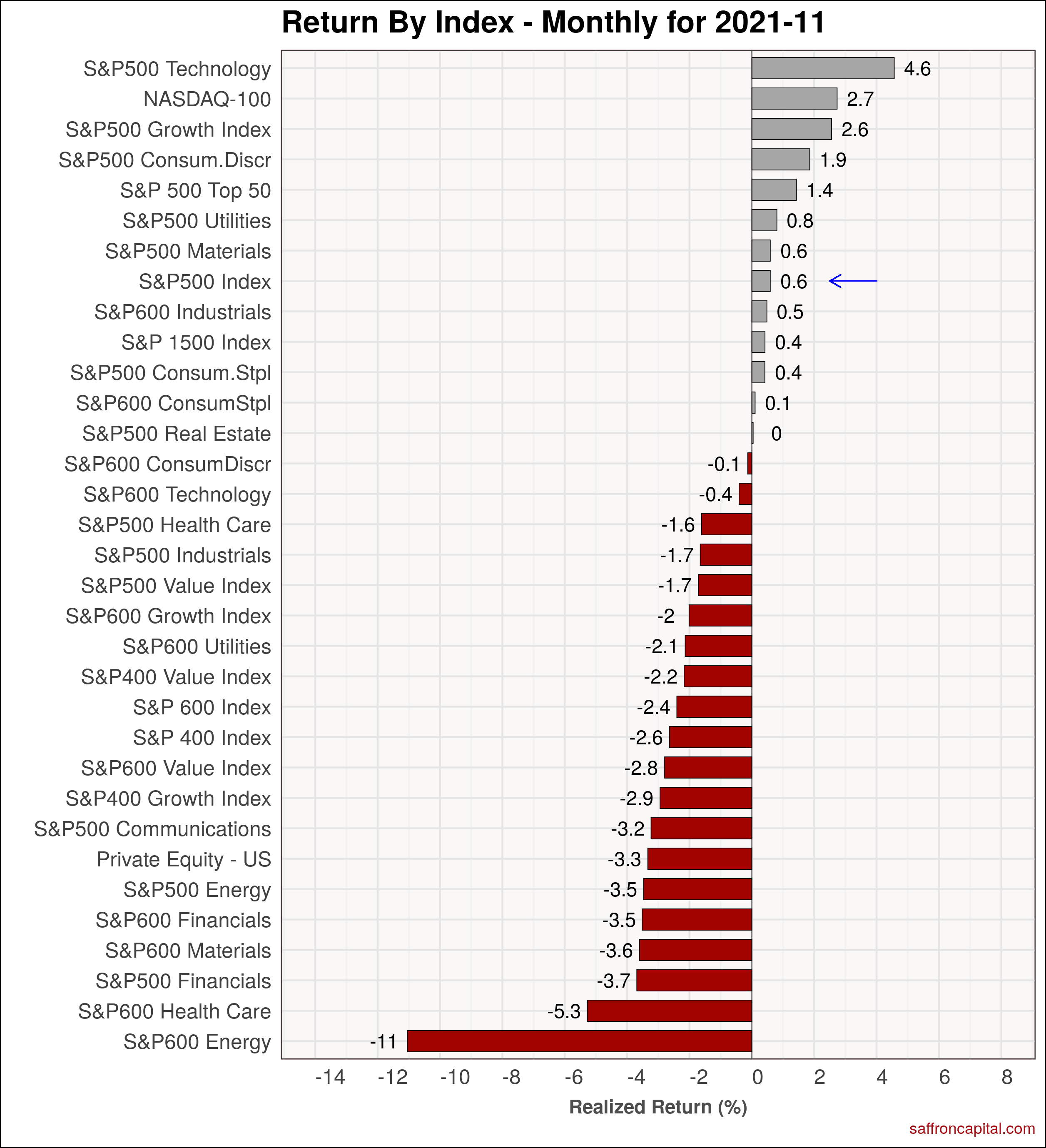

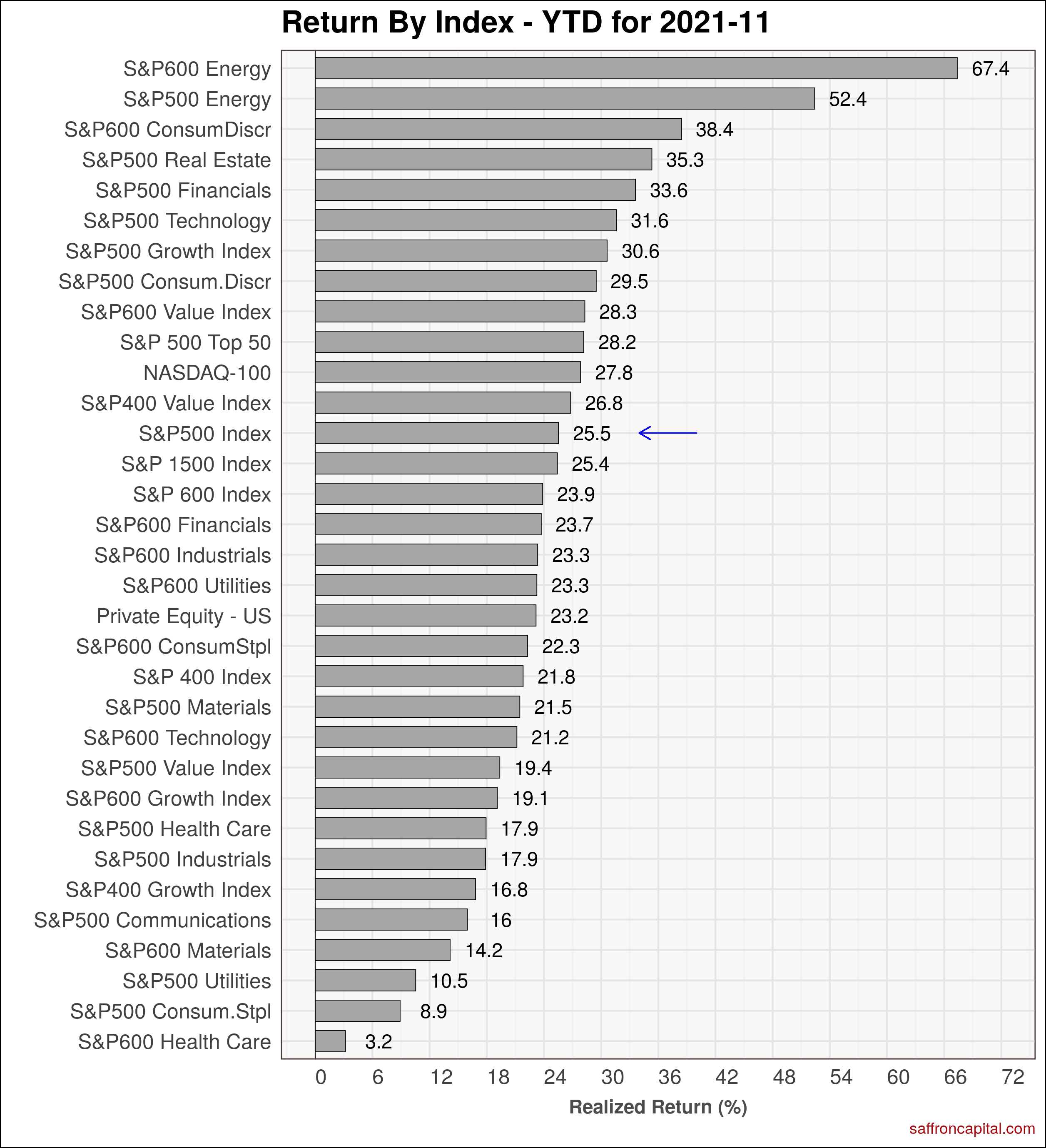

US Equities

The S&P 500 index was up 0.6% in November with year-to-date (YTD) returns of 25.5%. Technology sector stocks (+4.6%), the NASDAQ-100 index (+2.7%) and consumer discretionary stocks (+1.9%) proved to be safe havens given the recent volatility. Growth stocks (+2.6%) significantly outperformed value stocks (-1.7%).

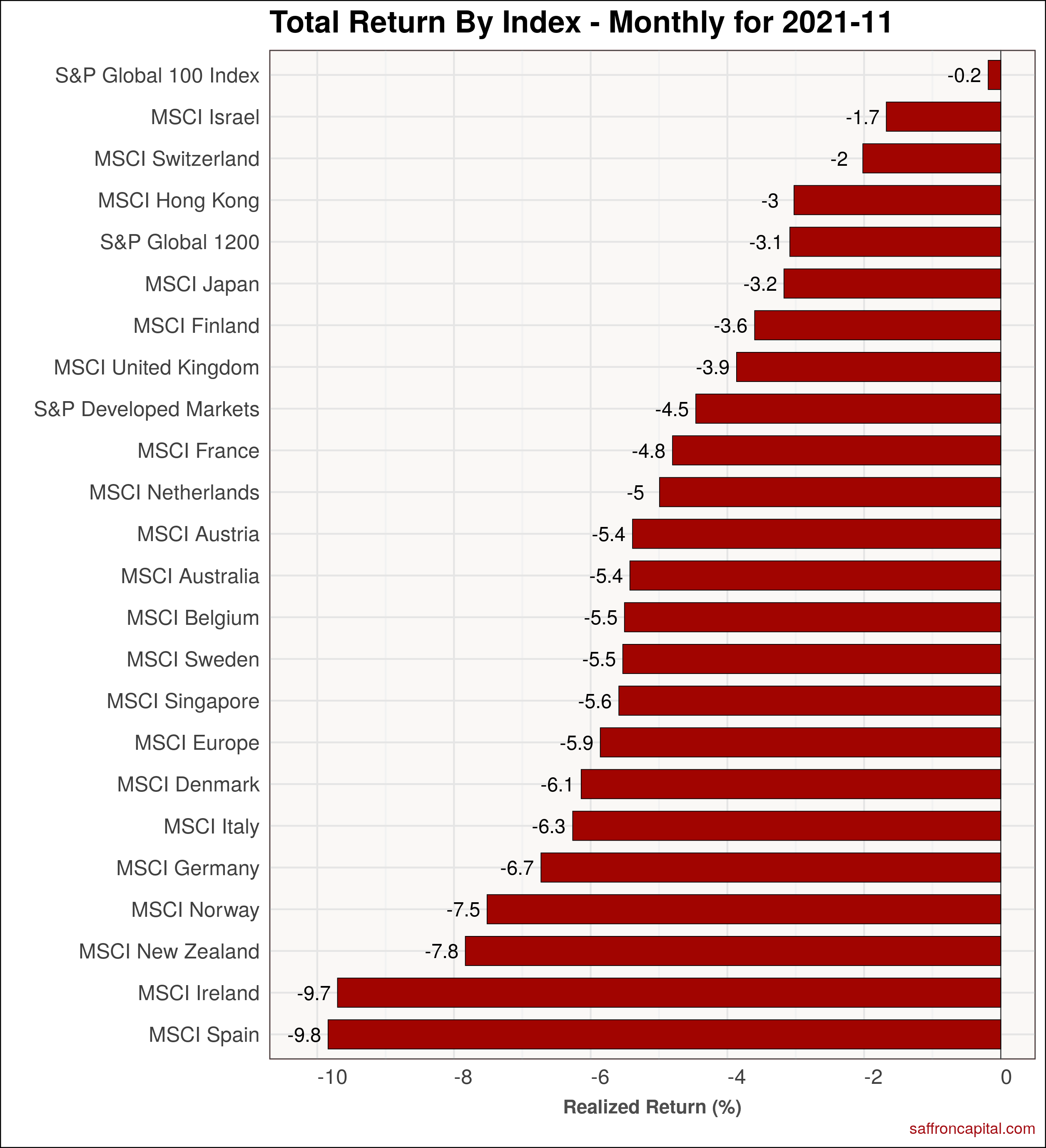

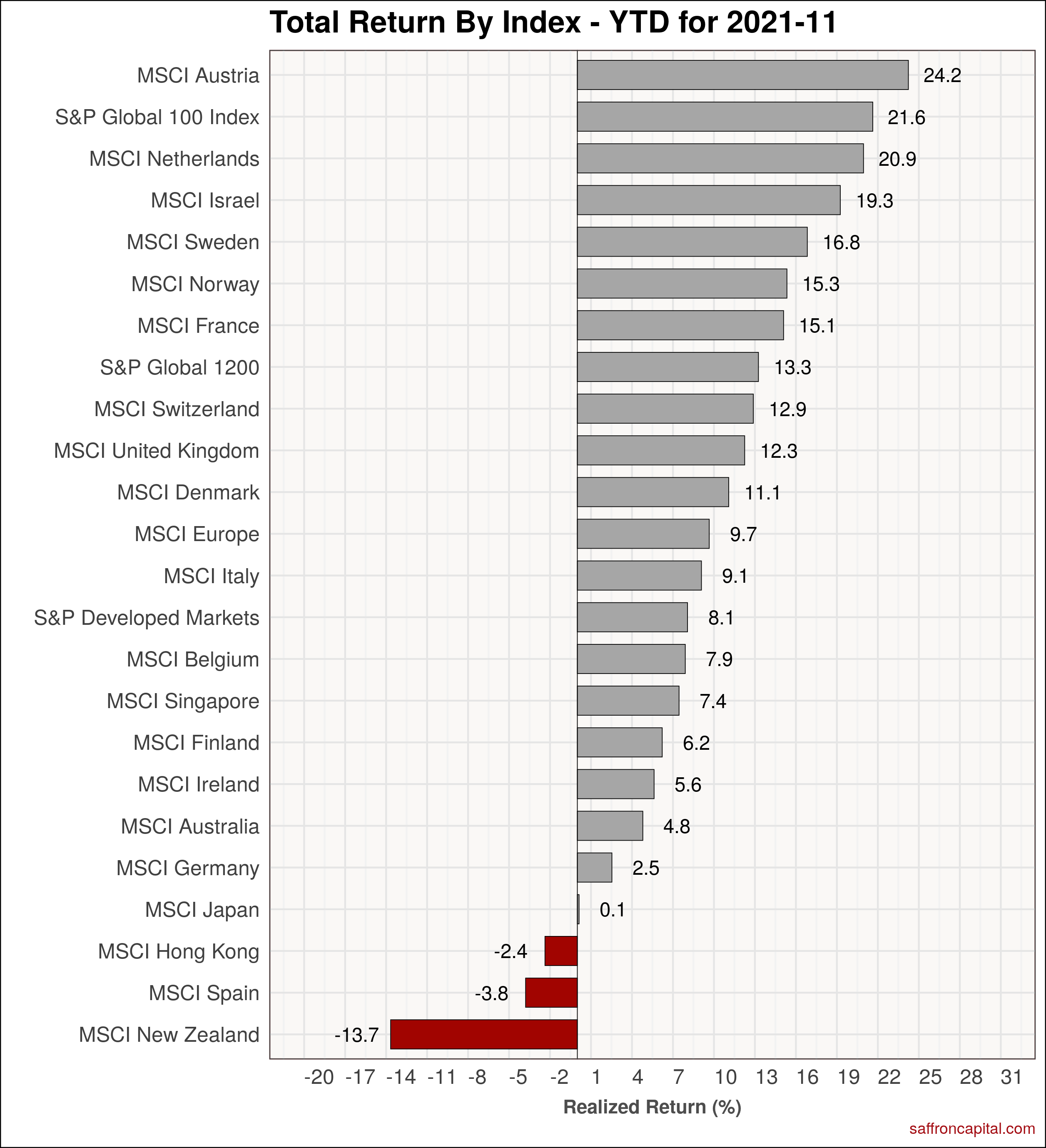

Developed Market Equities

Elsewhere, losses held sway as global equities lagged the US market. Israel (-1.7%), Switzerland (-2.0%) and Hong Kong (-3.0%) top the monthly performance chart. Meanwhile, the average YTD performance across the developed countries is roughly half that of U.S. performance benchmarks.

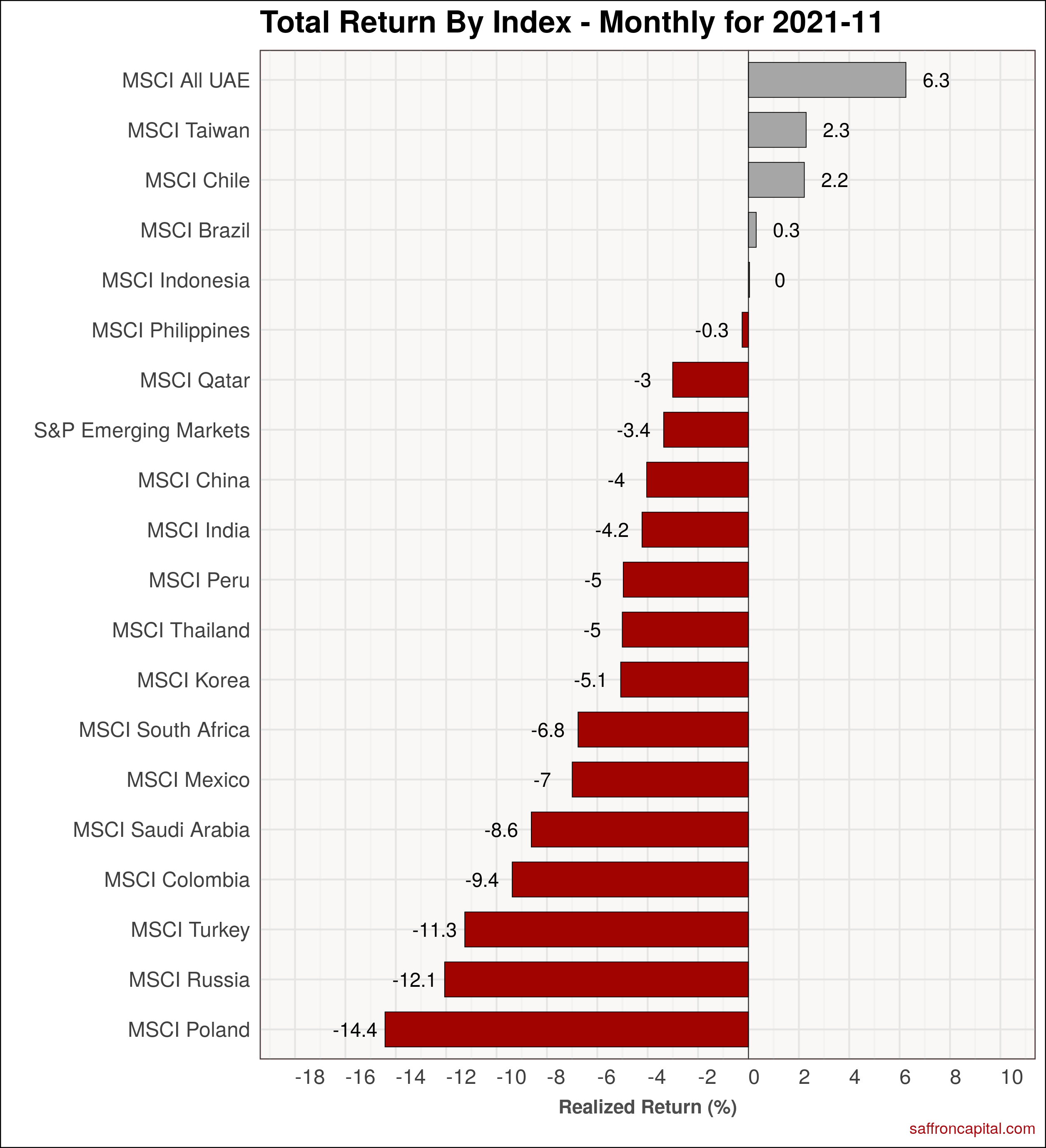

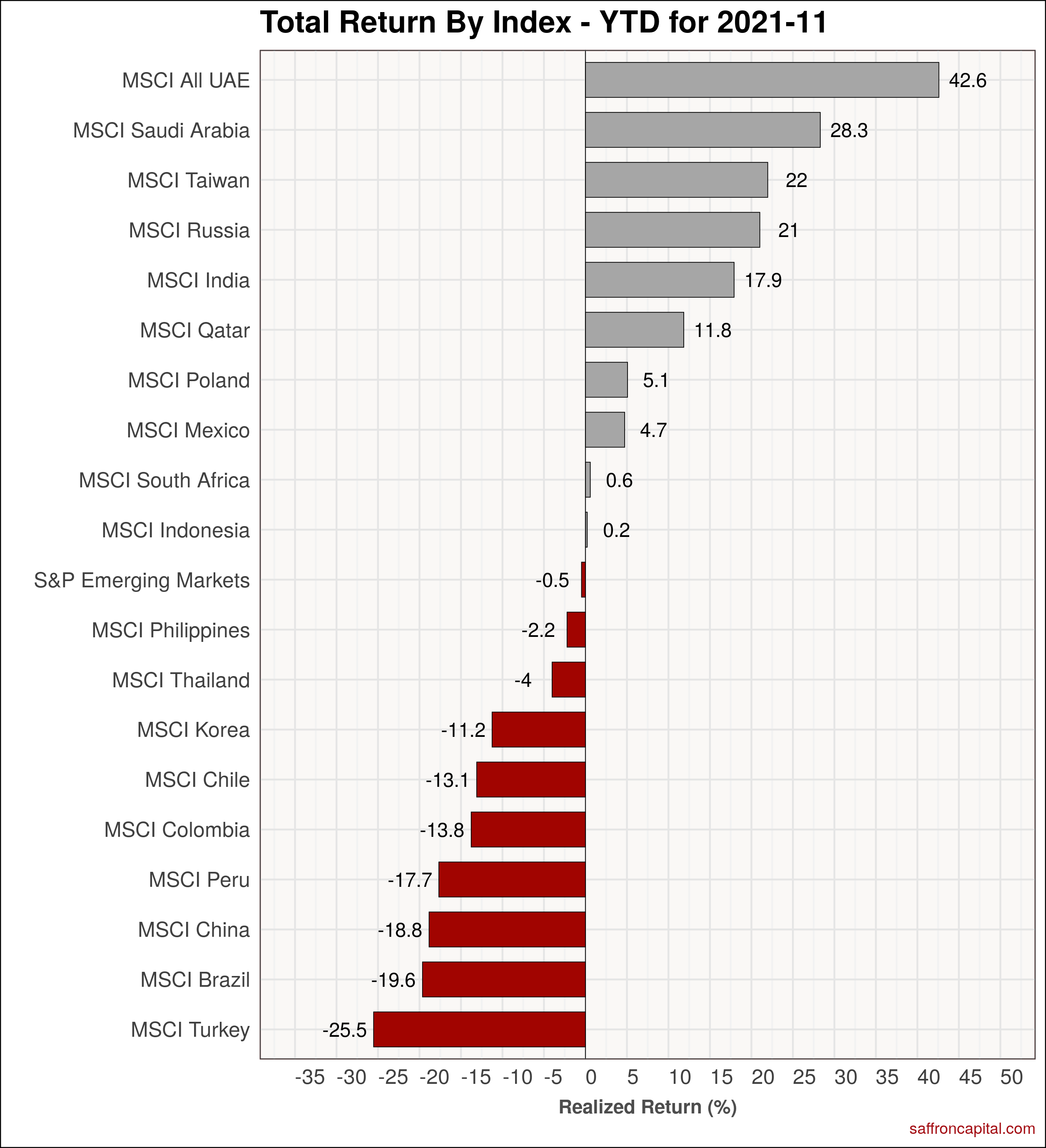

Emerging Market Equities

Emerging market economies that supply critical services and commodities beat U.S. market performance in November. For example, oil logistics, semiconductors and grains supported equity markets in the UAE (+6.3%), Taiwan (+2.3%), Chile (+2.2%), and Brazil (+2.2%). Meanwhile, natural resource and high growth economies top YTD performance.

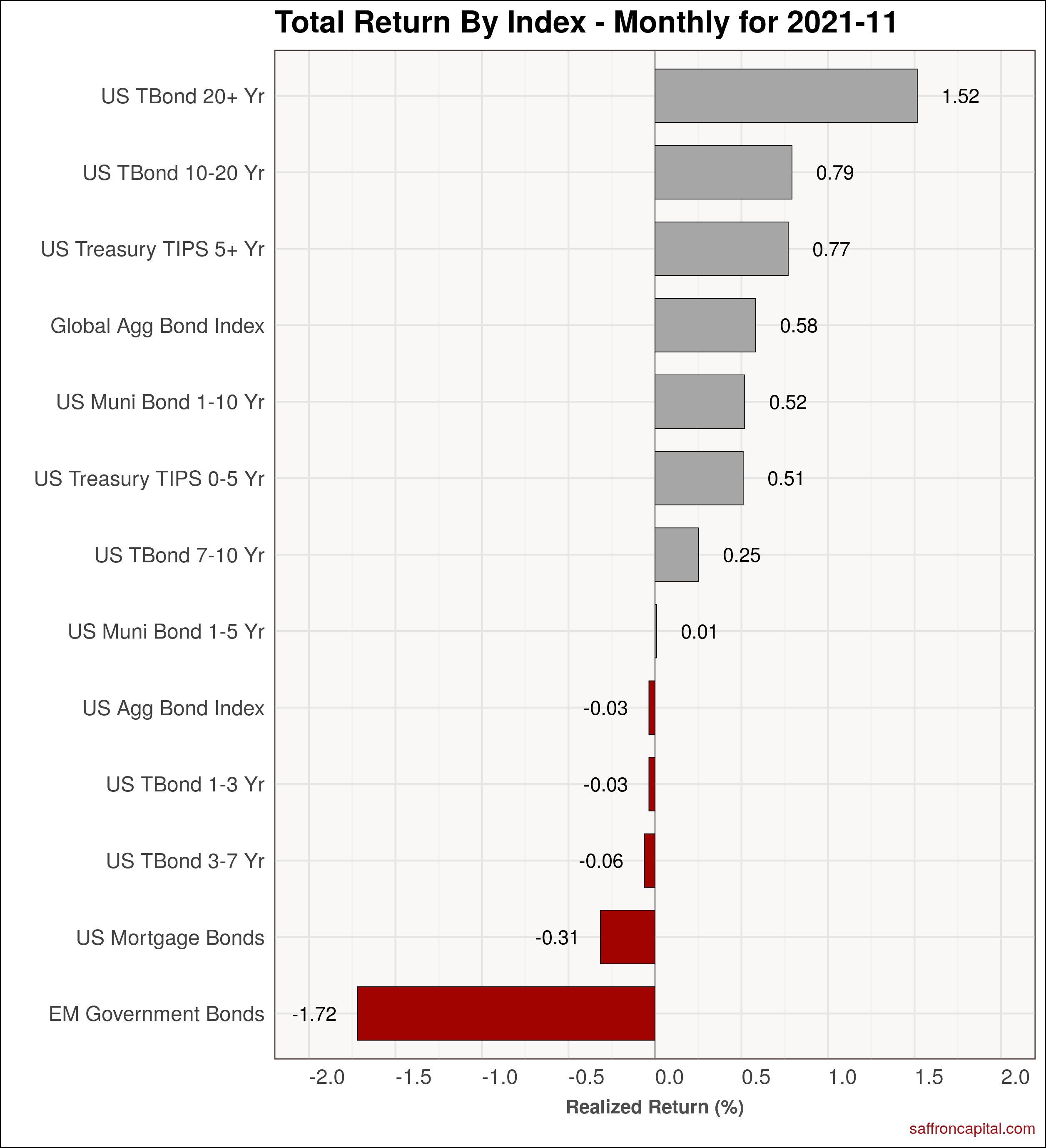

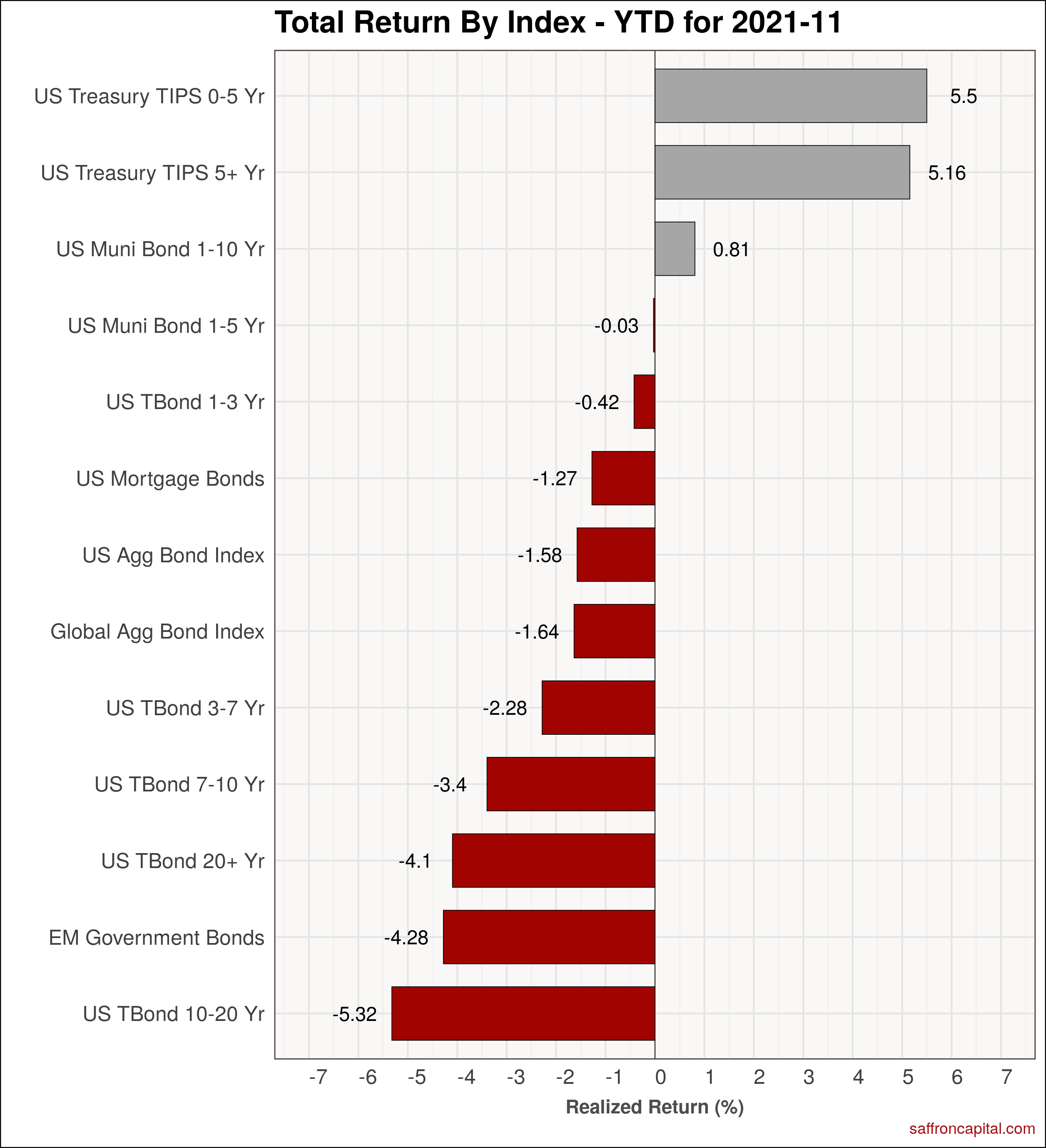

Government Bonds

U.S. Government bonds also outperformed U.S. equities in November. Top performance was in maturities of 20 years or more (+1.52%), 10 to 20 years (+0.79), plus inflation-indexed bonds (+0.77%). On the downside, emerging market bonds (-1.72%) were hard hit by inflation and covid concerns. Finally, inflation-indexed bonds continue to lead YTD results.

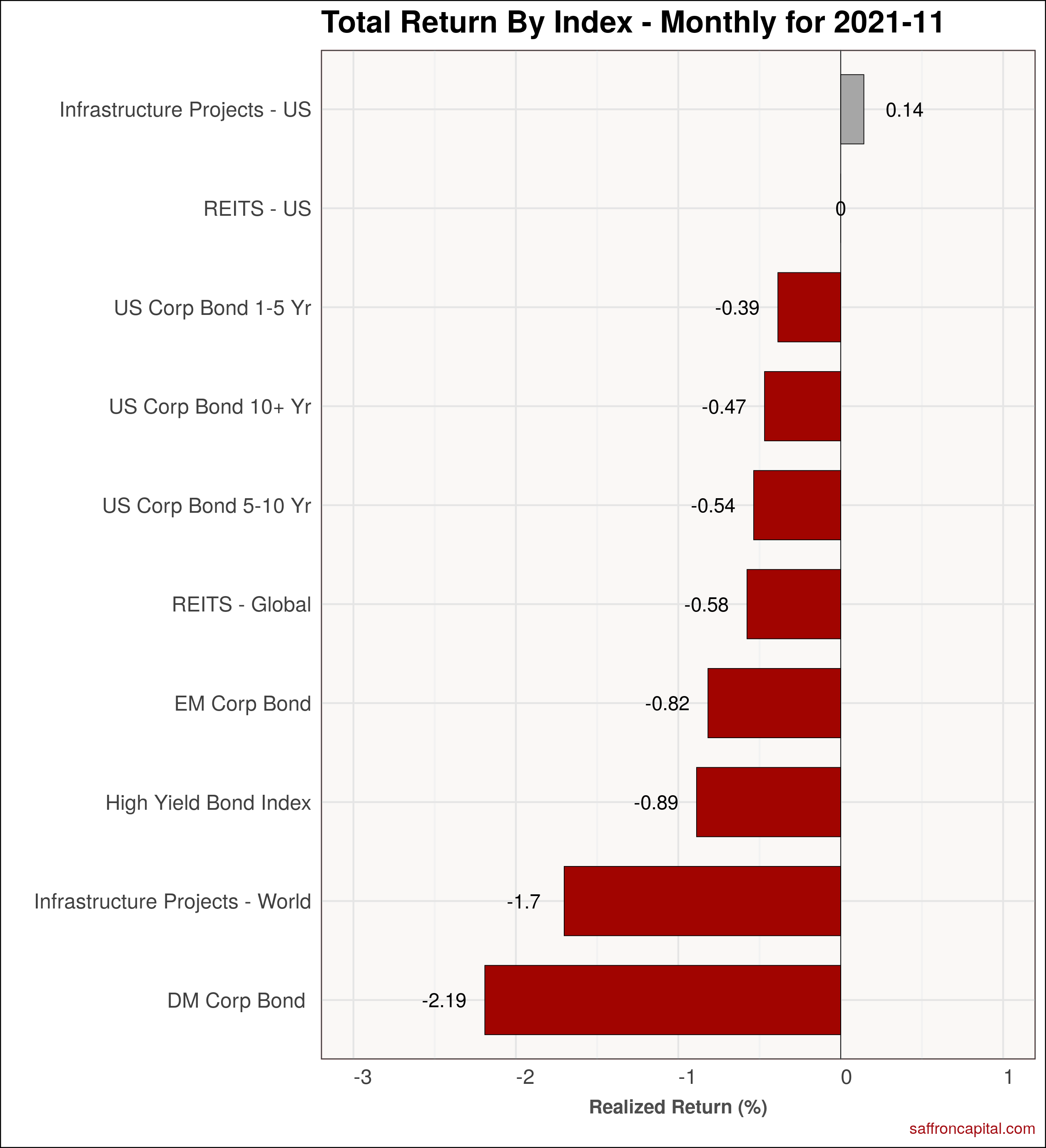

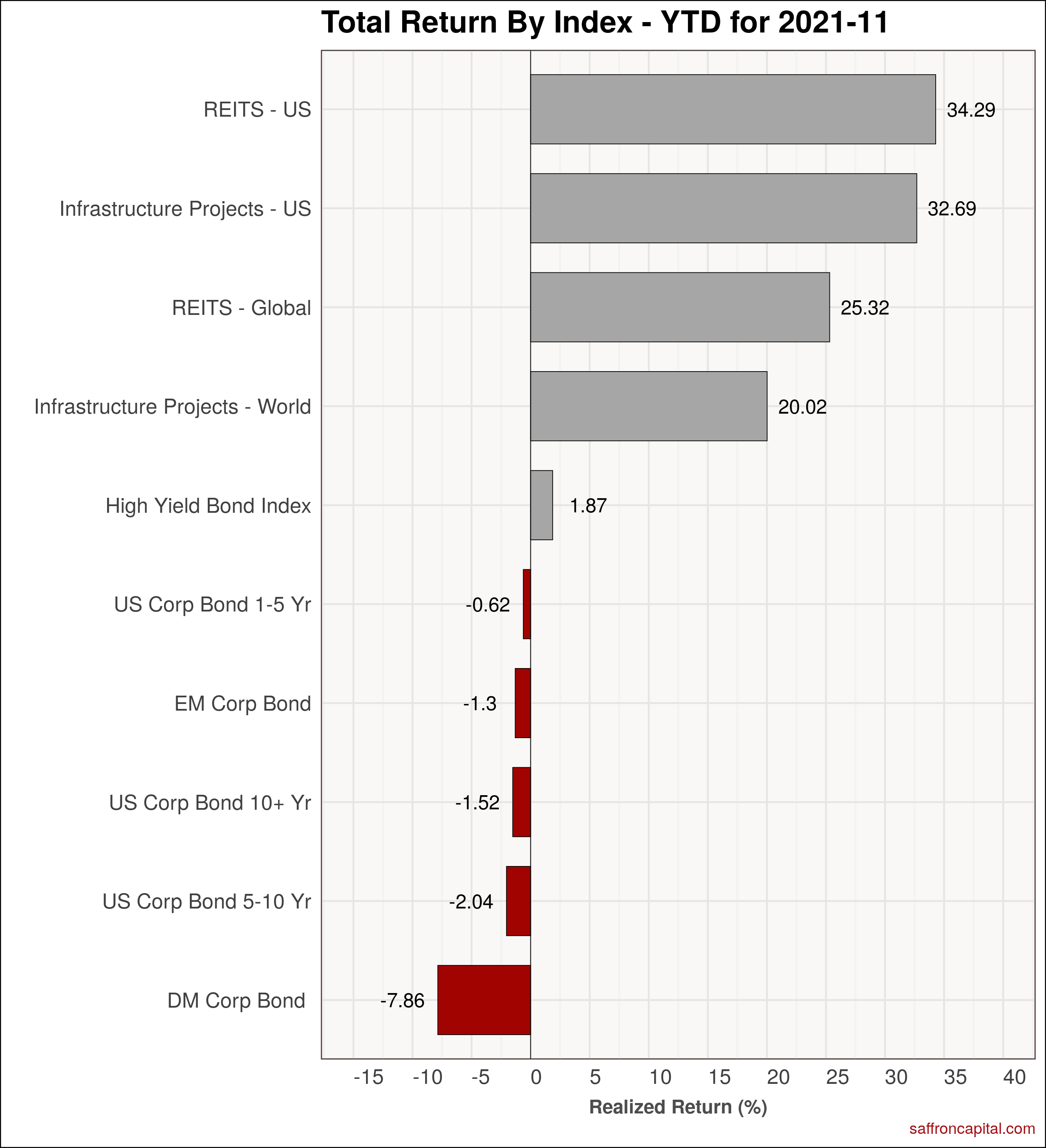

Corporate & Infrastructure Bonds

US infrastructure bonds (0.14%) and REITS (0.0%) barely avoided losses in November. However, their YTD performance is still significantly higher than US equities. Developed market corporate bonds (-2.19%) gave back nearly a quarter of their YTD performance this month given higher inflation and new covid risks.

Commodities

Commodities, again, led the broad asset classes in November, cementing their leadership role on a YTD basis. Lumber (+37.1%) surged, as did coffee (+12.4%), rice (+9.8%), and wheat (7.0%). Oil declined 16.6%, dropping 10% in just one day, pulling down gasoline (-15.2%) and heating oil (-14.2%) with it.

{kind=link}

{kind=link}