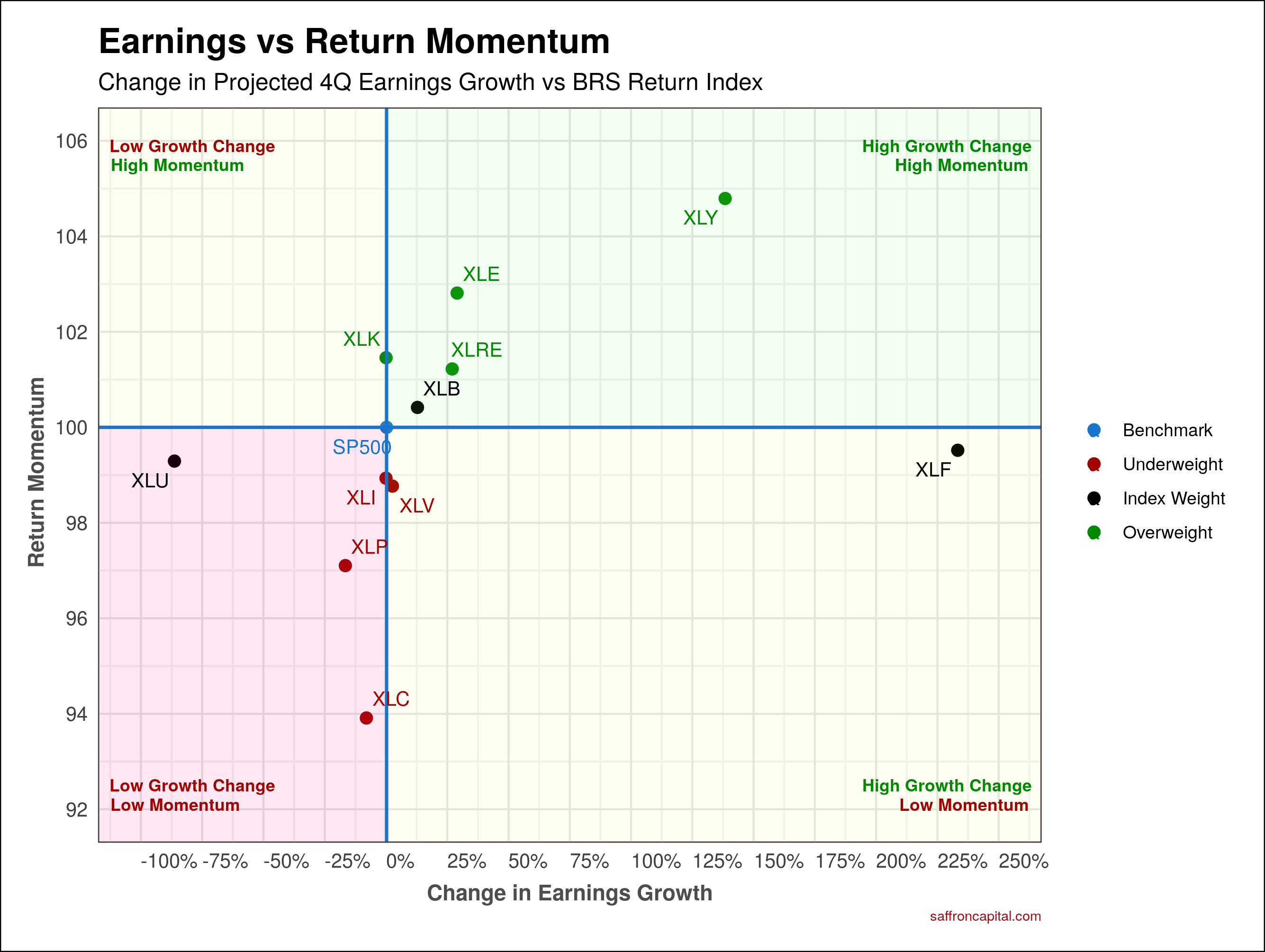

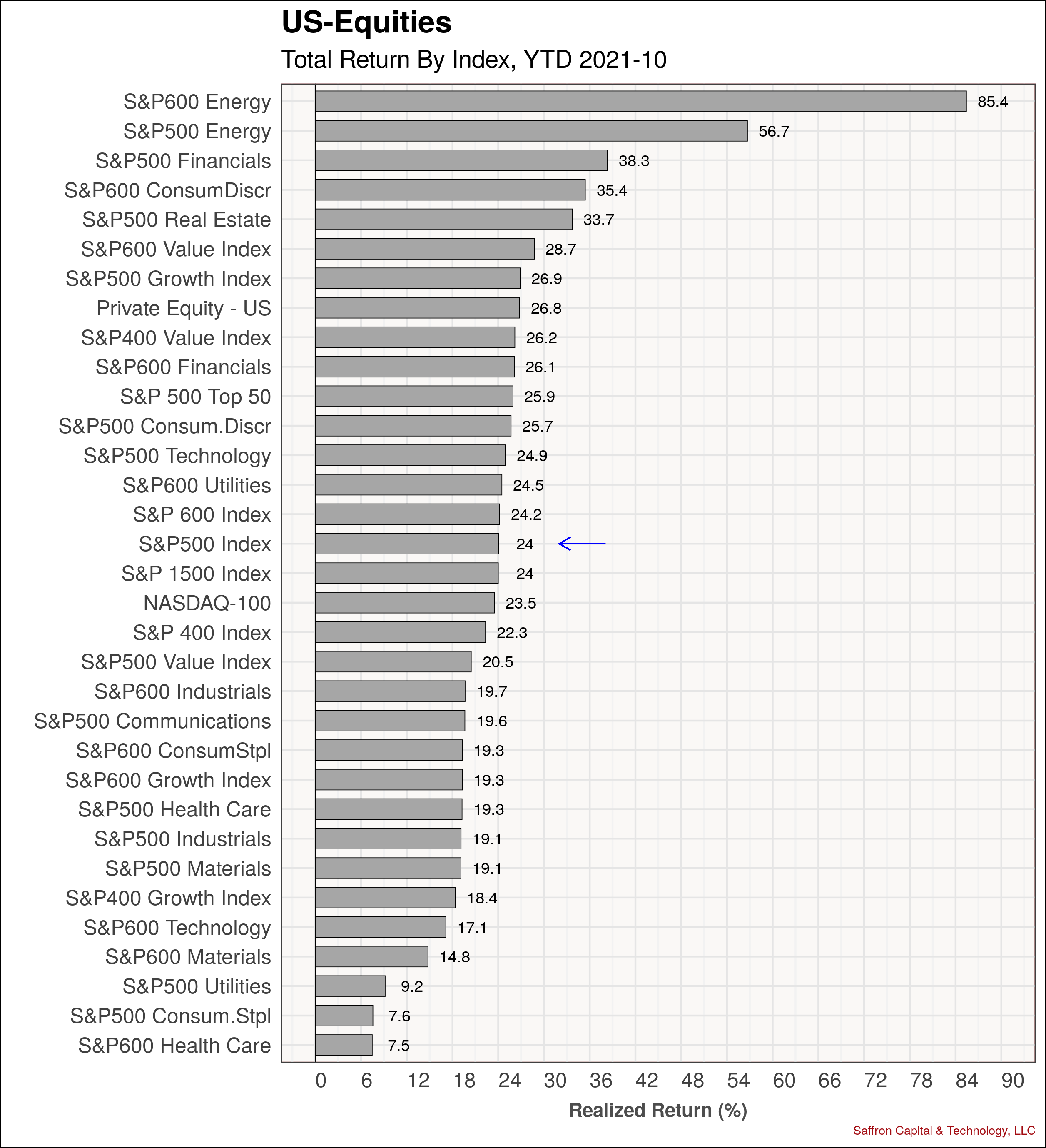

October returns were led by the stock market, which hit all time highs. As expected, the S&P 500 hit major highs at month’s end just as the earnings season kicked into high gear. The index has had three quarters in a row with annual net income growth higher than 30%. In addition, infrastructure project bonds and REITS were outstanding performers over the last 30 days. Meanwhile, the yield curve flattened during October with the long bond gaining in price and the short end falling. Commodity prices were mixed with Oats, Crude Oil and Gasoline topping all other markets. Finally, the Australian dollar rose the most among the major currency pairs against the U.S. Dollar

A detailed visual comparison of returns within and across the major asset classes is provided below:

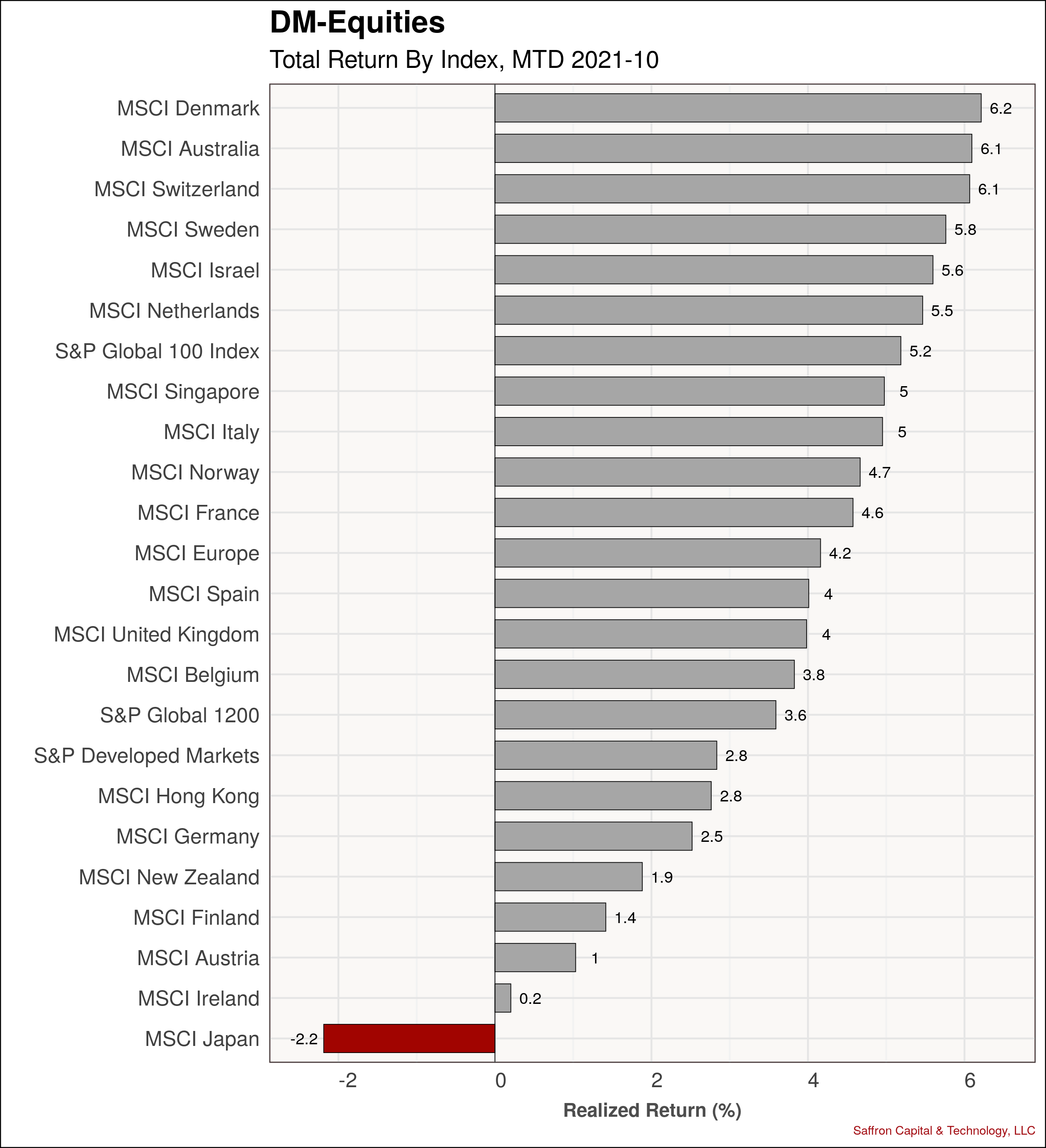

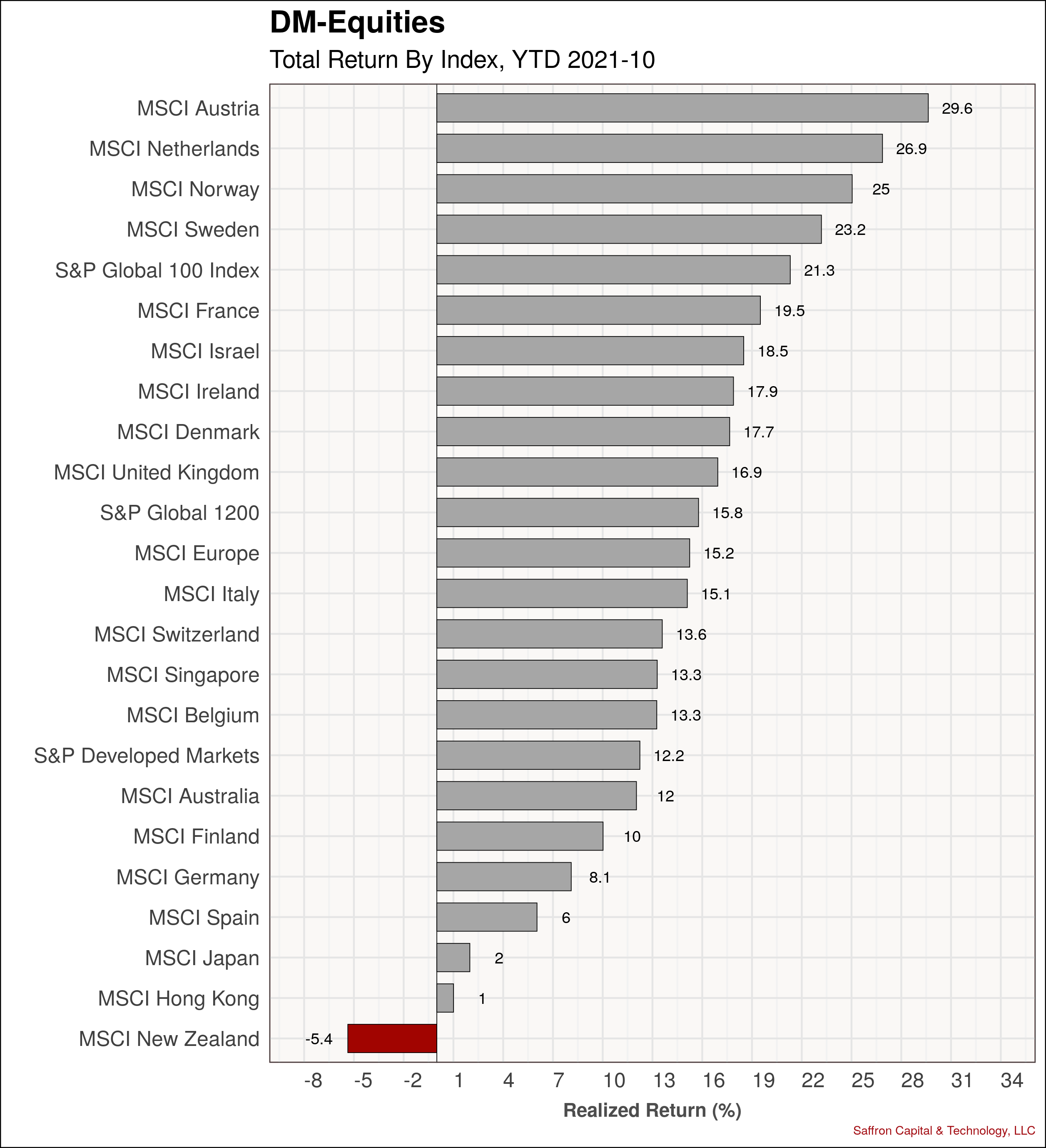

Developed Market Equities

On average, global equities continue to lag US markets but put in solid performance in October. Specifically, all major developed markets rebounded in October with the exception of Japan, which is vulnerable to high oil and LNG prices. Looking at YTD performance, we again see Austria, the Netherlands and Ireland topping the S&P 500 index. Otherwise, all major markets remain positive with the exception of New Zealand.

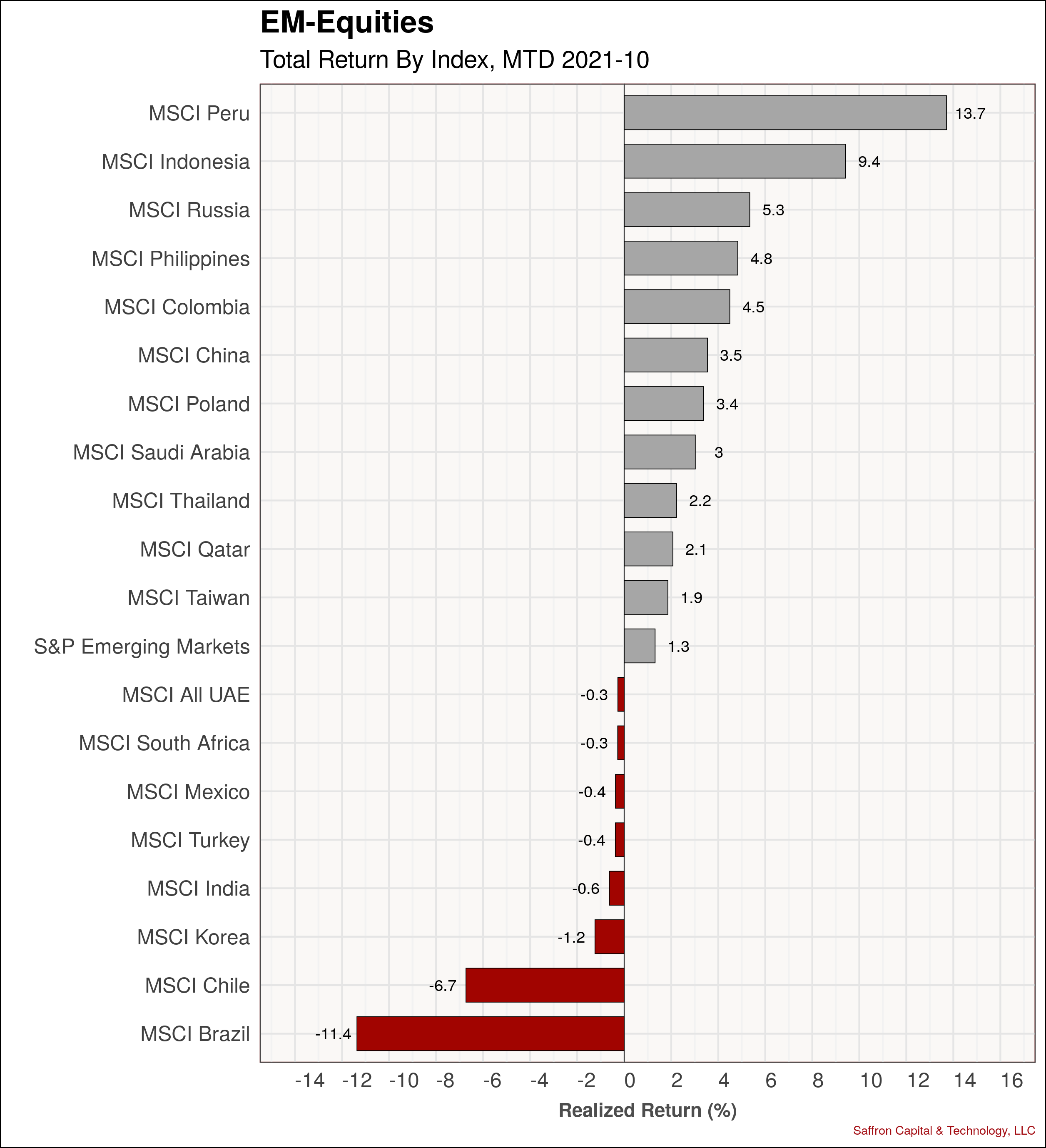

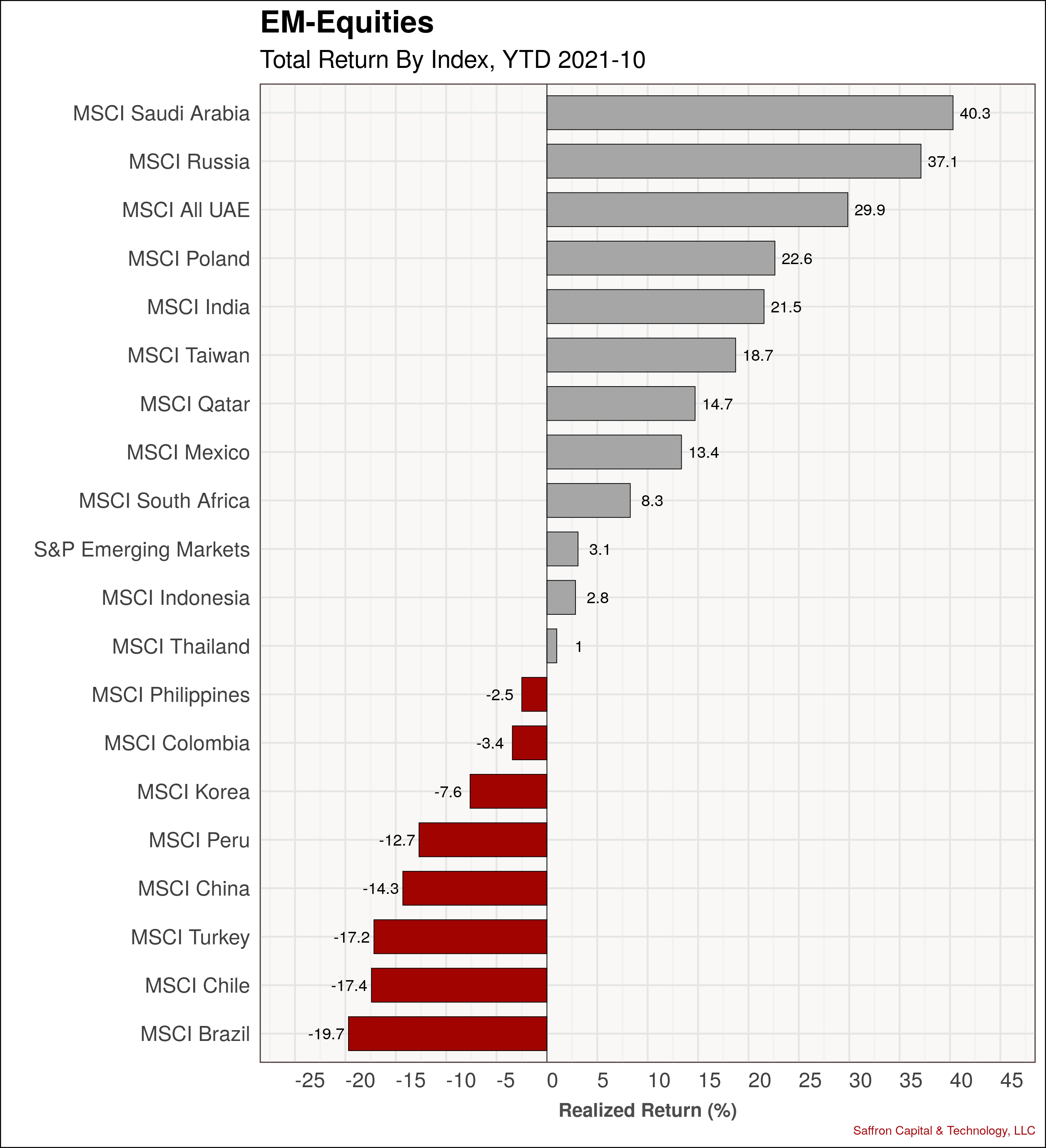

Emerging Market Equities

Peru and Indonesia led the emerging market list with solid gains, outperforming the US market. The 11.4% decline in the Brazilian market is notable. YTD performance continues to be dominated by oil and gas producers.

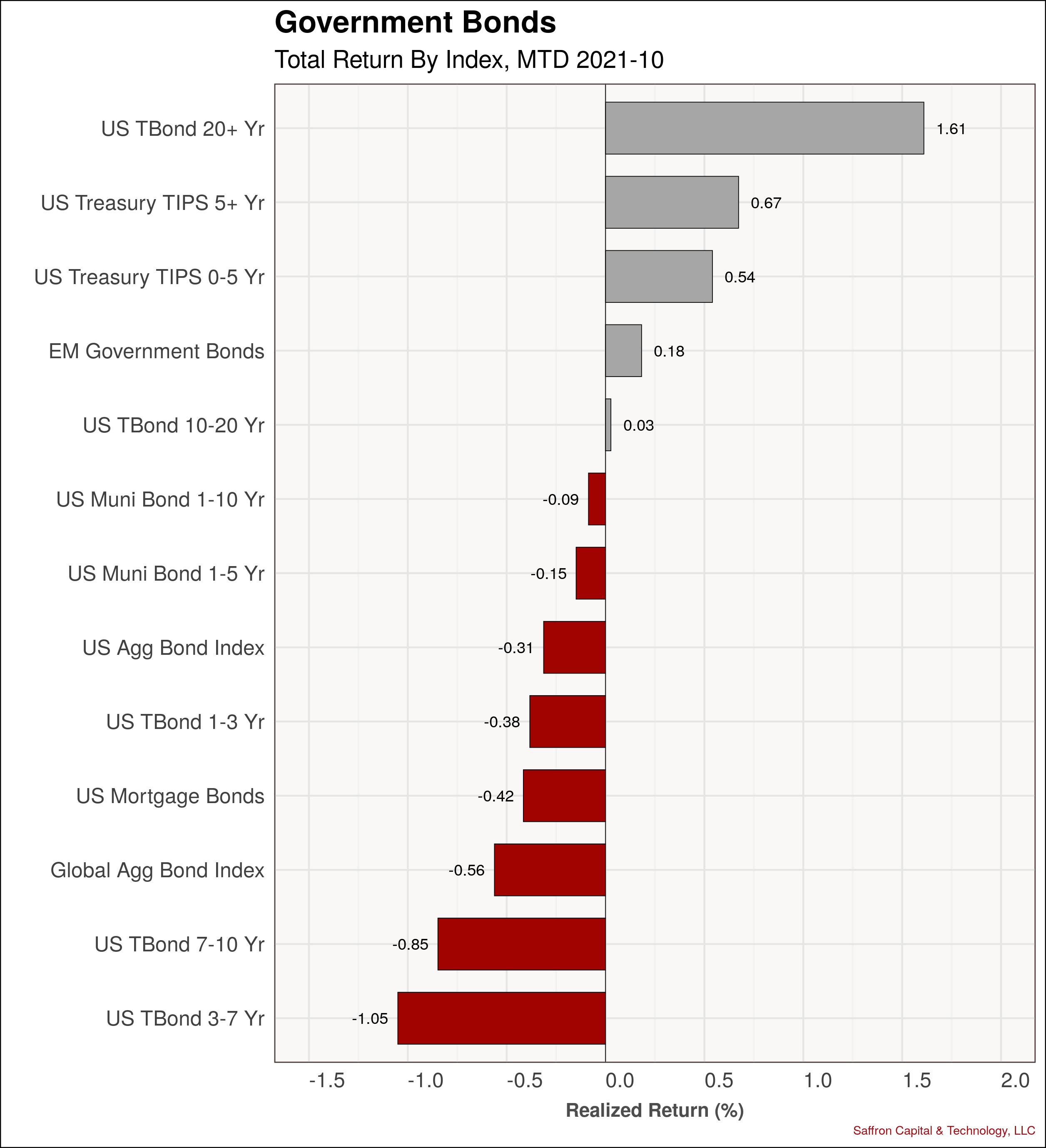

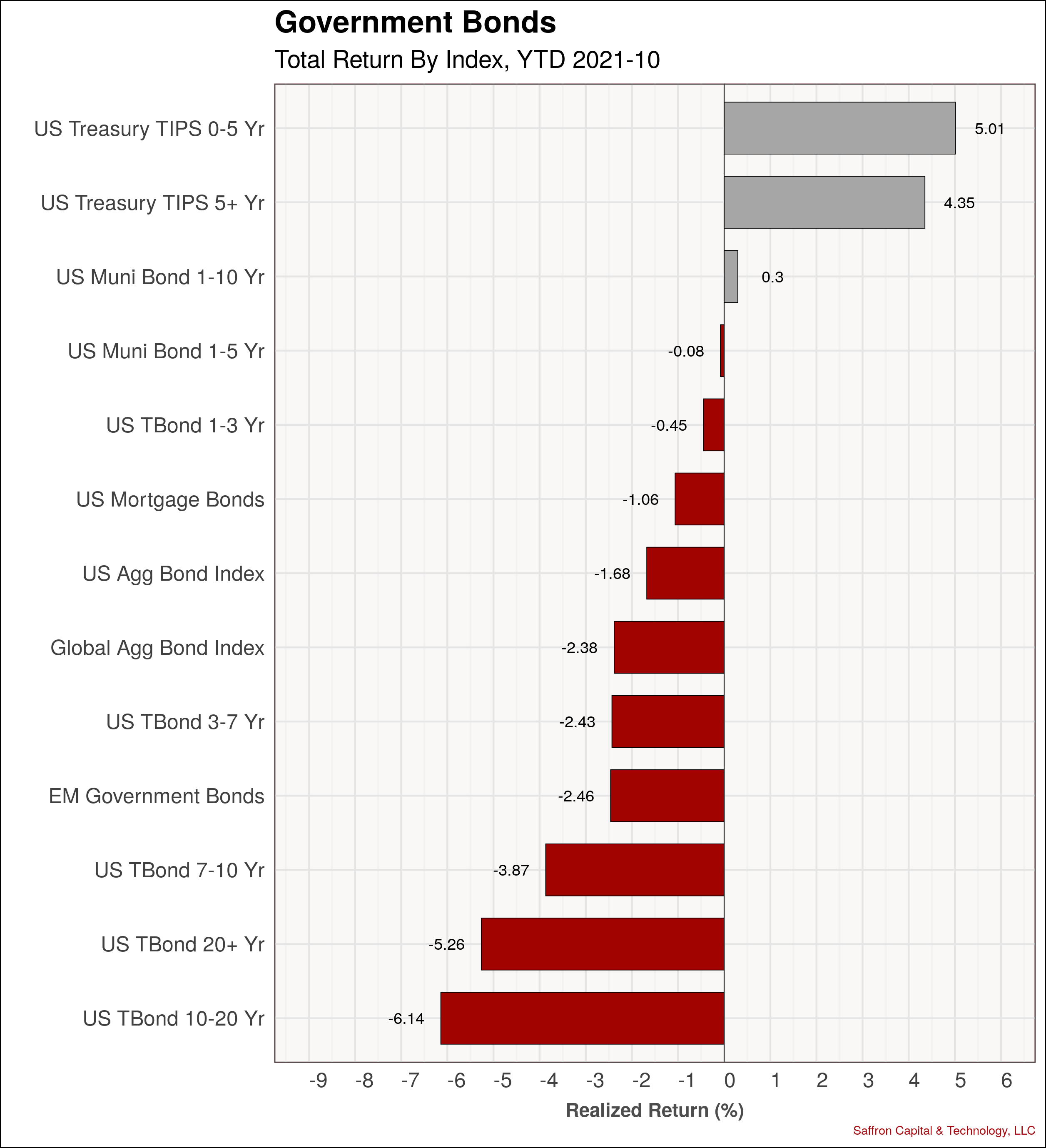

Government Bonds

Returns on US government bonds confirm that the yield curve flattened in October with long bond prices gaining and short bond pricess falling. Long-term inflation protected bonds continued to do well in the face of hot CPI numbers. Not surprisingly, inflation protected bonds continue to lead YTD performance returns.

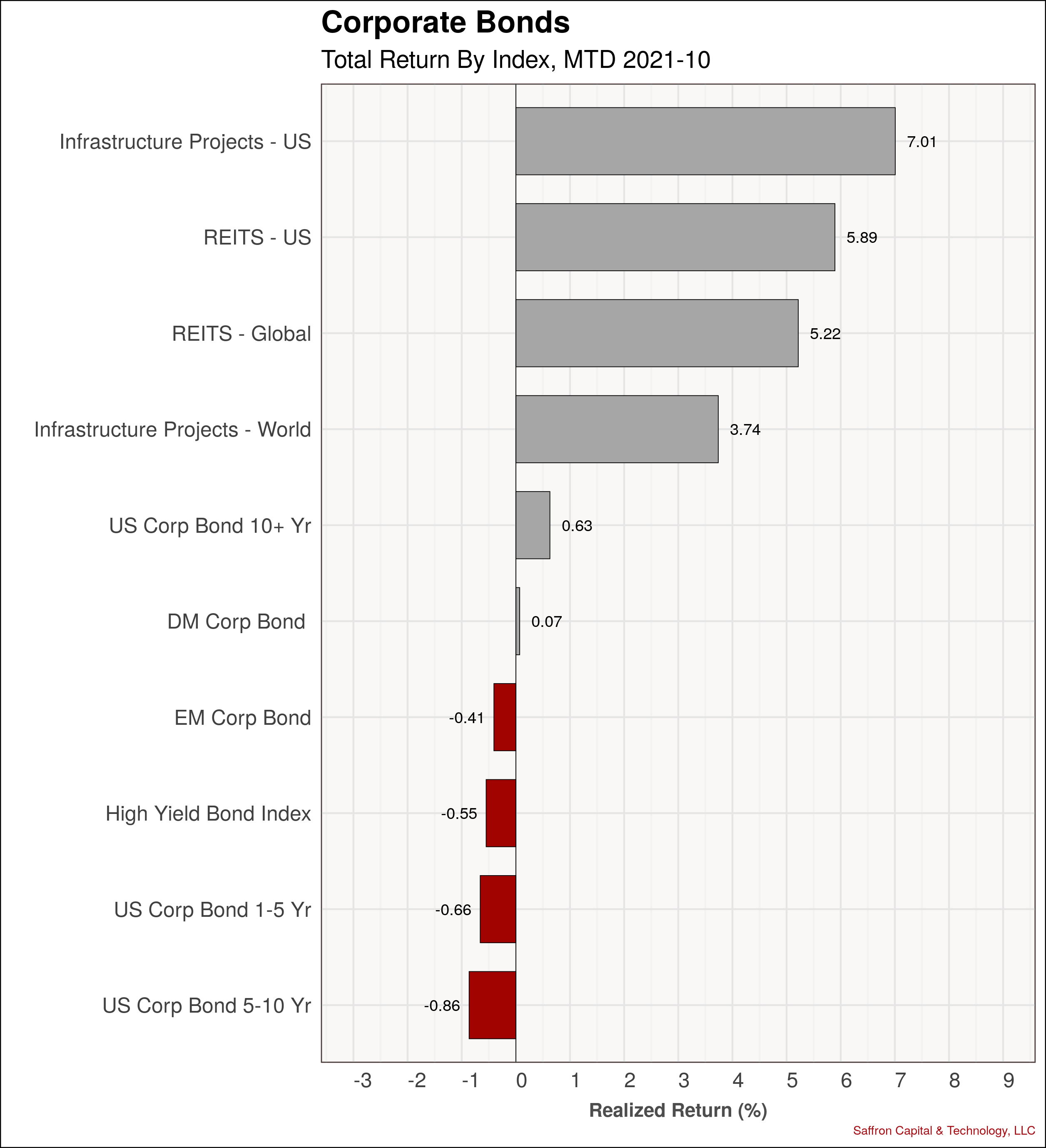

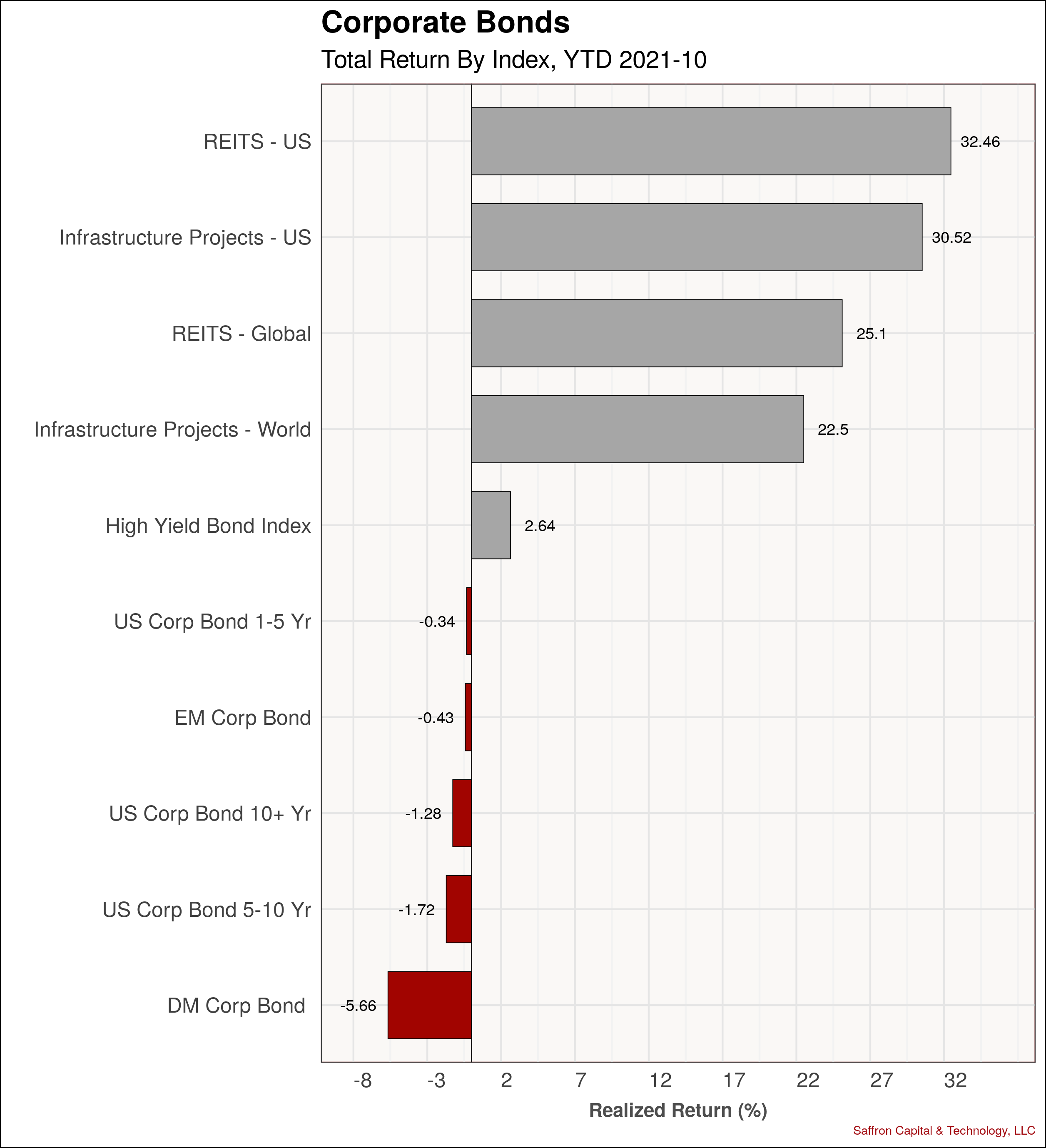

Corporate & Infrastructure Bonds

Infrastructure bonds and REITS kept pace with US stock market returns in October. At the same time, both asset classes continue to outperform US stocks on a YTD basis. For example, REITS are out-performing the S&P 500 by 800 basis points and infrastructure bonds by 600 basis points.

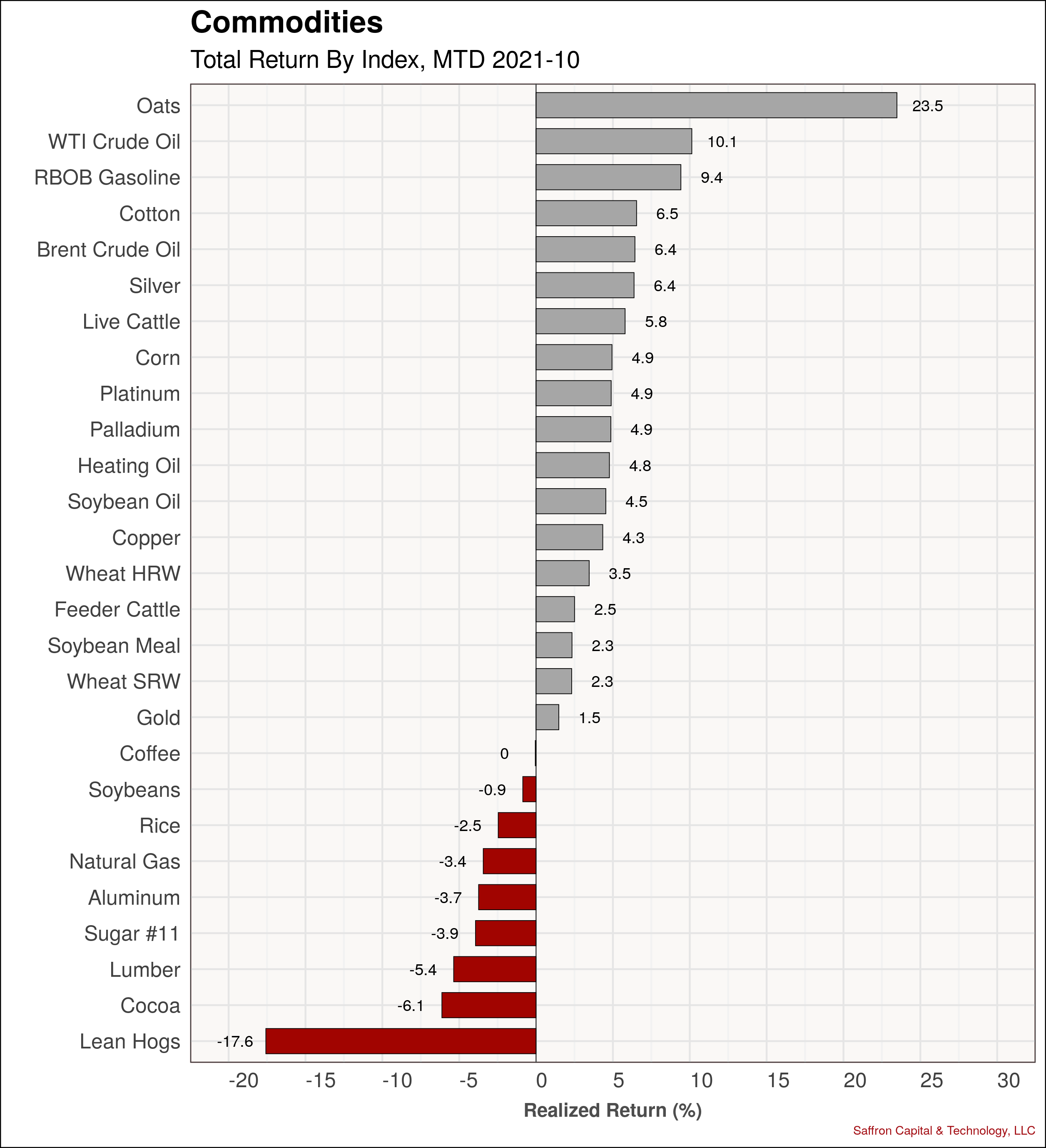

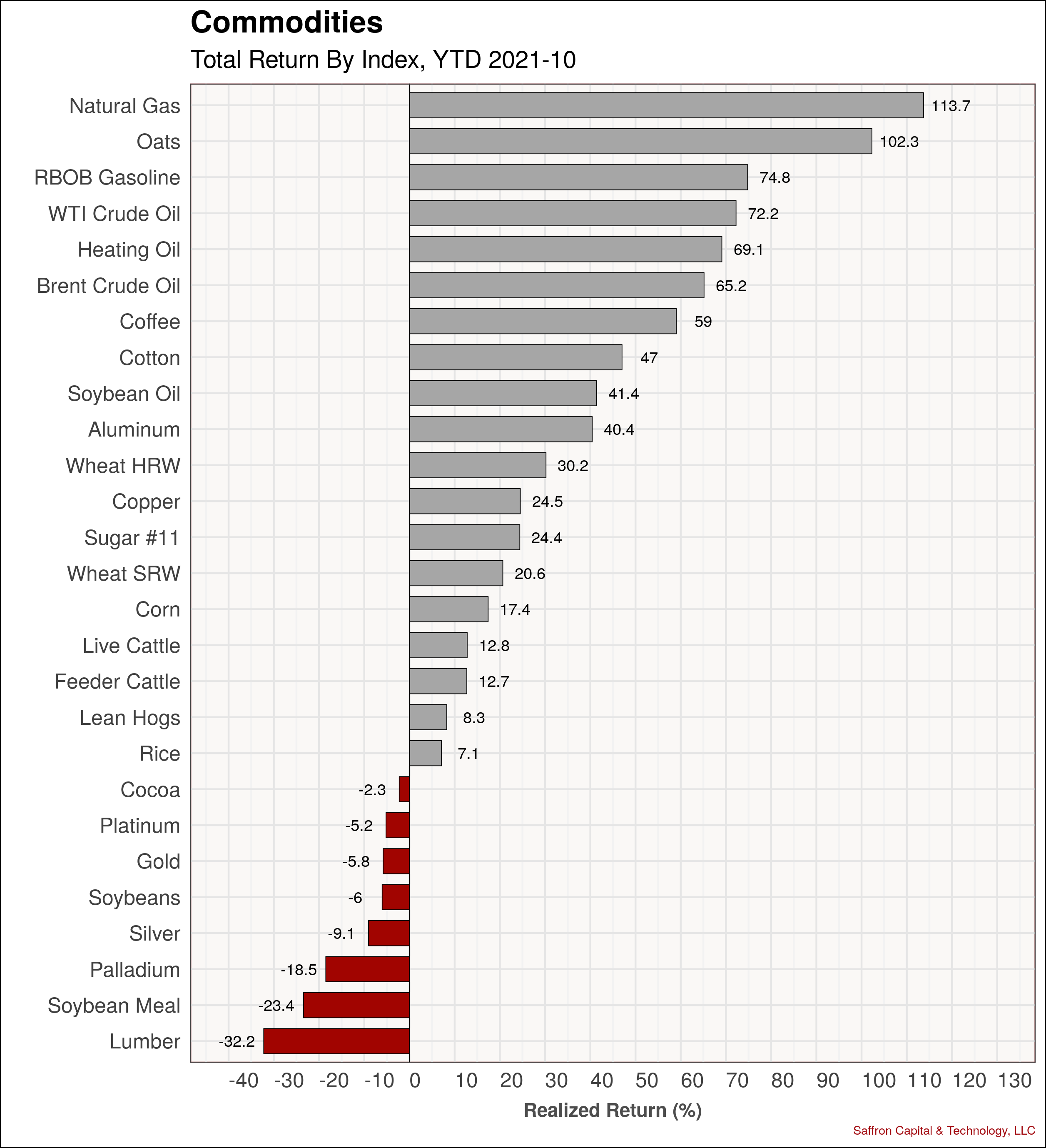

Commodities

Commodities continued to dominate asset returns in October lead by Oats, oil, gasoline and cotton. On the other hand, natural gas prices were down in October, though they still lead YTD performance. At this point, close to half the commodities tracked have put in better YTD performance than US equities, while gold, silver, soy products and lumber all have negative YTD returns.

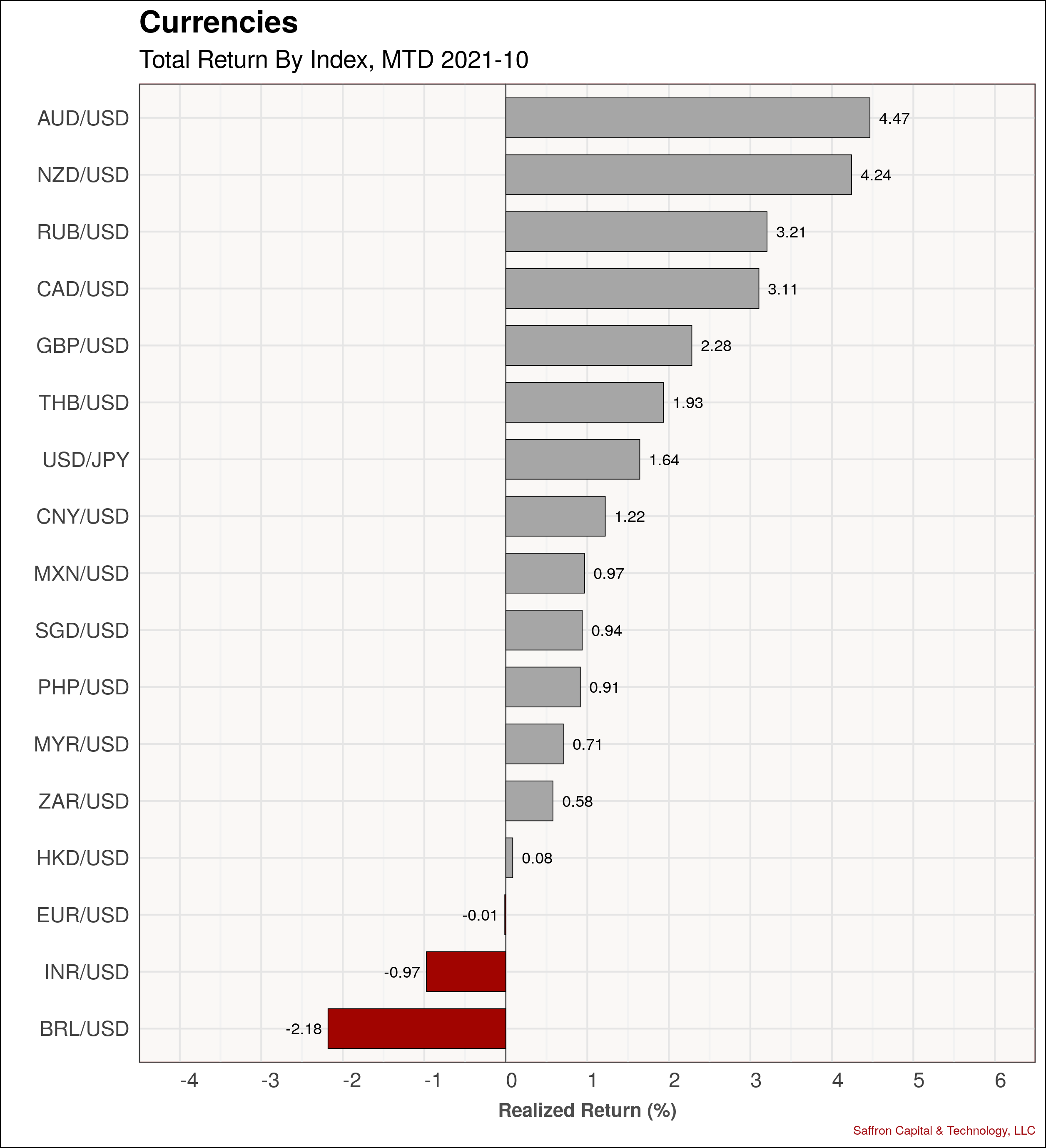

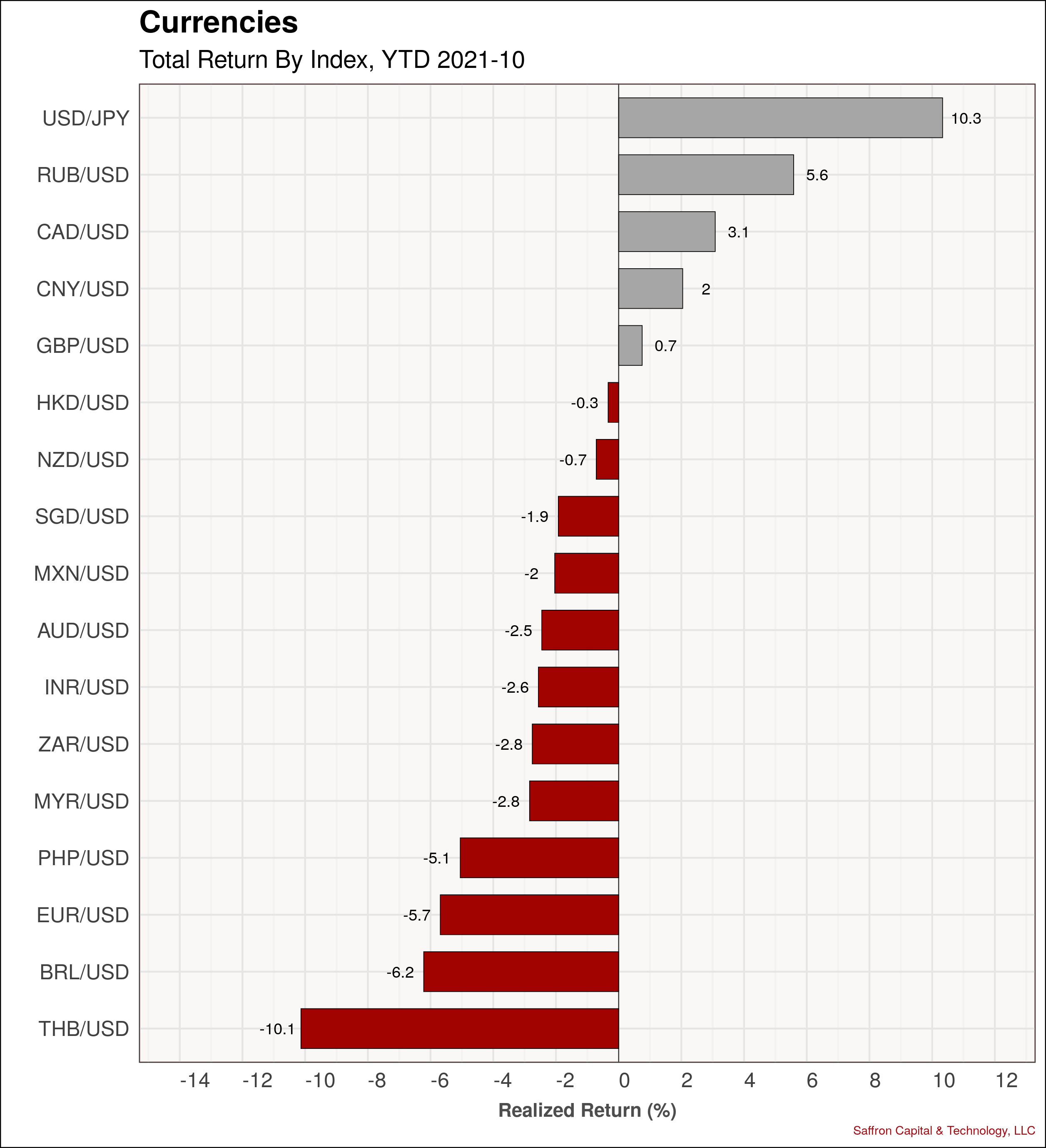

Currencies

Not surprisingly, the US Dollar was weak against most major currency pairs as yields moderated in October after strong gains in September. The Australian and New Zealand Dollars topped the charts in October, while the Indian Rupee and Brazilian Real were weak.

That’s it for October asset returns. If you have any comments or questions, you can contact me here.

{kind=link}

{kind=link}

{kind=link}